Mad Hedge Technology Letter

April 8, 2020

Fiat Lux

Featured Trade:

(AVOID YELP ON PAIN OF DEATH)

(YELP), (GRUB)

Mad Hedge Technology Letter

April 8, 2020

Fiat Lux

Featured Trade:

(AVOID YELP ON PAIN OF DEATH)

(YELP), (GRUB)

Tech investors should be migrating towards stocks that have high visibility of an earnings turnaround once a health solution is discovered for the current health scare. One that definitely does not fit the bill is Yelp (YELP) who has experienced negative earnings growth for the past three years.

What’s the deal with Yelp?

The company recently withdrew its first quarter and 2020 financial guidance because the coronavirus has destroyed large parts of its business probably to never return.

If you didn’t know, Yelp provides information through online communities on restaurants, shopping, nightlife, financial, health, and other services, so it’s easy to do the calculus as to why lockdowns and restrictions on public life are affecting these revenue streams.

A recent survey reported a higher average likelihood of households missing a debt payment over the next three months, meaning the consumer is in dire straits unless there is a swift 180 in circumstances.

In the longer-term, the New York Fed affirms a “persistent deterioration” in consumers’ expectations to access credit throughout the rest of 2020.

The New York Fed said the sharp decline in consumer expectations cuts across all age, education, and income groups.

Less money for consumer spending means less consumer demand on Yelp translating into lower ad revenue – it’s that simple.

On a conference call on February 13, Yelp mentioned that it expects 2020 revenues to grow between 10% and 12% year over year and adjusted EBITDA by 1 to 2 percentage points. It had also expected margins to expand again in 2020.

What a difference 4 weeks makes!

Now almost every company is in survival mode and Yelp is the weakest link.

Consumer interest in restaurants and nightlife has taken a nosedive in the new coronavirus economy.

Yelp data shows that consumer interest had declined 54% for restaurants and 69% for nightlife venues.

Cafes, French restaurants, and wineries decreased their share of daily consumer actions (down 66%, 47% and 44%, respectively) week over week.

In contrast, the weekly growth numbers favor just a select few - grocery stores interest is up 102%, fruit and vegetable shops are up 102%, fast-food joints are up 64%, and pizzerias round out the bunch up 44%.

Some hard-hit companies come in the form of bowling, yoga and martial arts services which tend to involve groups of people, declined by a respective 43%, 38%, and 33%, and these are all companies that would be spending ad money.

Even worse news on the financial side - mom and pop stores have a short leash with median cash buffer for a small business at just 27 days.

As you would assume, searches on home fitness equipment surged 344%, and interest in parks rose 53%.

Interest was also up 360% for buying guns and 166% up for buying water - breweries were down 61%.

Lawmakers and states, including New York, New Jersey, California, and Pennsylvania, have ordered a temporary closure of restaurants and bars and I can safely say that consumers probably won’t return the next day to barge down the entrance door.

The last earnings report wasn’t all that hot for Yelp who missed on revenue while spending 10% more on advertising to get to that miss.

Earnings per share also missed estimates by sliding 35% year over year validating my thesis that this is a sinking ship headed towards an iceberg.

These propped up numbers were before the coronavirus hit the company and the business model is poorly prepared for this type of phenomenon and the lasting effects.

I expect a material decrease in the growth of the number of paying advertising locations and lower advertising budgets from multi-location customers.

Paying advertising locations should drop by half just this quarter.

Materially lower traffic dropping over 50% is a trend that will perpetuate and even if there is a dead cat bounce because shares are so beaten down, this is an unequivocal “sell on the rally” type of stock.

“Culture eats strategy for breakfast.” – Said Microsoft CEO Satya Nadella

Global Market Comments

April 8, 2020

Fiat Lux

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (GOLD), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

SPECIAL GOLD ISSUE

I have been bullish on gold (GLD) for the last three years and the payoff is finally here (click here).

How high could it really go?

The recent massive stimulus measures to fight the Coronavirus-induced depression is certainly bringing forward the rebirth of inflation. The Fed has just increased all of the $17 trillion quantitative easing created globally over the past decade by a staggering 50% in weeks!

This is hugely gold-friendly.

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now, we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it peaked in the summer of 2011, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant (click here).

The biggest buyers of gold in the world, Indian investors, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

You could also blame the China slowdown for the declining interest in the yellow metal, which is now in its sixth year of falling economic growth.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,300 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those giant six-foot high tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD) didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate as older mines carry costs that go all the way down to $600 an ounce.

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

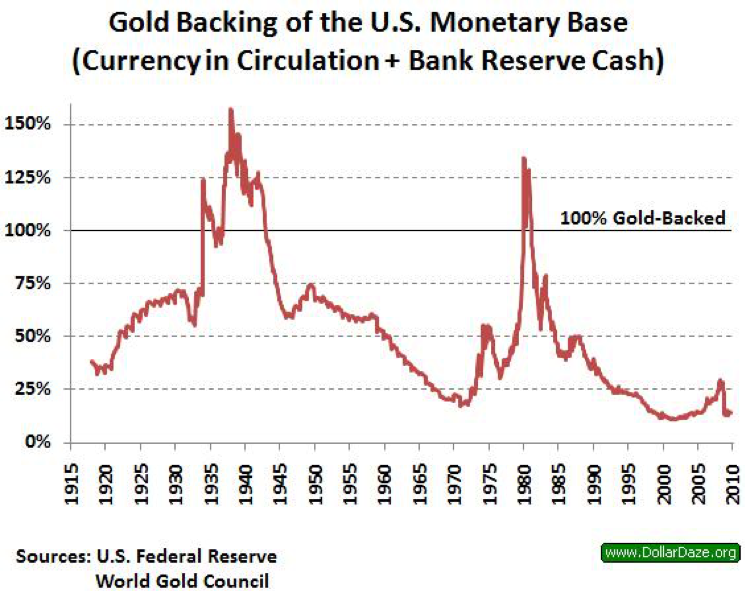

So, when the chart below popped up in my in-box showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce when the money supply was collapsing during the Great Depression and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten you interested yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980, to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and healthcare, but nowhere else. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid 2020s when shocking wage hikes spread elsewhere.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients other risk assets, good for you.

You’re finally learning!

Mad Hedge Biotech & Healthcare Letter

April 7, 2020

Fiat Lux

Featured Trade:

(AMGEN THROWS ITS HAT IN THE RING WITH COVID-19)

(AMGN), (ADPT)

Another biotech heavyweight, Amgen, has entered the race to find a cure for the deadly coronavirus disease (COVID-19).

Amgen (AMGN) has decided to collaborate with Adaptive Biotechnologies (ADPT) in order to develop a treatment targeting COVID-19. Specifically, the joint effort will rely heavily on Amgen’s immunology expertise combined with Adaptive’s innovative platform used to identify virus-neutralizing antibodies.

The trials will focus on studying the antibodies of individuals who successfully recovered from COVID-19.

Similar to how Biogen (BIIB) and Vir Biotechnology (VIR) handled their collaboration, Amgen and Adaptive also opted to take the plunge even before finalizing all the details of the deal.

Although the urgency of the pandemic is definitely one of the reasons both companies agreed to this setup, another reason could be their history of working together.

Amgen and Adaptive first started collaborating in 2017 when the two companies developed a test for acute lymphoblastic leukemia patients.

In 2019, they expanded their partnership with Amgen utilizing Adaptive’s next-generation sequencing assays for all the blood cancer drugs and even pipeline candidates.

Prior to its partnership with Amgen, Seattle-based Adaptive has been blazing a path in the biotech world. Its biggest claim to fame is its ability to sequence the human immune system.

This is far more challenging than human genome mapping, which only involves 30,000 genes. To sequence the immune system, you would need to look at 100 million genes.

As if that wasn’t challenging enough, Adaptive has also ventured on mapping over 30 billion immune receptors, even owning the data rights to 20 billion of those.

Sensing the potential and the demand from this genetic sequencing system, Microsoft (MSFT) actually offered a collaboration agreement with Adaptive in 2017.

This partnership resulted in a system that can create a universal blood test, which helps doctors read and analyze a patient’s immune system. They will then be able to determine what diseases a person’s body is fighting.

For instance, the body of a cancer patient knows of the threat so its immune system starts fighting the cancer cells. However, this is not immediately known to the doctors, especially without the usual symptoms.

With Adaptive’s system though, the doctors will be able to hack into the immune system of the patient and discover what the body is reacting to. This will allow the doctors to diagnose any disease as early as possible regardless of the appearance of symptoms.

Armed with the information from Adaptive’s test, the doctors will be able to prescribe the right treatments and drugs to boost the patient’s immune system and eventually cure the disease.

Needless to say, Adaptive’s innovative technology would be particularly useful in the fight against COVID-19.

Meanwhile, Amgen seems to be sailing through the economic crisis smoothly.

In fact, this giant biotech even recorded a 1.5% gain in March despite the historic beating suffered by the broader market.

To put things in perspective, the S&P 500, the Dow Jones Industrial Average, and the NASDAQ Composite Index all lost over 10% of their value last month.

In comparison, Amgen was one of the handful of blue-chip stocks to wrap up March on a positive note.

Several factors contributed to Amgen’s resilience amid the pandemic and economic crisis.

One is the company’s newer drugs in the market such as cholesterol treatment Repatha and postmenopausal drug Prolia. Both recorded a double-digit increase in sales for the first quarter of 2020.

Amgen is also banking on the expansion of its blockbuster psoriasis treatment Otezla, which represents a profitable growth space for the company. The worldwide psoriasis market is projected to reach roughly $46.6 billion by 2022.

Apart from these, Amgen has approximately 40 drugs queued in its pipeline with half already in their Phase 3 trials. Obviously, that’s promising news, especially for long-term investors.

The company has been quite optimistic about its performance this year, estimating a minimum 6.8% increase in annual revenue to fall somewhere between $25 billion and $25.6 billion.

Finally, Amgen has been steadily increasing its dividend every year. Just last year, the company paid a yearly dividend worth $5.80 for each share, showing a 10% jump from 2018.

So far, Amgen has proven itself as one of the stocks immune to the COVID-19 threats and even the widely feared economic crisis.

Since the pandemic isn’t anticipated to peter out in the next months, investors will definitely be on the lookout for high-quality businesses capable of paying solid dividends and can still earn despite the ongoing crisis. Amgen manages to tick off both of these crucial boxes.

![]()

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more