Global Market Comments

September 30, 2020

Fiat Lux

Featured Trade:

(INDUSTRIES YOU WILL NEVER HEAR FROM ME ABOUT

Global Market Comments

September 30, 2020

Fiat Lux

Featured Trade:

(INDUSTRIES YOU WILL NEVER HEAR FROM ME ABOUT

Industries You Will Never Hear from Me About.

The focus of this letter is to show people how to make money through investing in fast-growing, highly profitable companies which have stiff, long-term macroeconomic and demographic winds at their backs.

That means I ignore a large part of the US economy, possibly as much as 80%, whose time has passed and are headed for the dustbin of history.

According to the Department of Labor's Bureau of Labor Statistics, the seven industries listed below are least likely to generate positive job growth over the next decade.

As most of these stocks are already bombed out, it is way too late to short them. As an investor, you should consider this a “no go” list no matter how low they go. I have added my comments, not all of which should be taken seriously.

1) Realtors - The number of realtors is only down 10% from its 1.3 million peak in 2006. I have always been amazed at how realtors who add so little in value take home so much in fees, still around 6% of the gross sales price. Someone is going to figure out how to break this monopoly. The Internet is begging to destroy this business model.

2) Newspapers - these probably won't exist in five years, as five decades of hurtling technological advances have already shrunk the labor force by 90%. Go online or go away. Good thing I got out in time….40 years ago.

3) Airline employees - This is your worst nightmare of an industry, as management has no idea what interest rates, fuel costs, or the economy will do, which are the largest inputs into their business. Pilots will eventually work for minimum wage, or for free, just to keep their flight hours up.

4) Big telecom - Can you hear me now? Nobody uses landlines anymore, leaving these companies with giant rusting networks that are very costly to maintain. Since cell phone market penetration is 90%, survivors are slugging it out through price competition, cost cutting, and all that annoying advertising. How many Millennials even have land lines? About 30%.

5) State and Local Government - With employment still at levels private industry hasn't seen since the seventies, firing state and municipal workers will be the principal method of balancing ailing budgets. Expect class sizes to soar to 80 or go entirely online, to put out your own damn fires, and keep the 9 mm loaded and the back-door booby trapped for home protection. Anyone who sells to local governments is toast.

6) Installation, Maintenance, and Repair - I have explained to my mechanic that the motor in my new electric car has only eleven moving parts, compared to 1,500 in my old clunker, and this won't be good for business. But he just doesn't get it. Electric cars will soon price internal combustion ones out of the market.

The winding down of our wars in the Middle East is about to dump a million more applicants into this sector. The last refuge of the trained blue-collar worker is about to get cleaned out.

7) Bank Tellers - Since the ATM made its debut in 1968, this profession has been on a long downhill slide. Banks have lost so much money in the financial crisis, they can't afford to hire humans anymore. Thanks to the pandemic half of the big national branch networks have been closed.

It hasn't helped that hundreds of banks have closed during the recession, with many survivors merging to cut costs (read fire more people). Your next bank teller may be a Terminator.

Out With the Old

And in With the New

Mad Hedge Biotech & Healthcare Letter

September 29, 2020

Fiat Lux

(WHY THE PANDEMIC ISN’T STOPPING ELI LILLY’S WINNING STREAK)

(LLY), (PFE), (MRNA), (AZN), (GILD), (INCY), (REGN), (NVO), (BIIB)

Vaccine developers have taken center stage on Wall Street since the pandemic started, with companies like Pfizer (PFE), Moderna (MRNA), and AstraZeneca (AZN) enjoying soaring share prices for months now.

One of the primary reasons for this popularity is the US government’s Operation Warp Speed, which poured $11 billion into its chosen COVID-19 vaccine programs.

Realistically, the cold, hard truth is that a COVID-19 vaccine will not be the panacea for this deadly virus.

While the vaccine developers are rushing to complete their clinical trials, more people continue to die from COVID-19.

With almost a million deaths and over 30 million cases recorded to date, the need for treatments is more pressing than ever.

Among the companies working on COVID-19 treatments, one name has been quietly making headway: Eli Lilly (LLY).

So far, the company has two potential treatments that can cure COVID-19 patients.

One is its rheumatoid arthritis drug Olumiant, which the company developed with biotechnology firm Incyte (INCY).

Results showed that the treatment can lessen the days patients stay in hospitals when combined with Gilead Sciences’ (GILD) Remdesivir. Not only that, the combination also reduced the severity of the disease and allowed for less-intensive hospital care.

Once all the results have been tested and validated, Eli Lilly will seek an emergency authorization from the FDA.

Aside from Eli Lilly and Gilead Sciences, Pfizer is also working on a potential COVID-19 treatment. Although not much is known about the New York biopharmaceutical giant’s version of the antiviral drug, the target approval date is set in the second half of 2021.

Riding on the momentum of its successful Olumiant trials, Eli Lilly is working to extend its winning streak by being one of the first to develop a preventive COVID-19 treatment specifically designed for elderly patients.

Eli Lilly is developing the potent monoclonal antibody treatment, called LY-CoV555, with AbCellera. The Phase 3 trials conducted in nursing homes were launched in August and the company expects the results to be available by March 2021.

While using monoclonal antibody treatment is groundbreaking technology, Eli Lilly is not alone in the field.

The company faces considerable competition from other healthcare giants like AstraZeneca and Regeneron (REGN).

Nonetheless, the antibody market is massive enough for sharing, with this market estimated to rake in as much as $10 billion annually.

Conservatively speaking and assuming that Eli Lilly fails to attract major market share, there’s still a decent chance that the sales of LY-CoV555 can go beyond $1 billion every year starting 2022.

Outside its COVID-19 programs, Eli Lilly is a dominant player in the diabetes market, with Trulicity leading the charge along with up and coming products like Humalog, Jardiance, Basaglar, and Humulin.

The company is expected to attract at least 13.8% of the market share this year, ranking second only to Novo Nordisk (NVO) and its 30.7% hold of the sector.

In the second quarter earnings report this year, Trulicity sales showed a 20% year-over-year jump to reach $1.2 billion in that period.

This is an impressive performance as investors expect the diabetes drug to surpass its 2019 sales of $4.1 billion.

Although Trulicity delivers substantial sales, it is remarkable that Eli Lilly is not overly reliant on the drug.

In fact, the diabetes drug’s total revenue only accounts for less than one-fifth of the company’s overall sales.

To boost its presence in the diabetes market, Eli Lilly added another potential blockbuster in its pipeline: Tirzepatide.

This drug is projected to become “best-in-class for lowering glucose, weight loss, and cardiovascular risk.”

To date, Tirzepatide is undergoing Phase 3 trials to test it on diabetes, obesity, and heart disease. It is also queued in Phase 2 trials for the liver disease NASH.

The potential of Tirzepatide is hinged not only in being a diabetes drug but more importantly, as an obesity drug.

If successful, Tirzepatide is estimated to hit peak sales of $10 billion annually, with the number trailing by 2025 to record $3.7 billion.

Another potential moneymaker for Eli Lilly is Verzenio, which showed an impressive 56% increase in sales in the second quarter to contribute $208.6 million.

In a bid to expand its oncology pipeline, Eli Lilly is looking into adding a new indication for Verzenio as well.

The company recently released the promising results for the oral tablet as an early-stage breast cancer treatment.

If successful, this drug will be in direct competition against an industry leader, Pfizer’s Ibrance.

In terms of its neurology pipeline, Eli Lilly has also been active in developing its own Alzheimer’s program.

While most of the treatments are still in the early stages, the success of Biogen’s (BIIB) Aducanumab could provide a much-needed boost for Eli Lilly’s own Alzheimer’s candidates.

Eli Lilly offers an extensive product line that goes beyond its COVID-19 programs, underscoring the company’s resilience even during the pandemic.

After dominating in the diabetes sector, the company focused its efforts on becoming one of the top players in the oncology, immunology, and neurology fields.

Consequently, Eli Lilly has been consistent in posting first-rate earnings and revenue growth since 2017.

Eli Lilly markets treatments for life-threatening and chronic conditions, with the company owning the rights to products with consistently growing sales. It also has the ability to continuously boost its revenue stream thanks to its rich pipeline and strategic collaborations.

The COVID-19 pandemic may have negatively affected sectors of Eli Lilly’s business this year, but the company holds the qualities that make it a solid long-term investment.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

September 29, 2020

Fiat Lux

Featured Trade:

I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE),

(SOME SAGE ADVICE ON ASSET ALLOCATION)

Mad Hedge Technology Letter

September 28, 2020

Fiat Lux

Featured Trade:

(THE SIMPLE WAY TO SUPERCHARGE YOUR TECH PORTFOLIO)

(WCLD), (EMCLOUD)

Superiority is mainly about taking complicated data and finding perfect solutions for it; and trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the overarching themes I have promulgated since the launch of the Mad Hedge Technology Letter in February 2018.

Well, if you thought every tech letter until now has been useless, this is one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you.

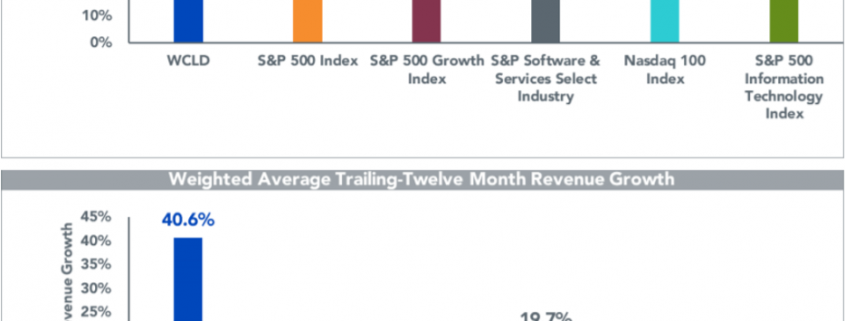

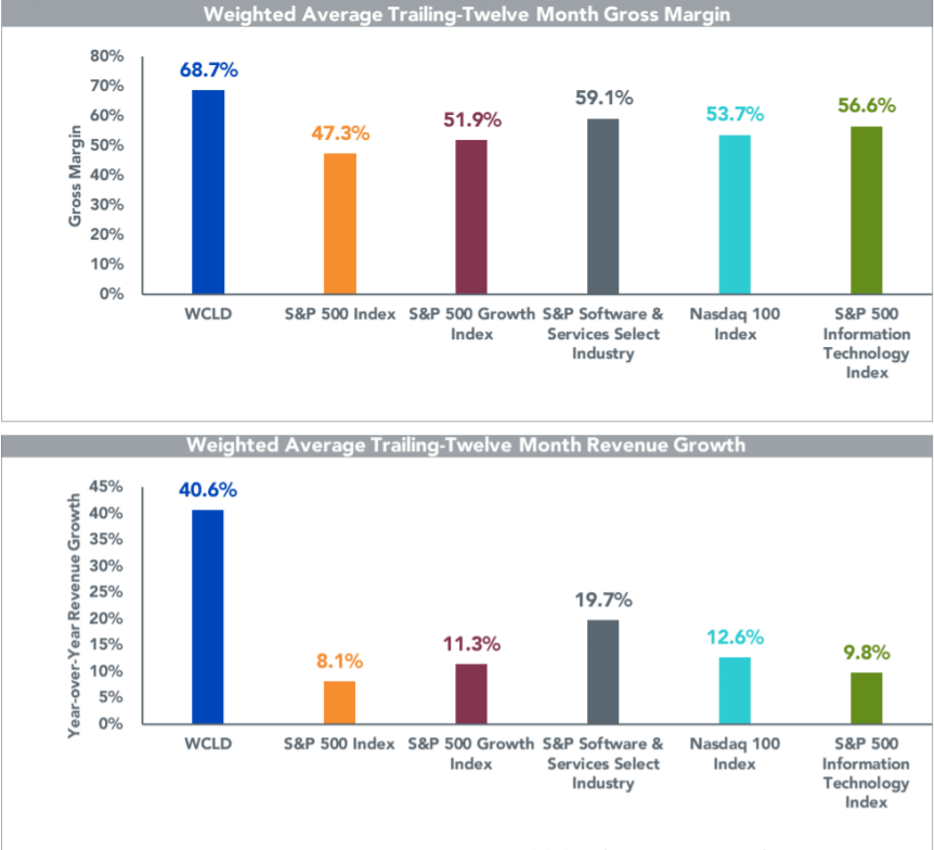

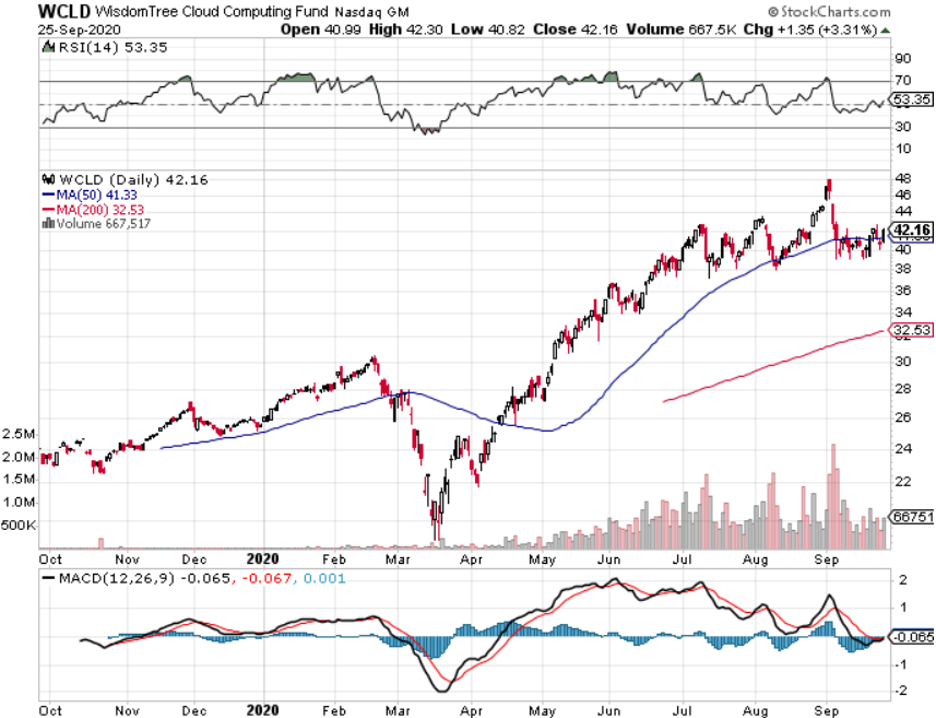

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

This is the idea that is powering the “shelter-at-home” trade which has been hotter than hot in 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge to accelerate due to advancements in artificial intelligence and the Internet of Things (IoT).

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry. Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Business Model Advantages

I believe the product and business model advantages of cloud SaaS companies have historically led to better margins, growth, free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must suffice critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD stock are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 40% from the lows they saw in March and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a direct play on cloud computing, but the elements of its cloud business is nothing short of brilliant.

But ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more risk because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extra-ordinary tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner.

“Learning to fly is not pretty but flying is.” – Said CEO of Microsoft Satya Nadella

Global Market Comments

September 28, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DID THE ELECTION OR COVID JUST HIT THE STOCK MARKET?),

(SPY), (TLT), (GLD), (TSLA), (UUP)