Mad Hedge Biotech & Healthcare Letter

December 24, 2019

Fiat Lux

Featured Trade:

(TAKING A SECOND LOOK AT SANOFI),

(SNY), (NVO)

Mad Hedge Biotech & Healthcare Letter

December 24, 2019

Fiat Lux

Featured Trade:

(TAKING A SECOND LOOK AT SANOFI),

(SNY), (NVO)

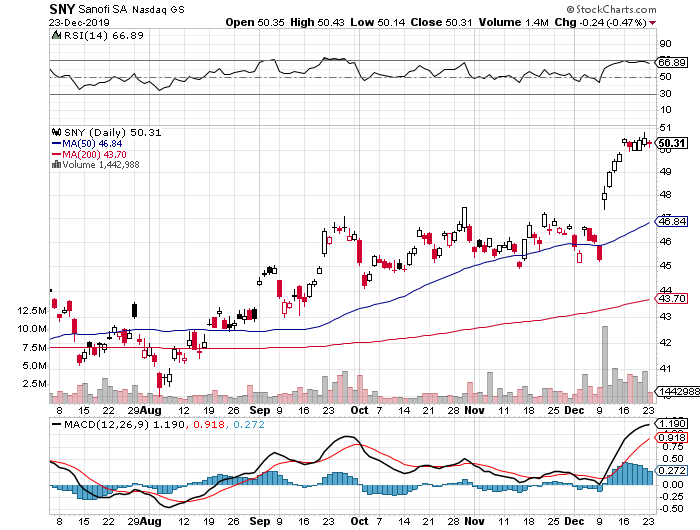

Investors on the lookout for a large-cap biotech investment have several options, with Sanofi SA (SNY) being one of the most interesting companies to consider. The French multinational pharma giant has a diverse drug portfolio which has been attracting attention recently thanks to its focus on the lucrative market of diabetes treatments.

Unfortunately, the diabetes project hasn’t been working as well as Sanofi hoped this year. Earlier in 2019, FDA rejected the company’s new diabetes candidate Zynquista. Despite this setback, the company announced more promising Phase 3 results from another diabetes treatment, Toujeo, which is aimed at children and adolescents with Type 1 diabetes.

Regardless of the roadblocks encountered by Sanofi in its bid to dominate this lucrative market, the company has been insistent in this endeavor -- a determination that’s actually pretty understandable given that the diabetes market covers over 425 million people worldwide.

So far, Sanofi has managed to be one of the leaders in this sector, with insulin injection pen Lantus working as a stable revenue driver for the biopharma for years now.

To offer a clearer perspective on the promising diabetes sector, Lantus raked in $3.95 billion in sales for 2018 alone -- an impressive growth that has been attracting competitors left and right.

In fact, this Sanofi diabetes moneymaker has been experiencing steep competition with sales slipping by over $1.17 billion largely due to the emergence of cheaper and stronger rivals in the market.

Nonetheless, Sanofi wants to maintain its stronghold so new deals are expected to crop up soon in an effort to shore up its declining Lantus revenue. Among the drugs in its portfolio, Toujeo has actually been doing quite well, raking in $930 million in sales in 2018. While this doesn’t really cover the $1.17 billion slip from Lantus sales over the same period, the figure is close enough to bring hope to investors and keep competitors at bay.

Sanofi’s strongest competitor, particularly in the diabetes market, is Novo Nordisk (NVO). The latter’s diabetes drug Tresiba has actually accounted for 84.2% of its overall sales.

While this is definitely daunting for Sanofi, the sales performance of Tresiba can also highlight a key differentiator between the two. That is, Sanofi offers a more diversified portfolio especially in terms of revenue sources. Meanwhile, Novo Nordisk is focused on the diabetes market alone.

Although both Toujeo and Lantus have been remarkable in sales thus far, Sanofi has a number of other top-performing drugs in its portfolio. After all, Sanofi isn’t just about diabetes treatments.

In terms of growth, eczema treatment Dupixent has shown a remarkable 142% jump in sales over the past year. Its revenues rose to $628 million for the third quarter in 2019. In comparison, the overall sales for Sanofi’s diabetes treatments declined by 18% since the third quarter of 2018.

While it’s easy to get distracted by the allure of the lucrative diabetes market, these treatments actually comprise a small portion of the French biopharma’s drug portfolio.

To date, Sanofi has 85 up-and-coming drugs, with 51 of these already sent to early clinical tests and the remaining 34 either in Phase 3 trials or sent for approvals. To provide a more direct comparison, reports show that only two drugs in the pipeline are aimed towards the diabetes market. The rest of Sanofi’s portfolio has 28 oncology candidates and 18 immuno-inflammation drug prospects.

Overall, Sanofi has a stable, well-rounded portfolio to offer its investors. However, stiff competition can prove to be a huge obstacle especially in the high-growth diabetes space. Its revenue growth in this sector isn’t also as remarkable as its competitors.

This doesn’t take away from Sanofi’s other products though. What it means is that it would be a better call to buy Sanofi stock once prices fall at a cheaper valuation.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

December 23, 2019

Fiat Lux

SPECIAL END-OF-YEAR ISSUE

Featured Trade:

(THANK YOU FROM THE MAD HEDGE FUND TRADER),

(MY LAST RESEARCH PIECE OF THE YEAR)

Mad Hedge Technology Letter

December 23, 2019

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND WALL STREET JOBS)

Automation is taking place at warp speed displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the direct capital of $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. bank jobs getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

Mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificial engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

Front-office staff have already felt the brunt of downsizing with purges carried out in 2018 representing a fifth year of decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 20% and the accumulation of hordes of data will advance the marketing effort into a smart, hybrid cloud-based and hyper-targeted strategy.

Historically, a strong labor market and low unemployment boost wage growth, but national income allocated to workers has dipped from about 63% in 2000 to 56% in 2018.

Causes stem from the deceleration in union membership and outsourcing has snatched away negotiating power amongst workers and the implemented mass automation has poured fat on the fire.

I was recently in Budapest, Hungary on a business trip and on a main thoroughfare, a J.P. Morgan and Blackrock office stood a stone’s throw away from each other employing an army of local English-proficient Hungarians for 30% of the cost of American bankers.

Banks simply possess wider optionality to outsource to an emerging nation or to automate hard-to-fill positions now.

In this race to zero, companies can easily rebuff requests for higher salaries and if they threaten to walk off the job, a robot can just pick up the slack.

Automation is getting that good now!

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies are chomping at the bit and even tech companies like Amazon and Apple have started tinkering with new financial products.

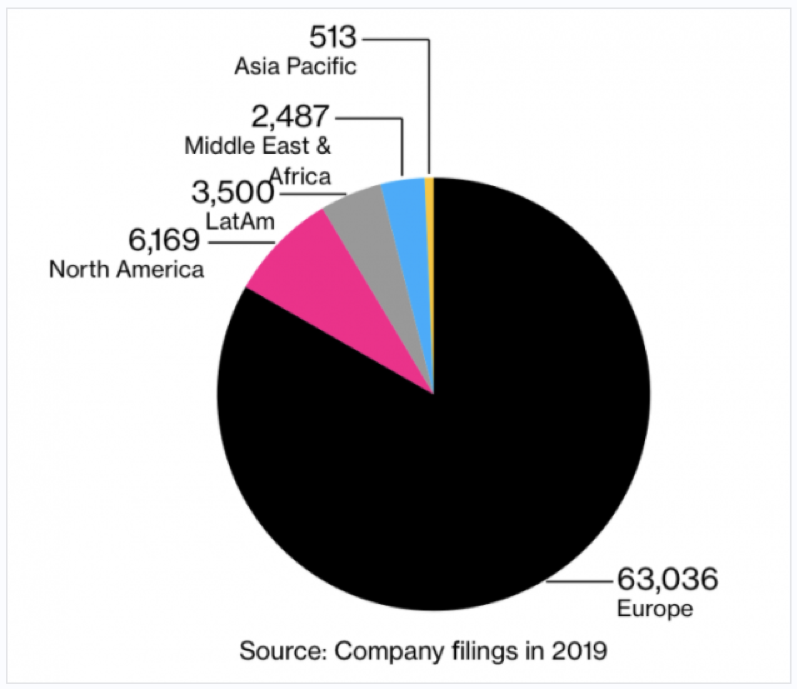

And if you thought this phenomenon was limited to the U.S., think again. Europe is by far the biggest culprit by already laying off 63,036 employees in 2019, more than 10x higher the number of U.S. financial job losses.

In a sign of the times, the European outlook has turned demonstrably negative with Deutsche Bank announcing layoffs of 18,000 employees through 2022 as it scales down its investment banking business.

Germany banks are also passing on the burden of negative interest rates to their clients.

A recent survey by Deutsche Bundesbank shows that 58% of banks are charging all savers negative interest rates while others only target wealthy and corporate clients.

If the U.S. dips into negative rates in the future, expect the same nasty effect on job force cuts that Europe has experienced.

Either way, don’t tell your kid to get into banking because they will most likely be feeding on scraps in the future.

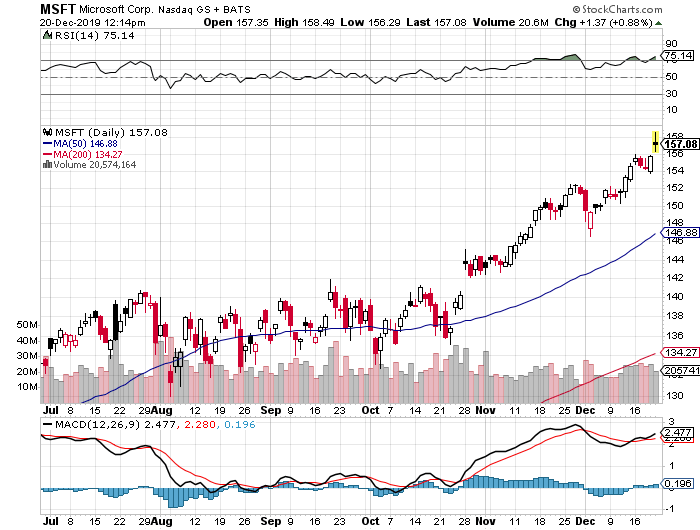

Trade Alert - (MSFT) - EXPIRATION

EXPIRATION of the Microsoft (MSFT) December 2019 $134-$137 in-the-money vertical BULL CALL spread at $3.00

Closing Trade

12-20-2019

expiration date: December 20, 2019

Portfolio weighting: 10%

Number of Contracts = 38 contracts

Provided that (MSFT) does not fall $20.08, or 12.73% by the close today, our position in the Microsoft (MSFT) December 2019 $134-$137 in-the-money vertical BULL CALL spread will expire at its maximum profit at $3.00.

As a result, you have earned $1,520, or 15.38% in 22 trading days. If you bought the shares instead, keep them. They are going much higher.

You don’t get any better quality than Microsoft (MSFT) in the tech world. It is the safest stock in which to invest today. This is a stock that you want to hide behind the radiator and keep forever. It is also one of the great turnaround stories of the decade.

In addition, this particular combination of strikes prices gave you huge support at the 50-day moving average at $140.67. Please note this option spread will be profitable whether the market goes up, sideways, or down small over the next four weeks.

This was a bet that Microsoft shares would NOT fall below $137.00 by the December 20 option expiration date in 22 trading days.

This was also a bet that we are not already in a recession, which I believe is still at least 12 months off.

You don’t need to do anything, as the expiration process is now fully automated. The profit will be deposited into your account and the margin freed up on Monday morning.

Well done, and on to the next trade!

EXPIRATION 38 December 2019 (MSFT) $134 calls at…….……$23.08

EXPIRATION short 38 December 2019 (MSFT) $137 calls at…….$20.08

Net Cost:………………………….…………..…..….….....$3.00

Profit: $3.00 - $2.60 = $0.40

(38 X 100 X $0.40) = $1,520 or 15.38% in 22 trading days.

The optics today look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter, and that is a good thing in 2018.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possible destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business. Microsoft Azure grew 87% YOY last quarter.

To see how to enter this trade in your online platform, please look at the order ticket above, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Spread” by clicking here at

http://www.madhedgefundtrader.com/ltt-vbpds/

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Keep in mind that these are ballpark prices at best. After the alerts go out, prices can be all over the map.

As you are all well aware, I have long been a history buff. I am particularly fond of studying the history of my own avocation, trading, in the hope that the past errors of others will provide insights for the future.

History doesn’t repeat itself, but it certainly rhymes.

So after decades of research on the topic, I thought I would provide you with a list of the eight worst trades in history. Some of these are subjective, some are judgment calls, but all are educational. And I do personally know many of the individuals involved.

Here they are for your edification, in no particular order. You will notice a constantly recurring theme of hubris.

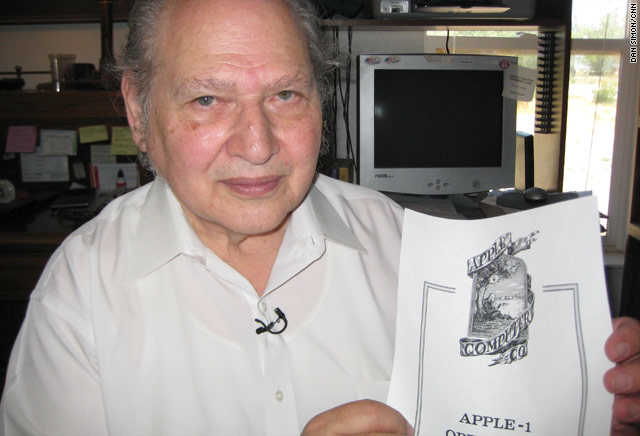

1) Ron Wayne’s sales of 10% of Apple (AAPL) for $800 in 1976

Say you owned 10% of Apple (AAPL) and you sold it for $800 in 1976. What would that stake be worth today? Try $120 billion, making it undoubtedly one of the history's worst trades. That is the harsh reality that Ron Wayne, 78, faces every morning when he wakes up, one of the three original founders of the consumer electronics giant.

Ron first met Steve Jobs when he was a spritely 21-year-old marketing guy at Atari, the inventor of the hugely successful “Pong” video arcade game.

Ron dumped his shares when he became convinced that Steve Jobs’ reckless spending was going to drive the nascent startup into the ground and he wanted to protect his own assets in a future bankruptcy.

Co-founders Jobs and Steve Wozniak each kept their original 45% ownership. Today, Jobs’s widow, Laurene Powel Jobs, has a 0.5% ownership in Apple worth $4 billion, while the value of Woz’s share remains undisclosed.

Today, Ron is living off of a meager monthly Social Security check in remote Pahrump, Nevada, about as far out in the middle of nowhere as you can get, where he can occasionally be seen playing the penny slots.

2) AOL's 2001 Takeover of Time Warner

Seeking to gain dominance in the brave new online world, Gerald Levin pushed old-line cable TV and magazine conglomerate, Time Warner, to pay $164 billion to buy upstart America Online in 2001. AOL CEO, Steve Case, became chairman of the new entity. Blinded by greed, Levin was lured by the prospect of 130 million big spending new customers.

It was not meant to be.

The wheels fell off almost immediately. The promised synergies never materialized. The Dotcom Crash vaporized AOL’s business the second the ink was dry. Then came a big recession and the Second Gulf War. By 2002, the value of the firm’s shares cratered from $226 billion to $20 billion.

The shareholders got wiped out, including “Mouth of the South” Ted Turner. That year, the firm announced a $99 billion loss as the goodwill from the merger was written off, the largest such loss in corporate history. Time Warner finally spun off AOL in 2009, ending the agony.

Steve Case walked away with billions, and is now an active venture capitalist. Gerald Levin left a pauper, and is occasionally seen as a forlorn guest on talk shows. The deal is widely perceived to be the worst corporate merger in history.

Buy High, Sell Low?

3) Bank of America's Purchase of Countrywide Savings in 2008

Bank of America’s CEO Ken Lewis thought he was getting the deal of the century picking up aggressive subprime lender, Countrywide Savings, for a bargain $4.1 billion, a “rare opportunity.” Little did he know he would make it on the worst trades in history list.

Because unfortunately, as a result, Countrywide CEO Angelo Mozilo pocketed several hundred million dollars. Then the financial system collapsed, and suddenly we learned about liar loans, zero money down, and robo-signing of loan documents.

Bank of America’s shares plunged by 95%, wiping out $500 billion in market capitalization. The deal saddled (BAC) with liability for Countrywide’s many sins, ultimately, paying out $40 billion in endless fines and settlements to aggrieved regulators and shareholders.

Ken Lewis was quickly put out to pasture, cashing in on an $83 million golden parachute, and is now working on his golf swing. Mozilo had to pay a number of out-of-court settlements, but was able to retain a substantial fortune, and is still walking around free.

The nicely tanned Mozilo is also working on his golf swing.

4) The 1973 Sale of All Star Wars Licensing and Merchandising Rights by 20th Century Fox for Free

In 1973, my former neighbor George Lucas approached 20th Century Fox Studios with the idea for the blockbuster film, Star Wars. It was going to be his next film after American Graffiti which had been a big hit earlier that year.

While Lucas was set for a large raise for his directing services – from $150,000 for American Graffiti to potentially $500,000 for Star Wars – he had a different twist ending in mind. Instead of asking for the full $500,000 directing fee, he offered a discount: $350,000 off in return for the unlimited rights to merchandising and any sequels.

Fox executives agreed, figuring that the rights were worthless, and fearing that the timing might not be right for a science fiction film. In hindsight, their decision seems ridiculously short-sighted.

Since 1977, the Star Wars franchise has generated about $27 billion in revenue, leaving George Lucas with a net worth of over $3 billion by 2012. In 2012, Disney paid Lucas an additional $4 billion to buy the rights to the franchise.

The initial budget for Star Wars was a pittance at $8 million, a big sum for an unproven film. So, saving $150,000 on production costs was no small matter, and Fox thought it was hedging its bets. They certainly never imagined they were making one of the worst trades in history.

George once told me that he had a problem with depressed actors on the set while filming. Harrison Ford and Carrie Fisher thought the plot was stupid and the costumes silly.

Today, it is George Lucas who is laughing all the way to the bank.

$150,000 for What?

5) Lehman Brothers Entry Into the Bond Derivatives Market in the 2000s

I hated the 2000s because it was clear that men with lesser intelligence were using other people’s money to hyper leverage their own personal net worth. The money wasn’t the point. The quantities of cash involved were so enormous they could never be spent. It was all about winning points in a game with the CEOs of the other big Wall Street institutions.

CEO Richard Fuld could have come out of central casting as a stereotypical bad guy. He even once offered me a job which I wisely turned down. Fuld took his firm’s leverage ratio up to 100 times in an extended reach for obscene profits. This meant that a 1% drop in the underlying securities would entirely wipe out its capital.

That’s exactly what happened, and 10,000 employees lost their jobs, sent packing with their cardboard boxes with no notice. It was a classic case of a company piling on more risk to compensate for the lack of experience and intelligence. This only ends one way.

Morgan Stanley (MS) and Goldman Sachs (GS) drew the line at 40 times leverage and are still around today but just by the skin of their teeth, thanks to the TARP.

Fuld has spent much of the last five years ducking in and out of depositions in protracted litigation. Lehman issued public bonds only months before the final debacle, and how he has stayed out of jail has amazed me. Today he works as an independent consultant. On what I have no idea.

Out of Central Casting

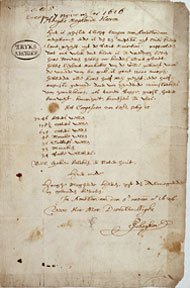

6) The Manhasset Indians' Sale of Manhattan to the Dutch in 1626

Only a single original period document mentions anything about the purchase of Manhattan. This letter states that the island was bought from the Native Americans for 60 Dutch guilders worth of trade goods which would consist of axes, iron kettles, beads, and wool clothing.

No record exists of exactly what the mix was. Native Americans were notoriously shrewd traders and would not have been fooled by worthless trinkets.

The original letter outlining the deal is today kept at a museum in the Netherlands. It was written by a merchant, Pieter Schagen, to the directors of the West India Company (owners of New Netherlands) and is dated 5 November 1626.

He mentions that the settlers “have bought the island of Manhattes from the savages for a value of 60 guilders.” That’s it. It doesn’t say who purchased the island or from whom they purchased it, although it was probably the local Lenape tribe.

Certainly one of the worst trades in history, though historians often point out that North American Indians had a concept of land ownership different from that of the Europeans. They regarded land, like air and water, as something one could use but not own or sell. So, it has been suggested that the Native Americans thought they were sharing, not selling.

It is anyone’s guess what Manhattan is worth today. Just my old two-bedroom 34th-floor apartment at 400 East 56th Street is now worth $2 million. Better think in the trillions.

7) Napoleon's 1803 Sale of the Louisiana Purchase to the United States

Invading Europe is not cheap, as Napoleon found out, and he needed some quick cash to continue his conquests. What could be more convenient than unloading France’s American colonies to the newly founded United States for a tidy $7 million? A British naval blockade had made them all but inaccessible anyway.

What is amazing is that president Thomas Jefferson agreed to the deal without the authority to do so, lacking permission from Congress, and with no money. What lies beyond the Mississippi River then was unknown.

Many Americans hoped for a waterway across the continent while others thought dinosaurs might still roam there. Jefferson just took a flyer on it. It was up to the intrepid explorers, Lewis and Clark, to find out what we bought.

Sound familiar? Without his bold action, the middle 15 states of the country would still be speaking French, smoking Gitanes, and getting paid in Euros.

After Waterloo in 1815, the British tried to reverse the deal and claim the American Midwest for themselves. It took Andrew Jackson’s (see the $20 bill) surprise win at the Battle of New Orleans to solidify the US claim.

The value of the Louisiana Purchase today is incalculable. But half of a country that creates $17 trillion in GDP per year and is still growing would be worth quite a lot.

Great General, Lousy Trader

8) The John Thomas Family Sale of Nantucket Island in 1740

Yes, the investments of my own ancestors are to be included among the worst trades in history. My great X 12 grandfather, a pioneering venture capitalist investor of the day from England, managed to buy the island of Nantucket off the coast of Massachusetts from the Indians for three ax heads and a sheep in the mid-1600s. Barren, windswept, and distant, it was considered worthless.

Two generations later, my great X 10 grandfather decided to cut his risk and sell the land to local residents just ahead of the Revolutionary War. Some 17 of my ancestors fought in that war including the original John Thomas who served on George Washington’s staff at the harsh winter encampment at Valley Forge during 1777-78. Maybe that’s why I have an obsession with not wasting food?

By the early 19th century, a major whaling industry developed on Nantucket fueling the lamps of the world with smoke-free fuel. By then, our family name was “Coffin,” which is still abundantly found on the headstones of the island’s cemeteries.

One Coffin even saw his ship, the Essex, rammed by a whale and sunk in the Pacific in 1821. He was eaten by fellow crewmembers after spending 99 days adrift in an open lifeboat. Maybe that’s why I have an obsession with not wasting food?

In the 1840s, a young itinerant writer named Herman Melville visited Nantucket and heard the Essex story. He turned it into a massive novel about a mysterious rogue white whale, Moby Dick, which has been torturing English literature students ever since. Our family name, Coffin, is mentioned seven times in the book.

Nantucket is probably worth many tens of billions of dollars today as a playground for the rich and famous. Just a decent beachfront cottage there rents for $50,000 a week in the summer.

The 2015 Ron Howard film, The Heart of the Sea, is breathtaking. Just be happy you never worked on a 19th-century sailing ship.

Yes, it’s all true and documented.

Hi Grandpa!

Not a day goes by when someone doesn’t ask me about what to do about trading Apple (AAPL).

After all, it is the world largest publicly-traded company at a $1.2 trillion market capitalization. It is the planet’s most widely owned stock. Almost everyone uses their products in some form or another. It buys back more of its own stock than any other company on the planet. Oh yes, it is also one of Warren Buffet’s favorite picks.

So, the widespread adulation is totally understandable.

Apple is a company with which I have a very long relationship. During the early 1980s, I was ordered by Morgan Stanley to take Steve Jobs around to the big New York Institutional Investors to pitch a secondary share offering for the sole reason that I was one of three people who worked for the firm who was then from California.

They thought one West Coast hippy would easily get along with another. Boy, were they wrong, me in my three-piece navy blue pinstripe suit and Steve in his work Levi’s. It was the worst day of my life. Steve was not a guy who palled around with anyone. He especially hated investment bankers.

I got into Apple with my personal account when the company only had four weeks of cash flow remaining and was on the verge of bankruptcy. I got in at $7 which, on a split-adjusted basis today, is 50 cents. I still have them. In fact, my cost basis in Apple is less than the 77-cent quarterly dividend now.

Today, some 200 Apple employees subscribe to the Diary of a Mad Hedge Fund Trader looking to diversify their substantial holdings. Many own Apple stock with an adjusted cost basis of under $5. Suffice it to say, they all drive really nice Priuses.

So I get a lot of information about the firm far above and beyond the normal effluent of the media and stock analysts. That’s why Apple has become a favorite target of my Trade Alerts over the years.

And here is the great irony: Nobody would touch the stock with a ten-foot pole at the end of 2018. Since then, Apple has rallied 71%, creating more market cap in a year than any company in history.

Here’s why. Apple was all about the iPhone which then accounted for 75% of its total earnings. The TV, the watch, the car, the iPod, the iMac, and Apple Pay were all a waste of time and consumed far more coverage than they are collectively worth.

The good news is that iPhone sales are subject to a fairly predictable cycle. Apple launches a major new iPhone every other fall. The share price peaks shortly after that. The odd years see minor upgrades, not generational changes.

Just like you see a big pullback in the tide before a tsunami hits, iPhone sales are flattening out between major upgrades. This is because consumers start delaying purchases in expectation of the introduction of the new iPhones 7 more power, gadgets, and gizmos.

So during those in-between years, the stock performance was disappointing. 2018 certainly followed this script with Apple down a horrific 30.13% at the lows. Maybe it’s a coincidence, but the previous generation in Apple shares in 2015 brought a decline of, you guessed it, exactly 29.33%.

The coming quarter could bring quite the opposite.

After March, things will start to get interesting, especially post the Q1 earnings report in April. That’s when investors will start to discount the rollout of the new 5G iPhone seven months later. Everyone and their brother is waiting for 5G to purchase their next iPhone, unless it gets lost or stolen first.

The last time this happened, in 2018, Apple stock rocketed by $86, or 55.33%. This time, I expect a minimum rally to $400 high, or much higher. After all, I am such a conservative guy with my predictions (Dow 120,000 by 2030?).

Even at that price, it will still be one of the cheaper stocks in the market on a valuation basis which currently trades at a 20X earnings multiple. This is up from a subterranean multiple of 14X a year ago. The value players will have no choice to join in, if they’re not already there.

But Apple is a much bigger company this time around, and well-established cycles tend to bring in diminishing returns. It’s like watching the declining peaks of a bouncing rubber ball.

This is not your father’s Apple anymore. Services like iTunes and the new Apple+ streaming service are accounting for an even larger share of the company’s profits. And guess what? Services companies command much higher multiples than boring old hardware ones. It’s the old questions of linear versus exponential growth.

A China trade deal will bring a new spring to Apple’s step, where sales have recently been in free fall. Their new membership lease program promises to deliver a faster upgrade cycle that will allow higher premium prices for their products. That will bring larger profits.

It all adds up to keeping Apple as a core to any long term portfolio.

Just thought you’d like to know.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more