“Technology is the knack of so arranging the world that we do not experience it.” – Said American existential psychologist Rollo May

“Technology is the knack of so arranging the world that we do not experience it.” – Said American existential psychologist Rollo May

Global Market Comments

March 8, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHAT’S UP WITH TECH?),

(MSFT), (TSLA), (AAPL), (QQQ), (NVDA), (MU), (AMD), (BRKB), (ARRK), (ROM), (VIX), (FCX), (TLT), (BRKB), (TSLA), (JPM), (SPY), (QQQ), (SPX)

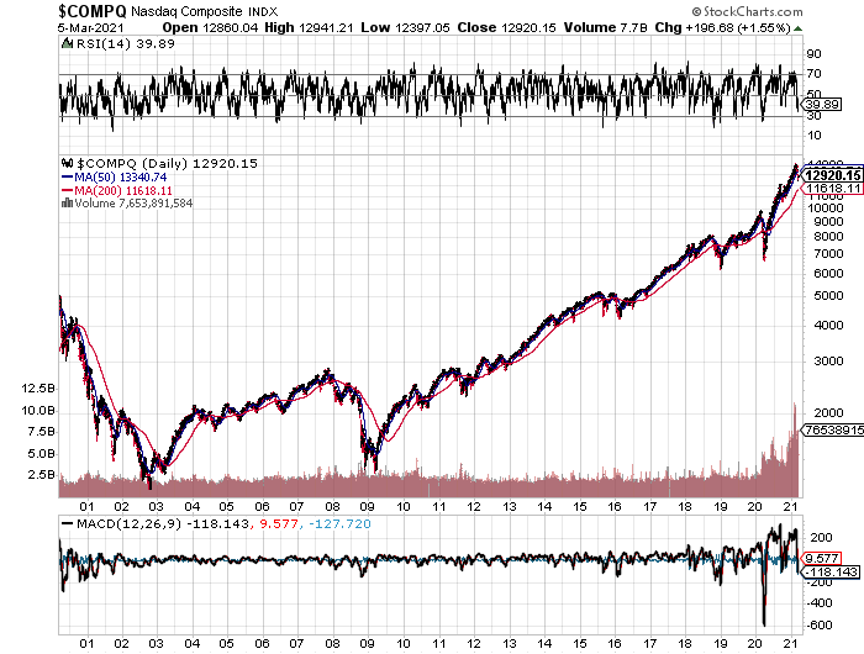

That great wellspring of personal wealth, technology stocks, has suddenly run dry.

The leading stock market sector for the past decade took some major hits last week. More stable stocks like Microsoft (MSFT) only shed 8%. Some of the highest beta stocks, like Tesla (TSLA), took a heart-palpitating 39% haircut in a mere two months.

Have tech stocks had it for good? Has the greatest investment miracle of all times ground to a halt? Is it time to panic and sell everything?

Fortunately, I have seen this happen many times before.

Technology is a sector that is prone to extremes. Most of the time it is a hero, but occasionally it is a goat. When too many short-term traders sit in one end of the canoe, we all end up in the drink.

This is one of those times.

Technology stocks undeniably need a periodic shaking out. You need to get rid of the day traders, the hot money, the excessively leveraged, and find out who has been swimming without a swimsuit. The sector rotates between being ridiculously cheap to wildly overvalued. We are currently suffering the latter.

During the past 12 years, Apple’s (AAPL) price earnings multiple has traded from 9X to 36X. It was a value play for the longest time, all the way up to 2016. Nobody believed in it. It is currently at a 33X multiple. While the stock has gone nowhere since August, its earnings have increased by more than 10%, and better is yet to come.

After trading tech stocks for more than 50 years, I can tell you one thing with certainty.

They always come back.

And this time, they are in position to come back sooner, faster, and bigger than ever before. Remember the Great Dotcom Bust of 2000-2003? It lasted two years and nine months and saw NASDAQ (QQQ) crater by 82%, from 5,000 to 1,000. This time, it’s only dropped by 13%, by 1,850 from 14,250 to 12,400.

I don’t see the selloff lasting much longer or lower, no more than another 5%-10% until September. For these are not your father’s technology stocks.

There are only three numbers you need to know. Technology now accounts for a mere 2% of the US workforce, but a massive 27% of stock market capitalization and 37% of total us company earnings. A sector with such an impressive earnings output won’t fall for very long, or very far.

The pandemic accelerated technological innovation tenfold. Companies now have mountains of cash with which to bring forward their futures.

This is no more true than for biotech stocks. The technologies used to create Covid-19 vaccines can be applied to cure all human diseases. And they now have mountains of cash to implement this.

So, I’ll be taking my time with tech stocks. But they are setting up the best long side entry point since the March 20, 2020 pandemic low.

The biggest call remaining for 2021 is when to take profits and sell domestic recovery value stocks and rotate back into tech. But if you are running the barbell strategy I have been harping about since the presidential election, the work is already being done for you.

Nonfarm Payroll comes in at a blockbuster 379,000 in February, far better than expected. It a preview of explosive numbers to comes as the US economy crawls out of the pandemic. That’s with a huge drag from terrible winter weather. The headline Unemployment rate is 6.2%. The U-6 “discouraged worker” rate is still a sky-high 11%, those who have been jobless more than six months. Leisure & Hospitality were up an incredible 355,000 and Retail was up 41,000. Government lost 86,000 jobs. We are still 12 million jobs short of the year-ago trend. See what employers are willing to do when they see $20 trillion about to hit the economy?

Will US GDP Growth hit 10% this year? That is the sky-high number that is being mooted by the Atlanta Fed for the first three months of 2021. The vaccine is working! They do tend to be high in the home of Gone with the Wind. This Yankee would be happy at 7.5% growth. Manufacturing just hit a three-year high as companies try to front-run imminent explosive growth. The only weak spot is employment, which is still at recessionary highs.

Herd Immunity is here or says the latest numbers from Johns Hopkins University. New cases have plunged from 250,000 to 46,000 in a month, the fastest disease rollback in human history. We may be seeing new science at work here, where mass vaccinations combine with mass infections to obliterate the pandemic practically overnight. If true, the Dow has another 8,000 points in it….this year. Buy everything on dips. The economic data is about to get superheated.

Warren Buffet’s Berkshire Hathaway blows it away, buying back a staggering $25 billion worth of his own stock in 2020, including $9 billion in the most recent quarter. It’s what I’m always looking for, buying quality at a discount. Warren pulled in $5 billion in profits during the last quarter of 2020, up 13.6% over a year earlier. Net earnings were up 23%. If Buffet, a long time Mad Hedge reader, is buying his stock, you should too. Buy (BRKB) on dips. It's also a great LEAP candidate as the best domestic recovery play out there.

Rising rates have yet to hurt Real Estate, as the structural shortage of housing is so severe. Historically speaking, interest rates are still very low, even though the ten-year yield has soared by 82% in two months. Cash is still pouring into REITs coming off the bottom. Home prices always see their fastest moves up at the beginning of a new rate cycle as everyone rushes to beat unaffordable mortgages.

The Chip Shortage worsens, with Tesla shutting down its Fremont factory for two days. The Texas deep freeze made matters much worse, where many US fabs are located, like Samsung, NXP Semiconductors, and Infineon Technologies. Buy (NVDA), (MU), and (AMD) on dips.

Jay Powell lays an egg at a Wall Street Journal conference. He said it would take some time to return to a normal economy. The speed of the interest rate rise was “notable.” We are unlikely to return to maximum employment in a year. We couldn’t have heard of more dovish speech. But all that traders heard was that inflation was set to return, but will be “temporary.” That was worth a 600-point dive in the stock market and a 5-basis point pop in bond yields. My 10% correction is finally here!

Here today, gone tomorrow. Cathie Wood was far and away the best fund manager of 2020. She, value investor Ron Baron, and I, were alone in the darkness four years ago saying that Tesla (TSLA) could rise 100-fold. Cathie’s flagship fund The Ark Innovation ETF (ARKK) rose a staggering 433% off the March 2020 bottom. Alas, it has since given up a gut-punching 30% since the February high, exactly when ten-year US Treasury bonds started to crash. Watch (ARKK) carefully. This is the one you want to own when rates stabilize. It’s like another (ROM).

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

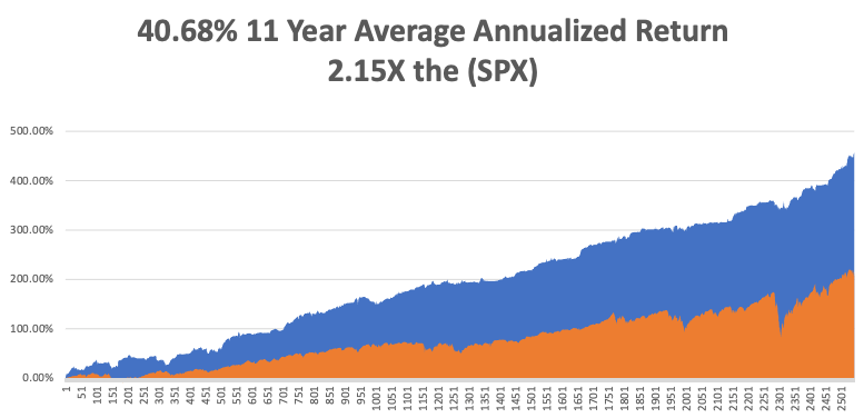

It’s amazing how well selling tops and buying bottoms can help your performance. My Mad Hedge Global Trading Dispatch reached a super-hot 11.61% during the first five days in March on the heels of a spectacular 13.28% profit in February. The Dow Average is up a miniscule 4.00% so far in 2021.

It was a week of frenetic trading, with the Volatility Index (VIX) all over the map. I took profits in Freeport McMoRan (FCX) and my short in US Treasury bonds (TLT) and buying Berkshire Hathaway (BRKB), Tesla (TSLA), JP Morgan (JPM). I opened new shorts in the S&P 500 (SPY) and the NASDAQ (QQQ).

This is my fifth double digit month in a row. My 2021 year-to-date performance soared to 35.10%. That brings my 11-year total return to 457.65%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.68%.

My trailing one-year return exploded to 110.25%, the highest in the 13-year history of the Mad Hedge Fund Trader.

We need to keep an eye on the number of US Coronavirus cases at 29 million and deaths topping 525,000, which you can find here.

The coming week will be a boring one on the data front.

On Monday, March 8, at 11:00 AM EST, Consumer Inflation Expectations for February are out.

On Tuesday, March 9, at 7:00 AM, The NFIB Business Optimism Index for February is published.

On Wednesday, March 10 at 8:30 AM, the US Inflation Rate for February is printed.

On Thursday, March 11 at 8:30 AM, Weekly Jobless Claims are out.

On Friday, March 12 at 8:30 AM, the Producer Price Index for February is disclosed.

At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, it was with great sadness that I learned of the passing of my old friend, Sheikh Zaki Yamani, the great Saudi Oil Minister. Yamani was a true genius, a self-taught attorney, and one of the most brilliant men of his generation.

It was Yamani who triggered the first oil crisis in 1973, raising the price from $3 to $12 a barrel in a matter of weeks. Until then, cheap Saudi oil had been powering the global economy for decades.

During the crisis, I relentlessly pestered the Saudi embassy in London for an interview for The Economist magazine. Then, out of the blue, I received a call and was told to report to a nearby Royal Air Force base….and to bring my passport.

There on the tarmac was a brand-new Boeing 747 with “Kingdom of Saudi Arabia” emblazoned on the side in bold green lettering. Yamani was the sole passenger, and I was the other. He then gave me an interview that lasted the entire seven-hour flight to Riyadh. We covered every conceivable economic, business, and political subject. It led to me capturing one of the blockbuster scoops of the decade for The Economist.

When Yamani debarked from the plane, I asked him “why me.” He said he saw a lot of me in himself and wanted to give me a good push along my career. The plane then turned around and flew me back to London. I was the only passenger on the plane.

When the pilot heard I’d recently been flying Pilatus Porters for Air America, he even let me fly it for a few minutes while he slept on the cockpit floor.

Yamani later became the head of OPEC. At one point, he was kidnapped by Carlos the Jackal and held for ransom, which the king readily paid.

And if you wonder where I acquired my deep knowledge of the oil and energy markets, this is where it started. Today, the Saudis are among the biggest investors in alternative energy in California.

We stayed in touch ever since.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

March 5, 2021

Fiat Lux

Featured Trade:

(THE NEXT BIG TECH GROWTH NAME)

(PLTR)

They are the tech company that beat out Lockheed Martin, BAE Systems, and 14 other unique systems to snatch an NSA contract to provide data analytics to the Five Eyes Alliance in 2011. Palantir has never looked back.

This could become the next 10-bagger.

It’s been that type of overperformance for Palantir since its inception in 2003.

By 2009, they had already amassed over $1.2 billion worth of government contracts and Palantir has already gone through 18 years of product development and spent more than $3 billion on R&D.

Palantir has an unswerving mandate to serve the U.S. government and its allies which has been an effective way to market its services.

This narrow message has effectively knocked out competition from Microsoft, Google, Facebook, Amazon, and Apple who have taken a “friends with everyone but friends with no one” approach to their business empires.

Their companies’ employees have protested against any type of government work with the U.S. army, withering at the thought that they would be responsible for blood on their hands.

Palantir makes sure that prospective employees understand where revenue is procured from and make no apologies for it.

Summing up Palantir is hard to do, but they really are the swiss army knife of data analytics that provide a platform in order to carry out executive decisions that put together trillions of data points from public, private, and secret sources into an easy to use, integrated, one-stop shop system.

This has worked wonders for the U.S. defense agencies and why CEO Alex Carp doubled down with Palantir’s five-year outlook of greater than $4 billion in revenue in 2025.

Starting in 2021, Palantir expects greater than 30% annual revenue growth each year for the next five years.

And in Q1 of this year, Palantir expects revenue growth of 45% or $332 million.

The strong outlook fuses with a sensational full-year 2020 performance of $1.93 billion in revenue, up 47% year over year. Fourth-quarter revenue was $322 million, up 40% year over year, and roughly $21 million above a prior guidance range.

Government revenue accelerated in the fourth quarter growing 85% year over year to $190 million.

Palantir signed several large deals in the quarter including a three-year $44 million expansion with the U.S. Food and Drug Administration and a two-year $31 million agreement with the NHS.

Some of the other deals signed were a multi-year contract with Pacific Gas and Electric to help it streamline operations across the company.

PG&E will now be able to perform root cause analysis and upgrade monitoring.

This should improve PG&Es electric operations and asset management, resulting in enhanced safety and grid reliability.

Palantir has deepened a partnership with BP. And in the fourth quarter, they signed a five-year nine-figure enterprise renewal and have an ongoing relationship with BP since 2014.

The largest part of Palantir’s annual revenue comes from the U.S. military with full-year government revenue rising 77% to $610 million, led by ongoing momentum in the U.S., which grew 91%.

Its Army operation continues to expand.

Palantir recently won a pair of new contracts with the Army to accelerate its modernization efforts.

Palantir was also the beneficiary of the U.S. Army executing its first option year with approximately $114 million as part of a partnership on the Army Vantage program.

Under the $8.5 million Phase 1 contract, Palantir will collaborate with the Army to demonstrate a solution that integrates space, high altitude, aerial, and terrestrial sensors for use in intelligence command and control.

In November 2020, Palantir was selected to provide a prototype for the Army's common data fabric and data security solutions.

Palantir provides an integrated solution that will ultimately improve access to critical data for commanders and soldiers, deliver efficient use of networks and denied integrated environments, and increase the collaboration with joint and allied partners.

The strength isn’t just relegating to U.S. government contracts, Palantir is experiencing intensive growth of existing customers with average revenue per customer growing 41% to $7.9 million.

They grew the number of accounts with $10 million of annual revenue or more by 50%.

For the full year 2020, 43% of Palantir’s revenue was generated from new customers in 2018 or later symbolizing their improving ability to rapidly onboard customers.

Palantir is also just scratching the surface of their commercial business heading into 2021 that saw a revenue rise of 107% year over year in fiscal 2020.

Growth tech firms typically preside over a margin problem at this early stage but Palantir exhibits some of the best margins around with full-year adjusted gross margin of 81%, up 1,000 basis points, compared with full-year 2019.

The year-over-year improvement in gross margin was driven by increased automation and efficiency in the delivery of our software.

Palantir is at the cutting edge of data analytics and whether it’s helping Fortune 500 companies navigate climate change headwinds, implementing Brexit policies for British companies, or modernizing U.S. military operations, they have seized the highest quality revenue possible.

The data analytic company is certainly a play on cyber espionage that is poised to explode on the sovereign and economic level as adversaries have bold plans to weaponize 5G.

One pain point is the overreliance of government contracts; however, I would argue that they are scratching the surface with the commercial operations and the path of least resistance for commercial revenue is up.

The pathway to grow from today’s $38 billion to $200 billion is wide open and if Palantir deploys their best of breed management to grow revenue 30% for the next 5 years, this is easily a $100 stock in the next 2 years.

“I'd rather Apple cannibalize Apple than somebody else cannibalize Apple.” – Said CEO of Apple Tim Cook

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more