"Complete independence means independence and freedom in every field such as politics, economics, judiciary, military, culture… Insufficiency in one of those fields means the total loss of independence of the nation." – Former President of Türkiye Mustafa Kemal Atatürk

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/warren-buffett.png540450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-15 15:00:322023-02-15 16:27:40Quote of the Day - February 15, 2023

American ecommerce companies are certainly feeling the pinch of high inflation as many US consumers tighten up their purse strings.

Ecommerce was one of the few growth engines for tech before 2020, now it’s harder to move the needle for many subsectors.

Just take a look at the giant ecommerce company Amazon (AMZN) whose stock price was higher in August 2018 compared to today.

Between now and 2018, Amazon experienced a pulsating melt-up due to a business boom, low interest rates, and positive global growth.

On the way down, the reverse has taken place.

We, as investors, just cannot assume tech will go from the bottom left to the top right anymore.

So if ecommerce companies of Amazon’s ilk are struggling to navigate tighter conditions, imagine how bad it is for ecommerce flagship companies in an Asian third-world backwater like South Korea.

The ecommerce company I am talking about is Coupang (CPNG), which I’ve been highly negative of since public inception, and rightly so.

CPNG's share price has done nothing but drop since its IPO from its $50 peak and now stands at $15 after bottoming out at $9.

What next for CPNG?

CPNG the South Korean e-commerce pioneer has lost billions of dollars since its inception but is rolling out an army of robots at fulfillment centers in the hope of achieving profitability.

They burned cash by building distribution centers throughout South Korea that could help it push the boundaries of speedy delivery with a broad selection.

Now the company is almost breaking even, with analysts projecting it will turn a profit for the second straight quarter and then report its first annual operating profit in 2023.

Coupang has used private venture capital to fund this expansion combined with a 2021 initial public offering to build logistics domestically.

Coupang is also pushing to expand new markets in Taiwan and Japan. I see that as a hard endeavor because legacy ecommerce like Rakuten is quite entrenched there.

I think they will be unable to outmaneuver local competition.

Strategies like cash burning to seize market share don’t work anymore because of the high cost of capital.

CPNG needs to optimize what it can in South Korea even if the country presides over one of the worst demographics in the world, with the average age of customers approaching the age of nursing home residents.

CPNG has more than 100 fulfillment and logistics centers in South Korea, but no footprint overseas.

Barreling into mature markets is a marginal strategy for CPNG today because they are 10 years too late.

Yet, I do really like what they are doing on the automation front domestically integrating automated robots into their operation.

The lack of workers and consumers in South Korea is another headwind due to poor demographics.

Externally, they also face various headwinds from the global backdrop souring.

I do believe in the short term as tech equities benefit from the disinflation narrative, there is a narrow path to a higher market share for CPNG to around $25 per share in 2023.

Anything higher I would avoid because it’s not worth paying a premium for this ecommerce company.

Relying on a “tide lift all boats” strategy is not ideal in today’s tech world, because that isn’t for sure anymore.

Long term, my assessment of CPNG is less rosy. This could be a good buyout ticket for a bigger fish because, at some point, they will realize that they were late to the party and might as well sell it off for whatever it's worth.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/help-wanted.png7801556Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-13 15:02:242023-02-19 22:22:55Ecommerce Takes A Back Seat

“Price is what you pay, value is what you get.” – Said Legendary American Investor Warren Buffett

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/warren-buffett.png540450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-13 15:00:062023-02-13 16:19:45Quote of the Day - February 13, 2023

That’s where we are at and that’s what we face as tech stocks need to overcome the “no landing” scenario to see better days in valuation.

There has been much chit-chat about what sort of recession the US economy will face in 2023.

Well, hold your horses there mister.

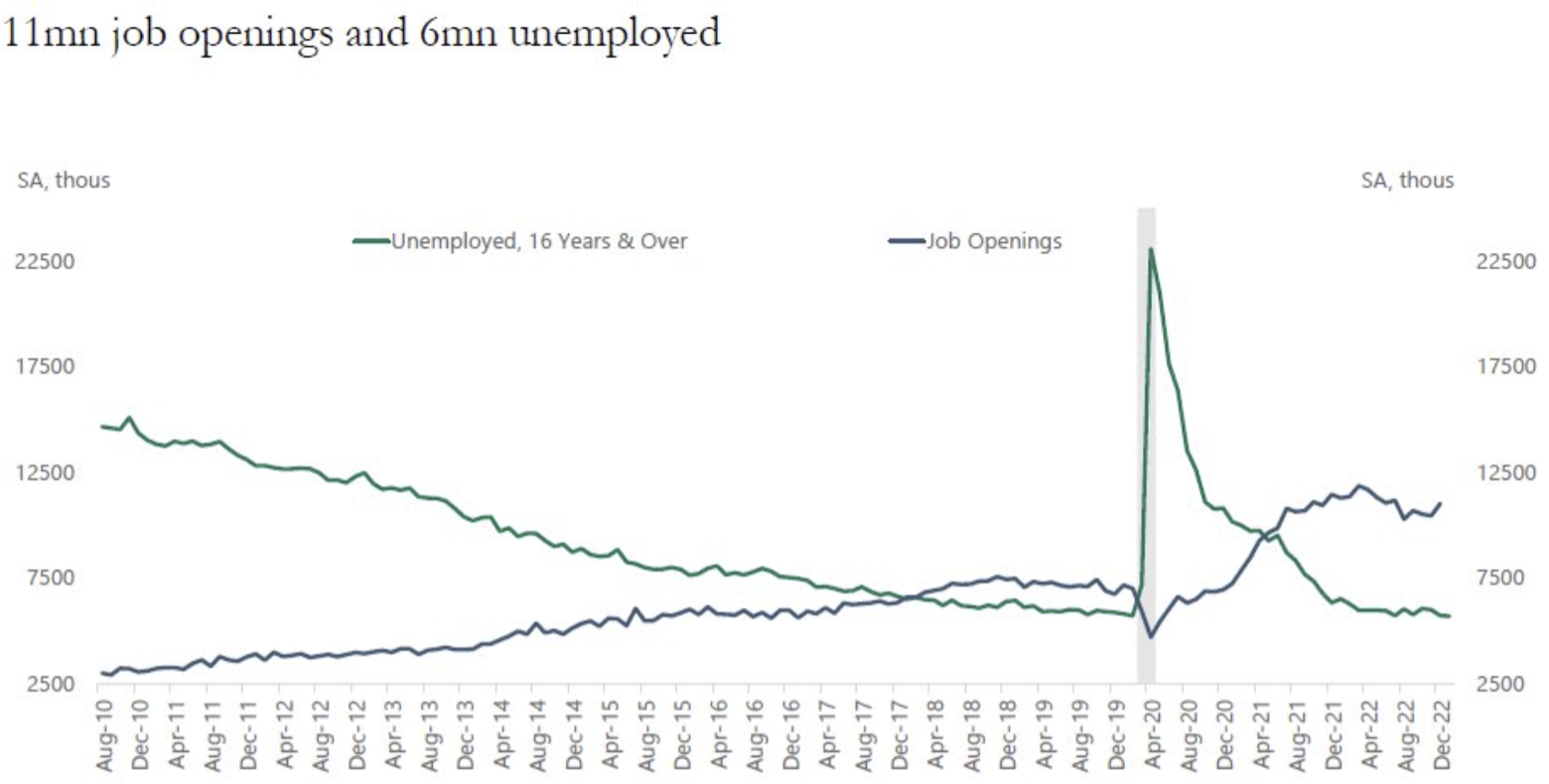

The smattering of positive labor data means there might not be a recession at all, which translates into neither a soft landing nor a hand landing for the economy.

Why does that matter for tech stocks?

The lack of light or deep recession has absolutely everything to do with inflation. High inflation kills growth stocks!

The logic behind this goes that if there is no recession, US workers will by and large keep their jobs.

From a societal point of view, this is great for Americans who can bank their salaries and spend, spend, spend.

However, this doesn’t work out so great if the stock market needs lower inflation for tech shares to go higher.

Let me just insert here that I am totally aware of all the tech job losses and they have topped around 200,000 so far and it’s a drop in the bucket to overall hiring and firing.

Interestingly enough, tech layoffs haven’t always resulted in the fired getting better jobs.

The jobs report shows a massive uptick in hiring particularly for restaurant jobs, retail, and hospitality.

Many of these are also part-time jobs which means the median US job is decreasing in quality and stability.

The result of more hiring for longer is that the US Central Bank might be forced to jack up rates again past the 5% that is priced in.

This is horrible news for the tech sector as the Nasdaq got off to a blistering start in January because of the clear path to lower inflation. This path is starting to close.

Last Friday’s January employment report saw the economy add a much stronger-than-expected 517,000 jobs, while the unemployment rate fell to 3.4%, its lowest level since 1969.

And if the services sector needs to fill hundreds of thousands of jobs, wage gains will threaten to make inflation spike yet again.

The reopening of China’s economy as reverses lockdowns could push commodity prices back to the upside, also contributing to price pressures after several months of slowing inflation readings.

The Fed has always pinpointed strong wage growth and full employment as an impediment to lowering rates.

I have banged on constantly that the Fed hasn’t done enough with lifting rates even though the pace of rate hikes has been historic.

Readers should remember that the amount of stimulus and handouts during the lockdowns were also historic as well.

Demand destruction simply will not occur if real rates are negative and that’s been the case for quite a while I might add.

Now there is a real risk of inflation reaccelerating because the Fed never raised rates high enough for companies to feel pain and fire employees.

This is why tech stocks have been swooning the last few days and the trading environment is still highly complex.

Expect whipsaws for the foreseeable future and if inflation does come back reincarnated, expect a page out of the 2022 playbook with stocks and bonds going decisively lower.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/help-wanted.png7801556Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-10 15:02:132023-03-01 20:48:43No Landing Outcome For Tech Stocks

Down 8% on a faulty chatbot conversation – that’s what happened to Google’s (GOOGL) stock today.

That’s why we need to pare back the euphoria and nonstop celebration of ChatGPT.

Hold your horses.

It’s an emerging technology and could end up with chatbots chatting with other chatbots for little or no value.

My point is that it can still go very wrong from here.

Google’s stock swan dived on Wednesday after its own iteration of A.I. chatbot erroneously answered a question about the first usage of space telescopes via its promotional material.

It all lends itself to surmise that Google is way behind in this game and Microsoft has the situation by the scruff of the neck.

Only just a few days ago, Microsoft integrated the AI technology into the front page of its Bing search engine, and is available for user downloads on the Bing app.

The drop in share price meant that Google lost more than $100 billion off its market cap.

The service called Bard is to compete with the popular ChatGPT.

Despite the chatbot’s claim in the ad, NASA reports that the first photo of a planet outside the Milky Way was taken by the Very Large Telescope in 2004 — nearly 19 years before NASA’s Webb telescope.

Unpreparedness by Google could translate into a significant loss of ad revenue for Google’s cash cow Google search.

The desperation of throwing Bard out there not on their timeline could mean they are exposing a product that isn’t up to Google’s standards.

An AI chatbot that consistently delivers false answers will turn off an advertiser quicker than no AI chatbot.

Investing in Google is still worth it even if it takes time to correct the quality of their AI. because it is logical to give a good company the benefit of the doubt.

Another problem is that Google could be stuck with bad AI for a few years before it turns the corner.

For better or worse, they were forced to go public with whatever they had just for the optics of competition even if they are badly lagging behind.

The worst-case scenario is receiving a direct blow to the cranium in terms of total ad revenue.

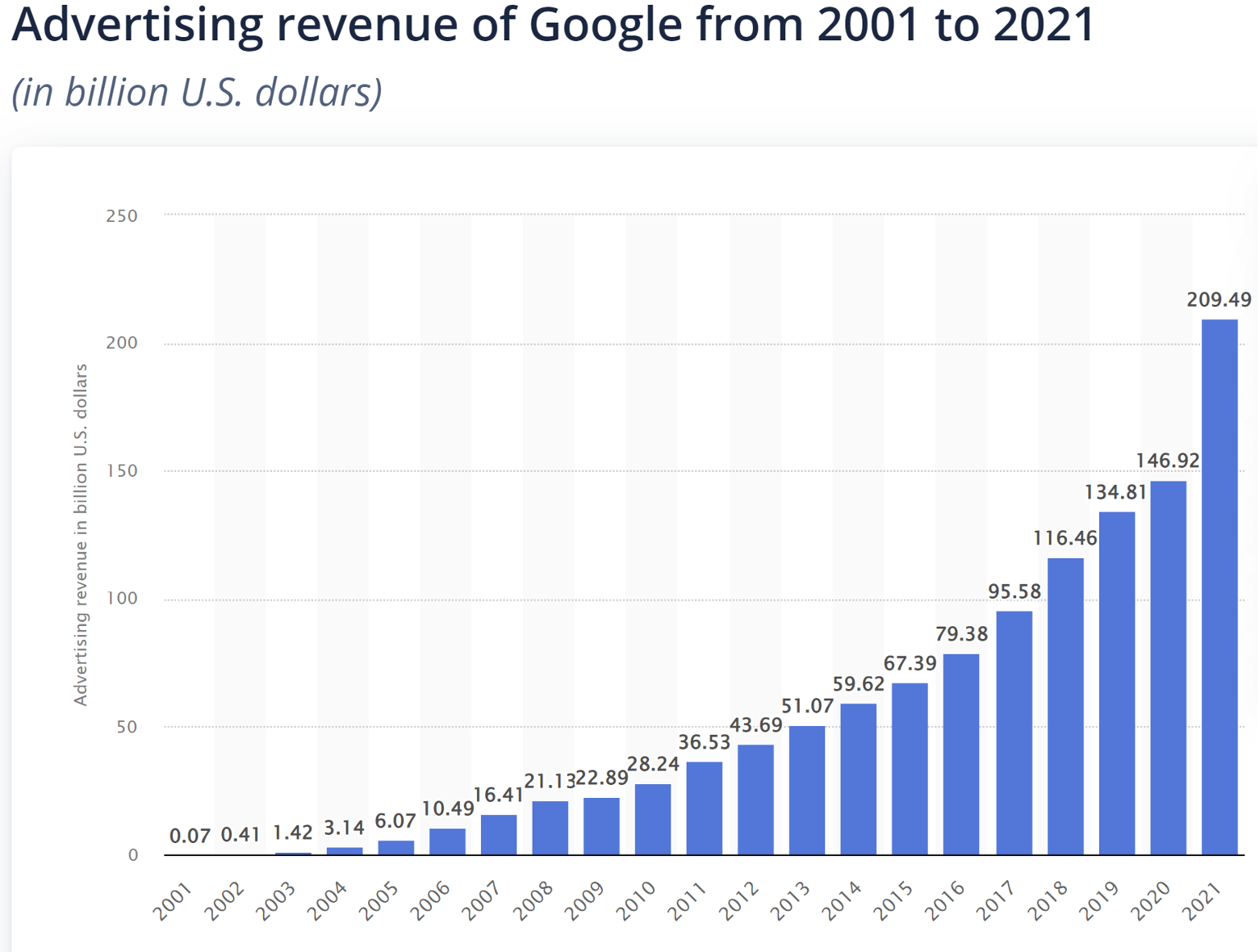

Google is still relying on search to drive the rest of its business.

They earned over $200 billion in ad revenue in 2021.

This is the first threat to Google’s search model in a generation and the threat has them on their toes.

I do believe they possess the resources to solve this issue.

No doubt that Google CEO Sundar Pichai is throwing the kitchen sink to find and poach the best AI engineers to beef up the chatbot team.

Ultimately, the real new world of higher interest rates and high inflation environment means that your father’s tech playbook must be thrown out the window.

It’s quite evident that we are in the midst of a paradigm shift and new leaders during this shift will emerge.

History shows us that tech leaders of old have a habit of falling behind because they are too set in their ways to adapt to a world with new rules.

It might be so that at some point in the not-so-near future, we might need to set the search default to Bing.

How ironic?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-08 15:02:442023-03-01 21:46:30Chatbots Sink Stock 8%

“Bad times are incredibly good for Palantir.” – Said CEO of Palantir Alex Karp

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/alex-karp.png803440Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-08 15:00:412023-02-08 23:48:20Quote of the Day - February 8, 2023

Mad Hedge Technology Letter

February 6, 2023 Fiat Lux

Featured Trade:

(PLATOONING AND TECH IS A MATCH MADE IN HEAVEN) (ODFL), (CVLG), (ARCB), (ULH), (SNDR), (WERN)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-06 17:04:292023-02-06 18:06:14February 6, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.