The Market Outlook for the Week Ahead, or The Tweet that Sank a Thousand Ships

I always wondered who the enemy was. Now, I know.

Not only is Fed governor Jerome Powell responsible for the upcoming recession, I also heard he fixed the 1918 World Series where the Chicago White Sox deliberately lost.

And come to think of it, Jack the Ripper and D.B Cooper were never caught either. If Tweets are to be believed, the Fed now needs to seek guidance from the president before any subsequent policy decision.

It all reminds me of the last days of the Third Reich when Adolph Hitler was ordering into action divisions that no longer existed.

And I love all of it.

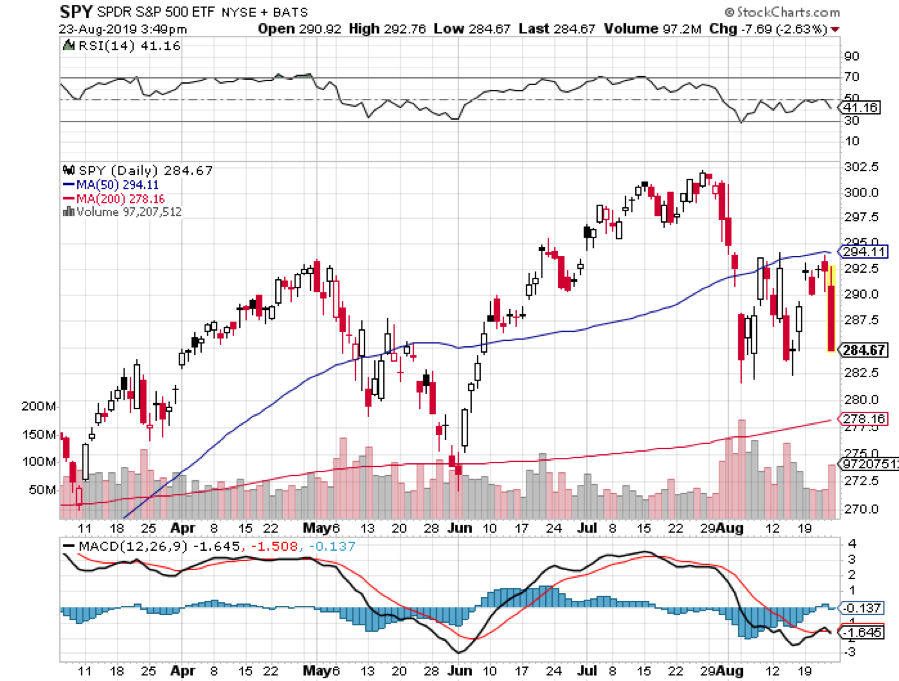

An 850 point top to bottom swan dive in the Dow Average vaporized all my short positions, which I had put on days ago for just this eventuality. It also allowed me to get back into Microsoft (MSFT) down $5, which I have been struggling to get back into for months.

My only miss of the month has been in Gold (GLD), whose move continues to be so parabolic that I haven’t been able to get you, or me, into it.

No doubt the administration will respond with another charm offensive, as this did this week, and ignite another ferocious short-covering rally.

The harsh truth is that confidence is eroding by the day. And the escalating talk of a recession can, in itself, cause a recession. So much depends on belief when share price earnings multiples are trading at a lofty 17X. But it is all looking increasingly like a little boy trying to head off a flood by holding his finger in a hole in a dike.

There’s no more waiting to see if the trade war escalates again on September 1. We already have the answer. It now appears we have instant escalation all the time with every Tweet. It’s not exactly what I want to bet my retirement fund on.

I have been getting questions as to why I have been adding long positions with the outlook so grim. For a start, these positions are all triply hedged.

I’m long a call against a short call with an identical maturity. I have low beta long positions hedged against high beta short positions. And finally, I don’t think we can break down below the 200-day moving average in the major indexes until the September 20 Fed meeting when they FAIL to cut interest rates again because the data isn’t there yet.

The net, net, net of all of this is that my portfolio can take a 1,000-point hit in the Dow Average and its no big deal.

And don’t forget. Ultra-low interest rates will put a higher floor under the market than we have seen in past selloffs.

I pray the insanity keeps up (did I hear a reference to the Messiah the other day?) because it is allowing me to ship out Trade Alerts as fast as I can write them.

Stocks rose briefly on German stimulus prospects. It's an idea imported from America, heavy borrowing and massive deficit spending to float the economy. It’s just what the world needs, more freshly printed money, like the last $17 trillion worked so well. It’s all confirmation that Europe is already in recession.

The US now has the world’s highest interest rates, at 3.60% for 30-year fixed-rate loans. Only the US offers loans of this duration, thanks to heavy government subsidies through Fannie Mae and Freddie Mac.

Floating rate loans in France are 1.39%, in Germany are 1.0%, Japan at 0.65%. In Denmark, banks will lend at a negative -0.50%. Yes, they will pay you to live in your house. But when you’re borrowing at -0.90% you can do that. Only China has higher interest rates, with an overnight at 4.60%. The irony runs deep.

Unsurprisingly, the Congressional Budget Office cut 0.3% off of its 2020 growth forecast and the US budget deficit will rise to a ruinous $1 trillion two years sooner than expected. Fading business investment and weakening consumer spending will be the problems. The trade war is also a drag. It’s funny how no one wants to spend in front of a recession.

“Mid Cycle Adjustment” is how the Fed described the last interest rates cut in minutes released on Wednesday. It makes further cuts less likely. So does a stock market trading 5% below all-time highs. They also mention the cut as an “insurance policy” not actually justified by the current economic data. Three weeks ago, the fed cut rates for the first time in a decade.

The Mad Hedge Trader Alert Service is posting its best month in two years. Some 22 of the last 23 round trips have been profitable, generating one of the biggest performance jumps in our 12-year history.

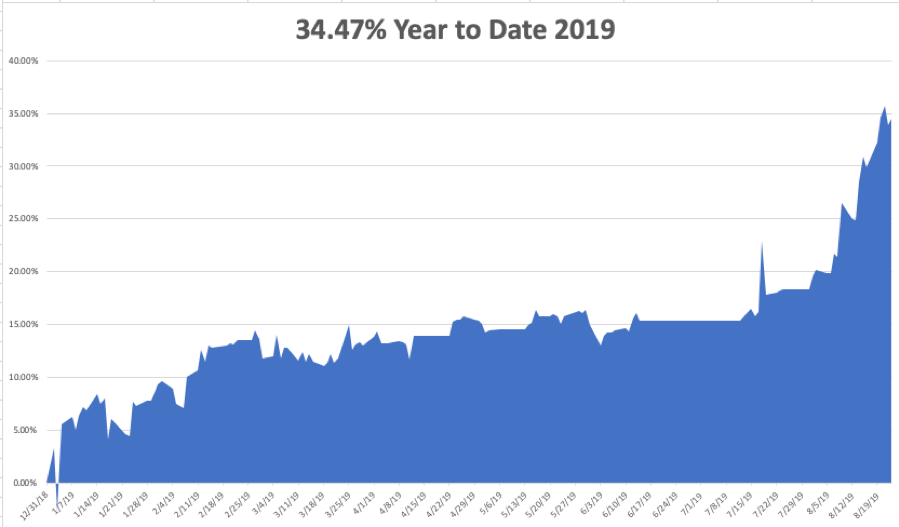

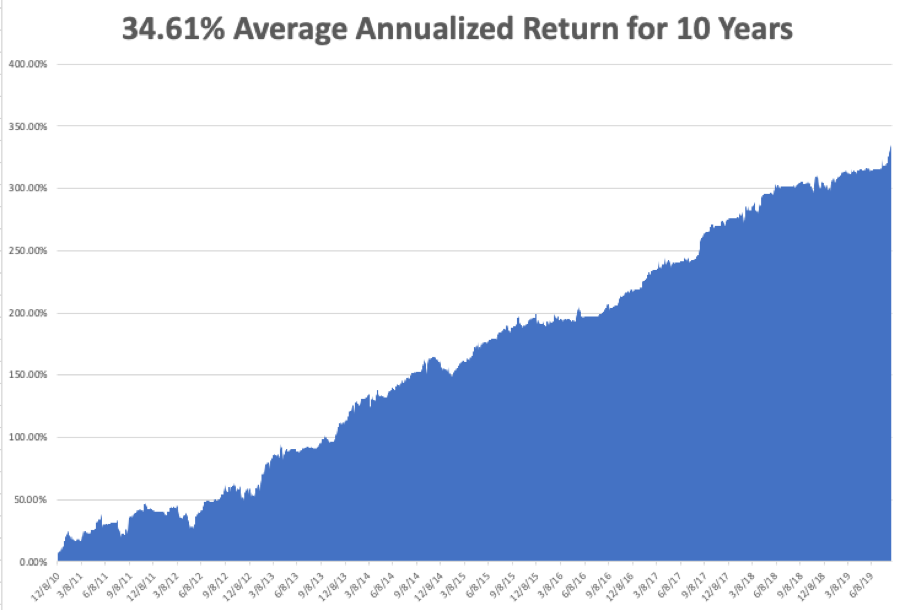

My Global Trading Dispatch has hit a new all-time high of 334.61% and my year-to-date shot up to +34.47%. My ten-year average annualized profit bobbed up to +34.62%.

I have coined a blockbuster 16.14% so far in August. All of you people who just subscribed in June and July are looking like geniuses. My staff and I have been working to the point of exhaustion, but it’s worth it if I can print these kinds of numbers.

As long as the Volatility Index (VIX) stays above $20, deep-in-the-money options spreads are offering free money. I am now 80% invested, 60% long big tech and 20% short, with 20% in cash. It rarely gets this easy.

The coming week will be a snore on the data front. Believe it or not, it could be quiet, as we grind through the last week of the summer.

On Monday, August 26 at 8:30 AM, US Durable Goods for July are out.

On Tuesday, August 27 at 9:00 AM, we get a new S&P Case Shiller National Home Price Index for June

On Wednesday, August 28, at 10:30, we learn the EIA Crude Oil Stocks for the previous week.

On Thursday, August 29 at 8:30 AM, the Weekly Jobless Claims are printed. July Pending Home Sales are published at 10:00 AM.

On Friday, August 30 at 10:00 AM, the University of Michigan Consumer Sentiment is printed.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, it will be a busy weekend with volunteer work at the Alameda Food Bank due and CPR training at the local fire department. I feel like I am getting my Eagle Scout rank all over again.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader