The Five Most Important Things That Happened Today

(and what to do about them)

1) Mueller Report has No Market Impact, with the Dow Average up a scant $14.51. No Bombshells here. It’s “RISK ON.” Buy the dips. Click here.

2) Apple Announces its New Streaming Service, Apple TV Plus, and the stock falls on a “sell the news” drop. Roku is included in the package, so buy (ROKU). The Apple offering is weak enough to allow plenty of room for Disney to launch its own streaming service, Disney plus, at the end of this year. Prepare for an onslaught of princesses. Buy (DIS) too. Click here.

3) The Existing Yield Inversion is Fake. Real yield inversions crush stock markets when short term rate soar, not collapse, so the bear market is on hold. Foreign investors have already figured this out and are pouring money into US stocks. It’s “’RISK ON” baby. Click here.

4) Home Price Appreciation Hits a Four-Year Low, with the S&P Case Shiller National Home Price Index growing only 4.2% YOY in January, down from 4.6% the previous month. Las Vegas, Phoenix, and Minneapolis are still showing the biggest gains while San Francisco and Seattle are seeing the biggest price drops. Avoid homebuilder (ITB). Click here.

5) Housing Starts Drop 8.7%, in February. Yes, falling prices will have that effect on a market. Avoid homebuilders more. Waiting to buy at the coming bankruptcy auctions. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(WHY I’M SELLING SHORT TESLA SHARES),

(TSLA)

(PINTEREST COMES OUT)

(PINS), (FB), (AAPL), (GOOGL), (AMZN)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-26 12:35:042019-03-26 12:35:04Mad Hedge Hot Tips for March 26, 2019

The news is out that new Tesla (TSLA) new car registrations in the major states are falling off a cliff. California, New York, and even Texas are the major culprits.

The company says the ramp up in mass production of the Tesla 3 is the main reason, and that car registrations, in any case, are a deep lagging indicator. (No kidding! I bought a Model X P100D in Nevada in November and it is still not registered).

Analysts say it is because the electric car subsidy was chopped in half by the Trump administration this year from $7,500 to $3,750 per vehicle, and it is going to zero next year, thus demolishing the Tesla 3 market for entry-level low-end buyers. They also point to the company’s fragile financial condition which could be going bankrupt at any time.

For whatever reason, I believe that the shares will break two-year support on the charts and plunge to new lows. At the very least, Tesla shares are capped for the time being.

I, therefore, sold short Tesla shares yesterday.

As much as this looks like a great short-term trade, I love Tesla long term and see it as a potential ten bagger from current price levels. Tesla will become the world’s largest car company within a decade and become the first car company with a $1 trillion market valuation.

As long as I have been following Tesla since the early venture capital days, it has been going bankrupt. It was going bankrupt during the move in the share price from $16.50 to $394, and it is going bankrupt today.

When I pulled up to the Fremont factory last week, I couldn’t believe what I found. There was a version 3 supercharger that would top up my battery at the staggering rate of 1,000 miles an hour!

That meant that with 50 miles of range left on my 300-mile range Model X battery, I could get a full charge in 15 minutes! The electric power was coming down the cable so fast that it had to be liquid-cooled.

I pinched myself to make sure I hadn’t fallen into a Star Trek movie. The V3 supercharger will soon be available across the country. No other car company is close to achieving something like this.

The fact is that I have been subjected to an unrelenting torrent of bad news, rumors, and envy since I first bought the shares at $16.50 ten years ago. This is the most despised company in the universe and regularly sits among the top five companies with the greatest short interest, often above 25%.

But I guess this is what happens when you take on big oil, the Detroit big three, the advertising industry, labor unions, and the entire Republican party all at once. By my calculation, Tesla is a disruptive threat to about 50% of the US GDP all at once.

I ignore them all and just look at the numbers. Here they are.

1) Tesla has increased its total production from 125 when I bought my first Model S1 in 2009 to 245,519 in 2018. It should hit 500,000 by the end of this year when the Shanghai factory comes online. They have gone from employing 100 people to 50,000.

2) With the completion of the Sparks, NV Gigafactory, battery prices are collapsing and are now 50% cheaper per mile than any other competitor, 4.1 miles per kWh versus 2.5 miles.

3) Tesla’s costs for batteries have cratered from $1,000 per kWh ten years ago to $100 per kWh today and are expected to drop to $75 per kWh in a few years. Below $100 per kWh Teslas are cheaper to run than conventional gasoline-powered cars, even without the tax subsidy.

4) Tesla now makes half the lithium batteries in the world, and that figure is growing by 50% a year.

5) Tesla’s vast national charger network will soon become the country’s largest electric power utility and that will also become an enormous money-spinner. They just raised prices to 30 cents per kWh versus a cost of 5 cents. Assuming that 5 million cars buy a 70-kWh charge three times a week, that works out to a $13.65 billion a year profit.

6) Anyone who actually reads Tesla’s balance sheet can see that the company is now spinning off $1 billion in free cash flow. It is investing in new plant and equipment at a prodigious rate.

7) With a market capitalization of $44.5 billion, Tesla just trails General Motors (GM) at $51 billion, but surpasses Ford Motors at $34 billion, and therefore can raise new capital to finance its hyper-growth any time it wants.

More product at high prices at a prodigiously falling cost sounds like a pretty good business model to me. Oh, and climate change is about to become the top political issue for the 2020 presidential election. Who is the big winner in that case?

Tesla.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/05/John-with-Tesla-e1463435153171.jpg385400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-26 10:06:552019-07-09 04:00:02Why I’m Selling Short Tesla Shares

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-26 08:57:522019-03-26 08:57:52March 26, 2019 - MDT Pro Tips A.M.

The Facebook (FB) of digital images is on deck and has filed to go public.

I'll give you the skinny on it.

Pinterest (PINS) has slightly different lingo - they call digital images pins, a collection of pins, a pinboard, and the users that post pins are pinners.

Aside from this little creative wrinkle, Pinterest does little to help flow my creative juices.

That's not to say they are a bad company, in fact, it's quite refreshing that on the financial side of the equation, Pinterest is a solid financial enterprise.

They make money and aren't going to burn through their cash reserves anytime soon.

This should give some peace of mind to potential investors looking at snapping up shares of Pinterest.

Even though they are not a bad company, I cannot promote them as a firm revolutionizing technology in the way we know it, they certainly don’t, and never will, at least at the current pace of innovation.

Pinterest derives almost 100% of its revenue from digital ads à la Facebook, they do not sell anything and much like Facebook, the user is the product by way of mining private data and selling them over to third-party ad agencies who subsequently sell targeted ads on Pinterest’s platform.

As I read through Pinterest’s S-1 filing with the SEC, an overwhelming portion of the content is reserved for the litany of regulatory risks that serving digital ads, curating others' content, and the international risks that pose to Pinterest growth story.

As with most tech growth stories, this particular narrative must orbit around the strength of incessantly growing its domestic and international user base.

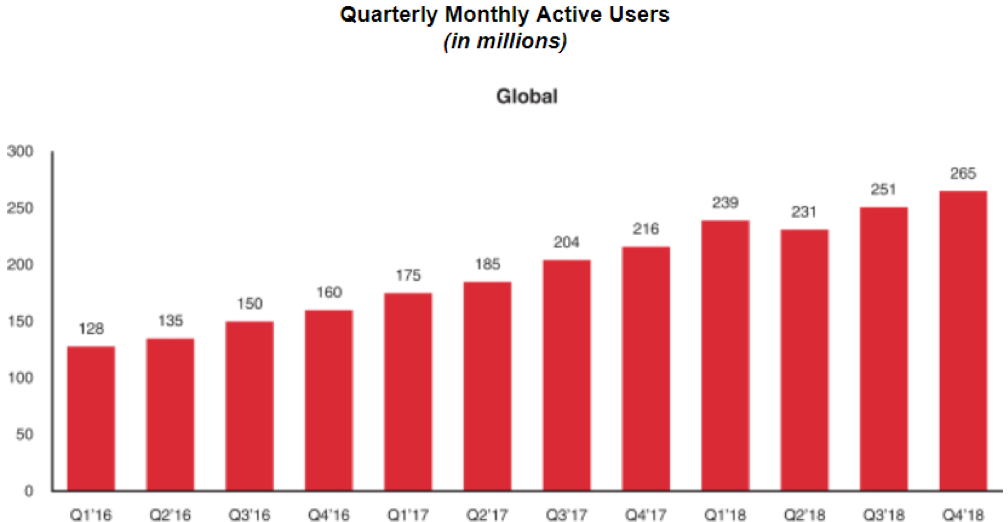

I surmise that part of the reason they desire to go public is because of the 265 million in global quarterly monthly users have reached the high watermark.

Therefore, this calculated risk of going public is entirely justified as the cash out for the venture capitalist and private owners that invested in this company as a burgeoning toddler.

Or the owners see catastrophic downside from the regulatory landscape which has been increasingly volatile in the past few quarters and wish to get out as soon as they can.

Let's make no mistake about this, Pinterest does not control its own destiny, and their success will be based upon external factors that they cannot control.

Some of these factors have already reared their ugly head, the most relevant example was when Google (GOOGL) changed its image search algorithm which disrupted Pinterest’s image function.

This was an example of third-party content originators clamping down on their willingness to allow Pinterest to populate content on their proprietary platform, and the lack of availability of content or the decreasing nature of it will sting the hope of increasing web traffic on Pinterest going forward.

Pinterest has clearly disclosed in its IPO filing that they are reliant on crawling third-party search engine services for third-party photos, this content is curated into their platform and credited to the original user.

I would classify this type of technology as unimpressively low grade and Pinterest will be susceptible to many more possible disruptions in the future.

In layman terms, if the stars do not align, Pinterest will be the first to feel it, and strategically speaking, this is a poor position to strategically operate from.

If Pinterest cannot serve the specific content that incites the tastes of pinners, this could destroy retention and engagement rates leading to a damaging downdraft of ad revenue.

Pinterest's feeble business model will certainly call for new investments in and around more innovative parts of technology.

What we have seen most successful technology companies flirt with are full-fledged recurring revenue models, and bluntly, Pinterest does not have one.

The likes of Microsoft, Amazon, Google, and Apple have pivoted hard towards this subscription model proving they can have their own cake and eat it too.

Funnily enough, Pinterest pays AWS, Amazon’s cloud arm, an extraordinary amount of money to store the pins or digital images on AWS Cloud platform to the tune of almost $800 million per year showing how beneficial it is to be on the other side of the equation.

Pinterest does benefit from a robust brand reputation and its footprint in America is quite large.

However, one group of potential customers have clearly been left out in the cold - Males.

The firm has been famous for being the go-to image platform for young mothers and generally speaking, American women born in the 1980s.

According to data analytics, it appears that content that males gravitate towards is not present on the platform and will need to be addressed going forward to grow users.

Another crucial problem that must be addressed is the lack of domestic growth in the user base.

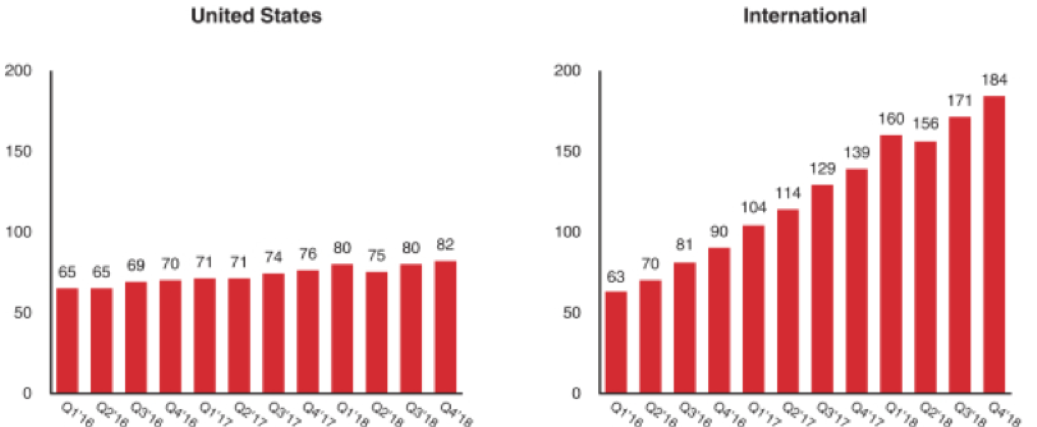

In Q1 2018, Pinterest achieved 80 million monthly active users, however, fast forward to Q4 in 2018 and the number had barely inched up to 82 million monthly active users.

From Q1 to Q2, there was a dramatic deceleration in the number of monthly active users falling by 5 million to 75 million monthly active users.

The company blamed this on Facebook changing their password security causing users who rely on Facebook passwords and username entrance data to be temporarily stonewalled from entering Pinterest.

Millions decided to avoid the hassle and just stop using Pinterest because they were unable to enter the platform, causing major carnage to Pinterest’s ad-supported revenue model because of the hemorrhaging usership.

Unfortunately, bigger platforms such as Facebook and Google are not responsible to telegraph these structural changes in policy to Pinterest which means that this type of loss of usership could be a bi-annual or annual exercise in damage control.

Losing 10% of your user base based on someone else’s systemic changes is a bitter pill to swallow.

Investors must ask themselves why a premium search engine like Google search want to allow Pinterest to continue to curate its images for ad revenue effectively skimming off of Google’s top line?

As you have seen, Google has hijacked many of these types of business initiatives by taking on these opportunities themselves, dismantling the choke points, and going in for the kill.

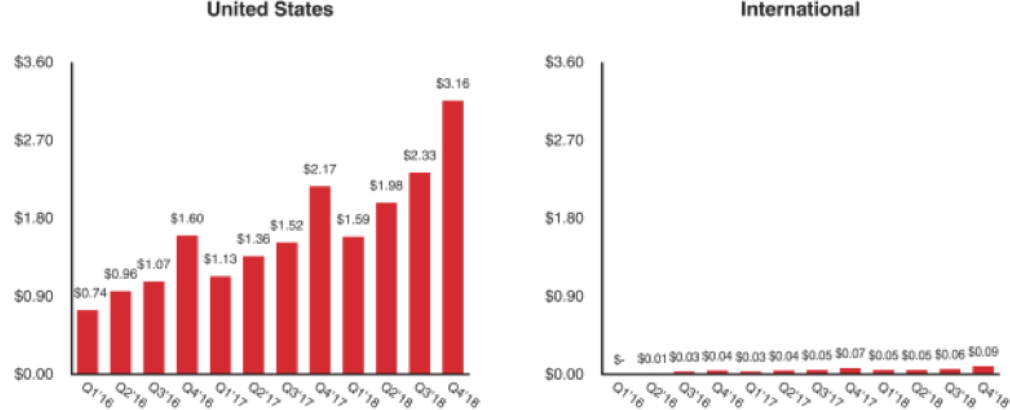

The main avenue of user expansion is its international audience, and sadly, the average revenue per international user is a paltry $0.09. This number was up sequentially from the prior quarter which was $0.06.

If you compare the revenue per user with America, then it's easy to understand why the company wants to go public now.

Management presided over a sequential increase of American revenue per user from $2.33 to $3.16 in the prior quarter and the same growth will be hard to maintain and replicate spurring the higher-ups to cash out.

International growth is staring down a barrel of a gun with restricted access by governments who do not allow this type of service in their countries such as China, India, Kazakhstan, and Turkey.

The impact of these broad-based bans decodes into Europe being the only possible answer to user growth in revenue terms and total usership.

To state that Pinterest is confronted by widespread global risk is an understatement.

However, the low-hanging fruit would be squeezing more revenue out of the American user and I would guess that the ceiling would be around $7 per user in the near-term.

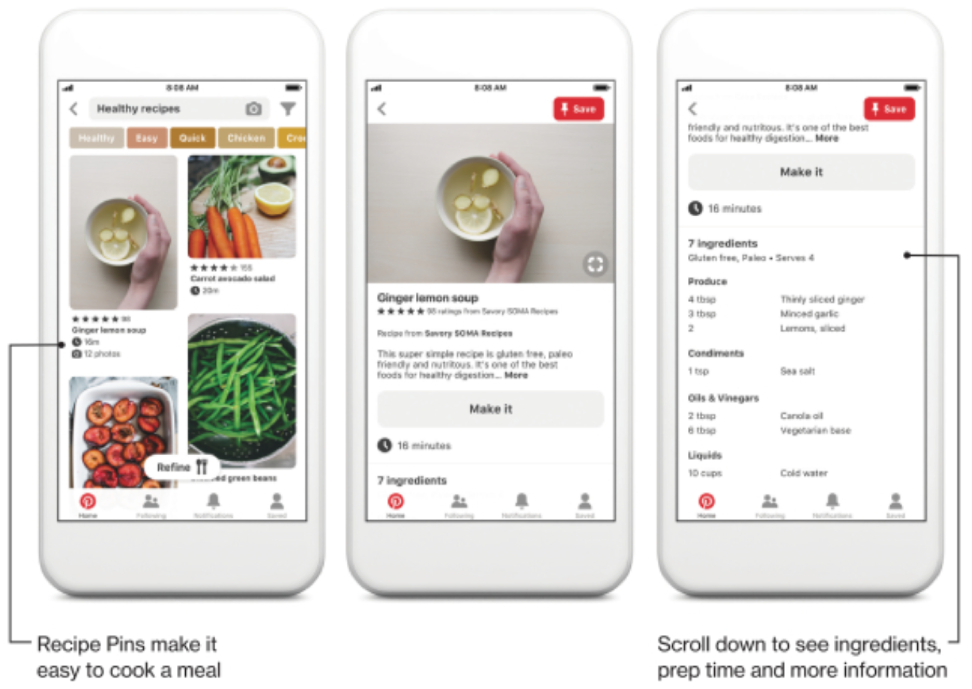

If management hopes to eclipse the $7 per American user, they will have to migrate into more data generative strategies such as video.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/Pinterest.png497743Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-26 07:06:212019-07-10 21:38:43Pinterest Comes Out

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-25 15:38:322019-03-25 15:39:13Trade Alert - (AMZN) March 25, 2019 - BUY

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-25 13:05:442019-03-25 13:06:08Trade Alert - (TSLA) March 25, 2019 - BUY

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-25 11:38:572019-03-25 13:07:00Trade Alert - (TLT) March 25, 2019 - BUY

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-25 11:09:322019-03-25 11:09:32March 25, 2019 - MDT Alert (NVDA)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.