Mad Hedge Technology Letter

November 18, 2022

Fiat Lux

Featured Trade:

(THE LUCK OF SILICON VALLEY)

(TWITTER)

Mad Hedge Technology Letter

November 18, 2022

Fiat Lux

Featured Trade:

(THE LUCK OF SILICON VALLEY)

(TWITTER)

Elon Musk sends people to outer space; I’m confident he can figure out how to run a simple app run by juveniles.

Let’s talk about the most controversial tech company out there right now, Twitter, and a tech firm that sets the tone for the rest of the industry.

Twitter has undergone an extreme makeover lately.

Not the product, but the staff.

Musk started off by firing half the staff, which later turned into an ultimatum for the rest to either get on board with the new Twitter or accept 3 months’ severance pay out the exit door.

Many left.

Cutting staff was rejuvenating, maybe not for the employees who were let go, but for a dire need of a mentality change.

Twitter became too corporate and too political inside its office.

Most of the former Twitter staff was utterly useless.

The 10% leftover is really what is essential and like Musk said, he was able to hang on to the “best people.”

Next, he should cut the office space to increase efficiencies or at the very minimum renegotiate the office lease to downsize the square footage by 90%. San Francisco city center is a ghost town now – a relic of its former self.

Twitter’s big layoff will also act as a feeder strategy for the rest of Silicon Valley to push staff into a leaner and more efficient model.

In a way, Musk is saving the technology sector by offering the blueprint of how to manage a software company.

Silicon Valley needs to fire 90% of staff immediately, maybe even 95%.

Elon Musk noted that Twitter was paying an average of $400 per lunch at the Twitter headquarters in San Francisco.

I know San Francisco is expensive and almost unlivable, but this was the type of extreme activity that was allowed to happen under the past management whose main job was to wait for their monthly paycheck.

It’s no wonder that shareholders were getting screwed.

Although it’s quite fashionable to jump on the Musk hate wagon lately to say how Twitter will go down in flames, I don’t think it’s justified and it appears to be more about sour grapes because many don’t like Musk’s politics.

Ruthlessly cutting costs is a great tactic for tech executives. Costs are way too high, which is why Facebook let go of 11,000 workers last week.

Amazon just announced 10,000 firings too, and I think they could handle 50,000 firings easily.

Luckily, positions like Chief Diversity Officer, Chief Ethics Officer, and the managers of middle managers need no replacements at all.

Musk noted that Twitter is losing $4 million per day and these measures will go a long way to fixing that.

He’s smart enough to find solutions and I wouldn’t bet against him. I can already visualize him picking apart the best slices of Twitter and supercharging them.

Twitter is a premium asset with unlimited scarcity value. We are just scratching the surface with it.

Where is the end game?

I wouldn’t be surprised if Twitter went public in 5-7 years with a valuation of $150 billion after Musk unlocks the embedded value that is literally everywhere on Twitter.

I would say $150 billion is lowballing him and this company will be worth between $180 billion- $220 billion in the next 7-10 years.

Many people still don’t understand Twitter very well and it’s become even more important than the mainstream media.

“Build something 100 people love, not something 1 million people kind of like.” – Said Co-Founder and CEO of Airbnb Brian Chesky

Mad Hedge Technology Letter

November 16, 2022

Fiat Lux

Featured Trade:

(CONTENT IS KING)

(AMZN), (GOOGL), (AAPL)

It’s the death of websites.

I love doing presentations to small businesses in my free time, partly to stay in touch with the pulse of the industry’s minnows that have the unenviable task of fighting uphill against the behemoths.

It’s bad enough that the tech giants have scaled locally turning one’s local playground into a disadvantage.

The presentation is aptly titled "Content is King... But Only Through One’s Ownership" where the same parallels are explored and unpacked for my audience.

Proprietary Content – must be yours and you must own it on your own turf - your blog, your vlog, your app, and so on, it goes for everything.

Repurposing content on other platforms as a supplement to your own is one thing, but the moment you adopt an enemy platform as your main platform, that’s your coup de grâce.

SMEs (small businesses enterprise) believe it’s plausible to work with the higher-ups, but don’t forget the higher-ups have every incentive to cut you off from the fountain of youth.

One could say the best skill big tech has today is undermining its competition.

Facebook doesn’t allow posting content that criticizes Facebook, have you ever wondered why?

Website innovation has ground to a halt because of the PageRank algorithm from Google - everybody is making websites the same, a top nav, descriptive text, a smattering of images, and a handful of other elements arranged similarly.

Google’s algorithms and the self-regulating nature of its ecosystem have perverted the chance to have a unique online experience.

Most internet users have discovered that most websites don’t work well and the execution is lousy.

Silicon Valley now has a monopoly on websites.

Because websites are the key to building businesses, Silicon Valley is now using the concept of websites and their position as de-facto moderators to prevent others from developing proper websites, killing off the competition.

Alphabet is notorious for ranking in-house products at the top of page one of any Google search.

Amazon has followed the same practice by sticking its in-house brands at the top of any Amazon search on Amazon.com.

Websites are used to give businesses a chance.

What’s next?

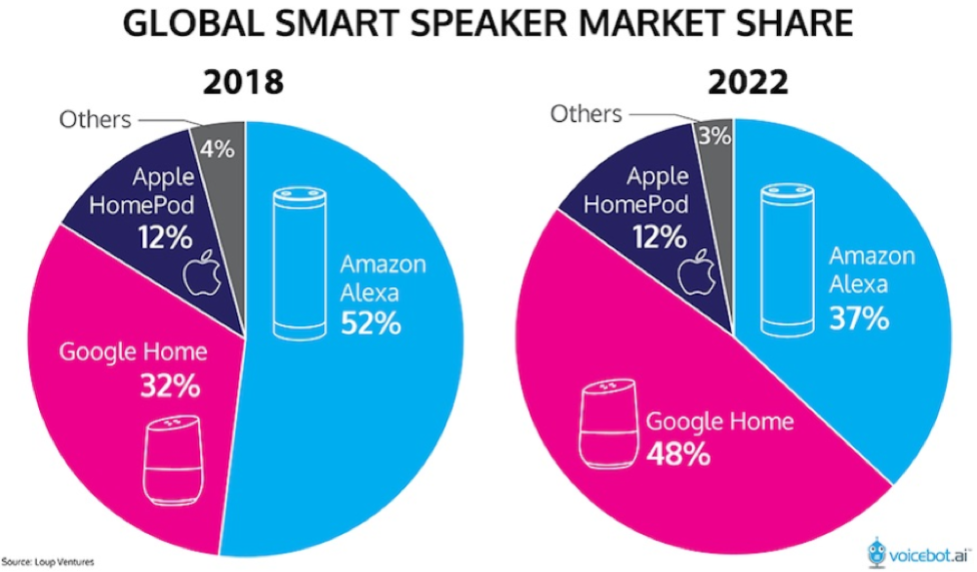

Once we migrate the lion’s share of content to voice platforms over the next 15 years, Google Home, Apple HomePod, or Amazon Alexa could easily choose to remove Joe’s Furniture Moving Business information because they aren’t following arbitrary “policies.”

Big tech will be the gatekeepers of all global information, business, and development in the world and we will need to satisfy their algorithms to get our own content uploaded on their voice platforms.

And because of the nature of voice, users cannot see what else is out there, users will only hear what these companies tell us offering an outsized opportunity to manipulate the user experience generating more dollars for these powerful platforms.

As we inch towards the day the US Central Bank will drop the Federal Funds rate, minus Facebook, readers must load up the truck and pile into these monopolistic tech stocks.

“If you are a big company, a big website, and lots of users come to your website, you will have attacks, and you have to deal with that.” – Said Founder and CEO of Baidu Robin Li

Mad Hedge Technology Letter

November 14, 2022

Fiat Lux

Featured Trade:

(LOW BAR HAS BEEN SET)

(COIN), (HOOD), (MSTR)

It’s been a historic and unprecedented last few weeks in the world of technology.

99.9% of crypto projects are effectively a zero after this weekend.

Cryptocurrency has now descended into a death spiral due to a fraud so large that it makes many who got caught up in the mess sick to their stomach.

This “trigger” event has massive ramifications for the technology industry and is highly positive for the health of the tech sector.

Enter Former CEO of FTX, the former second biggest crypto exchange, Sam Bankman-Fried or SBF.

His crypto exchange FTX filed for bankruptcy just days ago.

SBF was stealing customer deposits to invest in his lifestyle and bought off everyone he thought was useful, including politicians, regulators, sports athletes, and famous actors.

SBF even bailed out many crypto-related companies during the recent downturn that were confirmed Ponzi schemes or frauds just to onboard them onto an even bigger scam.

In the end, a bank run collapsed SBF’s crypto empire and exchange.

It was only after the house was on fire that normal investors found out that his business was rotten to the core.

How did SBF hide this?

FTX and SBF literally replaced these funds on their balance sheet with their own in-house crypto coin that was produced and created by FTX.

This self-made coin was called FTT and FTT represented $7.4 billion of “liquid” funds for FTX on their balance sheet.

Therefore, when mass demands for withdrawals took place, FTX didn’t have the capital to distribute back to account holders because the value of FTT had sunk 95%.

The $18 billion in liabilities was only propped up by $900 million of real liquidity with $470 million comprising of Robinhood (HOOD) stock shares.

Ultimately, FTX faced an $8 billion shortfall to fill in short notice or go under.

Any reader holding any crypto on any exchange should request immediate withdrawal of funds as soon as possible.

Don’t be the last one to ask for your money back. Get out while you can!

There is a good chance that every crypto exchange was faking their balance sheet with fake coins that have fake values while claiming these coins are liquid as US dollars.

That means weak balance sheets could plant the seeds of more bank runs putting extreme stress on liquidity and forcing them to halt withdrawals.

Any project related to FTX is now a zero.

This industry is truly broken and will take a generation to heal itself or might never come back.

I understand the FTX debacle as a highly positive event for the tech sector and tech stocks moving forward because it makes legitimate tech stocks look great.

FTX has set a low bar for tech stocks to jump over.

The Nasdaq market needed the fluff removed after the tech bubble had a 2-year accelerated bull market until 2022 and that came after a 10-year garden variety bull market in tech stocks.

FTX was the fluff. Avoid stocks such as Coinbase (COIN), Robinhood (HOOD), and MicroStrategy (MSTR).

Normal tech stocks will benefit after many incremental investors now believe crypto is completely fake.

This will forever be known as the colossal event that brought crypto to its knees.

I do believe that many of the leftover Bitcoin survivors will migrate into tech stocks moving forward because that’s the closest derivative to crypto.

Tech companies need to go through a lot of soul-searching to get their mojo back and a recession is always a good time to separate the good from the bad. Now, this is even better.

Crypto’s demise means venture capitalists will start to open the checkbook for non-crypto tech instead of spilling their money down a black hole.

“Technology is the key weapon in the fight for control of the industries of the future and in combating pandemics.” – Said American Economist Nouriel Roubini

Mad Hedge Technology Letter

November 11, 2022

Fiat Lux

Featured Trade:

(POSITIONING COUNTS)

(AMZN), (CVNA), (CPI)