Global Market Comments

June 24, 2021

Fiat Lux

Featured Trade:

(WHY DOCTORS, PILOTS, AND ENGINEERS MAKE TERRIBLE TRADERS)

Global Market Comments

June 24, 2021

Fiat Lux

Featured Trade:

(WHY DOCTORS, PILOTS, AND ENGINEERS MAKE TERRIBLE TRADERS)

Mad Hedge Technology Letter

June 23, 2021

Fiat Lux

Featured Trade:

(IGNORE THE GOOGLE COMPLAINTS)

(GOOGL), (AAPL), (MSFT), (FB), (AMZN)

The five largest tech companies last Fall 2020, Apple, Microsoft, Amazon, Alphabet, and Facebook, accounted for 23.8% of the S&P 500 and now that figure has surpassed 25%.

As much as we like to bring out the champagne and celebrate how well big tech has done, the euphoric times often lay the groundwork for the dramatic downfall.

A few warning signs have started to rear their ugly head.

These business models are rock-solid now, but that doesn’t mean the people who manage these business models are always rock-solid too.

Today, I would like to zone in on one of the architects of big tech that have taken one of these behemoths and juiced it up for shareholders — Alphabet CEO Sundar Pichai.

I am not arguing that returning capital to shareholders is bad, but when other critical elements are ignored, it sets the stage for toxicity to fester from the top down.

Don’t get me wrong, revenue and profits are charting new highs every three months for Alphabet.

They are now worth $1.67 trillion and rising. Google and its array of apps have made themselves indispensable in the lives of everyday Americans.

But an increasingly hostile workplace is taking hold that has been made worse by decisive leadership and improving the company has been shelved for a stultifying mindset of incrementalism and bureaucracy.

This is the 2021 version of Alphabet and attrition rates have soured at the management level.

Many of these key managers blame Pichai for leaving mentioning a bias toward inaction and a fixation on public perception as the real mantra inside Google headquarters.

This has created a workplace that has devolved into culture fights, and Pichai’s attempts to “wait out” the problems have an air of arrogance about it that employees don’t like.

Internal surveys are also hard to analyze as employees are indirectly encouraged not to speak out against positions of authority.

However, recently left employees do admit that Google is a more professionally run company than the one Pichai inherited six years ago.

During Pichai’s leadership, it has doubled its workforce to about 140,000 people, and Alphabet has tripled in value. It is not unusual for a company that has grown so quickly to get cautious.

At least 36 Google vice presidents have left the company since last year, according to profiles from LinkedIn.

Google executives proposed the idea of acquiring e-commerce firm Shopify as a way to challenge Amazon in online commerce a few years ago.

Rumor has it that Pichai was turned off by the high price of the asset even though SPOT has tripled in value since then.

As time goes by, Pichai is becoming known as the steward of what Google built before he got there and just a guy there to squeeze out the numbers.

Google was once known as the scruffy start-up and it’s only natural that it has become more conservative in its approaches. They simply have more to lose now.

The meteoric growth has also led to rising concerns about the U.S. stock market becoming increasingly concentrated in a just a few names.

The total market capitalization of U.S. tech stocks reached over $11 trillion, eclipsing that of the entire European market—including the UK and Switzerland, which is now valued at $9 trillion.

Although there are some flaws popping up in Google’s business model, and management appears to be getting worse, I don’t believe we are even close to any sort of in-house meaningful reckoning that would adversely affect its share price.

The external risks are currently far greater than the risk of Google blowing up from the inside.

And while I do acknowledge, it might not be the workplace it once was and much less than ideal, it still pumps out record earnings and the degree to which it outperforms earnings’ expectations is uncanny.

That’s why I would recommend trading this stock aggressively in the short-term while rumors of broken management model are unfounded, because fundamentally and technically, it’s hard to find a better business model and more beautiful chart.

While the golden goose is feeding you eggs, you eat as many eggs as you can and ride this trade until Google management finally runs into REAL problems and I am not talking about petty anti-trust fines by European regulators.

Simply put, even the best companies run into vanity problems that are storms in teacups. Artificially creating problems sure has to be a first world problem and until there is true evidence that Google’s ad tech is being dismantled, I don’t believe investors have anything to worry about with the ad dollars coming in.

Big tech is on the verge of breaking out after being range-bound, and it would be daft to overthink this move and not participate in the melt-up.

Short-term, I would be inclined to buy on any big or little dip in GOOGL, take profits, and wait for the next dip to get back into the same position.

“Cinema reflects culture and there is no harm in adapting technology, but not at the cost of losing your originality.” – Said Hong Kong-born Actor Jackie Chan

Global Market Comments

June 23, 2021

Fiat Lux

Featured Trade:

(WHY YOU MISSED THE TECHNOLOGY BOOM AND WHAT TO DO ABOUT IT NOW),

(AAPL), (AMZN), (MSFT), (NVDA), (TSLA), (WFC), (FB)

I often review the portfolios of new concierge subscribers looking for fundamental flaws in their investment approach and it is not unusual for me to find some real disasters.

The Armageddon scenario was quite popular a decade ago. You know, the philosophy that said that the Dow ($INDU) was plunging to 3,000, the US government would default on its debt (TLT), and gold (GLD) was rocketing to $50,000 an ounce?

Those who stuck with the deeply flawed analysis that led to those flawed conclusions saw their retirement funds turn to ashes.

Traditional value investors also fell into a trap. By focusing only on stocks with bargain basement earnings multiples, low price to book values, and high visible cash flows, they shut themselves out of technology stocks, far and away the fastest-growing sector of the economy.

If they are lucky, they picked up shares in Apple a few years ago when the earnings multiple was still down at ten. But even the Giant of Cupertino hasn’t been that cheap for years.

And here is the problem. Tech stocks defy analysis because traditional valuation measures don’t apply to them.

Let’s start with the easiest metric of all, that of sales. How do you measure the value of sales when a company gives away most of its services for free?

Take Google (GOOG) for example. I bet you all use it. How many of you have actually paid money to Google to use their search function? I would venture none.

What would you pay Google for search if you had to? What is it worth to you to have an instant global search function? Probably at least $100 a year. I would pay $10,000 as I use it all day long. With 92.05% of the global search market comprising 2 billion users, that means $200 billion a year of potential Google revenues are invisible.

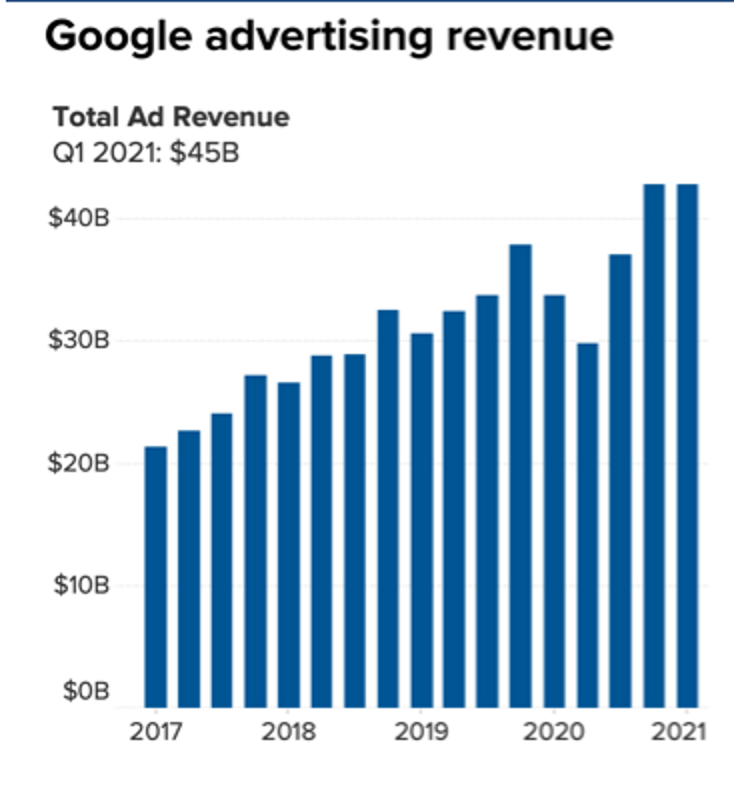

Yes, the company makes a chunk of this back by charging advertisers access to these search users, generating some $55.31 Billion in revenues and $17.93 billion in net income in the most recent quarter.

But much of the increased value of this company is passed on to shareholders not through rising profits or dividend payments but through an ever-rising share price. If you’re looking for dividends, Google doesn’t exist. It is also very convenient that unrealized capital gains are tax-free until the shares are sold, which may be never.

I’ll tell you another valuation measure that investors have completely missed, that of community. The most successful companies don’t have just customers who buy stuff, they have a community of members who actively participate in a common vision, which is then monetized. There are countless communities out there now making fortunes, you just have to know how to spot them.

Facebook (FB) has created the largest community of people who are willing to share personal information. This permits the creation of affinity groups centered around specific interests, from your local kids’ school activities to municipality emergency alerts, to your preferred political party.

This creates a gigantic network effect that increases the value of Facebook. Each person who joins (FB) makes it worth more, raising the value of the shares, even though they haven’t paid it a penny. Again, it’s advertisers who are footing your tab.

Tesla (TSLA) has one million customers willing to lend it $400 billion for free in the form of deposits on future car purchases because they also share in the vision of a carbon-free economy. When you add together the costs of initial purchase, fuel, and maintenance savings, a new Tesla Model 3 is now cheaper than a conventional gasoline-powered car over its entire life.

REI, a privately held company, actively cultivates buyers of outdoor equipment, teaches them how to use it, then organizes trips. It will then pursue you to the ends of the earth with seasonal discount sales. Whole Foods (WFC), now owned by Amazon (AMZN), does the same in the healthy eating field.

If you spend a lot of your free time in these two stores, as I do, The United States is composed entirely of healthy, athletic, good-looking, and long-lived, intelligent people.

There is another company you know well that has grown mightily thanks to the community effect. That would be the Diary of a Mad Hedge Fund Trader, one of the fastest-growing online financial services firms of the past decade. What is the value of our community? To give you a hint, the price of my Global Trading Dispatch has soared from $29 a month to $3,000 a year.

We have succeeded not because we are good at selling newsletters, but because we have built a global community of like-minded investors with a common shared vision around the world, that of making money through astute trading and investment.

We produce daily research services covering global financial markets, like Global Trading Dispatch, the Mad Hedge Technology Letter, and the Mad Hedge Biotech & Healthcare Letter. We teach you how to monetize this information with our books like Stocks to Buy for the Coming Roaring Twenties and the Mad Hedge Options Training Course.

We then urge you to action with our Trade Alerts. If you want more hands-on support, you can upgrade to the Concierge Service. You can also meet me in person to discuss your personal portfolios and my Global Strategy Luncheons.

The luncheons are great because long-term Mad Hedge veterans trade notes on how best to use the service and inform me on where to make improvements. It’s a blast.

The letter is self-correcting. When we make a mistake, readers let us know in 60 seconds and we can shoot out a correction immediately. The services evolve on a daily basis.

It all comes together to enable customers to make up to 20% to 100% a year on their retirement funds. And guess what? The more money they make, the more products and services they buy from me. This is why I have so many followers who have been with me for a decade or more. And some of my best ideas come from my own subscribers.

So, if you missed technology now what should you do about it? Recognize what the new game is and get involved. Microsoft (MSFT) with the fastest-growing cloud business offers good value here. Amazon looks like it will eventually hit my $5,000 target. You want to be buying graphics card and AI company NVIDIA (NVDA) on every 10% dip. It’s going to $1,000.

You can buy the breakouts now to get involved or patiently wait until the 10% selloff that usually follows blowout quarterly earnings.

My guess is that tech stocks still have to double in value before their market capitalization of 26% matches their 50% share of US profits. And the technologies are ever hyper-accelerating. That leaves a lot of upside even for the new entrants.

Mad Hedge Biotech & Healthcare Letter

June 22, 2021

Fiat Lux

FEATURED TRADE:

(PRIMED FOR DOMINANCE)

(TDOC), (AMZN), (AMWL), (WMT), (CVS), (ARKK), (TSLA)

While growth stocks have already begun clawing their way back following the losses they suffered earlier this year, there are still former market favorites struggling to bounce back.

One of them is Teladoc Health (TDOC).

To date, Teladoc is still trading at roughly 40% below its previous highs.

While this can be frustrating for its investors, the current situation might just be an opportune time to add this stock to your portfolio.

Teladoc emerged as the leader in virtual care in 2020 by being at the right place at the right time when the pandemic struck. That year, the company’s revenue rose by a whopping 145% compared to its 2019 performance.

These days though, the stock has lost half of its value. Although that’s definitely a head-scratcher, Teladoc’s 51.5 million paid memberships in the United States alone still make it the most dominant force in this industry.

For a long-term investor, the situation presents a compelling opportunity.

Teladoc is a growing business that’s expanding both in the US and globally. While penetrating more markets would happen over time, the basic footprint has been established. This offers Teladoc much-needed exposure to a massive addressable market.

The global market for telemedicine is estimated to expand from $49.9 billion in 2019 to a jaw-dropping $459.8 billion by 2030.

In North America, which holds roughly 34.4% of the market share in 2020, the telemedicine market generated $19.23 billion during the pandemic.

Taking into consideration Teladoc’s revenue of $967.4 million for its US segments in 2020, it becomes clear that the company is only getting started, as this comprised only 5% of the market size.

If the company maintains its momentum, then the next 10 years would be an incredible journey for Teladoc investors.

Despite the disappointing share price performance of Teladoc in the past months, the company’s actual business has sustained its growth.

Revenue continues to rapidly rise, showing off a 151% growth in the first quarter of 2021.

This impressive growth has prompted Teladoc to boost its full-year revenue guidance to $2 billion, which indicates an 80% year-over-year gain.

Impressive growth has been observed all around, with access fee revenue going up 183% while visit fees climbed 24%.

Considering the size of the market, it no longer comes as a surprise that Teladoc is facing competitive threats.

Amazon (AMZN) and Amwell (AMWL) have recently entered the virtual care market. Even Walmart (WMT) and CVS (CVS) have been working on toppling Teladoc as well.

Despite the competition, Teladoc remains ahead of the pact thanks to its continuous efforts to innovate.

For example, the latest innovation from Teladoc is Primary360.

This product is designed to take virtual healthcare to the next level. It offers personalized service at the patient level. Here’s a preview of how it works.

Traditionally, patients go to their doctors when they discover a health problem. This is a reactive way of dealing with health. In contrast, Primary360 is proactive.

That is, the product monitors the patients individually from annual checkups to ongoing treatments to manage chronic conditions. Through closely monitoring the patients, Teladoc is able to perform earlier diagnoses of potential diseases and help doctors reach better outcomes for treatments.

To better picture the long-term rewards of this company, it’s good to keep in mind that Teladoc is actually the second biggest holding of Cathie Wood’s ARK Innovation ETF (ARKK), next only to Tesla (TSLA).

Teladoc Health emerged as one of the most popular pandemic plays in 2020.

While the stock tumbled when vaccines hit the market, its projected growth trajectory remains promising. In fact, Teladoc’s revenue growth is anticipated to skyrocket over the remainder of this decade, with telemedicine estimated to reach roughly half a trillion dollars by 2030.

For investors on the lookout for long-term plays, Teladoc Health's tumble has presented a good opportunity to add it to your portfolio.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

June 22, 2021

Fiat Lux

Featured Trade:

(THE LAZY MAN’S GUIDE TO TRADING)

(ROM), (UXI), (BIB), (UYG)

(TESTIMONIAL)