When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-17 11:31:452020-06-17 11:31:45Trade Alert - (SPY) June 17, 2020 - BUY

I am going to revisit a call I made last October 2019 on a tech stock that has outperformed mightily this year, and for good reasons.

There isn’t a tech stock more relevant today than Veeva Systems (VEEVA) because of the wave of health spending transcending the world.

Find me a country that is spending less on healthcare today!

I recommended this stock last October and the shares keep climbing over itself to reach all-time highs over and over again.

The one-sentence answer to why buy this stock is that Veeva’s latest earnings showed quarterly total revenue growing 37.7% year-over-year and EPS surging 32% year-over-year.

If I stopped here, that would most likely be enough to convince readers about this spectacular company.

Read on to understand more about this health cloud upstart positioned at the intersection of healthcare and cloud technology.

Veeva provides cloud-based CRM, data storage, and analytics services for life science and pharmaceutical companies.

It was co-founded by the former senior VP of technology at Salesforce, and its services are seamlessly integrated into Salesforce's platforms.

Veeva's tools help companies keep track of customer relationships, clinical trials, government regulations, prescribing habits, and other data in real-time.

I guess you could call it the Salesforce of cloud healthcare.

It enjoys a first-mover's advantage in the space and services an all-star lineup of top pharmaceutical companies like GSK and Novartis.

The first-mover advantage is critical because Microsoft announced a copycat version of Veeva’s services just a month ago.

To read about Microsoft heading into the health cloud business, click here.

Demand for Veeva's services has surged over the past few years, thanks to vicious competition between drugmakers and the need for real-time data.

The health crisis will also generate tailwinds for Veeva as leading drugmakers scramble to develop treatments and vaccines.

The company hasn’t been quiet, rolling out new products this year.

In May 2020, the company announced MyVeeva for clinical trials.

It is software built to enable clinical research sites to interact remotely with their patients easing the burden on in-clinic visits.

In March 2020, the company commercially launched Veeva Data Cloud, a robust technology platform constructed for the development and delivery of large-scale patient data and analytics.

The coronavirus is the catalyst that is forcing our healthcare industry to digitize rapidly and modernize.

The data backs up this trend.

The healthcare IT Market is forecasted to be valued at $511.06 Billion by 2027, growing at a CAGR of 13.8%.

Veeva analytics showed us that monthly doctor visits were halved in February compared to April before the widespread lockdown.

Teleconference doctor calls have skyrocketed increasing 30% year-over-year in April, compared with less than 1% in February.

Remote meetings between pharmaceutical companies and doctors increased more than 30 times and email communications doubled from February to April.

Veeva's management wholeheartedly believes it will reach its goal of generating $3 billion in revenue by 2025.

Their goals are impressive with an expectation of year-over-year growth rate of 26% at the midpoint.

Veeva loves to overdeliver, and if one thing is clear from the Q1 scorecard, health cloud computing services are more critical than ever to the life sciences and healthcare industries.

The company also has a pristine balance sheet with $1.38 billion in cash and short-term investments (nearly three years of cash operating expenses at the Q1 run rate) and zero debt.

Moving forward, I firmly believe that Veeva Systems will fetch a growing premium to the overall market.

The stock has zoomed from the March lows of $133 and is now trading at a robust $223 and the path of least resistance is up.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-17 10:02:162020-06-18 00:40:30Why Veeva Has More to Run

“Study hard so that you can master technology, which allows us to master nature.” – Said Argentine Revolutionary Che Guevara

https://www.madhedgefundtrader.com/wp-content/uploads/2020/06/che-guevara.png126103Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-17 10:00:152020-06-17 10:23:49June 17, 2020 - Quote of the Day

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-17 09:24:162020-06-17 09:24:16June 17, 2020 - MDT Pro Tips

Thanks for all your help with my trading. Your service is very effective.

As you know, I went heavily into some LEAPS two days ago including United Airlines, (UAL), Delta Airlines (DAL), Wynn Resorts (WYNN), MGM Resorts International (MGM), and Simon Property Group (SPG) that have returned as much as a 25% ROI over that short period.

I know two days does not prove anything, but it is a great way to begin a trade.

Thanks again,

John

Seattle, WA

Berlin 1968

https://www.madhedgefundtrader.com/wp-content/uploads/2017/07/west-berlin-1968.jpg363348Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-17 09:02:352020-06-17 09:16:57Testimonial

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-16 14:43:132020-06-16 14:43:13Trade Alert - (TLT) June 16, 2020 - BUY

The COVID-19 crisis has yanked the rug from under companies across all industries, and among the businesses that experienced a completely altered landscape these days is the health insurance industry. Imagine a business where sales increase fourfold overnight, but the customers can’t pay.

With the unemployment rate rising to historic levels since the pandemic hit, more people are dropping off commercial coverage rolls. Visits to the doctors and other elective procedures have been postponed indefinitely. Even political talks on healthcare reforms appear to be tabled until 2021.

Overnight, some doctors at country hospitals have seen workloads double and the suicide rate soar, while those in private practice are essentially unemployed.

While healthcare stocks are understandably struggling to survive, there are standouts that managed to take the blow without crumbling to ruins.

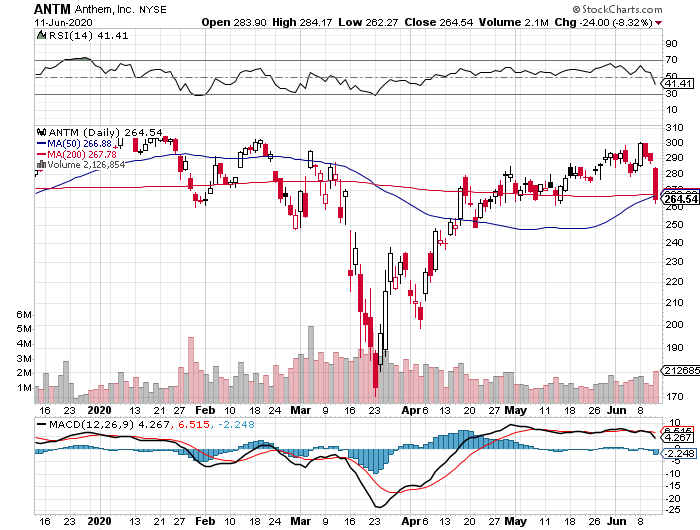

One of them is Anthem (ANTM).

With a market capitalization of $75.78 billion, Anthem is one of the biggest health insurers in the United States today.

Recently, the company wielded its power to offer $2.5 billion worth of premium credits as a form of financial assistance to its members during the pandemic.

This comes in the form of cost-share waivers, extensions for their virtual care coverage, and even assistance for struggling employers to help in maintaining the healthcare of their own employees.

While a lot of companies have been rapidly downgrading 2020 guidance due to the pandemic, Anthem updated its 2020 forecasts to reflect an increase in its adjusted net income from $19.44 per share to an eye-popping $22.30.

This indicates that Anthem has extra bandwidth for growth primarily thanks to its stable revenue stream, increasing membership, and solid earnings.

In its first quarter report for 2020, Anthem’s operating revenues jumped by 20.7% year over year to reach $29.4 billion, with profits from its IngenioRx launch.

As for its net income in the said period, Anthem raked in $1.52 billion or roughly $5.94 per share compared to $5.91 per share in 2019.

Anthem even increased its dividend by 19% in January.

However, it’s Anthem’s cash flow that continues to impress. From 2019 up until the first quarter of this year, Anthem’s cash flow surged by 58% year over year.

One of the main factors that boost the growth of a health insurance company is membership, and Anthem managed to tick off that box as well in the first quarter.

Anthem’s medical enrollment climbed to 42.1 million members, showing off a 3.2% increase year over year. With backing from government business enrollment as well as commercial and specialty businesses, this number is expected to climb higher this year.

Even Anthem’s inorganic growth ventures promise great results, with acquisitions and collaborations continuously boosting the Medicare Advantage growth of the company.

A good example is its acquisition of the Medicaid members in Missouri and Nebraska via WellCare Health at the beginning of 2020. This led to 849,000 lives added to its government business enrollment since 2019.

Meanwhile, its acquisition of AmeriBen added 452,000 members to its commercial and specialty business sector.

Anthem’s takeover of Beacon Health, which is the biggest independent behavioral health firm in the US, serves to further strengthen its position in this sector. This move added roughly 300,000 Medicaid members under Anthem’s coverage.

In terms of adapting to the needs of its members during the pandemic, Anthem is making more aggressive moves to promote its telehealth services.

Although this sector is currently widely associated with Teladoc Health (TDOC), which has a market capitalization of $12.93 billion, the rest of the league is catching up quick.

Since the average cost per telehealth session is roughly $100 less compared to fees paid in visits to the doctor’s office, this is definitely a platform-managed care providers are looking into.

According to Anthem, its telehealth app recorded over 170,000 new downloads since the COVID-19 crisis started.

It also reported a 250% surge in the demand for its virtual care services.

Anthem isn’t the only health insurer joining the telehealth fray. CVS Health (CVS), Humana (HUM), Centene (CNC), and even industry leader UnitedHealth Group (UNH) has been looking into the service.

In this period of uncertainty, choosing a stable company with a robust outlook and sold at a reasonable price is always a wise investment.

With Anthem’s profits projected to grow by roughly 47% over the next years, this company’s future offers security to its investors. Its impressive cash flow also plays a significant role in its higher share valuation.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-06-16 10:00:522020-06-17 01:01:03The One Bright Start in the Healthcare Industry

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.