Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

It is not at all surprising that the biggest names in the healthcare industry are dominating the COVID-19 vaccine race.

After all, Big Pharmas such as Pfizer (PFE), AstraZeneca (AZN), Johnson & Johnson (JNJ), and Sanofi (SNY) are backed with vast resources that even media favorites like Moderna (MRNA) find challenging to compete against.

For months now though, going head to head with these big-name frontrunners is a clear outlier: Novavax (NVAX).

So far, there are only 10 COVID-19 vaccine candidates that have reached late-stage testing and Novavax’s NVX-CoV2373 has been performing at par (if not better) than its rivals—and the market has definitely noticed.

When 2020 started, Novavax’s market capitalization was less than $130 million and traded at roughly $4 per share.

Ten months into the pandemic, this small biotechnology company’s market cap grew to over $6.5 billion and has been trading at $110 per share—and that is already after a price decrease in the past weeks.

Given the disparity in its size and resources compared to its competitors, it’s safe to say that Novavax has been punching way above its weight class particularly in terms of landing supply agreements for its COVID-19 program.

Novavax first received a CEPI grant in March worth $4 million, which was immediately dwarfed by the $384 million the biotech company got in May.

In a matter of months, Novavax joined the major league players and secured a $1.6 billion funding courtesy of the US government’s Operation Warp Speed program.

In exchange, the biotech company will supply 100 million doses of NVX-CoV2373 to the US upon approval.

Novavax also inked an agreement with the UK for 60 million doses and another with Canada for 76 million doses.

Novavax has also landed deals with Japan through Takeda Pharmaceutical (TAK) and India via the Serum Institute of India.

As expected, the grants and supply agreements were perceived as votes of confidence on Novavax’s work and the company reaped the rewards.

In March, the prices started moving from less than $10 per share to almost $50.

By May, the price moved up to roughly $80 per share.

After its Operation Warp Speed contract in July, Novavax’s price per share soared all the way to $189 before eventually falling to $110 this October.

Novavax has only conducted late-stage testing in the UK. But, Phase 3 is expected to begin in the US soon as well.

Admittedly, a lot is riding on NVX-CoV2373.

However, the company has actually offloaded the majority—if not all—of its financial risks linked to the program.

Riding the momentum of its COVID-19 vaccine candidate, Novavax has been working on a related influenza vaccine called Nanoflu.

Given the market size for this, Nanoflu is estimated to rake in an annual revenue somewhere between $550 million and $1.7 billion.

Another potential blockbuster is respiratory syncytial virus (RSV) vaccine ResVax, which is projected to reach peak sales of $2 billion.

Novavax is also working on a vaccine candidate for the Ebola virus, the Middle East Respiratory Syndrome (MERS-CoV), and Severe Acute Respiratory Syndrome (SARS).

While NVX-CoV2373 is anticipated as Novavax’s moneymaker in the coming years, the biotech company can only realistically expect massive sales from this until 2023.

Looking at the company’s manufacturing partnerships and the aggressive timeline it has taken, Novavax is expected to produce 2 billion doses of its COVID-19 vaccine by mid-2021.

This is great news for its investors because of Novavax’s smaller market capitalization compared to its competitors.

Since the biotech company is projected as one of the first companies—if not the first—to offer a vaccine, then it can cover a substantial market share before its bigger rivals take over the market.

Even if Novavax prices its COVID-19 vaccine cheaply, say, $10 per dose, it can still generate $20 billion in annual sales.

Moreover, the late-stage success of NVX-CoV2373 will definitely cause Novavax’s stock price to skyrocket.

Despite this potential though, it’s important to keep in mind that this biotech company still has a way lower market cap than its rivals.

That means its share price will move a lot higher compared to the stocks of the other vaccine leaders.

Therefore, Novavax’s small size is not a negative for its investors—it is actually an advantage.

So for biotech investors who are searching for a promising COVID-19 vaccine stock, there’s nothing cheaper and more promising than Novavax.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

October 22, 2020

Fiat Lux

Featured Trade:

(IS AIRBNB YOUR NEXT TEN BAGGER?),

(WYNN), (H)

Mad Hedge Technology Letter

October 21, 2020

Fiat Lux

Featured Trade:

(WILL ANTITRUST PROBLEMS UNLEASH GOOGLE?)

(GOOGL), (AMZN), (FB), (AAPL)

The Department of Justice and 11 U.S. states filing an antitrust lawsuit against Google isn’t as bad as it seems.

Abusing its monopoly power to make Google the default search service on browsers, mobile devices, computers, and other devices has meant quarter after quarter of cash cow growth.

Alphabet’s cash reserves are to the point where they can fritter away capital on loss-making divisions like autonomous driving technology Waymo.

Yes, it’s true that Google is no longer the scrappy start-up that they once were, but that doesn’t matter, and they certainly have the financial balance sheet to deal with any litigation that might or might not take place.

Part of the Google shares not selling off was validation that they are resourceful enough to get through this unscathed and they certainly have had years to prepare how to defend itself through the courts.

Google let their position known publicly by tweeting that the “lawsuit by the Department of Justice is deeply flawed. People use Google because they choose to — not because they're forced to or because they can't find alternatives.”

The standard corporate speak that Google uses is just a sign of the times where big tech has dwarfed the banks, is too big to fail and of pure clout in American government, business and society.

This has been a long time coming as the firm has been under investigation by the Justice Department, the Federal Trade Commission, and state attorney general that its search engine and digital advertising businesses may operate as illegal monopolies.

The specific lawsuit will likely reference competitors like Bing for denying them access to user data, as well as targeting Google’s “search advertising.”

It was only in July, Alphabet CEO Sundar Pichai, along with the CEOs of Amazon (AMZN), Apple (AAPL), and Facebook (FB) appeared before a hearing of the House Judiciary Committee’s Subcommittee and were made to look bad for their dominant position in the digital ad game.

Google has repeatedly pointed to earlier antitrust investigations by the FTC and state attorney general into its display search business that concluded in 2013 and 2014 without incident but they surely have known that this issue would pop back up time and time again.

The knock-on effects have been drastic with American innovation sapped of its incubatory juices.

In the modern age of tech, it’s almost impossible to build a unicorn from scratch without getting your business model hijacked from one of the anti-competitive tech firms.

And now — there are 6 tech firms that use their scale and power to drag down innovation.

The consequences have been higher share prices for big tech because if they can’t scare competition out of place, they will either buy them or find internal ways to sabotage their business ala Yelp.

Google’s digital advertising business has faced accusations due to its unrivaled size and volume which is also why it makes so much money.

The company controls some of the most important links in the online advertising chain, centrally its DoubleClick platform, a premier tool for online publishers, helping them to create, manage, and track online marketing campaigns.

This is why the “internet” or the companies that have access to tracking technology know everything about you and can front run the marketing process to cater towards you.

Acquired in 2007, DoubleClick was cited by Senator Elizabeth Warren (D-MA) as one of the major acquisitions Google should be forced to unwind to improve competition in the advertising space.

If DoubleClick were to unwind itself from Google, they would be an instant unicorn out of the gate.

And that isn’t just the only unicorn in the stable, there are many stand-alone unicorns in Google’s umbrella of assets — from Gmail, Google Cloud, Google Maps, YouTube, and even Google’s hardware division that manufactures phones such as the Google Pixel line.

I believe in the argument that the sum of the parts is dragging down each segment meaning once broken from the Alphabet death grip, each unicorn would be able to pursue decisions that are best suited for their own division and not just the parent company Alphabet.

There is only so long that each unicorn is willing to play for the team and once they go out into the wild, each will become its own unique growth company.

One possibility is Google’s search business spun out while the other businesses stay inside under parent company which is also viable since the investigations specifically pinpoint Google search.

Google search controls more than 90% of the world’s search traffic market share and most notably, Yelp complain about Google favoring its own products in search results.

In July, a Wall Street Journal investigation found Google’s search algorithm biased towards its own YouTube videos in search results over those of other services.

Google’s repeated abuses would likely be mitigated just by spinning out Google search and not allowing them to favor itself.

It is highly unlikely that a stand-alone Google search business would cede market share because they are simply the best search engine by a country mile.

They would most likely expand on the lead they already have.

In either case, if Google isn’t broken up, they win, and the share price will rise.

If they are broken up, the victory will be even more emphatic while supercharging each individual asset ending up in an even higher share price.

This could finally offer a jolt of innovation into the stagnant tech space which honestly has too many too-big-to-fail companies that are focused more on financial engineering at this point.

“Wear your failures as a badge of honor.” – Said Current CEO of Alphabet Sundar Pichai

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

October 21, 2020

Fiat Lux

Featured Trade:

(WHY YOU MUST AVOID ALL EV PLAYS EXCEPT TESLA),

(TSLA), (GM)

Markets live on fads. Once a certain investment theme takes hold, the imitators start coming out of the woodwork in droves.

In 1989, all of the largest Japanese banks stampeded to issue naked short put options on the Nikkei Average by the billions of dollars when the index was at an all-time high. It then fell by 85%.

I remember signing the paperwork on a $3 billion deal for the Industrial Bank of Japan on behalf of Morgan Stanley. It’s been 31 years, but I’m still waiting for those investors to come after me.

Then there was the peak of the Dotcom Bubble in 2000 and no less that five online pet food delivery companies raised billions. (remember those cute sock puppets?) Every one of them went under.

So, what has been one of the biggest fads of 2020?

That would be electric vehicles.

You no longer have to wear Birkenstocks, grow your hair long, and smoke pot to drive an electric car. They are about to become a major part of the American economy. According to Adam Jonas at Morgan Stanley, EVs account for 1.3% of the total car market today and will grow to 10% by 2025 and 25% by 2030.

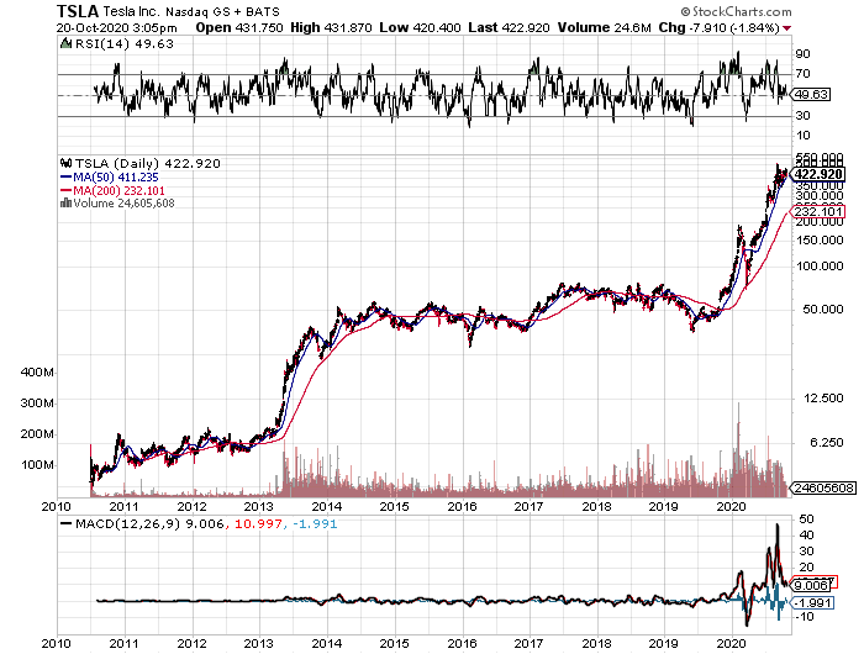

I have been involved in Tesla since its earliest days back in 2003. Then it was one rich man’s hobby, with technology that was a reach at best, and unlikely to ever see the light of day as a public company. There it remained for seven years.

Then they brought out the Model S in 2010, which I snapped up as fast as I could, picking up chassis no. 125 at the Fremont factory. My signature is still on the wall there. If it worked this had the potential to be a real car. If it didn’t, I would wind up with $100,000 worth of inert aluminum, steel, silicon, rubber, and copper.

The trials were then only just beginning for Musk. He faced nervous breakdowns, sleeping in factories, and SEC prosecutions. After a decade of abuse, suddenly everything clicked. Total Tesla production soared to over one million units and the shares leaped 150-fold to $500 from their post IPO low of $3.30. That move financed a lot of retirements among my readers.

I remember what Steve Jobs once told me; “Like many overnight successes, this one took decades to pull off.”

Suddenly, making electric cars looked easy. Raising money to finance them looked even easier.

Enter the hoards, which I list below, a roll call of the shameless:

Nikola Badger – Roll out is expected in 2021 and has a hydrogen fuel cell power source that hasn’t a hope in hell of ever becoming economic. As I never tire of explaining to investors, while electric power is digital and scalable, hydrogen is analog and isn’t. Maybe that’s why the stock is down 83% since June. Too many unbelievable promises and no actual functioning model. Gravity was their only actual power source.

Fisker – If at first, you don’t succeed, why not fail again? This had double the number of parts of a conventional international combustion engine. Its chief claim to fame was that it got a free factory from the government in Joe Biden’s home state and the fact that Justin Bieber drives one. More flailing at the wind.

Aspark Owl – A $3.2 niche supercar with appeal to maybe three car collecting Saudi princes.

Bollinger B1 – Is a $125,000 SUV expected from a Michigan startup with only a 200-mile range. Why not pay nearly double the cost of a Tesla Model X and get half the performance?

The Byton M-Byte – Is a $45,000 crossover car from a Chinese start up. China has actually been building electric cars longer than Tesla, but they have a tendency to breakdown or catch on fire. Quality and safety problems have until now kept them out of the US, and probably always will.

Genesis Essentia – A Croatian-based startup with a major investment from South Korea’s Hyundai. It will most likely never get off the drawing board. The last time Croatia built cars was for the Austria Hungarian Empire during WWI.

Rivian R1T – A startup with a reasonably priced truck and up to 400 miles of range that will only make it because they have a 100,000-unit order from the largest shareholder, Amazon (AMZ). It’s perfect for local deliveries.

By now, virtually every major car manufacturer has or is about to roll out its own entry in the electric car race. I list them below, skipping those that are more than two years out over the horizon. Notice the profusion of the letter “e” in the names.

They include the Porsche Taycan, Audi eTron, Jaguar I-Pace, Austin Mini Electric, Fiat 500e, Kia Niro EV, BMW i3, Chevy Bolt EV, Hyundai Kona Electric, and the Hyundai Ioniq Electric, Ford F-150 Electric, Ford Mustang Mach-E, and Nissan Ariya.

Not one of these comes even close to the price/performance and battery density of the Tesla cars. Tesla is a decade ahead of the competition and is accelerating its lead. At best, they will sell a few electric cars to those who are intensely loyal to their brands and lose money doing it.

In the meantime, Tesla hasn’t been sitting on its hands. Elon Musk plans to bring out a $25,000 model in two years that will bar entry to the field any other competitor. It is bringing out its own $250,000 supercar, the Tesla Plaid, which will go zero to 60 MPH in 1.9 seconds and have a 600-mile range. The Tesla Cyber Truck at $40,000 has the specs to take on the enormous US pickup market. Did I mention that the company is on the verge of developing technology that will improve battery performance by a staggering 20-fold?

So Tesla is branching out to suck up every profit in every branch of the entire global auto industry.

And this is what most traders, especially the short sellers, got wrong about Tesla. The data is worth more than the car. The miles driven provide a springboard from which the company can offer very high value-added and profitable services, like autonomous driving. Not even Alphabet (GOOGL) can replicate this.

When I bought my first Tesla more than a decade ago, I knew I was betting on the company. The big risk was that General Motors (GM) would step in with their own cheap electric car and drive Tesla out of business.

In the end (GM) did that, but too little, too late. It’s Chevy Bolt EV didn’t hit the market until the end of 2016. Today, it offers a boring design, lacks autonomous driving, possesses only a 259-mile range for $36,620, and is subject to recall, thanks to recurring battery fires (click here for the link).

The quality is, well, Chevy quality.

This year, Chevy will sell under 20,000 Bolts. Tesla is approaching 500,000. It’s too late to close the barn door after the horse has “bolted,” as GM is earning. Over the past decade, Tesla shares are up 150 times. GM shares are nearly unchanged during the greatest bull market of all times.

It is competing against Teslas that are 20 years from the future, are fully autonomous, goes to street-to -treet autonomous driving next year, and upgrades itself once or twice a month.

Make mine Tesla, please, which will soon become the world’s first trillion dollar car company. Don’t waste your time or money on the others, either as a driver or investor.