Featured Trade: (JUNE 19 DALLAS, TEXAS GLOBAL STRATEGY LUNCHEON) (THE TERRIBLE NEWS THE BOND MARKET IS TELLING TO GOLD), (GLD), (GDX), (SIL), (ABX), (REMX), (SLV)

The news from Australia?s Perth Mint was horrific last week. The refiner for the world?s second largest producer reported that sales hit a new three year low.

And the worst is yet to come.

Shipments of gold coins and bars plunged to 21,671 ounces in May, compared to 26,545 ounces in April. Silver sales have seen similar declines.

I have been warning readers for the last four years that investors want paper assets paying dividends and interest, not the hard stuff, now that the world is in a giant reach for yield.

Ten-year US Treasury yields jumping from 1.83% to 2.43% this year is pouring the fat on the fire.

This all substantially raises the opportunity cost of owning the barbarous relic. With bond yields now forecast to reach as high as 3.0% by the end of the year, the allure of the yellow metal is fading by the day.

The gold perma bulls have a lot of splainin? to do.

Long considered nut cases, crackpots, and the wearers of tin hats, lovers of the barbarous relic have just suffered miserable trading conditions since 2011. Gold has fallen some 39% since then during one of the great bull markets for risk assets of all time.

Let me recite all the reasons that perma bulls used your money to buy the yellow metal all the way down.

1) Obama is a socialist and is going to nationalize everything in sight, prompting a massive flight of capital that will send the US dollar crashing.

2) Hyperinflation is imminent, and the return of ruinous double-digit price hikes will send investors fleeing into the precious metals and other hard assets, the last true store of value.

3) The Federal Reserve?s aggressive monetary expansion through quantitative easing will destroy the economy and the dollar, triggering an endless bid for gold, the only true currency.

4) To protect a collapsing greenback, the Fed will ratchet up interest rates, causing foreigners to dump the half of our national debt they own, causing the bond market to crash.

5) Taxes will skyrocket to pay for the new entitlement state, the government?s budget deficit will explode, and burying a sack of gold coins in your backyard is the only safe way to protect your assets.

6) A wholesale flight out of paper assets of all kind will cause the stock market to crash. Remember those Dow 3,000 forecasts?

7) Misguided government policies and oppressive regulation will bring financial Armageddon, and you will need gold coins to bribe the border guards to get out of the country. You can also sew them into the lining of your jacket to start a new life abroad, presumably under an assumed name.

Needless to say, things didn?t exactly pan out that way.

The end-of-the-world scenarios that one regularly heard at Money Shows, Hard Asset Conferences, and other dubious sources of investment advice all proved to be so much bunk.

I know, because I was once a regular speaker on this circuit. I, alone, a voice in the darkness, begged people to buy stocks instead.

Eventually, I ruffled too many feathers with my politically incorrect views, and they stopped inviting me back. I think it was my call that rare earths (REMX) were a bubble that was going to collapse was the weighty stick that finally broke the camel?s back.

By the way, Molycorp (MCP), then at $70 a share, recently announced it was considering bankruptcy. Rare earths didn?t turn out to be so rare after all.

So, here we are, five years later. The Dow Average has gone from 7,000 to 18,000. The dollar has blasted through to a 14 year high against the Euro (FXE).

The deficit has fallen by 75%. Gold has plummeted from $1,920 to $1,150. And no one has apologized to me, telling me that I was right all along, despite the fact that I am from California.

Welcome to the investment business. Being wrong never seems to prevent my competitors from prospering.

Gold has more to worry about than just falling western demand. The great Chinese stock bubble, which has seen prices double in only nine months, has citizens there dumping gold in order to buy more stocks on margin.

This is a huge headache for producers, as the Middle Kingdom has historically been the world?s largest gold buyer. As long as share prices keep appreciating, demand there will continue to ebb.

So now what?

From here, the picture gets a little murky.

Certainly, none of the traditional arguments in favor of gold ownership are anywhere to be seen. There is no inflation. In fact, deflation is accelerating.

The dollar seems destined to get stronger, not weaker. There is no capital flight from the US taking place. Rather, foreigners are throwing money at the US with both hands, escaping their own collapsing economies and currencies.

And with global bond markets having topped out, the opportunity cost of gold ownership returns with a vengeance.

All of which adds up to the likelihood that today?s gold rally probably only has another $50 to go at best, and then it will return to the dustbin of history, and possibly new lows.

I am not a perma bear on gold. There is no need to dig up your remaining coins and dump them on the market, especially now that the IRS has a mandatory withholding tax on all gold sales. I do believe that when inflation returns in the 2020?s, the bull market for gold will return for real.

You can expect newly enriched emerging market central banks to raise their gold ownership to western levels, a goal that will require them to buy thousands of tons on the open market.

Gold still earns a permanent bid in countries with untradeable currencies, weak banks, and acquisitive governments, India, another major buyer.

Remember, too, also that they are not making gold anymore, and that all of the world?s easily accessible deposits have already been mined. The breakeven cost of opening new mines is thought to be around $1,400 an ounce, so don?t expect any new sources of supply anytime soon.

These are the factors which I think will take gold to the $3,000 handle by the end of the 2020?s, which means there is quite an attractive annualized return to be had jumping in at these levels. Clearly, that?s what many of today?s institutional buyers are thinking.

Sure, you could hold back and try to buy the next bottom. Oh, really? How good were you at calling the last low, and the one before that?

Certainly, incrementally scaling in around this neighborhood makes imminent sense for those with a long-term horizon, deep pockets, and a big backyard.

Oops!

Maybe It Doesn?t Look So Good After All

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/John-Thomas-Gold-e1455831491219.jpg297400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-10 01:03:122015-06-10 01:03:12The Terrible News the Bond Market is Telling to Gold

Featured Trade: (WEDNESDAY JUNE 10 GLOBAL STRATEGY WEBINAR), (JUNE 22 WASHINGTON DC GLOBAL STRATEGY LUNCHEON), (THE DEATH OF MCDONALD?S), ?(MCD), (WFM) (SHAK), (CMG), ?(PNRA), (MO), (YUM)

McDonald's Corp. (MCD) Whole Foods Market, Inc. (WFM) Shake Shack Inc. (SHAK) Chipotle Mexican Grill, Inc. (CMG) Panera Bread Company (PNRA) Altria Group Inc. (MO) Yum! Brands, Inc. (YUM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-09 11:08:152015-06-09 11:08:15June 9, 2015

Come join me for lunch for the Mad Hedge Fund Trader?s Global Strategy luncheon, which I will be conducting in Washington DC on Monday, June 22, 2015. A three-course lunch will be followed by an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be tossing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $217.

I?ll be arriving at 11:30 AM and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive private club in the downtown area of the city near Farragut Square that will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my?online store.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/04/Washington-DC-e1429195716994.jpg246400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-09 11:03:452015-06-09 11:03:45June 22 Washington DC Global Strategy Luncheon

McDonald?s (MCD) has always figured large in my life.

I grew up next door to one of the first five stands built in the country, in the Los Angeles metropolitan area. That?s when visionary milkshake mixer salesman, Ray Kroc, started to franchise his revolutionary new ideas for delivering fast food.

One of my fondest childhood memories was when my mother used to take us out to dinner there. At 15 cents a burger you fed seven growing kids for a buck and still had money left over for French fries. We brought our own cokes in an ice chest to save money.

I always gummed up the works by asking for a hamburger that had mustard only and no pickles. I clearly did not fit into the company?s stripped down Speedee Service business model.

In high school, I managed to land a coveted minimum wage job ($1 an hour) under the Golden Arches. I learned first hand the harsh realities of working for a living, and that you didn?t necessarily want to know how the sausage was made.

Then, the Big Mac came out, the blockbuster beef equivalent of a Saturn V rocket. Chicken McNuggets, Egg McMuffins, and Filet of Fish followed (for the Catholics on Fridays), and it seemed the company could do no wrong.

In a few decades, the company grew into the world?s largest restaurant, expanding its list of franchises to a staggering 36,000 shops in 119 countries.

It became the planet?s largest consumer of beef and potatoes in the world. Its presence is ubiquitous on US military bases around the world. Its chocolate shake is said to be able to withstand a nuclear attack.

However, since 2011, the stock has largely failed to perform, and has greatly underperformed the S&P 500. Its business model is aging. Its menu needs a major reworking.

The company has suffered sales declines at existing locations in five out of the last six quarters, with the rate of decline accelerating this year.

The problem is that people just don?t want to buy what they make anymore.

I went into a store the other day, and I was appalled. It was almost empty.

The few customers it had all seemed sick, obese, or unemployed, wearing polyester clothes. They periodically ducked outside for a quick cigarette.

They needed a double bacon cheeseburger like a hole in the head. Health was not their priority. They were a market that was literally dying.

It is becoming increasingly clear that the American market is moving beyond McDonald?s. Can the long vaunted company now play catch up?

This is the big problem. Millennials, those aged 18-34, which should be the company?s highest growth market, aren?t showing much interest in the company?s secret sauce.

They are, in fact, adopting a complete different life style that doesn?t have Ronald McDonald anywhere in it. They are very cautious in what they put in their young bodies.

Think organic, locally grown, low fat, low calorie, non-GMO, high fiber, and no artificial hormones or coloring anywhere. Think of health food, and you don?t exactly run off to a McDonald?s to eat. McDonald?s has a serious brand problem.

Organic foods are booming, seeing sales growth of 30% a year nationally, with far higher profit margins.

If you don?t believe me, look no further than the stock chart of Whole Foods (WFM) below, which at one point, saw its shares gain 116% relative to (MCD).

This is also a generation that is vastly more environmentally conscious that the Gen Xer?s and baby boomers before them. Beef is the single most environmentally destructive food product you can buy, with all the waste and methane byproducts.

One quarter pound beef patty requires a profligate 450 gallons of water to produce. That?s double the daily ration for a family of four here in drought suffering California. And who knows what the hell they are putting in it to preserve it down a very long global supply chain.

McDonald?s did make some limited progress on this front by announcing that they would no longer put ?pink slime? into their beef patties. If you don?t know what ?pink slime? is, then you don?t want to know. Suffice it to say that it is definitely not a great new marketing angle for health food nuts.

The company is also encountering ferocious competition for the fast food dollar from the new, rapidly growing ?fast casual? industry. These include Five Guys, Shake Shack (SHAK), Chipotle Mexican Grill (CMG), and Panera Bread (PNRA).

These companies are all snapping up the high margin end of the market, even though any one of them is miniscule in size when compared to McDonald?s. Collectively, they are nipping at Ronald McDonald?s heels.

I can?t even get my own kids to eat at McDonald?s anymore, they preferring the legendary In and Out Burger on the West Coast (no double entendre intended), which emulates the McDonald?s stripped down menu of the early 1950?s.

(In and Out is a fascinating business story for another day, as the $2 billion, 300 stand LA based company is now controlled by a 33 year old four time married heiress named Lynsi Snyder.)

McDonald?s is one of the world?s largest and best managed companies. In 2014 it generated an impressive $4.8 billion profit on $27.4 billion in sales, producing a not too shabby net margin of 17.5%. So we?re not, by any means, talking chapter 11 material here.

But it is going ex growth, and that invites a lower stock multiple, and a lower stock price, something you, as equity investors should be aware of. Is (MCD)?s position in the Dow Average 30 at risk?

Yikes! That would be a disaster for shareholders!

The company has seen the writing on the wall. It recently brought in a new CEO, Steve Easterbrook, to shake things up. But so far, all of the changes he has implemented have been administrative in nature. There is no category killing super burger anywhere on the horizon.

McDonald?s does still have some huge advantages. Its efficiencies, purchasing power, and economies of scale are epic. But the business is so enormous that any incremental change is unlikely to move the needle on the earnings front.

It is the classic dilemma when navigating a supertanker.

Another headache arises from the snowballing minimum wage, or living wage movement, which has McDonald?s squarely in its crosshairs. This promises to be a big political campaign issue in 2016.

Several cities, like San Francisco and Seattle, have already boosted pay from $8 to $15 and hour, which would substantially increase (MCD)?s operating costs and cut its price advantage.

It is possible that McDonald?s could go the route of so many other legacy industries that were born here, and then migrated abroad when the home market disappeared. I?m thinking about cigarettes (Altria Group (MO), Kentucky Friend Chicken (YUM), and coal (PEA).

Indeed, on my last trip to China, I ate regularly at McDonald?s, and couldn?t help but notice that it had become the country?s hot high end date. But the burden of proof lies on the current management as to whether they can pull this off.

So, you won?t find me buying (MCD) shares anytime soon. If you must own it for that generous 3.6% dividend, at the very least you should be writing covered calls against your position to take in premium income to offset the lack of capital appreciation.

In the meantime, I?ll be grabbing a double cheeseburger and chocolate shake at In and Out Burger, even though the lines there can be miserable.

Watch Out, McDonald?s!

https://www.madhedgefundtrader.com/wp-content/uploads/2015/06/John-Thoms-In-Out.jpg381348Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-09 11:03:002015-06-09 11:03:00The Death of McDonald?s

?It?s a manic depressive economy. Every other month we decide we might be in a recession,? said Kevin Hassett of the American Enterprise Institute.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/06/Masks-e1433861760534.jpg239300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-09 10:56:212015-06-09 10:56:21June 9, 2015 - Quote of the Day

When the US Department of Labor announced its blockbuster May nonfarm payroll showing a 280,000 gain, stocks behaved like the world had just ended.

The 32,000 in March and April upward revisions didn?t help either.

You would think data showing that the economy is improving much faster than many realized would be positive for ?RISK ON? equity investments.

It wasn?t.

Now, the laser focus is on the bond market, which is collapsing globally. The complete disappearance of liquidity is exacerbating the moves.

Bond traders are now hyper sensitive to any news of a stronger American economy, which will soon lead to higher interest rate rises by Janet Yellen?s Federal Reserve.

A world is ending, but not the one you think. The zero interest rate regime on which we have all become heavily addicted over the last eight years is about to go into the history books.

Welcome to the looking glass world of investment these days. Good new is bad news and bad news good.

Players are in a manic depressive mood, expecting the economy to plunge into recession one month, and then discounting a robust recovery the next.

Then there?s Greece, which threatens to default on its debt on alternate days, and then offers to pay on the others. This has prompted the Euro (FXE) to undergo more gyrations than a circus contortionist.

Not a friendly environment for a trader. Sturm und drang with no net movement in the indexes doesn?t pave the road to trading riches. Even staying long volatility (VIX) is not working, unless you have the fastest finger in Chicago.

This is why I am keeping the Mad Hedge Fund Trader model trading portfolio to an absolute minimum bare bones of positions, a single 10% weighting in the S&P 500 that I snapped up at the Friday lows. And even that one has me edgy.

After polling many of my most loyal, long-term readers, I learned that they would rather see a small number of great trades than a large number of positions that include a few losers.

So, cherry picking it is, at least, for now.

To say that the nonfarm was fantastic is something of an under statement.

Private nonfarm jobs jumped by a dynamic 262,000. High paying professional and business services employment increased by a runaway 63,000. Leisure and hospitality ramped up to 57,000. Health care picked up 47,000.

The big loser was mining (coal, gold, silver), which shed 17,000 jobs. Headline unemployment held steady at 5.5%, while average hourly earnings rose by 0.3%.

It was almost a perfect report.

It certainly reinforces my own forecast of a hot 3% GDP growth rate for the final three quarters of 2015. The question bedeviling traders and investors alike now is, ?How much of this growth is already discounted in today?s prices??

You almost wonder if stocks are tired of going up, which have been appreciating for more than six years. Stock buyers need a new story.

With a discount Euro beckoning, it sounds like this summer will be the best ever to take a long vacation.

Looks Like This is a Down Day

https://www.madhedgefundtrader.com/wp-content/uploads/2015/06/Pogo-Stick.jpg390168Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-08 09:22:402015-06-08 09:22:40Why Stocks Hated the May Nonfarm Payroll

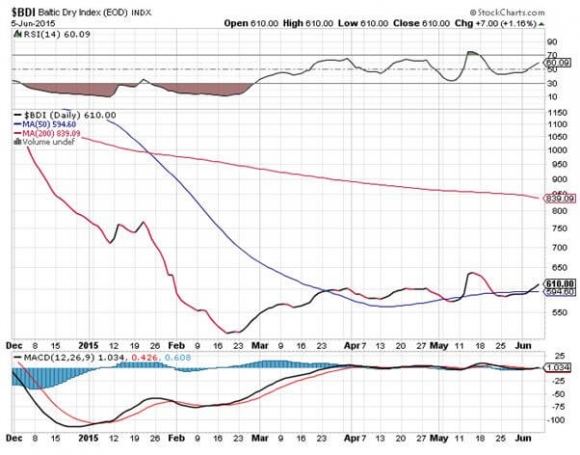

The shipping stocks have had an OK year so far in 2015. The big question remains: ?Is it real,? and ?Is it sustainable??

This sector has been down for so long that most investors left it for dead ages ago. All that was missing was the tolling of the Lutine Bell at the Lloyds of London insurance exchange to mark news of a sunken ship.

Lured by the heroin of artificially cheap financing during the 2000?s, the industry massively expanded capacity, believing that international trade would continue to grow at double digit rates forever.

It didn?t.

Sound familiar? Think of it as ?subprime at sea.?

Then the 2008 financial crisis hit, and demand evaporated. International trade, the main driver of freight rates, collapsed. Rates dropped as much as 90%, and share prices even more.

In those dark days, readers delighted in sending me maps of laid up ships with forlorn crews in Singapore harbor, which at the worst, numbered in the hundreds. You could almost walk to neighboring Malaysia and not get your ankles wet.

For most industries, the economy bottomed shortly thereafter and began a long, slow recovery. Not so for shipping.

China, the world?s largest buyer of bulk commodities, saw its economy peak in 2010, with annualized GDP growth halving since then from 13.5% to 7.0%.

This unleashed a second, even more vicious crisis for the shipping industry. With massive capital requirements, order times for new ships lasting three years, and hefty cancellation fees common, recovery delays are not what you want to hear about.

Ships ordered at the peak of the financing bubble suddenly started showing up in large numbers. So, the industry remained with excess capacity of 20%, especially in the dry bulk, container and crude oil tanker segments.

This was happening in the face of steadily rising fuel prices, thanks to events in Iran, Egypt, Libya, Syria, the Ukraine and now Iraq. The China slowdown also caused scrap metal rates to plummet, so downsizing shippers were paid less for junking their older, smaller, less fuel efficient bottoms.

American energy independence, thanks to the ?fracking? boom, means fewer ships are needed to carry oil from a tempestuous Middle East.

It has been the perfect storm of perfect storms. All but seven of the 30 largest shipping companies bled money in 2012, lots of it. Cumulative industry losses amounted to a mind numbing $7 billion over the previous four years. Companies continued to hemorrhage cash, and shareholders suffered.

And then a funny thing happened. The Chinese economic data slowly started to get better. Any price tied to business activity in the Middle Kingdom started marching upward in unison, including those for iron ore (BHP), (RIO), the Australian dollar (FXA), and Chinese and Australian stocks (FXI), (EWA).

This improvement, no matter how uncertain it may be, was not lost on the shipping industry. Capesize charter rates surged from $5,000 to $16,500, while Panamax rates are expected to fly from $8,000 to $9,500 by January.

Shipping stocks, the most highly leveraged of asset classes, skyrocketed. This enabled the Baltic Dry Index ($BDI), a measure of the cost of chartering bulk carriers for coal, iron ore, wheat, and other dry commodities, to steadily improve.

Apparently, it is off to the races once again.

I am not normally a person who buys a stock after it has just doubled, unless Costco is running a special on Jack Daniels. But if a share has fallen 99%, a double takes it down to only 98%, leaving it still absurdly cheap.

Shipping stocks fell so far, they were well below long dated option value. That means the market thought all of these guys were going under, which was never going to happen.

This is certainly the case with Dry Ships (DRYS), your poster boy for the Greek shipping industry. Adjusted for splits, the shares cratered from $120 to $0.60. It has just clawed its way up to $0.72. The company?s fleet consists of 38 dry bulk carriers, 10 tankers, and has orders for another four ships.

It has completed a major refinancing that takes the firm out of the fire and puts it back into the frying pan. This should buy (DRYS) some time, while other competitors, like Genco Shipping and Trading (GNK) are expected to go under, removing unwanted overcapacity from the market.

It also wisely diversified into offshore oil drilling right at the bottom of the market, picking up a 59% stake in Ocean Rig (ORIG) and its two semisubmersible rigs.

(DRYS) is not your typical ?widows and orphans? type investment. The web is chock full of allegations of insider trading, nepotism, and self-dealing by senior management.

It is domiciled in the Marshall Islands, so don?t expect much transparency. Pass the smell test, it does not. After all, it is a Greek shipping company.

If (DRYS) scares you, and it should, there are safer ways to play the rebound. The Guggenheim Shipping ETF (SEA) offers a broad mix of industry exposure with lower volatility. It is up a healthy 17% so far this year.

Even in the best-case scenario, shipping will never return to the heady growth rates of the naughts. China is highly unlikely to ever return to the breakneck growth rates of yore. The law of large numbers is kicking in with a vengeance.

It is modernizing its economic strategy, from one led by a low value added commodity exports, to a more domestically driven, services oriented approach. The bad news for shippers: The new model uses fewer bulk commodities, and therefore the ships to carry them.

However, if the China recovery is real, even a modest one, then the shipping industry offers one of the best multiple baggers that I can think of.

Just make sure you don?t get seasick from the volatility.

The Lutine Bell

https://www.madhedgefundtrader.com/wp-content/uploads/2013/09/Lutine-Bell.jpg336503Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-08 09:19:332015-06-08 09:19:33Have Calm Waters Returned for Shipping Stocks?

?This goes down as a cycle that is short on respect, but long on resiliency,? said economist, David Rosenberg.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/06/Rodney-Dangerfield-e1433769315782.jpg300223Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-06-08 09:16:192015-06-08 09:16:19June 8, 2015 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.