Come join me for lunch for the Mad Hedge Fund Trader’s Global Strategy luncheon, which I will be conducting in Miami, Florida, on Tuesday, October 16, 2018.

A three-course lunch will be followed by an extended question-and-answer period.

I’ll be giving you my up-to-date view on stocks, bonds, foreign currencies, commodities, energy, precious metals, and real estate.

And to keep you in suspense, I’ll be tossing a few surprises out there, too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $248.

I’ll be arriving at 11:30 AM and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a restaurant at a major downtown hotel.

I look forward to meeting you, and thank you for supporting my research.

One of the few people who can magnify pressure on the venture capitalists of Silicon Valley is none other than Masayoshi Son.

What a ride it has been so far. At least for him.

His $100 billion SoftBank Vision Fund has put the Sand Hill Road faithful in a tizzy – utterly revolutionizing an industry and showing who the true power broker is in Silicon Valley.

He has even gone so far as doubling down his prospects by claiming that he will raise a $100 billion fund every few years and spend $50 billion per year.

This capital logically would flow into what he knows best – technology and the best technology money can buy.

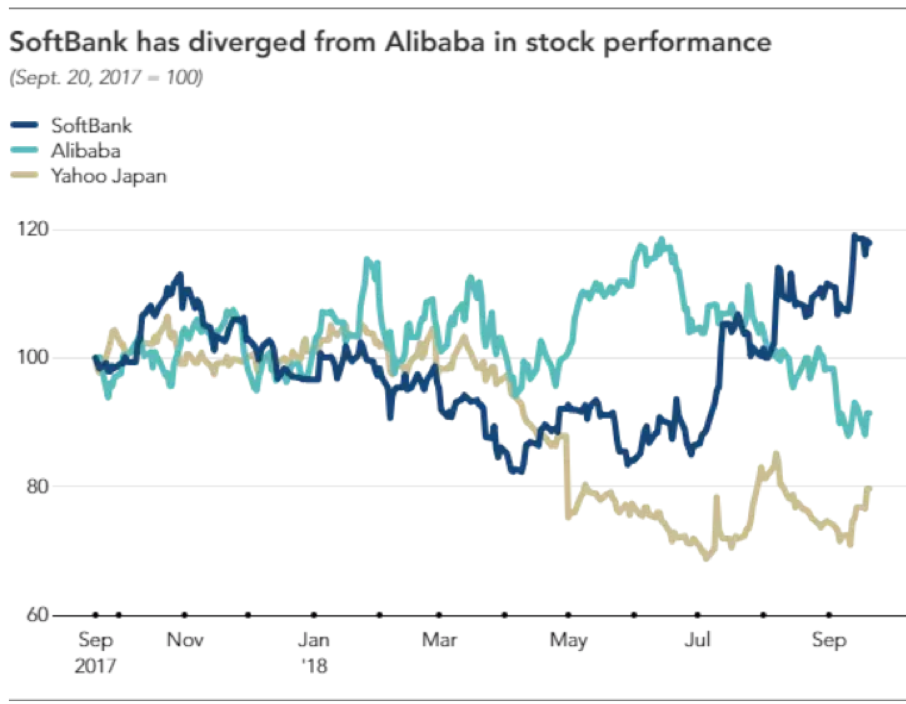

As Yahoo Japan and Alibaba (BABA) shares have floundered, SoftBank’s stock has decoupled from the duo displaying explosive brawn.

SoftBank’s stock is up 30% in the past few months and I can tell you it’s not because of his Japanese telecommunications business which has served him well until now as his cash cow.

Yahoo Japan, in which SoftBank owns a 48.17% stake, has existing synergies with SoftBank’s Japanese business, but has experienced a tumble in share price as Son turns his laser-like focus to his epic Vision Fund.

His tech investments are bearing fruit and not only that, Son revealed his Alibaba investment is about to clean up shop to the tune of $11.7 billion next year shooting SoftBank shares into orbit.

A good portion of the lucrative windfall will arrive from derivatives connected to the sale of Alibaba, and the other 60% comes from the paper profits finally realized in this shrewd piece of business.

Equally paramount, SoftBank’s Vision Fund hauled in $2.13 billion in operating profits from the April-June quarter underscoring the effectiveness of Masayoshi Son’s tech ardor.

Son said it best of the performance of the Vision Fund saying, “Results have actually been too good.”

So good that after this June, Son changed his schedule to spend 3% of his time on his telecom business down from 97% before June.

His telecommunications business in Japan has turned into a footnote.

It was the first quarter that Son’s tech investments eclipsed his legacy communications company.

Son vies to rinse and repeat this strategy to the horror of other venture capitalists.

The bottomless pit of capital he brings to the table predictably raises the prices for everyone in the tech investment world.

Son’s capital warfare strategy revolves around one main trope – Artificial Intelligence.

He also strictly selects industry leaders which have a high chance of dominating their field of expertise.

Geographically speaking, the fund has pinpointed America and China as the best sources of companies. India takes in the bronze medal.

Unsurprisingly, these two heavyweights are the unequivocal leaders in artificial intelligence spearheading this movement with the utmost zeal.

His eyes have been squarely set on Silicon Valley for quite some time and his record speaks for himself scooping up stakes in power players such as Uber, WeWork, Slack, and GM (GM) Cruise.

Other stakes in Chinese firms he’s picked up are China’s Uber Didi Chuxing, China’s GrubHub (GRUB) Ele.me and the first digital insurer in China named Zhongan International costing him $500 million.

Other notable deals done are its sale of Flipkart to Walmart (WMT) for $4 billion giving SoftBank a $1.5 billion or 60% profit on the $2.5 billion position.

In 2016, the entire venture capitalist industry registered $75.3 billion in capital allocation according to the National Venture Capital Association.

This one company is rivalling that same spending power by itself.

Its smallest deal isn’t even small at $100 million, baffling the local players forcing them to scurry back to the drawing board.

The reverberation has been intense and far-reaching in Silicon Valley with former stalwarts such as Kleiner Perkins Caufield & Byers breaking up, outmaneuvered by this fresh newcomer with unlimited capital.

Let me remind you that it was considered standard to cautiously wade into investment with several millions.

Venture capitalists would take stock of the progress and reassess if they wanted to delve in some more.

There was no bazooka strategy then.

SoftBank has thrown this tactic out the window by offering aspiring firms showing promise boatloads of capital up front even overpaying in some cases.

Conveniently, Son stations himself nearby at a nine-acre estate in Woodside, California complete with an Italianate mansion he bought for $117.5 million in 2012.

It was one of the most expensive properties ever purchased in the state of California even topping Hostess Brands owner Daren Metropoulos, who bought the Playboy Mansion from Hugh Hefner in 2016 for $100 million.

If you think Son is posh – he is not. He only fits himself out in the Japanese budget clothing brand Uniqlo. He just needed a comfortable place to stay and he hates hotels.

In August, SoftBank decided to top off the $4.4 billion investment in WeWork, an American office space-share company, with another $1 billion leading Son to proclaim that WeWork would be his “next Alibaba.”

Son continued to say that WeWork is “something completely new that uses technology to build and network communities.”

The rise of remote workers is taking the world by storm and this bet clearly follows this trend.

The unlimited coffee and beer found in the new Japanese Roppongi WeWork office that opened earlier this year was a nice touch.

WeWork plans to open 10-12 offices in Japan by the end of 2018.

Thus far, WeWork is operating in over 300 locations in over 20 countries.

Revenue is growing rapidly with the $900 million in 2017 a 12-fold improvement from 2014.

The newest addition to SoftBank’s dazzling array of unicorns is Bytedance, a start-up whose algorithms have fueled news-stream app Jinri Toutiao’s meteoric rise in China.

The deal values the company at $75 billion.

It also runs video sharing app Douyin, and overseas version TikTok.

Bytedance’s proprietary algorithm, serving to personalize streams for users, is the best in China.

They have been able to insulate themselves from local industry giants Tencent and Alibaba.

TikTok has piled up over 500 million users and brilliant investment like these is why Son revealed that the Vision Fund’s annual rate of return has been 44%.

SoftBank’s ceaseless ambition has them in the news again with whispers of investing in a Chinese online education space with a company called Zuoyebang.

China’s online education market is massive. In 2017, this industry pulled down over $33 billion in revenue, and 2018 is poised to break $55 billion.

Zuoyebang has lured in Goldman Sach’s (GS) as an investor.

This platform allows users to upload homework questions for third party assistance – the name of the app literally translates into “homework help.”

Cherry-picking off the top of the heap from the best artificial intelligence companies in the world is the secret recipe to outperforming your competitors.

At the same time, aggressively throwing money at these companies has effectively frozen out any resemblance of competition. Once the competition is frozen out, the value of these investments explodes, swiftly super-charged by rapidly expanding growth drivers.

How can you compete with a man who is willing to pay $300 million for a dog walking app?

Venture capitalist funds have been scrambling to reload and mimic a Vision Fund-like business of their own, but its not easy raising $100 billion quickly.

This genius strategy has made the founder of SoftBank the most powerful businessman in the world.

Son owns the future and will have the largest say on how the world and economies evolve going forward.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Softbank-CEO-2.png539472MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-04 09:01:392018-10-04 08:51:07How Softbank is Taking Over the US Venture Capital Business

Since we sold short the US Treasury bond market on Monday, it has plunged a stunning 3 points. Bond yields just performed a rare 10 basis point move up to 3.18%. You usually only see that during a major “RISK OFF” geopolitical event or financial crisis.

You could see all of the key support levels failing like a hot knife for butter. The next support for the United States Treasury Bond Fund (TLT) is now at $111, or some 2.5 points down from here, pointing to a 3.25% yield for the ten-year bond.

My yearend forecast of a ten-year yield of 3.25% and a one-year target of 4.0% is alive and well.

The break marks an important departure from a stubborn two-year trading range….to the downside.

As with major breaks there is not a single a data point that broke the camel’s back. It could have been the agreement to NAFTA 2.0 on Monday or the blistering hot ISM Services print at a 21-year high on Wednesday.

Rather, it has been a steady death by a thousand cuts spread over several points that did it. It was just a matter of time before a 4.2% GDP growth rate crushed the fixed income market.

If I had to point to one single thing that triggered this debacle, it would be Amazon’s (AMZN) decision to give a 25% raise to its 250,000 US employees to $15 an hour.

If Wal-Mart (WMT), McDonald’s (MCD), or Target (TGT) have to resort to the same, you could have a serious outbreak of inflation on 2019. Imagine that, a bidding war for minimum wage workers.

ALL of those costs will be passed on to us, which is highly inflationary, and bonds absolutely HATE inflation.

Other than giving us boasting rights, the bond market move carries several important messages for us.

Money is about to start transferring from borrowers to savers in a major way. You won’t hear about seniors unable to live off of their savings anymore, a common refrain of the past decade.

Cash is now offering a serious competitor to bond and equity investments. And the next recession and bear market have just been moved closer.

The rocketing US budget deficit is starting to bear its bitter fruit as the government is starting to crowd out private sector borrowers. The budget deficit should be running at a $1 trillion annualized rate by the end of this year.

All of you celebrating your windfall tax cuts are getting a sharp reminder that the money has been entirely borrowed, some 40% from foreign bond investors we have been attacking. It will have to be paid back some time.

Of course, we all knew this was coming. It is no accident that the most capital-intensive industries in the country, also the heaviest borrowers, have seen the worst stock performance of 2018 including real estate, REITS, steel, and autos. Their profit margins have all just been seriously chopped.

So, what to do about the bond market now that we have begun the next leg in a 30-year bear market? For a start, don’t sell. Rather, wait for the next rally back up to the old support level at $116. It should revisit the old support level at least once.

When it does, SELL WITH BOTH HANDS.

I Just Love That 25% Wage Hike

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Factory-worker.png233447MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-04 09:01:072018-10-03 20:12:54Bonds Finally Break Two Year-Range

“The biggest loss I ever suffered was not buying Amazon when I met Jeff Bezos in 1999,” said legendary value investor Ron Baron, when Amazon was trading at $15 a share.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Ron-Baron.png196233MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-04 09:00:442018-10-03 20:12:27October 4, 2018 - Quote of the Day

The Five Most Important Things That Happened Today

(and what to do about them)

1) Will China Get the Same Free Pass as Canada? If so, stocks will rally another 10% from here. Keep buying those dips, especially in my “trade peace” stocks. Click here.

2) Intel Says it Will Reach Full Year Targets. And the rest of the chip sector seems to be bottoming on the back of the USMCA trade deal. Is it off to the races once again? Buyers are certainly looking for laggards. Click here.

3) Aston Martin IPO Bombs in London. The wrong industry at the wrong time in the wrong place, down 10% on the first day. Buy the car, not the stock. Actually, buy a Tesla (TSLA) instead. The whole world is going electric, and Aston Martin doesn’t fit anywhere in that picture. Click here.

4) Private Sector Hiring Blows Out to the Upside, with the September ADP Report surprising as if you needed more proof of a full employment economy. Smaller companies did most of the hiring, another sign of a topping economy. Click here.

5) ISM Services Index Hits a 21 Year High, jumping from 58.5 to 61.6 in September. It shows how irrelevant manufacturing really has become. And you wondered why investors are so heavily loaded with technology stocks. Buy software, short hardware! Click here.

Published today in the Mad HedgeGlobal Trading Dispatch and Mad Hedge Technology Letter:

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-03 13:41:492018-10-03 13:41:49Mad Hedge Hot Tips for October 3, 2018

Long Term Equity Anticipation Securities, or LEAPS, are a great way to play the market when you expect a substantial move up in a security over a long period of time. Get these right and the returns over 18 months can amount to several hundred percent.

At market bottoms these are a dollar a dozen. At all-time highs they are as scarce as hen’s teeth. However, scouring all asset classes there are a few sweet ones to be had.

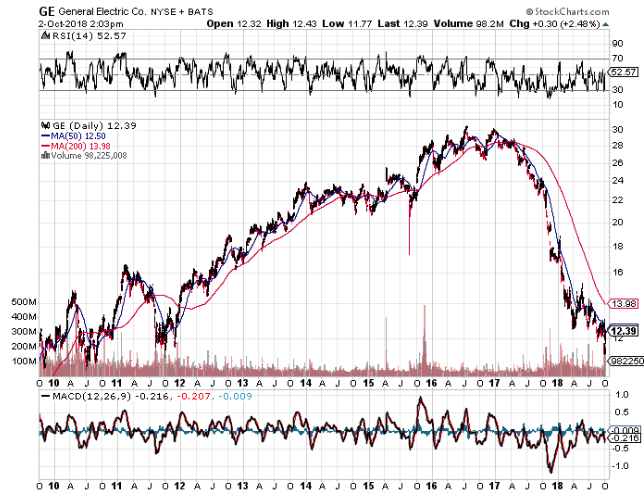

General Electric (GE) is a stock that has been taken out to the woodshed and beaten senseless. Management has made every possible mistake they could have over the past two decades.

During the 2000’s the company paid enormous premiums to get into the financial sector, thus causing the pros to dub it as the “hedge fund that made light bulbs.” They bailed out right at the market bottom after the 2008 crash for pennies on the dollar.

If it weren’t for Oracle of Omaha Warren Buffet’s generous move to buy their 10% yielding convertible bonds the company would have almost certainly gone under.

Another legacy dud dates back to former CEO Jack Welch’s entry into the insurance business. Although most of that business has been sold off, it still managed to lose $6.2 billion in the fourth quarter of 2017.

The result of this epic mismanagement has been to wipe out over $1 trillion in market capitalization. The shares have plunged some 66%, from $32 to $11.

At the urging of major shareholders a long-suffering board ousted GE’s latest CEO, John Flannery, after only a year in the job and replaced him with former Danaher (DHR) CEO Lawrence Culp. The move may have finally put a bottom in the stock.

It’s obvious what GE has to do here. It needs to liquidate the remaining money losing assets that have been such a huge drain on cash flow.

It could also sell a few other successful business lines at big premiums that are money makers, just as jet engines or its Baker Hughes oil subsidiary. These days investors are paying up for almost everything.

I don’t know how long it will take Culp to work his magic. However, I bet the stock market will start to sniff out a turnaround sometime in the next year and a half.

The GE January 17, 2020 $15-$18 vertical bull call spread (called a LEAP because it has a maturity of more than one year) is currently priced at 55 cents.

If the shares make it back up to $18, the price it traded at in January, the LEAP would be worth $3.00, delivering you a gain of 345%. It makes a very low risk, high return set up for investors tired of paying new all-time highs for everything else.

Whatever happened to Jack Welch, who originally created this disaster? Jack retired a billionaire and is now giving lectures on corporate managements. Go figure.

I’ll try to come up with another interested LEAP idea tomorrow. I know you’re all starved for them.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/GE-broken-logo.png364644MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-03 09:02:062018-10-02 18:07:26Taking a Look at General Electric (GE) LEAPS

Pat yourself on the back if you pulled the trigger on Square (SQ) when I told you so because the stock has just lurched over an intra-day level of $100.

It was me aggressively pushing readers into buying this gem of a fin-tech company at $49. To read that story, please click here (you must be logged in to www.madhedgefundtrader.com).

Since then, the price action has defied gravity levitating higher each passing day immune to any ill-effects.

The Teflon-like momentum boils down to the company being at the cross-section of an American fin-tech renaissance and spewing out supremely innovative products.

At first, Square nurtured the business by targeting the low hanging fruit– small and medium size enterprises in dire need of a strong injection of fin-tech infrastructure.

It largely stayed away from the big corporations that adorn billboards across the Manhattan skyline.

That was then, and this is now.

Square is going after the Goliath’s fueling a violent rise in gross payment volume (GPV).

Modifying themselves for larger institutions is the next leg up for Square.

They recently inaugurated Square for Restaurants for larger full-service restaurants.

Business owners do not need technical backgrounds to operate the software and integrating Caviar into this program emphasizes the feed through all of Square’s software.

Dorsey has built an ecosystem that has morphed into a one-stop shop for comprehensively running a business.

Migrating into business with the premium corporations offers an opportunity to augment higher margin business.

This is the lucrative path ahead for Square and why investors are festively lining up at the door to get a piece of the action.

The downside with an uber-growth company like Square are lean profits, but they have managed to eke out three straight quarters of marginal spoils.

However, the absence of profits can be stomached considering the total addressable market is up to $350 billion.

Grabbing a chunk of that would mean profits galore for this too hot to handle company.

Expenses are always a head spinner for Silicon Valley firms and attracting a dazzling array of engineers to spin out breathtaking profits can’t be done on the cheap.

The Cash app download figures are sizzling and is one of the most popular apps in the app store.

Square’s marketing strategy is also turning a corner getting out their name leading to sale conversions.

These are just several irons in the fire.

The last two years has seen this stock double each year, could we be in for another double next year?

If measured by growth, then I see why not.

Growth is the ultimate acid test deciding whether this stock will be dragged down into the quick sand or let loose to run riot.

Other second-tier tech firms in the middle of a sweet growth spot pack a potent punch like Spotify (SPOT) and Grubhub (GRUB) which are growing annual sales around 50-60%.

Material profits are also irrelevant for the aforementioned tech juggernauts.

Square is expanding at the same fervent pace too, and the hyper-growth only makes payment processors like Visa (V) quasi-jealous of such staggering numbers.

And when Square trots out numbers to the public like that with (GPV) shooting out the roof, the stock does nothing but go gangbusters.

Either way, Square has popularized making credit card payments through smartphones and that in itself was a tough nut to crack amongst tough nuts.

Square also has a line-up of impressive point-of-sales products such as Caviar.

In fact, merchant sellers are adopting an average of 3.4 Square software apps with invoices, loans, marketing, and payroll software being the most beloved.

Square also offers other software that can handle back office tasks and manage inventory.

The software and services business is on pace to register over $1 billion in sales in 2019.

The breadth of functions that can boost a company’s execution highlights the quality of software Dorsey has produced.

I always revert back to one key ingredient that all tech companies must wildly indulge in to fire up the stock price – innovation.

Innovation in bucket loads is something all the brilliant tech firms crave such as Microsoft (MSFT), Amazon, and Salesforce (CRM).

Overperformance starts from the top and trickles down to the people they hand pick to manage and run the businesses.

Jack Dorsey is right up there with the best of them and his influence cannot be denied or ignored.

His stewardship over his other company Twitter (TWTR) is sometimes worrisome because of a pure scheduling conflict, but it’s obvious which company is having a better year.

Square steers clear of the privacy and regulatory minefields handcuffing Twitter.

And it could be safely assumed that Dorsey enjoys his afternoons more at Square than his mornings across the street at Twitter where he is bombarded by heinous problems up the wazoo.

When you conjure up an up-and-coming company that could rattle the establishment, Square is one of the first companies that comes to mind.

Some analysts even argue this company deserves to be lifted into the vaunted Fang group.

I would say they are on their merry way but they just aren’t big enough to command a spot on the Fang roster.

I have immense conviction this stock will be a deep influencer of our time, and its diversified software offerings add limitless dimensions underpinning massive revenue streams.

In Q2, the subscription revenue grew 127% YOY underscoring the success the software team is having, crafting productive apps applicable to business owners.

Business owners can even take out a loan through Square Capital which issues micro-loans to small business owners.

In need of financing? Ring up Dorsey’s company for a few quid.

Starkly contrasting Square in the payment processors space is Visa (V).

Visa is not a hyper-growth company going ballistic, but a stoic behemoth unperturbed.

The 3.283 billion visa cards that adorn its insignia represents scintillating brand awareness and efficiency.

When Tim Cook was asked if Apple (AAPL) plans to disrupt Visa, he smirked and said, “People love their credit cards.”

This is a prototypical steady as she goes-type of company.

They do not offer micro-loans to small businesses or dabble with any of the murky sort of products that can be found on the edge of the risk curve.

They are a safe and steady pure payment processor.

Its network can digest 65,000 transactions per second and is universally cherished as a brand around the world.

All of this led to an operating margin of 66% in 2017.

Square has identified other parts of the payment process to snatch and do not directly compete with Visa.

They partner with Visa and pay them a processing fee.

Subsequently, Square is paid a merchant fee after the payment is approved.

Visa has a monopoly and a moat around their business as wide as can be.

Square is a different type of beast – growing uncontrollably and hell-bent on spawning a revolutionary fin-tech paradigm shift.

The question is can Square eventually turn payment heavyweights like Visa on its head?

The path is fraught with booby traps and as Square generates the projected sales and bolsters its revenue, it could start to encroach on these legacy processors too.

Yet, it’s too early to delve into that threat yet.

Enjoy the ride with Square and better to lay off this potent stock until a better entry point presents itself.

This stock will go higher. Giddy-up!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-03 09:01:422018-10-03 08:59:28Our Home Run On Square (SQ)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.