Mad Hedge Technology Letter

March 6, 2023

Fiat Lux

Featured Trade:

(DEALING WITH A BLACK BOX)

(TSLA), (UBER), (LYFT)

Mad Hedge Technology Letter

March 6, 2023

Fiat Lux

Featured Trade:

(DEALING WITH A BLACK BOX)

(TSLA), (UBER), (LYFT)

Who is responsible when artificial intelligence harms someone?

The California jury may soon have to make a decision. In December 2019, a man driving a Tesla (TSLA) with an AI navigation system killed two people in an accident. The driver faces up to 12 years in prison.

These events were bound to happen as teething pains are quite common with new technology especially one that is ambitious enough to transport machines in a human world.

Multiple federal agencies are investigating Tesla crashes, and The California Department of Motor Vehicles is investigating the use of AI-controlled driving functions.

Our current liability system, used to determine liability and compensation for injuries, is not AI-friendly.

Liability rules were designed for a time when humans caused most injuries.

But with AI, errors can occur without direct human intervention. The liability system must be adjusted accordingly. Poor accountability won't just stifle AI innovation. It will also harm patients and consumers.

It's time to start thinking about accountability as AI becomes ubiquitous but remains under-regulated. AI-based systems have already contributed to injuries.

The right accountability approach is critical to unlocking the potential of AI. Uncertain regulations and the prospect of costly litigation will deter investment, development, and deployment of AI in industries ranging from healthcare to autonomous vehicles.

Currently, liability claims typically begin and end with the person using the algorithm. Of course, if someone abuses the AI system or ignores its warnings, that person should be held accountable.

But AI errors are often not the user's fault. Who can blame an emergency doctor for letting an AI algorithm miss papilledema — a swelling of part of the retina?

AI's failure to detect the disease could delay care and potentially cause the patient to lose their eyesight. Papilledema is difficult to diagnose without an ophthalmologist.

AI is constantly self-learning, which means it takes in information and looks for patterns in it. This is a "black box" that makes it difficult to understand which variables affect the outcome.

The key is to ensure that everyone involved - users, developers, and everyone else in the chain - has been vetted to keep AI safe and effective.

First, insurers should protect policyholders from AI injury litigation costs by testing and validating new AI algorithms before deploying them.

Car insurers have also been comparing and testing cars for years. An independent security system can provide AI stakeholders with a predictable system of accountability that adapts to new technologies and practices.

Second, some AI errors should be challenged in courts that specialize in uncommon cases. These tribunals may specialize in particular technologies or topics.

Third, proper regulatory standards from federal agencies can offset the excessive liability of developers and users. For example, some forms of medical device liability have been superseded by federal regulations and laws. Regulators should focus on standard AI development processes early on.

Regulation can make or break AI in the upcoming years and I definitely lean towards the laissez faire attitude of deregulation.

Too many regulations will stifle the development and bring about undue costs.

No company will continue with loss-making operations unless they see a light at the end of the tunnel.

If allowed to develop with light regulation, AI will be that supercharger to tech stocks that investors dreamed of.

Transportation-based tech stocks such as Uber and Lyft will be one of the largest winners from the widespread implementation of driverless technology.

Also, throw in there the food delivery companies like DoorDash (DASH).

Another group with immense expense-saving possibilities is all the airlines around the world because theoretically, self-driving technology will become good enough to deploy in short and long-haul flights.

Getting to the point of consumers and regulators fully trusting self-driving technology is still a long and windy path, but I do believe we will arrive there.

When we do get there, the tech companies exposed to these great benefits will feel a 10X boost to their share price.

Mad Hedge Technology Letter

March 3, 2023

Fiat Lux

Featured Trade:

(THE PAPER REGULATOR IN WASHINGTON)

(FEDERAL STOCK BUYBACK TAX)

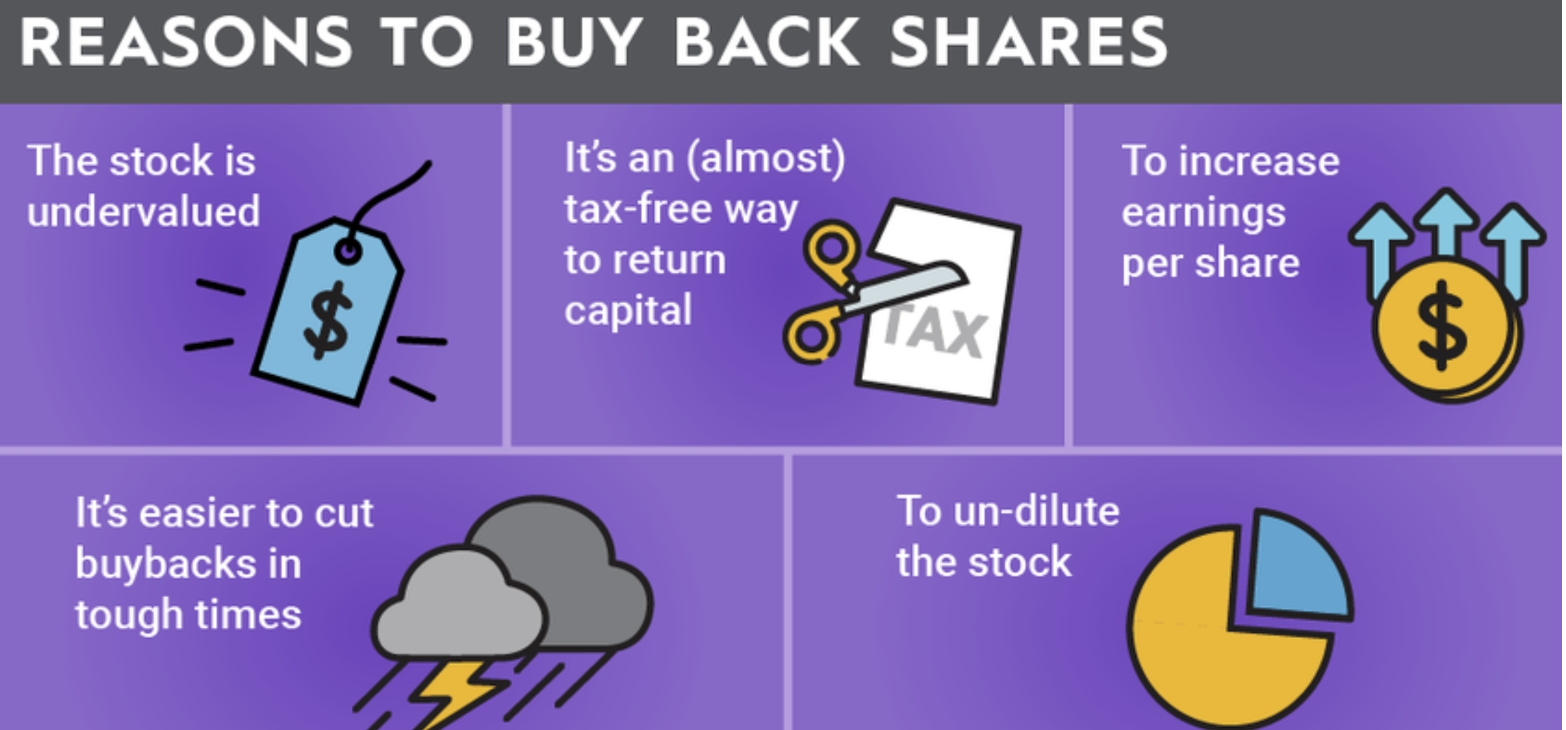

It’s a misnomer that this proposed stock buyback tax has teeth.

It offers easy loopholes to make it largely ineffective.

If management is smart enough – it’ll be a 0.

This is more or less a slam dunk for tech firms.

The Federal government is already too cozy with big tech to actually do anything that harms them, otherwise they would have removed Section 230, the law that doesn’t make corporations liable for content posted on their platform, a long time ago.

In fact, I would argue that the stock buyback tax in its current form will be good for tech companies because it offers the veneer of regulation without actually regulating big tech.

I’m referring to the new 1% excise tax on share repurchases that went into effect on Jan. 1, 2023.

This tax has caused some concern in some corners of Wall Street, based on the notion that buybacks were the biggest tailwinds supporting the past decade’s bull market — and anything weakening that advantage could lead to lower valuations.

Even more anti-stock market is the possibility that Ukrainian Supporter Joe Biden wants to ratchet up and quadruple federal taxes on US buybacks to 4%.

It’s all bark and no bite for Biden as usual.

This proposal is considered dead on arrival in Congress so it is convenient to just throw it out there to sound like he’s actually regulating when this thing has no chance of passing into law.

Virtue signaling has been a popular behavioral trait for US politicians for quite some time now.

So what is the loophole?

Foundationally, the new excise tax — whether 1% or 4% — is applied to NET buybacks — the key word being NET.

These are repurchases in excess of how many shares the corporation may have issued.

As has been widely reported for years, the shares that many companies are buying back often are barely enough to compensate for the new shares they issue as part of their compensation to company executives and top talent.

As a result, net repurchases — on which the new tax will be levied — are extremely less than gross repurchases.

There is much irony in the excise tax’s application to net repurchases.

Close your eyes when talking about some tech companies like data company Palantir (PLTR) who issue new stock as if it is going out of fashion.

There is so much new gross stock issued at PLTR that the stock is constantly mired in single digits.

Much of the stock issuance in the past has been diverted to the founders and executive management like Alex Carp and Peter Thiel who use this financial engineering tactic as their personal piggy banks.

In fact, a buyback tax based on a low stock price will incentivize founders and upper management to issue loads of new stock to cash out since they will need a higher volume of nominal stock to achieve whatever nominal amount is desired.

This leads to a situation where the stock buyback tax for net repurchases will never be applicable and will effectively always be 0%.

It’s precisely when share repurchases equal share issuance that the tax would not apply and if there is ever a remote possibility of happening, I can easily see management issuing whatever amount of stock to make sure the stock buyback tax always stays at 0.

Yet, that’s not all, I believe the stock buyback tax will promote higher dividends.

Up until now, the tax code provided an incentive for firms to repurchase shares rather than pay dividends when they wanted to return cash to shareholders.

Tech firms could absolutely return to delivering higher dividends to shareholders if share buybacks become too politically toxic.

This would be good news because, dollar for dollar, a higher dividend yield has more bullish consequences than a higher buyback yield.

In a largely copycat industry where if one strategy works, all notable companies pile into the same trend, we could see a renaissance of increasing dividend yields in tech companies.

Tech employees are also interested in these developments because many possess stock options.

The value of these stock options is tied to the price of the stock and recently, many of these employees are upset that once their stock options vest, they are cashing out with only half the amount compared to the peak of the Nasdaq index in November 2021.

Tech continues to be the least regulated industry in the US and as tech investors, let’s hope it stays that way.

This stock buyback tax plan has more holes in it than a piece of Swiss cheese, which is why it has done nothing to slow down share repurchases in the first 3 months of 2023.

It’s just more of the Federal government being a paper regulator and not a real one.

“I think everybody understands how important the cloud is.” – Said CEO of Salesforce Marc Benioff

Mad Hedge Technology Letter

March 1, 2023

Fiat Lux

Featured Trade:

(THE VISION FUND LACKING VISION)

(WE), (SOFTBANK), (VISION FUND)

The most painful place to be in tech these days is where the venture capitalists used to make their name.

Private startups used to be glamorized, and now nobody wants to touch them with even a 10-foot pole.

VCs are the capital-rich guys who used to buy companies privately, hold onto them until they grew 10X, and then dish them off to the public once they went ex-growth.

That playbook was the surefire way to capitalize from companies during their highest growth phase.

Softbank’s Vision Fund was the poster boy for this strategy as the founder of Softbank Masayoshi Son deployed gargantuan resources from his Japanese telecom company (mostly in the form of debt) to pour into private tech firms.

Now, The Vision Fund has basically blown up as ideas like throwing $300 million at a dog walking app haven’t resulted in higher valuations from ludicrous types of aggressive investments.

Markets can behave irrationally for a while, but sooner or later, it regresses back to reality.

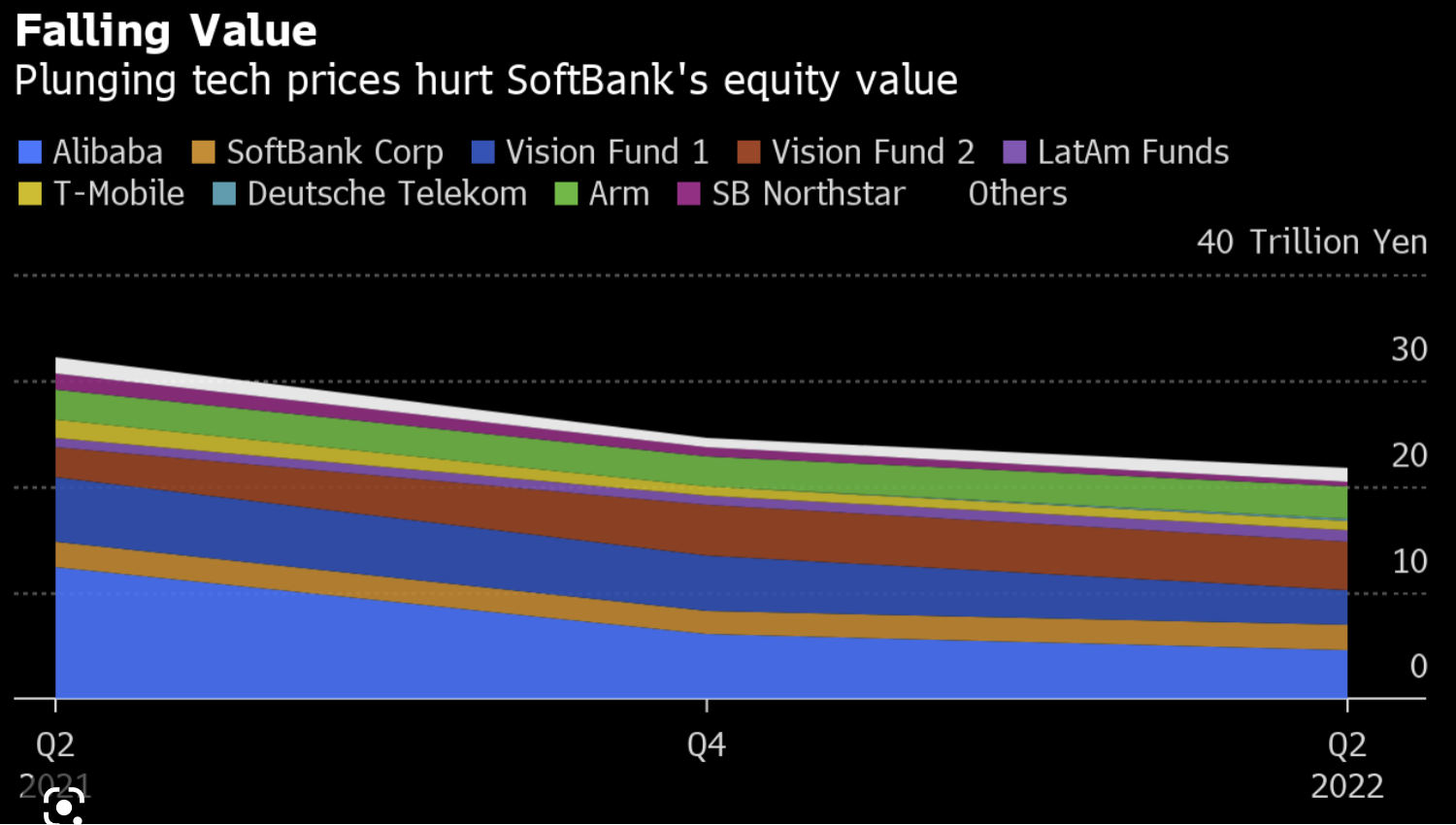

In the end, the world’s most brazen tech investor, Softbank, wasted billions helping to artificially lift tech valuations, only to see them plunge and lose their own money along with other adjacent investors.

In some cases like the office sub-let company WeWork (WE), they were the only investors to value assets at such lofty valuations. In WeWork’s case, they valued the company at $48 billion at its peak, and at the time of this writing, WE has a valuation of $920 million after finally going public.

So it’s not a surprise to see WE’s experience highlighting a broader failure of epic underperformance from Softbank with a decline in value for 73% of its 472 investments from an expert boutique firm that apparently is on the pulse of every new tech trend.

They would have done better with a monkey throwing darts at a dart board.

To address the headwinds, they are drastically reducing investment for the time being because they are tired of being wrong.

For the October to December quarter, SoftBank reported an investment loss of ¥731.94bn ($5.5bn), compared with a ¥1.38tn loss in the previous quarter for its two Vision Funds and a fund investing in start-ups in Latin America.

As of the end of December, SoftBank said the fair value of the $100bn Vision Fund I was down 4.4% from a year earlier due to markdowns in privately held companies despite gains in some listed holdings, such as ride-hailing groups Didi and Grab. The valuation for investments in Vision Fund II was down 6.2%

Son announced last year that he would step back from day-to-day operations to basically get out of the way of himself.

I applaud him for doing that because many arrogant leaders don’t understand when their time is up.

The private markets aren’t what they used to be and the deal breaker is higher rates.

This part of tech won’t come back until cheap money floods visionary ideas because these ideas are usually risky and most attempts become a zero.

Tech stocks will continue to be choppy in the meantime and continue to represent ideal trader markets for investors to jump in and out of tech stocks.

It’s natural for a reversion to the mean after a blistering January and big moves up and down will be the likely story in this stock pickers market for 2023.

However, the time for those 10Xers from VCs is dead until further notice.

Mad Hedge Technology Letter

February 27, 2023

Fiat Lux

Featured Trade:

(THE UNBEATABLE PARTNERSHIP)

(EMR), (GRMN), (AMBA), (NVDA), (DXCM), (CSCO), (INTC), (QCOM)

Let me introduce to you one of the hottest trends in tech.

They have been on the tip of everyone's lips for years, and that might be an understatement, but the interaction of the internet of things (IoT) and artificial intelligence (AI) offers companies a wide range of advantages.

In order to get the most out of IoT systems and to be able to interpret data, the symbiosis with AI is almost a must.

If the Internet of Things is merged with data analysis based on artificial intelligence, this is referred to as AIoT.

Moving forward, expect this to be the hot new phrase in an industry backdrop where investors love these hot catchphrases and monikers.

What is this used for?

Lower operating costs, shorter response times through automated processes, and helpful insights for business development are just a few of the notable advantages of the Internet of Things.

AI also offers a variety of business benefits: it reduces errors, automates tasks, and supports relevant business decisions. Machine learning as a sub-area of AI also ensures that models – such as neural networks – are adapted to data. Based on the models, predictions and decisions can be made. For example, if sensors deliver new data, they can be integrated into the existing modules.

The Statista research institute assumes that there will be 75 billion networked devices by 2025.

This is exactly where AI comes into play, which generates predictions based on the sensor values received.

However, many companies are still unable to properly benefit from the potential of connecting IoT and AI, or AIoT for short.

They are often skeptical about outsourcing their data - especially in terms of security and communication.

In part because the increased number of networked devices, which requires the connection of IoT and AI, increases the security requirements for infrastructure and communication structure enormously.

It is not surprising that companies are unsettled: Industrial infrastructures have grown historically due to constantly increasing requirements and present companies with completely new challenges, which manifest themselves, for example, in an increasing number of networked devices. With the combination of IoT and AI, many companies are venturing into relatively new territory.

By connecting IoT and AI, a continuous cycle of data collection and analysis is developing.

But companies can no longer deny the advantages of AIoT because this technical combination makes networked devices and objects even more useful.

Based on the insights generated by the models, those responsible can make decisions more easily and reliably predict future events. In this way, a continuous cycle of data collection and analysis develops. With predictive maintenance, for example, production companies can forecast device failures and thus prevent them.

The combination of the two technologies also makes sense from the safety point of view: continuous monitoring and pattern recognition help to identify failure probabilities and possible malfunctions at an early stage – potential gateways can thus be better identified and closed in good time.

The result: companies optimize their processes, avoid costly machine failures, and at the same time reduce maintenance costs and thus increase their operational efficiency.

In this way, IoT and AI represent a profitable fusion: While AI increases the benefit of existing IoT solutions, AI needs IoT data in order to be able to draw any conclusions at all.

AIoT is therefore a real gain for companies of all sizes. They thus optimize processes, are less prone to errors, improve their products and thus ensure their competitiveness in the long term.

Some hardware, software, and semiconductor stocks that will offer exposure into AIoT are Emerson Electric Co. (EMR), Garmin (GRMN), Ambarella (AMBA), Nvidia (NVDA), DexCom (DXCM), Cisco (CSCO), Intel (INTC), and Qualcomm (QCOM).