Having trouble raising capital for your new hedge fund?

Just list Warren Buffet as your “Honorary Chairman.”

That’s what California prison guard Ottoniel Medrano did. To help his marketing efforts, he also claimed that he had $4.8 billion in assets under management as well as massive real estate holdings somewhere in Asia.

Medrano’s International Realty Holdings managed to raise $700,000 from individuals with this scam which he promptly shipped to offshore bank accounts before the Feds shut him down.

When you think you’ve heard everything, something like this pops up. Unbelievable.

You would think that people have heard of “due diligence” by now.

People with famous financial names like Morgan, Rockefeller, Rothschild, Getty, and DuPont often find out they are endorsing things they have never heard of to help someone’s fundraising effort.

I once heard of a guy who got a license plate of GETTY 1 just so he could get free valet parking at restaurants.

More recently, president Donald Trump has faced the same problem.

More than 200 companies in China are marketing products under his name without his permission.

After years of languishing in the courts, one judge finally ruled in his favor, the day after the new president affirmed the long-standing ‘One China Policy.”

Who said being Commander in Chief didn’t have its benefits?

It all brings back unpleasant memories of the Bernie Madoff scandal.

By the way, Bernie has only 123 years left on his sentence. By then he will be 201 years old.

Who knows? Maybe on that low-fat, low-carb prison diet, he’ll make it. He has a better health plan than I do.

I’m only on Medicare.

Want to Invest in My Fund?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/Bernie-Madoff.jpg282354Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2019-04-04 01:06:502019-04-04 01:17:14Scam of the Month Club

You cannot accuse Autodesk (ADSK) of ignoring the prodigious migration to digital and full-blown automation.

The company gives credence to the tech theory of taking a pretty darn good software product, repackage it as a subscription, then watch revenues and marginal profitability go through the roof.

Autodesk is one of the original pioneers of AutoCAD, a commercial computer-aided design (CAD) and drafting software application.

Before AutoCAD was introduced, most commercial CAD programs ran on mainframe computers or minicomputers, with each CAD operator working at separate graphics terminal.

Autodesk’s AutoCAD and Revit software are mainly applied by architects, engineers, and structural designers to design, draft, and model buildings.

Being one of the flagbearers of the industry has its perks with Autodesk’s AutoCAD software being involved in world-renowned projects from the One World Trade Center to Tesla electric cars.

Once I roll through their 2018 achievements, it will be impossible not to define this company as part of the cloud aristocracy.

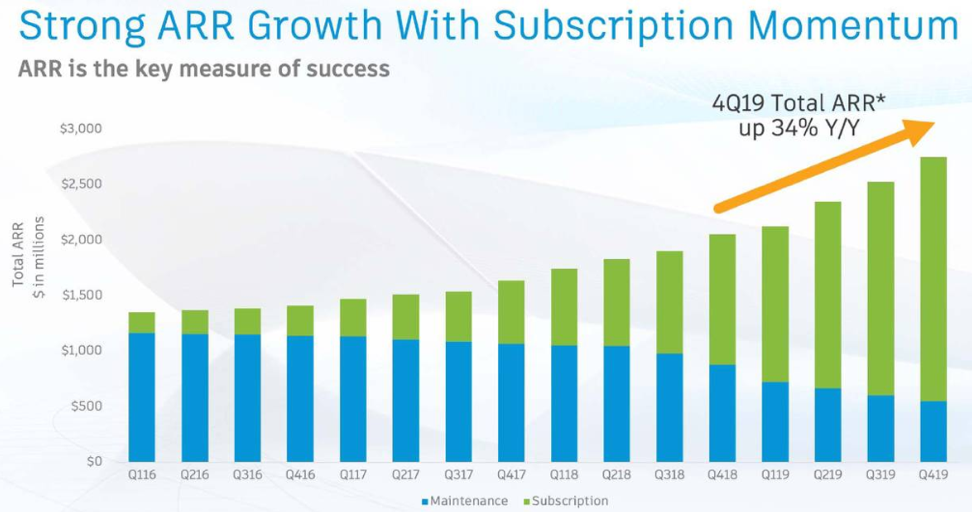

Scrolling through the numbers, my eyeballs pinpoint at the all-important Annual Recurring Revenue (ARR) as the starting point for clues to its success.

(ARR) is a crucial metric used by software-as-a-subscription (SaaS) businesses who define the contract length and the (ARR)’s specific dollar value contracted in return for proprietary software.

You’d be chuffed to bits to discover that Autodesk’s (ARR) delivers 95% of total annual revenue which amounted to almost $2.6 billion in fiscal 2018, a record for this company headquartered in San Rafael, California.

On an annualized basis, (ARR) growth amounted to 34% and billings cruised past the $1 billion mark for the first time last quarter.

Autodesk would be lying if they said subscriber growth isn’t the lynchpin to growing revenue, it certainly is, and they are doing their best to take advantage of this opportunity.

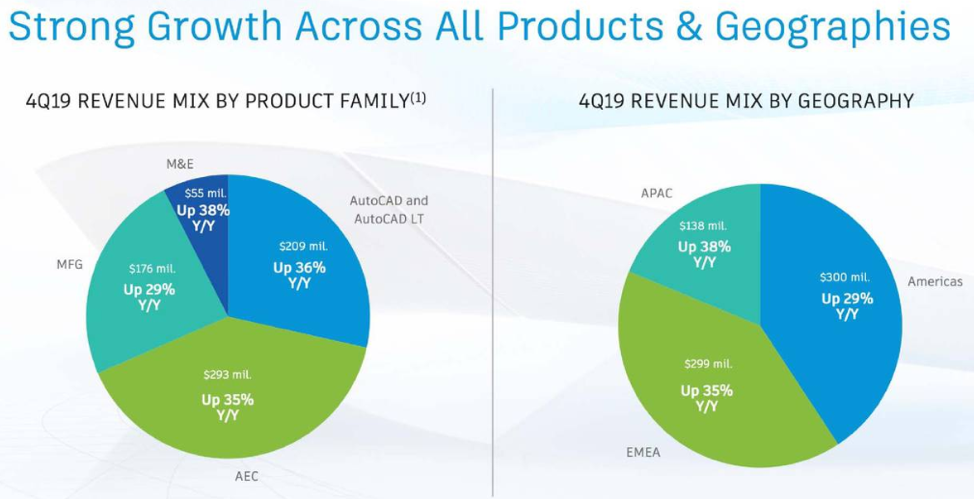

When talking about the strengths, we must look at Autodesk’s AutoCAD software which featured among the top 10 fastest growing skills in technology job searches.

According to Upwork’s latest quarterly index, Revit expertise is highlighted among the top 15 hardest skills for freelancers in the U.S. job market.

Building information modeling (BIM) is a process involving the generation, production, and management of digital representations of physical and functional characteristics of places.

Clayco, an ambitious construction design firm based in Chicago, has been an Autodesk customer for years.

They use BIM 360, Assemble, PlanGrid and Building connective as they are single-mindedly focused on fully embracing the digitization of construction.

BIM adoption remains one of the underlying reasons of investments in the infrastructure space.

An industry-wide cry for adopting BIM drove another seven figured enterprise agreement with a large European infrastructure provider last quarter.

Autodesk doubled the contract with the customer as the company hopes the adoption of BIM for building and managing will enhance the quality of infrastructure projects.

Autodesk’s unique portfolio design tools are allowing them to expand from products like AutoCAD and Inventor into Revit the world’s leading BIM design tool.

On the manufacturing side, generative design and investments in Fusion continue to attract global manufacturing leaders to collaborate with Autodesk.

A vivid example is the cloud agreement signed with Korean automobile maker Hyundai Motor Group who plan to leverage Autodesk’s software to generate innovative car designs.

Taking a microscope to the financials, the average revenue per user (ARPS) increased 17% because of the 13% boost in the number of subscriptions.

The subscription plan subs grew by 291,000 organically.

Continued adoption of BIM 360 solutions gave a 51,000 boost to cloud subs.

Autodesk is finishing up migrating the maintenance customers to subscription packages.

In Q4, 110,000 customers moved from maintenance to product subscriptions, meaning Autodesk has switched over nearly 800,000 maintenance customers to subscriptions since the inception of the program.

The maintenance plan was abandoned in the fall of 2016 as a way of driving revenue momentum. Before, Autodesk offered software upgrades and the latest product releases for free.

Dramatically shifting to a subscription model has laid the pathway to monetize their software through a monthly recurring payment system.

The company also offers a discounted three-year subscription that 3rd parties can lock in if they are serious about a long-term relationship with Autodesk.

At the end of this month, Autodesk plans to increase the cost of certain subscription plans by between 2.5% and 10% allowing the company to deliver more value to the engineers that religiously rely on Autodesk.

Even though maintenance plan packages are slowly winding down, after this small group’s special discount expires, they will be recommended to join the new subscription program.

As it stands, less than 20% of revenues is generated from the maintenance agreements as the subscription revenue model has furthered Autodesk’s financial interests, effectively executing Autodesk’s growth strategy.

The shift to a cloud-based subscription setup is one of the crucial ways Autodesk has maximized free cash flow and has been a massive catalyst of a profitability surge.

The company is smack in the middle of growth sweet spot benefitting the top line and combined with gross margin expansion, I trust Autodesk shares to be an outsized winner of the cloud aristocracy.

Buy Autodesk on the dip.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/autodesk-products.png499974Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-04 01:06:132019-04-03 16:31:10A Legacy Tech Company You Have to Buy

"Markets will over value what you can quantify," said Ann Lamont at Oak Investment Partners, referring to the extreme high prices for public companies versus the discount valuations of private ones.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2019-04-04 01:05:362019-04-03 16:43:14Quote of the Day - April 4, 2019

The Five Most Important Things That Happened Today

(and what to do about them)

1) See You at the Skybridge SALT Conference in Las Vegas, May 7-10, the Woodstock of alternative asset investors. Learn what the hedge funds are planning next, and it’s a blast. Meet former UN Ambassador Nikki Haley, AOL Founder Steve Case, Carlyle Group co-founder David Rubenstein, and hyper entrepreneur Mark Cuban. Click here.

2) Oil Prices are Going Ballistic, up four days in a row, topping $62 a barrel. OPEC has developed a new short squeeze. It’s going to be hitting the local pump soon, just as the peak driving season is approaching. Click here.

3) US Auto Sales Were Terrible in Q1, the worst quarter in a decade. General Motors (GM) suffered a 7% decline with Silverado pickups off 16% and Suburban SUVs plunging 25%. Is this a prelude to the Q1 GDP number? Risk is rising. Click here.

4) Trump Called Fed Governor on the March Stock Dip. Is this micromanaging, or what? Talk about a free put on the market. Risk on! Click here.

5) Semiconductor Index Hits New All-Time High. Advanced Micro Devices (AMD), a Mad Hedge favorite, soars 9%. It’s the future, so why not? Buy dips. Click here.

Published today in the Mad HedgeGlobal Trading Dispatch and Mad Hedge Technology Letter:

(WHO WILL BE THE NEXT FANG?)

(FB), (AMZN), (NFLX), (GOOGL), (AAPL),

(BABA), (TSLA), (WMT), (MSFT),

(IBM), (VZ), (T), (CMCSA), (TWX),

(YOUTUBE’S BIG MOVE INTO INDIA)

(GOOGL), (NFLX), (AMZN)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 15:17:302019-04-03 15:17:47Mad Hedge Hot Tips for April 3, 2019

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 15:02:062019-04-03 15:02:06April 3, 2019 - MDT Alert (FB)

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 10:18:032019-04-03 10:33:23Trade Alert - (TSLA) April 3, 2019 - SELL-STOP LOSS

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 08:49:132019-04-03 08:49:13April 3, 2019 - MDT Pro Tips A.M.

YouTube has to be the online streaming asset of the year even relegating Netflix (NFLX) to the minor leagues – I’ll tell you why.

India is the new China.

Netflix’s growth strategy is intertwined with India and the management has been extraordinarily vocal about their interests there.

The Indian online streaming renaissance isn’t just fueling Netflix’s rise. In fact, YouTube and its free platform are performing miracles along the Ganges River.

How big is YouTube in India?

YouTube already has 245 million monthly active users in India penetrating 85% of the country’s internet population making India one of its best-performing markets.

The company says more than 60% of its streaming hours in India come from outside the six metros, meaning YouTube has captured the hearts and minds of the rural population who cannot afford to pay for online content.

KPMG forecasts India’s online streaming audience to surpass 550 million by 2023 and YouTube will capture 70% of the 550 million audience.

How did YouTube manage to do this?

First, the content is free with ads allowing rural Indians to join in.

Second, local Indians became hooked on Alphabet’s YouTube with Alphabet (GOOGL) taking an already brilliant platform and supercharged it by tailoring it to popular local influencers that are joining in droves inciting a massive network effect.

Effectively, YouTube attracted these influencers with eye-popping audiences to create organic and original content without the $8 billion Netflix planned content budget in 2019.

YouTube was able to do this by borrowing the Instagram format but transferring it to a more effective video platform model.

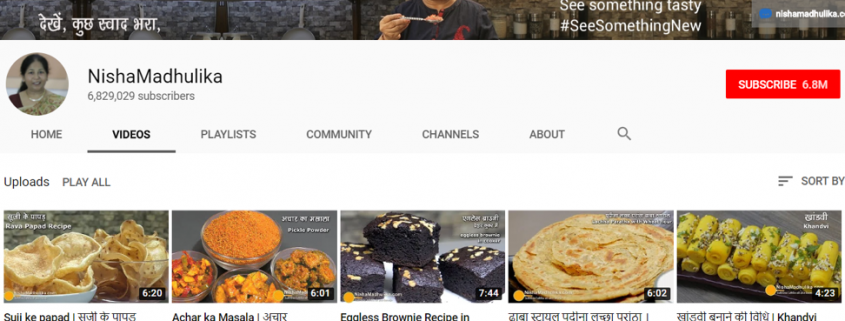

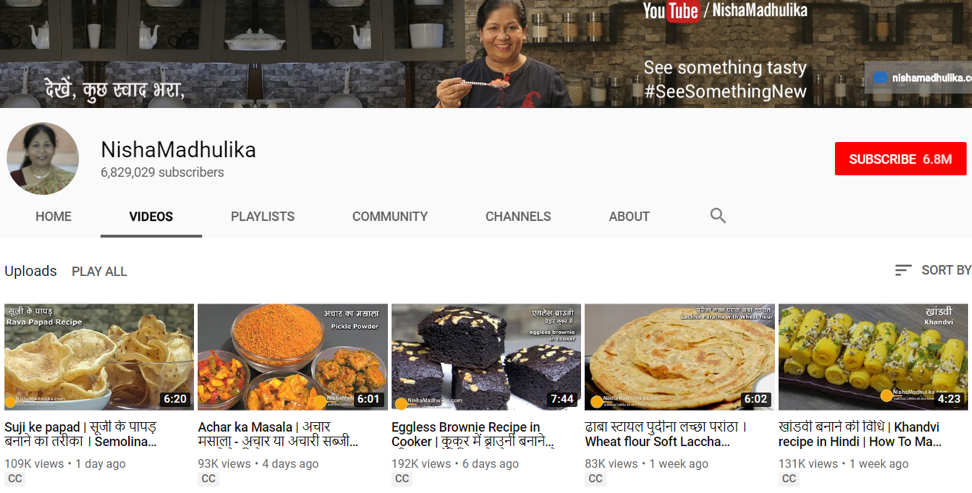

Take for instance Nisha Madhulika whose channel has blossomed into one of the most popular Hindi language-based online cooking channels on the internet.

Her channel has over 6.8 subscribers, yet, accumulating subscribers is one thing, and making money is another.

Past videos that were posted around 2-3 weeks ago have views between 200,000 to 400,000.

These influencers build up revenue by displaying 3rd party ads generated by Alphabet.

A general rule of thumb is that for every 1 million view, ad revenue collected is around $2,000.

Therefore, Nisha and fellow YouTubers with massive audiences are incentivized to pump out high-quality content in high volume.

Scrolling through her numbers, Nisha appears to average around $700 of revenue per video.

She sprinkles in the occasional viral video that garners 1.5 million views which would earn her a tidy $3,000 for a single video.

Not bad and that is before any of the possible marketing opportunities are quantified.

As long as she focuses on the quality of the videos, she can consistently earn $700 per video, then she can do more by partnering with affiliates to sell 3rd party products and receive a commission that is trackable through the links she leaves at the bottom of her videos.

Nisha’s video business works like this, her channel entails producing 3-5 short videos per week producing around 9-11 million views per month adding up to between $18,000-$22,000 in revenue per month.

Remember that while she is accumulating views for newly posted videos, there are still viewers rummaging through her older content demonstrating the beauty of the network effect.

Older videos in Nisha’s case usually add an extra $3,000-$5,000 per month to the bottom line in pure profit.

Many influencers curate, edit, design, and film the content themselves, or subcontract these jobs for a cheap fee.

An influencer could run their YouTube channel for less than $100 per month minus the fees for the equipment.

YouTube has created a powerful platform for content creators to monetize their original content and give them incentives to stick around and build a business.

Netflix has more of a mercenary model where they contract highly paid actors to contribute a finite amount of content for a fee.

YouTube’s model penetrates to the heart of the average person with regular people instead of propping up overpaid Hollywood actors like Netflix.

In many cases, YouTube’s influencers offer live, raw, and personal access, and the data suggests that live, unscripted content are one of the most monetizable types of content on the market due to its original nature and unpredictability.

That is why live sports like the NFL and NBA are easy to sell, monetize, and in great demand.

I do believe that Netflix has a great product but overpaying for Hollywood’s best talent is not sustainable because the cost-benefit ratio isn’t worth it, which is why Netflix is raising customer prices to monetize the quality of streaming content better.

With other big tech players coming into the market, it will push up the costs for Hollywood talent putting more short-term pressure on their financial model.

Even if Netflix does get the right actors to provide content, they do have their fair share of bad movies.

YouTube’s performance in India will be hard to compete with, even harder when they avoid expensive mistakes, a bad video is simply glossed over and ignored.

Netflix is in the midst of testing a mobile-only Indian subscription package for around $3.64 per month, or 250 Indian rupees, to respond to YouTube’s godlike presence there.

Remember that most rural Indians do not have access to hardware such as computers, laptops, or tablets, and run their lives with cheap Chinese smartphones from Oppo and Vivo.

If you thought $3.64 was a cheap streaming package, then Amazon (AMZN) takes it one step further by offering Amazon prime video for $1.88 per month or 129 Indian rupees.

I like Netflix’s product and the narrative is still intact, but I adore and love YouTube’s transformation that has caught many of us by surprise.

This massive shift wouldn’t be possible without Google’s army of best of breed ad tech.

Even more poignant, YouTube takes direct to consumers to a rawer entry point enhancing the special experience.

The problem with Hollywood talent is that reformulating them onto Netflix’s platform brings them closer to the audience to a certain degree, but not like Nisha’s cooking channel where she can speak directly to the viewer and even interact with her audience in the comment section.

YouTube has mastered this relationship between content creator and audience, and no matter how many times I watch Will Smith’s Bright, I can’t expect him to reply to my comments.

Well, there’s not even a comment section on Netflix’s platform.

In short, Netflix’s Indian strategy is incomplete and I predict that YouTube will extend its lead there because the scalability is well-suited for the Indian rural audience who have little or no discretionary income.

The freemium model wins out again.

Affixing a Netflix grade streaming asset to Alphabet’s booming digital ad business is a match made in heaven.

Buy Alphabet on the dip – YouTube’s outperformance in 2019 will surpass expectations and carry Alphabet shares to new all-time highs this calendar year.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/youtube.png493972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 08:06:492019-04-03 08:21:24YouTube’s Big Move Into India

“Artificial intelligence is the future, not only for Russia but for all humankind. Whoever becomes the leader in this sphere will become the ruler of the world.” – Said President of Russia Vladimir Putin

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/putin.png379237Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 08:05:042019-04-03 08:20:51April 3, 2019 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.