“The United States is afflicted with new eras. Let us not think that the current illusion is unique. It is intimately part of the American character," said the great American economist, John Kenneth Galbraith.

“The United States is afflicted with new eras. Let us not think that the current illusion is unique. It is intimately part of the American character," said the great American economist, John Kenneth Galbraith.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Biotech & Healthcare Letter

October 27, 2020

Fiat Lux

FEATURED TRADE:

(HOW VERTEX IS CURING THE INCURABLE)

(VRTX), (PTI), (GLPG), (CRSP)

Erratic. Unpredictable. Volatile. Take your pick of the descriptions used when it comes to biotechnology stocks. Each of these adjectives can be a fitting descriptor to the industry most of the time.

However, not all biotechnology companies fall under that category. Some are reasonably stable, offering steady and increasing profits.

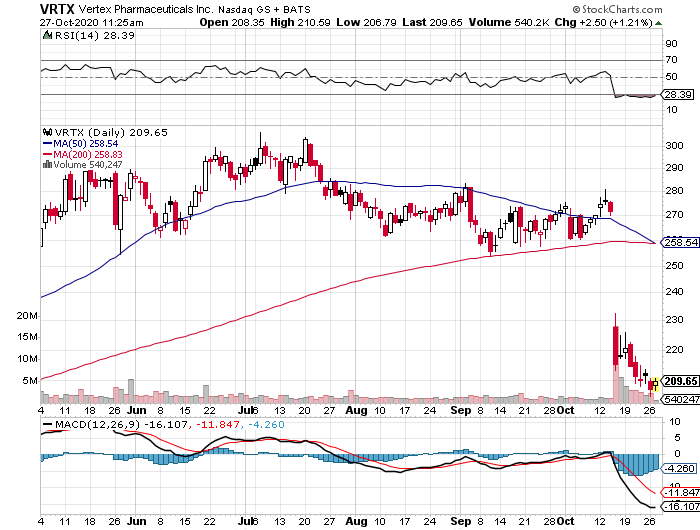

Vertex Pharmaceuticals (VRTX) is one of those biotechnology stocks that you can simply buy and hold for over a decade without losing any sleep.

One of the key factors in Vertex’s success is its monopoly on the cystic fibrosis (CF) market.

CF is a rare and life-threatening genetic disease that affects a patient’s digestive system and lungs. To date, there is no cure for this condition that overshadows the lives of 68,000 individuals in the US and the EU. However, there are treatment options for it.

Vertex developed the first-ever FDA-approved drug, Kalydeco, for the condition. As expected, it gained the much-coveted head start that led to its dominance today.

Its closest rivals, Proteostasis Therapeutics (PTI) and Galapagos NV (GLPG), are years away from ever catching up to the Massachusetts-based biotechnology stalwart. Neither has an approved drug as of today.

Since the approval of Kalydeco in 2012, Vertex stock has been enjoying an upward trajectory. With the recent addition of another CF blockbuster, Trikafta, the company is anticipated to keep its momentum.

From the moment Trikafta was released to the market, Vertex’s revenue and bottom line showed impressive growth. The drug, which is a triple combination therapy, is projected to capture almost 90% of the CF market worldwide.

Needless to say, Vertex has made it in the shade for at least the next 5 years, thanks to its CF market dominance.

In its second quarter earnings report, Vertex showed a 62% jump in its revenue year over year to hit $1.52 billion. Its net income of $837 million demonstrated a whopping 213% increase compared to the same period in 2019.

As anticipated, the star of the show was Trikafta.

The drug raked in $918 million in the second quarter alone – an amount higher than the combined sales of all the drugs in Vertex’s product line and an impressive growth from the $420 million it contributed last year.

As Vertex’s bottom line grew, its margins showed substantial improvement as well. Its operating margin for the second quarter of 2020 is at 57% compared to 44% during the same quarter last year.

With Vertex’s key metrics topping expectations, the company changed its 2020 revenue guidance from $5.7 billion to $5.9 billion, showing off a noteworthy increase from the $4 billion in sales it reported in 2019.

Although its CF pipeline has a number of promising candidates, Vertex is also looking outside the market for additional avenues of growth.

One of the most promising and exciting partnerships it forged in the past decade is with gene-editing company CRISPR Therapeutics (CRSP).

Just looking at this collaboration makes it clear that Vertex is once again playing the long game.

What we know so far is that the two companies are working on a treatment, called CTX001, for rare genetic blood disorders sickle cell disease and transfusion-dependent beta-thalassemia.

They are also developing two potential treatments for alpha-1 antitrypsin deficiency (AATD), which is a rare genetic liver and lung disorder that is similar to CF.

Detractors might point out that Vertex is a pricey stock. However, this biotechnology company currently has $71.2 billion in market capitalization.

More notably, it has no debt and holds $5.5 billion in cash. That puts the true value of Vertex at roughly $65.7 billion.

I believe that the biotechnology company’s overall outlook more than does justice for its valuation.

Granted that it is trading at 11 times its revenue and 26 times its adjusted EPS, its consistent performance and promising future ensure that its investors will be getting more bang for their buck.

In a word, Vertex remains a first-rate biotechnology stock to buy.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

October 27, 2020

Fiat Lux

Featured Trade:

(DECODING THE GREENBACK),

(THE TECHNOLOGY NIGHTMARE COMING TO YOUR CITY)

Mad Hedge Technology Letter

October 26, 2020

Fiat Lux

Featured Trade:

(WHAT DOES DIGITAL UPSKILLING MEAN TO TECH?)

(AAPL), ($COMPQ)

The signals are there offering the impetus to the U.S. workforce to become increasingly tech-savvy in a hurry.

A word was even coined for it: “Digital upskilling.”

The idea of this development in digital skills is, in fact, the reason why every investor needs to look at tech growth stocks as the cornerstone of their investment portfolio.

To understand the trajectory of tech growth stocks, analyzing the entry level of industry employment offers a clearer snapshot of the meat and bones of the industry.

The tech workforce is upskilling precisely because they are incentivized with the opportunity to secure higher salaries.

The higher salaries exist precisely because tech corporations can afford to pay their workers more when they participate in a business cycle that delivers 40% higher revenue than the year before.

It’s a virtuous cycle that not only enriches the shareholder but is a golden chance for U.S. workers to secure a high-quality life when other U.S. industries like retail, hospitality, and energy have crashed and burned.

The very day that tech companies stop doling out larger than life salaries will be the cue that we are at ex-growth and investors must be able to pivot quickly to target the next growth part of the economy.

The great x-factor of technology is that there will always be a new start-up tech reshaping the industry and old technologies just become obsolete like the fax machine and Atari game console.

Therefore, the upskilling at all levels of the tech ladder means the possibility that someone will strike it rich by discovering a new technology that is able to revolutionize the industry.

Companies are even offering in-company courses to encourage employees to hone their skills.

This can often lead to exciting promotions even in a time where the economy has been throttled to a standstill.

The latest accelerator has been none other than the coronavirus as corporations have been forced to continue operations without the help of a physical office.

Corporations are fast-tracking their embrace of digital technologies and enabling workers to learn wherever they are, whenever they want, on any device.

Around 86% of top-performing companies reported that digital training programs boosted employee engagement and performance.

The aim of tech companies is to load itself with employees skilled in data science, data storage technology skills, tech support, and digital literacy.

Other marketable skills include software development, digital marketing, and IT administration.

The real hurdle in digital upskilling lies in execution, making an entire workforce digitally savvy is a tough chore and there will always be stragglers bringing up the rear.

Corporates have ploughed full steam into upskilling and even though Silicon Valley hasn’t moved on from the smartphone, it is squeezing as much juice from this grapefruit as it can.

We are now onto the Apple (AAPL) iPhone 12 and who knows, we might get to the iPhone 20 or 30.

We are onto the Apple iPhone 12 because it’s a cash cow and that won’t stop which is why investors need to feed their appetite for premium US tech stocks.

Stocks are divided into “value” and “growth” halves. The former consists of the stocks that are cheapest in relation to net assets, current cash flow, and so on. These tend to be older, duller, and less exciting companies.

The other half, “growth,” tends to consist of the glamorous companies that have monopolies.

Just look at the performance of value stocks. The average U.S. large company “value” mutual fund has lost 8% so far this year, even including reinvested dividends.

The average growth fund? It’s up a stunning 30%. And this gap has been going on for years: “Growth” funds have beaten “Value” funds since as far back as 2007, market data show.

From the upskilling at entry-level jobs, there are signs everywhere that investing in high growth tech is the way to go and if you compare tech to the rest of the market in 2020, the numbers are a no-brainer.

“I would trade all of my technology for an afternoon with Socrates.” – Said Co-Founder of Apple Steve Jobs

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more