Mad Hedge Biotech & Healthcare Letter

November 5, 2019

Fiat Lux

Featured Trade:

(DIALING FOR DOLLARS WITH TELEHEALTH),

(TDOC)

Mad Hedge Biotech & Healthcare Letter

November 5, 2019

Fiat Lux

Featured Trade:

(DIALING FOR DOLLARS WITH TELEHEALTH),

(TDOC)

Healthcare consumers are experiencing a crisis. Over the past years, America has transformed into a country with the most expensive costs of care in the world with the American Medical Association reporting that the average spending of one person reaches $11,000 annually.

While this situation obviously burdens the consumers, looking at it from an investment perspective reveals just how much health insurers could stand to profit from it.

For instance, Anthem (ANTM) stock actually rose over 100% in the past three years, thanks to moderate revenue gains and huge bottom line profits. As enticing as that sounds, there are still healthcare companies out there aiming to keep the costs reasonable and the service convenient. One of them is Teladoc Health (TDOC).

Teladoc is a telehealth company that offers health services and medical advice to patients over the phone or via video conference calls. Although this is by no means a replacement of the traditional visits with your healthcare providers, the technology expands the reach of specialists especially when it comes to consultation services. It also provides a convenient platform for patients who will no longer need to actually make a trip to their doctors.

Most importantly, telehealth allows care providers to offer their services at lower prices. So far, spending on telehealth services is estimated to reach roughly $30 billion -- a staggering decrease from the multi-trillion-dollar amount Americans spend on healthcare services every year.

In the next five years or so though, the spending on telehealth services is anticipated to increase by approximately 20%. This could bring spending on this industry to a whopping $100 billion annually. Here is where Teladoc’s competitive advantage comes in.

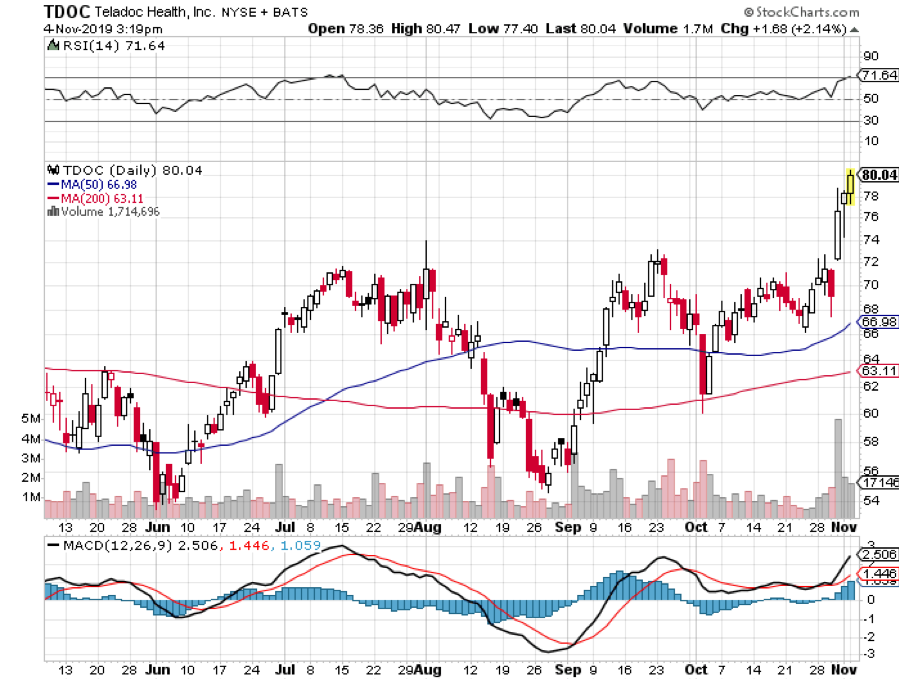

At the moment, Teladoc is one of a handful of providers that actually has a global presence. The company is available in 130 countries and accessible in 30 languages. With such a broad market, Teladoc revenues showed an 89% increase year over year in 2017 and 79% in 2018. Meanwhile, the first half of 2019 saw the company’s profits hit a 40% increase year over year, with total patient visits rising 73% to reach 1.97 million.

Teladoc has also invested in promising acquisitions. Its $440 million merger with competitor Best Doctors back in 2017 has proved to be a great way to expand quickly and cover more ground.

For the third quarter of 2019, Teladoc once again delivered good results. The company’s revenues increased by 24% to reach $138 million, which surpassed Wall Street’s estimate of $136.5 million. Paid memberships in the United States grew by 55%, which now puts the total at 35 million members.

For its fourth-quarter earnings report, the company is expected to keep the momentum and rake in roughly $149 million to $153 million in profits, with a 2019 full-year revenue to be somewhere between $546 million and $550 million.

Despite the promising performance of Teladoc so far, there are still risks to consider before buying the stock. One of the major concerns is competition. Although Teladoc retains the title of being the leader in the telehealth services industry today, competitors American Well, Grand Rounds, and MDLive are gaining traction as well. Nonetheless, name recognition alone sets Teladoc apart from its rivals. However, the entrance of Amazon via its Amazon Care initiative in September is considered a major threat to the company.

All in all, Teladoc stock remains attractive. As with practically everything in investing, the key is to exercise due diligence and diversifying your portfolio. Teladoc is not a perfect company, but its sheer presence is already disrupting the healthcare industry. This makes the stock a good addition to a diversified portfolio, and the fact that you could be one of the pioneering investors makes it all the more exciting to own.

BUY (TDOC) on the next dip.

Global Market Comments

November 5, 2019

Fiat Lux

Featured Trade:

(THE HARD TRUTH BEHIND BUYING IN NOVEMBER),

(NOTICE TO MILITARY SUBSCRIBERS),

Global Market Comments

November 4, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE SUMMIT)

(GM), (BA), (MSFT), (SPY), (TLT), (TSLA), (AMZN)

In 1976, I joined the American Bicentennial expedition to climb Mount Everest led by my friend and mentor, Jim Whitaker. Since I was a late addition, there was no oxygen budget for me which, in those days, was very heavy and expensive.

Still, I was encouraged to climb as far as I could without it, which turned out to be up to Base Camp II at 21,600 feet. At that altitude, you couldn’t light a cigarette as the matches went out too quickly. There just wasn’t enough oxygen.

Out of 700 men on the team, including 600 barefoot Nepalese porters, only two made it to the top. By the time I made it back to Katmandu 150 miles away, I had lost 50 pounds, taking my weight down to a scarecrow 125.

You can see the metaphor coming already.

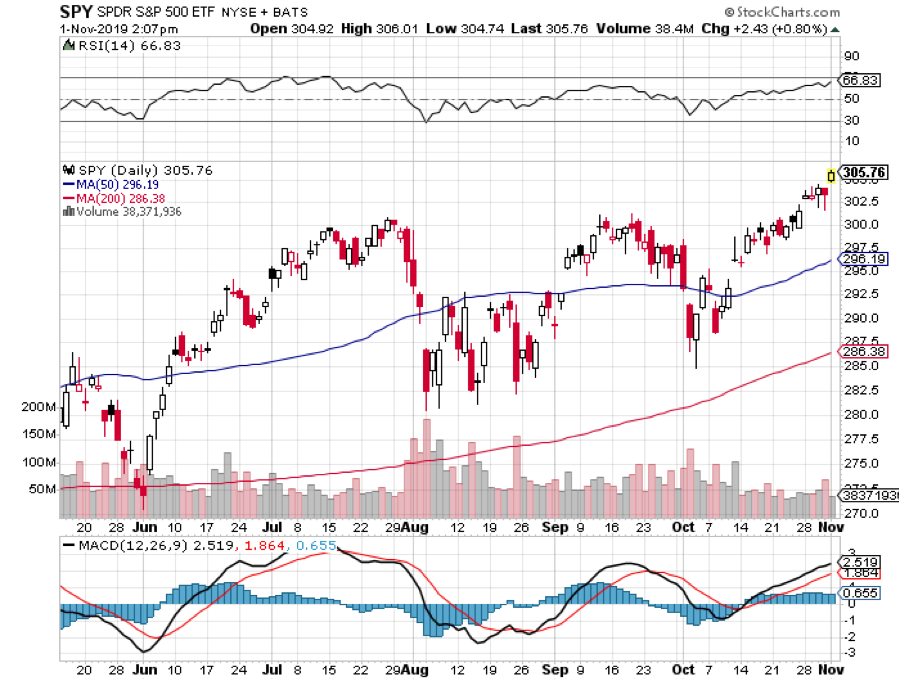

Here I am at my screen looking at 27,500 in the Dow Average and not only am I gasping for oxygen, I am ready to pass out. My Mad Hedge Market Timing Index hit a new high for 2019 at an acrophobic 85. All of this is happening in the face of slowly eroding fundamentals and a global economic slowdown.

Could the market go higher? You betcha! At least a couple percent more by yearend. Market bottoms are easy to identify when valuations hit decade lows. Market tops are impossible to gauge because greed is unquantifiable and knows no bounds.

I’ll give you a perfect example. The US and Japan signed the Plaza Accord in 1985 calling a doubling of the value of the yen against the dollar and the eventual transportation of half of Japan’s auto production capacity to the US. We all knew this would eventually destroy the Japanese economy. Yet the Nikkei Average rose for five more years until it finally crashed.

Of course, the impetus for all of this are artificially low-interest rates, which dropped 25 basis points again last week for the third time this year.

There were with two dissents, while the December rate cut futures fall to 20%. If we get Japanese levels of interest rates, we might get a Japanese type 30-year stagnant economy.

US Q3 GDP came in at 1.9% in its most recent report, better than expected, but we are still in a serious downtrend. The economy is most likely running at a lowly 1.5% rate now. Weakness is a sure thing, now the government has run out of money for special projects. Don’t count on more with a Democratic house. It’s not the bed of roses I was promised.

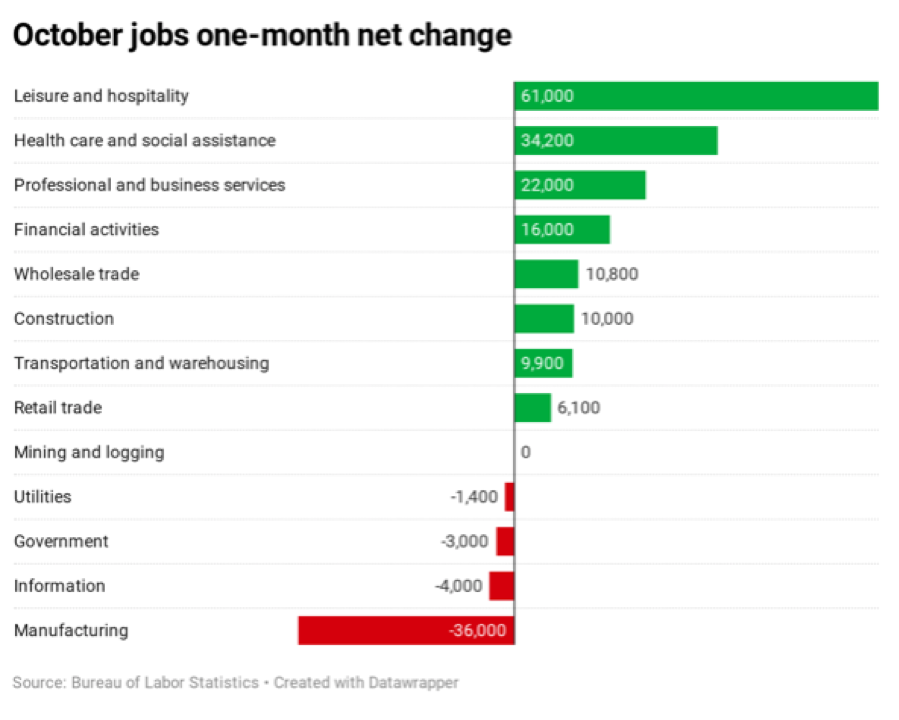

However, if there is trouble, you won’t see it in the employment data. The October Nonfarm Payroll Report surprised to the upside, at 128,000. Many expected much worse in the aftermath of the GM (GM) strike and Boeing (BA) grounding.

The headline Unemployment Rate ticked up 0.1% to 3.6%. The big gains were in Hospitality and Leisure, up a stunning 61,000, Health Care & Social Assistance, up 31,000, and Professional and Business Services, up 22,000. Manufacturing lost 36,000 jobs, a ten-year high. 20,000 temporary jobs were lost from the 2020 census wind down.

August and September were revised up by an unbelievable 95,000. The market loves these numbers.

Tesla shocked, bringing in a profit for only the third time in company history, and causing the stock to soar $55. The 100,000-unit production target within yearend looks within reach. Most importantly they opened up a new supercharger station in Incline Village, Nevada!

Tesla is now America’s most valuable car maker, beating (GM). The ideological Exxon-financed shorts have been destroyed once and for all. Buy (TSLA) on dips. There’s still a ten bagger in this one.

Amazon put out a gloomy Christmas forecast on the back of a disappointing earnings report, crushing the shares by 7%. Looks like the trade war might cause a recession next year. Q3 revenues were great, up 24% to an eye-popping $70 billion.

Good thing I took profits on the last option expiration. Poor Jeff Bezos, the abandoned son of an alcoholic circus clown, dropped $7 billion in net worth on Thursday. Buy (AMZN) on the dips.

The safest stock in the market, Microsoft (MSFT), says it’s all about the cloud. Azure revenues grew a stunning 59% in Q3. (MSFT) is now up 37% on the year. Keep buying every dip, if we ever get another one.

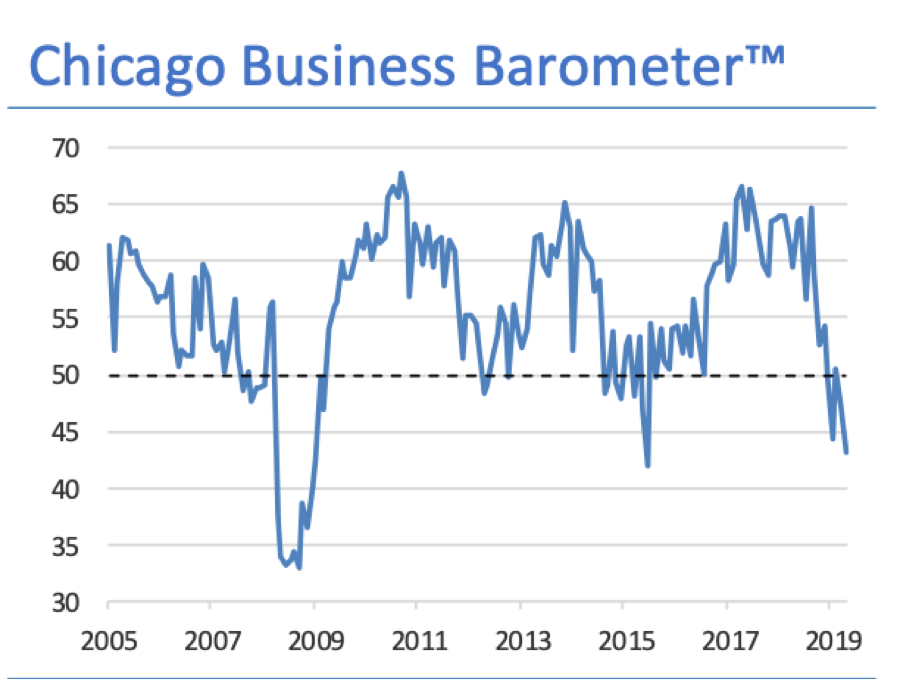

The Chicago PMI crashed, plunging from to 43.2, a four-year low. This horrific number was last seen during the recession scare of 2015. New orders have virtually disappeared, or order backlogs have vaporized. Inventories are soaring. This is the worst economic report this year and will cause a lot of economists’ hair to catch on fire.

This was a week for the Mad Hedge Trader Alert Service to stay level at an all-time high. With only two positions left, in Boeing (BA) and Tesla (TSLA), not much else was going to happen.

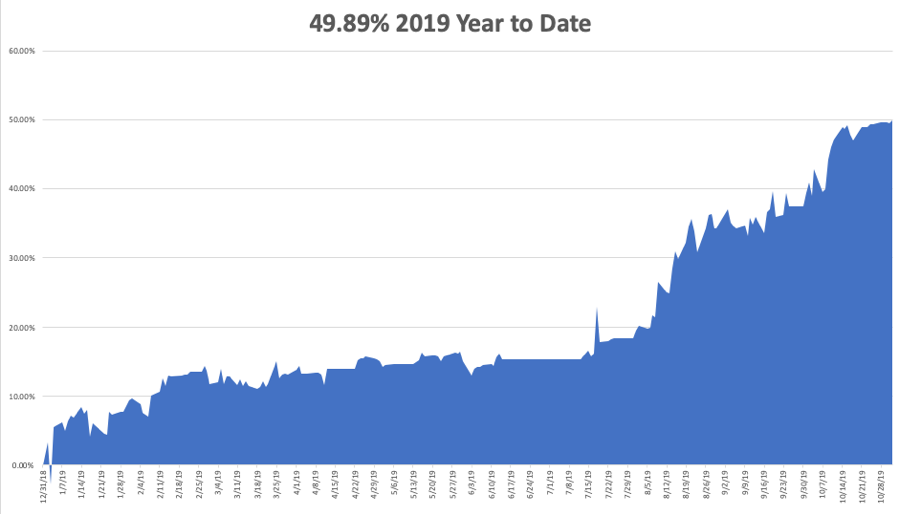

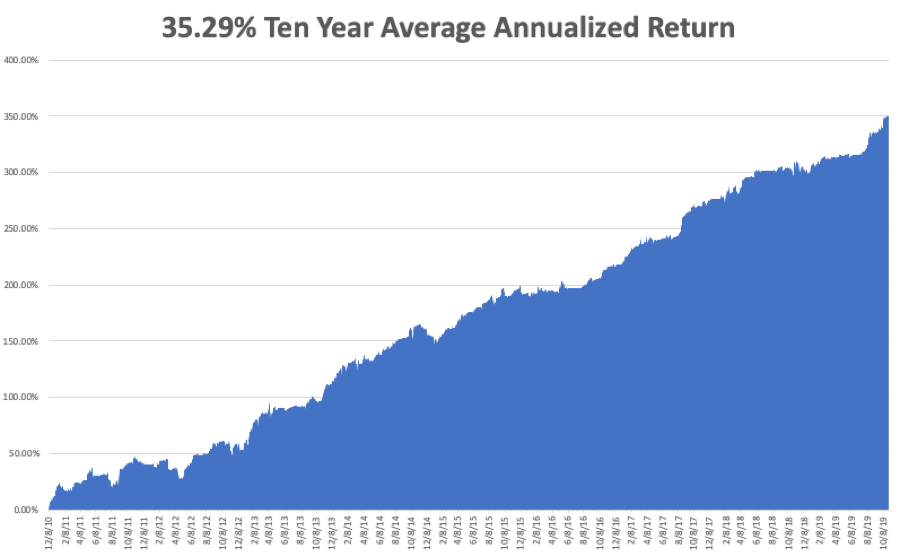

My Global Trading Dispatch reached new pinnacle of +350.03% for the past ten years and my 2019 year-to-date accelerated to +49.89%. The notoriously volatile month of October finished at +12.23%. My ten-year average annualized profit held steady at +35.29%.

The coming week is pretty non eventful of the data front after last week’s fireworks. Maybe the stock market will be non-eventful as well.

On Monday, November 4 at 8:00 AM, US Factory Orders for September are out. Uber (UBER) and Under Armor (UAA) report.

On Tuesday, November 5 at 8:00 AM, the October ISM Nonmanufacturing Index is published. US API Crude Oil Stocks are released at 2:30 PM EST. Peloton (PTON) reports.

On Wednesday, November 6, we get a raft of Fed speakers unrestrained by any impending meetings. QUALCOM (QCOM) and Humana (HUM) report.

On Thursday, November 7, there are a heavy duty series of bond auctions. Walt Disney (DIS) and Zoetis (ZTS) Report.

On Friday, November 8 at 8:00 AM, the University of Michigan Consumer Sentiment Indicator is learned.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am heading for Santa Cruz, California for the weekend to get out of the smoke and do some serious backpacking. I might even try to squeeze in a surfing lesson there. I’ll never give up.

By the way, several guests at the Tahoe conference remarked on the prominent scar on the side of my nose. That was caused by an ice ax that plunged straight through it in a fall while climbing Mount Rainer in 1967. Who patched it up and got me back down to the bottom? My friend Jim Whitaker.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

November 4, 2019

Fiat Lux

Featured Trade:

(THE CHICKENS COME HOME TO ROOST WITH SMALL TECH),

(AAPL), (MSFT), (AMZN), (GOOGL), (WDC), (TXI), (ANET), (PINS)

The tech story is still intact, but the edges are losing its shine.

That is the takeaway from the recent slew of earnings reports from many of the prominent yet second-tier tech companies.

On one hand, companies like Apple (AAPL) have been holding the fort as it blasts through to new highs even amid the backdrop of the Chinese trade war that has dragged many of the strong tech names into the mud.

What we did see lately was a magnificent swan dive by chip names like Western Digital (WDC) and Texas Instruments (TXI) which were blindsided by 10-15% haircuts because of lackluster guidance.

The agony didn’t stop there with second rate cloud names like Pinterest (PINS) and Arista Networks, Inc. (ANET) reaching for scapegoats for their weak guidance. These took instant 20% haircuts.

The problem with smaller stocks like these besides having narrower spreads, they are slaves to just a few contracts and when one goes, their guidance and revenue estimates implode in their faces.

Arista slid more than 25% on news that they expect quarterly revenue of $540 million-$560 million, with the midpoint about 20% below the previous Street consensus at $686.2 million.

Arista CEO Jayshree Ullal said in a statement that the company expects “a sudden softening in Q4 with a specific cloud titan customer.”

That is Facebook who comprise about 10% of Arista’s revenue composition because Facebook has pulled back the reigns on cloud spend to cut costs amid a murky global backdrop and regulatory minefield.

Unfortunately, second tier cloud names must accept that they do not offer the best pricing when directly competing with the superior cloud names of Google Cloud, Microsoft Azure, and Amazon Web Services (AWS) because they simply can’t scale as well to the extent these monopolistic FANGs can.

Data storage often comes down to whoever has the cheapest cost of capital to pile into server farms allowing pricing to be ultra-cheap and these three companies win out.

If these firms lose one contract like Walmart’s switch over to Microsoft Azure from Amazon, it’s not a big deal.

It doesn’t put a 10% black hole in the revenue stream like for Arista.

Pinterest was one of the most overhyped IPOs of 2019 promising growth, growth and more growth.

Its digital ad business needs to deliver accelerating growth for its share price to rise and when the latest earnings report showed year-over-year growth slow from 62% to 47%, investors saw the writing on the wall.

The company only grew its users 8% in the lucrative North American market and 38% abroad.

But the foreign markets were tainted by the gruesome underbelly of earning only 13 cents per foreign users.

There is user growth but at the cost of an inferior quality of growth.

Analysts can clearly observe the accelerated erosion of Pinterest, and I can say from a personal point of view that the website isn’t that useful.

Management’s excuse was a tough comparison to the prior year but if a growth firm has a superior model, they should be able to grow past any minor problems if the secular trends stay hemmed in.

Weak excuses now and probably weak excuses next quarter as the global tech landscape gets squeezed even more at the periphery.

What does this all mean?

There has been a flight to tech quality into the Teflon names like Microsoft and Apple.

Names that are showing growth headaches saddled with too much competition and structural softness are getting killed.

Don’t even think about investing in the marginal names like Pinterest and Arista.

Better to be safe on your perch inside the moat than outside isolated from the drawbridge.

Not all tech is created equal and it's rearing its ugly face in a frothy market.

“I'd rather Apple cannibalize Apple than somebody else cannibalize Apple.” – Said Current CEO of Apple Tim Cook