My friend and long-time subscriber, San Marks, invited me to appear on a podcast with him the other day. Who am I to say no? Besides, you never know when you might get a new question you haven’t heard, a truly original analysis, or a well-justified out-of-consensus approach.

It is my most up-to-date view on all asset classes out there, so you might take a listen. In these tumultuous times, you can never be current enough. To listen to the interview in full, please click here.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-20 06:06:072018-11-20 05:56:25Catch My All Asset Class Review on “Invest Like a Boss”

One of the fastest parts of technology growing at a rapid clip is fintech.

Fintech has taken the world by storm threatening the traditional banks.

Companies such as Square (SQ) and PayPal (PYPL) are great bets to outlast these dinosaurs who have a laser-like focus on technology to move the digital dollars in an efficient and low-cost way.

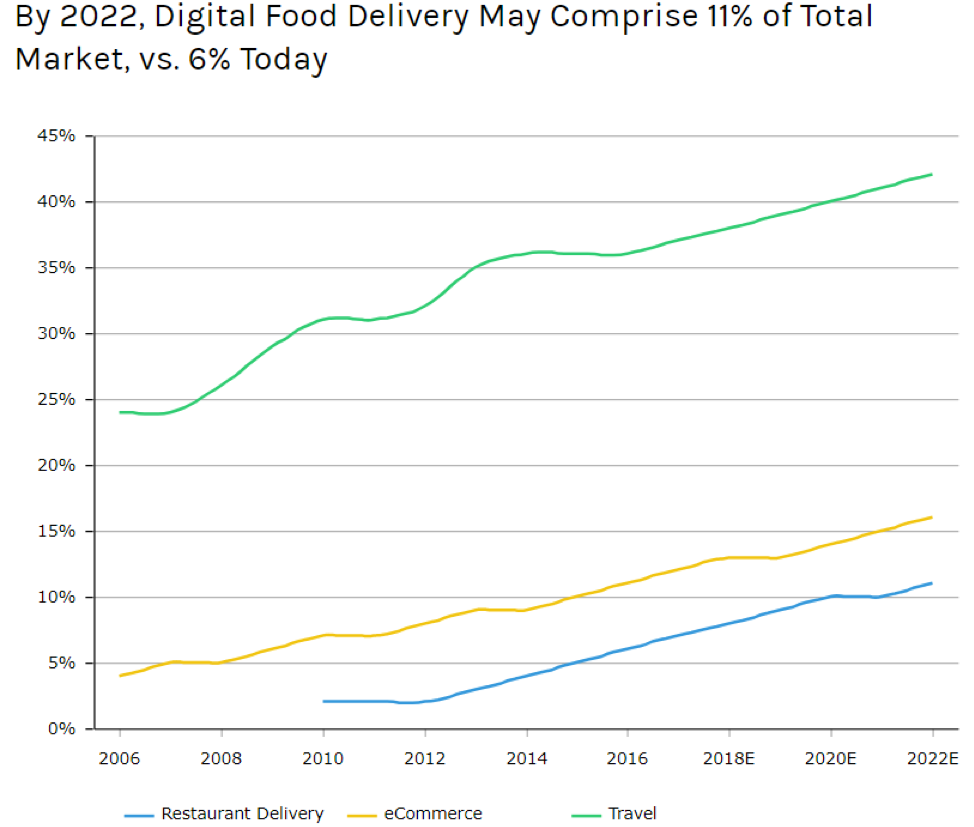

Another section of the technology movement that has caught my eye morphing by the day is the online food delivery segment that has soaring operating margins aiding Uber on their quest to go public next year.

There have been whispers that Uber could garner a $120 billion valuation dwarfing Chinese tech giant Alibaba’s (BABA) IPO which was the biggest IPO to date at $25 billion.

Uber is following in Amazon’s footsteps executing the “blitzscaling” method to suppress competition.

This strategy involves scaling up as quick as possible and seizing market share before anyone can figure out what happened.

The growth explodes at such speed that investors pile in droves throwing inefficient capital at the business leading the company to make bold bets even though profit is nowhere to be seen.

Blitzscaling has fueled American and Chinese tech to the top of the global tech charts and the trade war is mainly about these two titans jousting for first and second place in a real-time blitzscale battle of epic proportion.

The audacious stabs at new businesses usually end up fizzling out, but the ones that do have the potential to blaze a trail to profitability.

One business that has Uber giving hope of one day returning capital to shareholders is Uber Eats – the online food delivery service.

Total sales of restaurant deliveries will hit 11% of revenue if the current trend continues in 2022 marking a giant shift in consumer attitudes.

No longer are people eating out at restaurants, according to data, younger generations view ordering from an online food delivery platform as a direct substitute.

This mindset is eerily similar to Millennials attitude towards entertainment.

For many, Netflix (NFLX) is considered a better option than attending a movie theatre, and all forms of outdoor entertainment are under direct attack from these online substitutes.

One firm on the forefront of this movement has been Domino’s Pizza (DPZ).

You’d be surprised to find out that over half of the Domino’s Pizza staff are software developers.

They have focused on the customer experience doubling down on their online platform to offer the easiest way to order a pizza.

In 2012, the company was frightened to death that it still took a 25-step process to order a pizza.

By 2016, Domino’s rolled out “zero-click ordering” offering 15 different ways to order their product across many major platforms including Amazon’s Alexa.

This has all led to 60% of sales coming from online and rising.

The consistency, efficiency, and seamless online payment process has all helped Dominoes stock rise over 800% since May 2012 and that is even with this recent brutal sell-off.

Uber is perfectly positioned to take advantage of this new generation of dining in.

In the third quarter, Uber booked $2.1 billion of gross booking volume in their powerful online food delivery service.

The 150% YOY rise makes Uber Eats a force to be reckoned with.

Uber’s investment into e-scooters and bike transportation stems from the potential synergies of online food delivery efficiency.

It’s cheaper to deliver pizzas on a bicycle or anything without an internal combustion engine.

If you ever go to China, the electric powered three-wheel modified tuk-tuk with a storage compartment in the back instead of passenger seating is pervasive.

Often navigating around narrow alleyways is inefficient for a four-wheel automobile, and as Uber sets its sights on being the go-to last mile deliverer of food and whatnot, building out this vibrant transport network is vital to its long-term vision.

In fact, Uber is not an online ride-sharing platform, it will be something grander and its Uber elevate division could showcase Uber’s adaptability by making air transport cheap for the masses.

As soon as the robo-taxi industry gathers steam, Uber will ditch human drivers for self-driving technology saving billions in labor costs.

As it stands, Uber keeps cutting the incentive to drive for them with rates falling to as low as an average of $10 per hour now.

The golden age of being an Uber driver is long gone.

Uber is merely gathering enough data to prepare for the mass roll-out of automated cars that will shuttle passengers from point A to B.

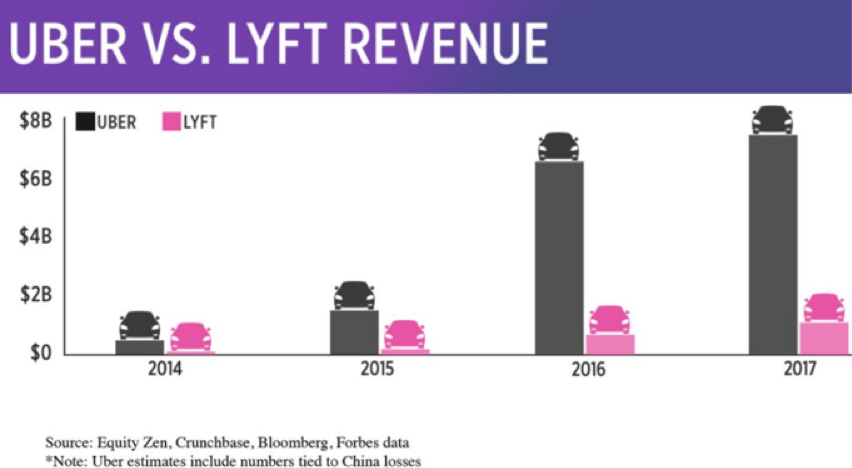

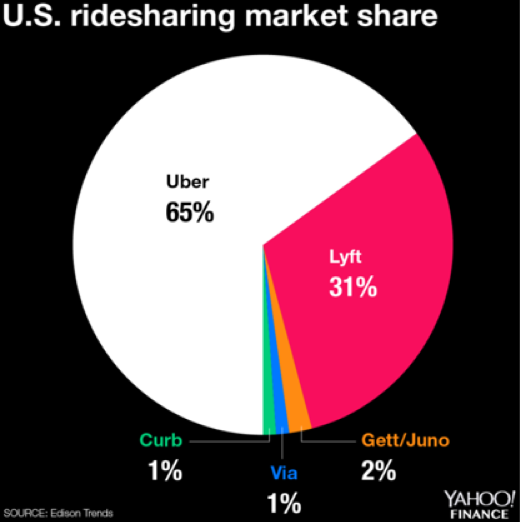

It doesn’t matter that Lyft has gained market share from Uber. Lyft’s market share was in the teens a few years ago and has rocketed to 31% taking advantage of management problems over at Uber to wriggle its way to relevancy.

It does not reveal how poor of a company Uber is, but it demonstrates that Uber’s network is spread over different industries and the sum of the parts is a lot greater than Lyft can fathom.

Lyft is a pure ride-share company and brings in annual revenue that is 4 times less than Uber.

Naturally, Uber loses a lot more money than Lyft because they have so many irons in the fire.

But even a single iron could be a unicorn in its own right.

CEO Dara Khosrowshahi recently talked about its Uber Eats division in glowing terms and emphasized that over 70% of the American population will have access to Uber Eats by the end of next year.

Uber’s position in the American economy as a pure next-generation tech business reverberates with its investors causing Khosrowshahi to brazenly admit that Uber “suffers from having too much opportunity as a company.”

Ultimately, the amped-up growth of the food delivery unit feeds back into its ride-sharing division. These types of synergies from Uber’s massive network effect is what management desires and dovetails nicely together.

In 2018 alone, 40% of Uber Eat’s customers were first-time samplers.

A good portion of these customers have never tried Uber’s ride-sharing service and when they travel for business or leisure, they later adopt the ride-sharing platform leading to more Uber converts.

Uber Freight has enabled truckers to push a button and book a load at an upfront price revolutionizing the process.

The online food delivery service is the place to be right now and it would be worth your while to look at GrubHub (GRUB).

Quarterly sales are growing over 50% and quarterly EPS growth was 61% sequentially for this industry leader.

Profit Margins are in the mid-20% convincingly proving that the food delivery industry will not be relying on razor-thin margins.

Charging diners $5 for delivery and taking a cut from the restaurateurs have been a winning strategy that will resonate further as more diners choose to munch in the cozy confines of their house.

Blitzscaling has led Uber to the online food delivery business and they are pouring resources into it to juice up profits before they go public next year.

The ride-sharing business is a loss-making enterprise as of now, and Uber will need to exhibit additional ingenuity to leverage the existing network to find strong pockets of revenue.

I believe they have the talent on their books to achieve finding these strong pockets making this company an intriguing stock to buy in 2019.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-20 06:06:032018-11-20 05:21:34A Lesson in Blitzscaling

“The first rule of any technology used in a business is that automation applied to an efficient operation will magnify the efficiency. The second is that automation applied to an inefficient operation will magnify the inefficiency.” – Said Co-Founder of Microsoft Bill Gates

https://www.madhedgefundtrader.com/wp-content/uploads/2013/08/Bill-Gates.jpg337335MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-20 06:05:512018-11-20 06:09:14November 20, 2018 - Quote of the Day

The Five Most Important Things That Happened Today

(and what to do about them)

1) Chinese Stocks Hit a One Month High, on hopes that a deal gets cut at the G-20 meeting in Buenos Aires on November 29. Do they know something we don’t? Click here.

2) The Housing Market is Effectively Closed, with new sales grinding to a complete halt. NAHB Housing Market Index crashes from 67 to 60, the biggest drop in four years. Some brokers haven’t done a deal in three months. Click here.

3) Salesforce Stock is Trashed $8, on protests over running illegal immigrant databases for the US government. Buy the dip. Click here.

4) Tech Gets Trashed Again, but won’t hit new lows this time. Another chance to get in before the yearend rally. Click here.

5) Hedge Fund Blowup Takes Natural Gas Down 20% in a Day. James Cordier got away with naked call selling for years until he didn’t. All investors completely wiped out. I have always told followers to avoid this strategy for years. It’s picking up pennies in front of a steamroller. Same for naked puts too. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MASS EVACUATION)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-19 10:49:272018-11-19 10:49:27Mad Hedge Hot Tips for November 19, 2018

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-19 08:30:252018-11-19 08:30:25November 19, 2018 - MDT Pro Tips A.M.

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MASS EVACUATION)

(SPY), (WMT), (NVDA), (EEM), (FCX), (AMZN), (AAPL), (FCX), (USO), (TLT), (TSLA), (CRM), (SQ)

I will be evacuating the City of San Francisco upon the completion of this newsletter.

The smoke from the wildfires has rendered the air here so thick that it has become unbreathable. It reminds me of the smog in Los Angeles I endured during the 1960s before all the environmental regulation kicked in. All Bay Area schools are now closed and anyone who gets out of town will do so.

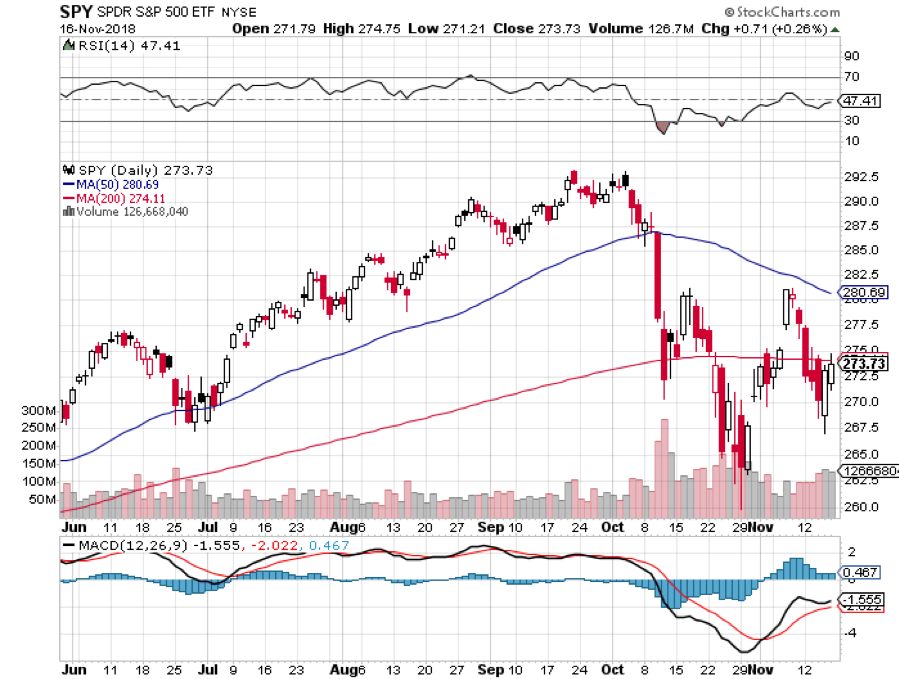

There has been a mass evacuation going on of a different sort and that has been investors fleeing the stock market. Twice last week we saw major swoons, one for 900 points and another for 600. Look at your daily bar chart for the year and the bars are tiny until October when they suddenly become huge. It’s really quite impressive.

Concerns for stocks are mounting everywhere. Big chunks of the economy are already in recession, including autos, real estate, semiconductors, agricultural, and banking. The FANGs provided the sole support in the market….until they didn’t. Most are down 30% from their tops, or more.

In fact, the charts show that we may have forged an inverse head and shoulders for the (SPY) last week, presaging greater gains in the weeks ahead.

The timeframe for the post-midterm election yearend rally is getting shorter by the day. What’s the worst case scenario? That we get a sideways range trade instead which, by the way, we are perfectly positioned to capture with our model trading portfolio.

There are a lot of hopes hanging on the November 29 G-20 Summit which could hatch a surprise China trade deal when the leaders of the two great countries meet. Daily leaks are hitting the markets that something might be in the works. In the old days, I used to attend every one of these until they got boring.

You’ll know when a deal is about to get done with China when hardline trade advisor Peter Navarro suddenly and out of the blue gets fired. That would be worth 1,000 Dow points alone.

It was a week when the good were punished and the bad were taken out and shot. Wal-Mart (WMT) saw a 4% hickey after a fabulous earnings report. NVIDIA (NVDA) was drawn and quartered with a 20% plunge after they disappointed only slightly because their crypto mining business fell off, thanks to the Bitcoin crash.

Apple (AAPL) fell $39 from its October highs, on a report that demand for facial recognition chips is fading, evaporating $170 billion in market capitalization. Some technology stocks have fallen so much they already have the next recession baked in the price. That makes them a steal at present levels for long term players.

The US dollar surged to an 18-month high. Look for more gains with interest rates hikes continuing unabated. Avoid emerging markets (EEM) and commodities (FCX) like the plague.

After a two-year search, Amazon (AMZN) picked New York and Virginia for HQ 2 and 3 in a prelude to the breakup of the once trillion-dollar company. The stock held up well in the wake of another administration antitrust attack.

Oil crashed too, hitting a lowly $55 a barrel, on oversupply concerns. What else would you expect with China slowing down, the world’s largest marginal new buyer of Texas tea? Are all these crashes telling us we are already in a recession or is it just the Fed’s shrinkage of the money supply?

The British government seemed on the verge of collapse over a Brexit battle taking the stuffing out of the pound. A new election could be imminent. I never thought Brexit would happen. It would mean Britain committing economic suicide.

US Retails Sales soared in October, up a red hot 0.8% versus 0.5% expected, proving that the main economy remains strong. Don’t tell the stock market or oil which think we are already in recession.

My year-to-date performance rocketed to a new all-time high of +33.71%, and my trailing one-year return stands at 35.89%. November so far stands at +4.08%. And this is against a Dow Average that is up a miniscule 2.41% so far in 2018.

My nine-year return ballooned to 310.18%. The average annualized return stands at 34.46%. 2018 is turning into a perfect trading year for me, as I’m sure it is for you.

I used every stock market meltdown to add aggressively to my December long positions, betting that share prices go up, sideways, or down small by then.

The new names I picked up this week include Amazon (AMZN), Apple (AAPL), Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and a short position in Tesla (TSLA). I also doubled up my short position in the United States US Treasury Bond Fund (TLT).

I caught the absolute bottom after the October meltdown. Will lightning strike twice in the same place? One can only hope. One hedge fund friend said I was up so much this year it would be stupid NOT to bet big now.

The Mad Hedge Technology Letter is really shooting the lights out the month, up 8.63%. It picked up Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and Apple (AAPL) last week, all right at market bottoms.

The coming week will be all about October housing data which everyone is expecting to be weak.

Monday, November 19 at 10:00 EST, the Home Builders Index will be out. Will the rot continue? I’ll be condo shopping in Reno this weekend to see how much of the next recession is already priced in.

On Tuesday, November 20 at 8:30 AM, October Housing Starts and Building Permits are released.

On Wednesday, November 21 at 10:00 AM, October Existing Home Sales are published.

At 10:30 AM, the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 22, all market will be closed for Thanksgiving Day.

On Friday, November 23, the stock market will be open only for a half day, closing at 1:00 PM EST. Second string trading will be desultory, and low volume.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I'd be roaming the High Sierras along the Eastern shore of Lake Tahoe looking for a couple of good Christmas trees to chop down. I have two US Forest Service permits in hand at $10 each, so everything will be legit.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/John-Thomas-Ax.png375522MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-19 03:06:042018-11-19 02:57:54The Market Outlook for the Week Ahead, or Mass Evacuation

That is exactly what management of a fast-growing tech company doesn’t want to hear.

Losing money isn’t fun. And investors only put up with it because of the juicy growth trajectories management promises.

Without the expectations of hard-charging growth, there is no attractive story in a world where investors need stories to rally behind.

Setting the bar astronomically high in the approach to management’s execution and product development will always be, the single most important element in a tech company.

This is the secret recipe for thwarting entropy and rising above the rest.

You might be shocked to find out that most tech firms die a harrowing death, the average Joe wouldn’t know that, with constant headlines glorifying our tech dignitaries.

Just look at the pageantry on display that was Amazon’s (AMZN) quest to find a second headquarter.

According to Apex Marketing, the hoopla that coalesced around Amazon’s year-long search netted Amazon $42 million in free advertising by tracking the absorbed inventory of exposure from print, TV, and online.

Social media traffic by itself rung up $8.6 million of freebies.

These days, tech really does sell itself, and I didn’t even mention the billions in tax breaks Amazon will harvest from their Willy Wonka and the Chocolate Factory style headquarter search.

The only thing I would have changed would have been extending the contest into the second year.

Amazon’s brand is probably the most powerful in the world, and that is not because they are in the business of only selling chocolate bars.

One company that might as well sell chocolate bars and has been stymied by the throes of entropy is TiVo (TIVO).

TiVo was once the darling of the technology world.

It was way back in 1999 when TiVo premiered the digital video recorder (DVR).

It modernized how television was consumed in a blink of an eye.

Broad-based adoption and outstanding product feedback were the beginning of a long love affair with diehard users wooed by the superior functionality of TiVo that allowed customers to record full seasons of television shows, and, the cherry on top, fast-forward briskly through annoying commercials.

The technology was certainly ahead of its time and TiVo had its cake and ate it for years.

The stock price, in turn, responded kindly and TiVo was trading at over $106 in August of 2000 before the dot com crash.

That was the high-water mark and the stock has never performed the same after that.

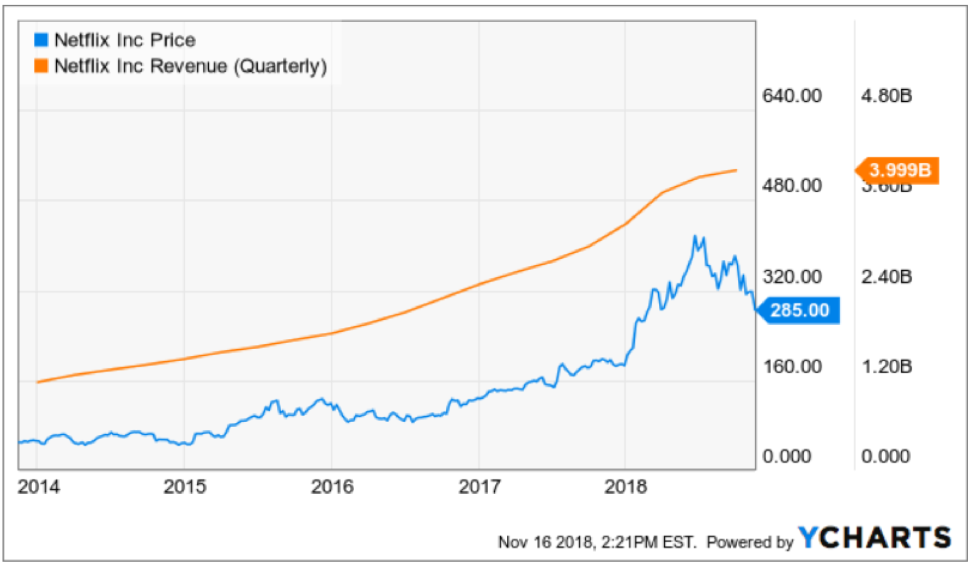

TiVo’s cataclysmic decline can be traced back to the roots of the late 90’s when a small up and coming tech company called Netflix (NFLX) quickly pivoted from mailing DVD’s to producing proprietary online streaming content.

Arrogant and set in their old ways, TiVo failed to capture the tectonic shift from analog television viewers cutting the cord and migrating towards online streaming services.

Consumer’s viewing habits modernized, and TiVo never developed another game-changing product to counteract the death of a thousand cuts to traditional television and its TiVo box that is still ongoing as I write this.

Like a sitting duck, Charter Communications (CHTR) and Dish Network (DISH) devoured TiVo’s market share in the traditional television segment constructing DVR’s for their own cable service.

And instead of licensing their technology before their enemies could build an in-house substitute, TiVo chose to sue them after the fact, resulting in a one-time payment, but still meant that TiVo was bleeding to death.

Enter Project Griffin.

Netflix (NFLX) spent years developing Project Griffin, an over-the-top (OTT) TV box that would host its future entertainment content and poured a bucket full of capital into the software and hardware of this revolutionary product.

Making the leap of faith from the traditional DVD-by-mail distribution model that would soon be swept into the dustbin of history was an audacious bet that looks even better with each passing year.

This Netflix branded OTT box was specifically manufactured for Netflix’s Watch Instantly video service.

In 2007, Netflix was just week’s away from rolling out the hardware from Project Griffin when CEO of Netflix Reed Hastings decided to trash the project.

His reason was that a branded Netflix box would hinder the software streaming content confining their growth trajectory to only their stand-alone platform.

This would prevent their streaming service to populate on other networks.

To avoid discriminating against certain networks was a genius move allowing Netflix to license digital content to anyone with a broadband connection, and giving them chance to make deals with other companies who had their own box.

It was the defining moment of Netflix that nobody knows about.

Netflix became ubiquitous in many Millennial households and Roku (ROKU) was spun-out literally bestowing new CEO of Roku Anthony Woods with a de-facto company-in-a-box to build on thanks to old boss Reed Hastings.

Woods cut his teeth borrowing TiVo’s technology and developed the digital video recorder (DVR) as the founder of ReplayTV before he joined Netflix and was the team leader of Project Griffin.

Now, he had a golden opportunity dropped into his lap and Woods ran with it.

Woods quickly became aware that hardware wasn’t the future of technology and switched to a digital ad-based platform model allowing any and all streaming services to launch from the Roku box.

No doubt Woods understood the benefits of being an open platform and not playing favorites to certain networks in a landscape where Apple (AAPL), Google (GOOGL), Facebook (FB), and Amazon have made “walled gardens” an important part of their DNA.

Democratizing its platform was in effect what the internet and technology were supposed to be from the onset and Roku has excavated value from this premise by playing nice with everyone.

This also meant scooping up all the ad dollars from everyone too.

At the same time, Wood’s mentor Hastings has rewritten the rules of the media industry parting the sea for Roku to mop up and dominate the OTT box industry with Amazon and Apple trailing behind.

Roku was perfectly positioned with a superior finished product, but also took note of the future and zigged and zagged when they needed to which is why ad sales have surpassed their hardware sales.

By 2021, over 50 million Americans will say adios to cable and satellite TV.

The addressable digital ad market is a growing $80 billion per year market and Roku will have a more than fair shot to secure larger market share.

The rock-solid foundations and handsome growth story are why the Mad Hedge Technology Letter is resolutely bullish on Roku and Netflix.

Roku and Netflix have continued to evolve with the times and TiVo is now desperately attempting to sell the remains of itself before the vultures feast on their corpse.

What is left is a portfolio of IP assets that brought in $826 million in 2017, and they have exited the hardware business entirely halting production of the iconic TiVo box.

Digesting 100% parabolic moves up in the share price is a great problem to have for Roku and Netflix.

These two are set to lead the online streaming universe and stoked by robust momentum to go with it.

The Mad Hedge Technology Letter currently holds a Roku December 2018 $30-$35 in-the-money vertical bull call spread bought at $4.35, and it is just the first of many tech trade alerts that will be connected to the rapidly advancing online streaming industry.

THE FRUITS OF PROJECT GRIFFIN

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/Netflix-hardware.png443924MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-19 02:06:442018-11-19 01:56:31Roku’s Unassailable Lead

“Technology will change, will change us, so we should change as well” –Said Chairwoman of the International Monetary Fund (IMF) Christine Lagarde.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-19 02:05:082018-11-19 01:33:41November 19, 2019 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.