Mad Hedge Technology Letter

July 2, 2021

Fiat Lux

Featured Trade:

(WHAT’S UP WITH MICRON?)

Mad Hedge Technology Letter

July 2, 2021

Fiat Lux

Featured Trade:

(WHAT’S UP WITH MICRON?)

Semiconductor chips have been a contentious issue since a dearth of supply has crippled tech companies around the world.

Memory and storage have become increasingly critical across diverse end-market applications, spanning from the data center to the edge and from business to consumer.

Within this context, Micron (MU) is strengthening not only financially, but also competitively.

Micron is transforming into a product leadership company that will help with upcoming node transitions, strengthening product portfolio, and deeper customer engagements that will further enhance its competitive position.

Ironically, Micron's transformation is taking place against a global backdrop of unprecedented geopolitical and economical challenges.

In the near term, enterprise servers have been weak, and that’s impacting the demand outlook.

In the first half of 2020, strong cloud demand trends were building up through the year.

The inventories, by and large, accelerated in cloud for a while and accelerated in enterprise as well until covid hit, as financial and other sectors invested in enterprise server side, but the pandemic changed everything from March 2020.

This caused enterprise to be generally weak since then, but the Cloud demand, given the work-from-home and e-commerce and streaming, all these kinds of applications have driven strong growth on the cloud side, and the strength isn’t going away anytime soon.

The middle chunk of the calendar-year 2020 saw a surge in demand in cloud.

Naturally, in the second half, Micron expects the cloud side to moderate as workers go back to the office signaling a pickup in the enterprise side of the business.

And don’t forget, in 2020, because of the pandemic, total smartphone unit sales were down by 10% year-over-year basis.

But in 2021, smartphone sales are expected to pick up as consumers feel the need to improve their phones and economies bounce back in North America.

In fact, smartphone sales are already picking up in the marketplace right now.

Not only is it a story of increasing smartphone sales as we go through calendar 2021 beyond the seasonally slower first quarter of the calendar, but it is also the story in 5G of higher content, both for memory and storage.

These are the demand drivers that are offering an optimistic outlook for DRAM demand in calendar-year 2021, continuing to improve, starting from the beginning of the year, particularly as we get past the seasonal calendar Q1 time frame.

I would expect a backdrop of demand expectation of 20% growth in DRAM.

Desktop PC sales have been weak due to pandemic-driven changes to customer buying patterns, but DRAM and NAND content growth continue to be a secular trend in the automotive market, supported by advanced infotainment systems and increased automation in cars. The pandemic has significantly impacted both auto production and demand in fiscal 2020, but there was a strong recovery toward the end of fiscal Q4, and expect sequential growth in sales of Micron products in the automotive market in Q1.

Huawei has been a large customer at approximately 10% of fiscal Q4 sales and Micron received notification to cut off sales given a month by the US government to do so. This is a highly negative event resulting in a loss of sales.

Micron estimates that 2020 industry DRAM bit demand growth is likely to be in the “mid-teens percent range”, while NAND bit demand growth is likely to be in the “mid-20s”.

Q4 revenue was approximately $6.1 billion, up 11% sequentially and 24% year over year which I would deem healthy.

DRAM revenue increased 22% sequentially and 29% year over year.

Micron is also holding higher levels of raw material during this period because of supply uncertainty and expects inventory levels to normalize over the course of 2021.

To sum it up, Micron’s management has started to see recovery in the mobile, auto, and consumer markets, but the pace of recovery has been moderated by the continued impact of the pandemic, and shortages of certain non-memory components in some end markets.

Enterprise demand is still weak, and customers may be carrying higher inventory.

Micron continues to execute well despite continued market uncertainty and geopolitical challenges.

The stock sold off on disappointing news that Huawei’s lost business was 10% of sales, weak enterprise activity, and negative PC sales momentum.

There has been a great deal of news regarding the shortage of chips, little do many know, non-chip components are also needed to build Micron’s chip products.

Even though their cloud business was up big during the pandemic, enterprise business was down big because office workers were sent home and management felt there was no reason to progress with the enterprise upgrade cycle.

The lack of smartphone sales affected sales for Micron’s chips as many people held off on their own smartphone upgrade cycle and maintained the phone they already had.

It was a mixed bag for sure, which is why Micron sold off on the earnings’ report and the stock will need time to digest shares after a pandemic-induced boost in expectations that led the stock higher from $42 to $92.

Expectations and performance got too far ahead of itself in the short-term and analyzing this earnings’ performance, it’s cut and dry that there are also many drawbacks to a NAND and DRAM chip business in the pandemic.

Some parts do well, and some do worse and that expectation wasn’t baked into the pricing.

Expect Micron to retrace further as the market has told us they will need to fix parts of their business such as the enterprise side, phone business, and PC desktop business for the stock to reaccelerate past $92.

“I know that you must be passionate, unreasonable, and a little bit crazy to follow your own ideas and do things differently.” – Said CEO and Founder of Salesforce Marc Benioff

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

July 2, 2021

Fiat Lux

SPECIAL EARLY RETIREMENT ISSUE

Featured Trade:

(HOW TO JOIN THE EARLY RETIREMENT STAMPEDE)

Mad Hedge Biotech & Healthcare Letter

July 1, 2021

Fiat Lux

FEATURED TRADE:

(NOT YOUR AVERAGE ONE-HIT WONDER)

(BNTX), (MRNA), (PFE), (REGN), (DNA)

It was only a few months ago when investors believed that COVID-19 developers like Moderna (MRNA) and BioNTech (BNTX) had enjoyed their best performances.

With the uncertainty returning, many figured that the profits and revenues for these stocks have dried up as well.

This isn’t the case these days, though. If anything, it looks like these companies have incredibly bright futures ahead.

BioNTech, in particular, shows tremendous promise after emerging as one of the most compelling success stories in the scientific world during the pandemic.

Working alongside Pfizer (PFE), this German biotechnology company created the first-ever vaccine that utilized messenger RNA to receive authorization across the globe.

Since being a first mover in the COVID-19 vaccine race, BioNTech has established a strong financial position that gave it the capacity to pursue other breakthrough treatments in its pipeline.

Moreover, the general sentiment toward BioNTech remains positive thanks to the effectiveness of its vaccine.

Just last month, the US Centers for Disease Control and Prevention disclosed the latest data on the efficacy of mRNA-based vaccines. It showed an impressive 91% reduction rate in terms of infections based on real-life reports.

The sustained demand for COVID-19 vaccines also translated to an outpouring of orders, with BioNTech recently completing another agreement with New Zealand and even the Philippines.

Health officials are also looking into the need for booster shots, which means it’s entirely possible that a whole new revenue stream could open up for BioNTech once again.

In the first quarter of 2021, revenues from BioNTech’s share from the COVID-19 vaccine marketed alongside Pfizer amounted to over $3.5 billion, including milestone payments.

This puts it on track to reach the $8.3 billion revenues estimated from the vaccine alone in 2021.

Apart from its agreement with Pfizer, this German biotech has been ramping up its own production. So far, it anticipates selling roughly 250 million doses of the COVID-19 vaccine in the first half of 2021.

Let’s say that each dose is sold at $14, and BioNTech could sustain its manufacturing capacity until December, then it can supply a total of 500 million doses.

That would rake in $7 billion in direct revenue.

On top of these, BioNTech has a separate deal with China’s Fosun Pharma.

This means that the earlier estimate of $15 billion in revenue for BioNTech this year is definitely feasible.

However, that’s a conservative estimate.

BioNTech intends to expand its manufacturing capacity to produce 3 billion doses by the end of 2021 and more by 2022.

By next year, the entire world comprising 7 billion people would be eligible to take the vaccine shots as approvals get rolled out.

Even with the competition, BioNTech stands to cover at least 30% market share or roughly 2 billion doses in the years to come.

Despite the expected price reduction to probably $10 per dose, that’s still a whopping $20 billion in annual sales for a biotechnology company with a current market capitalization of $54.10 billion.

Going back to its current deals with bigger biopharmaceutical companies, BioNTech had an impressive first quarter this year, showing off a 7,295% surge in its sales.

Leveraging this massive revenue stream, the company has boosted its pipeline programs and is pushing to ride the momentum.

So far, it has 14 drug candidates queued in clinical trials.

One of the most promising and advanced is its melanoma treatment pipeline, which has two programs slated to advance to Phase 2 within the year.

The first one, BNT111, is a collaboration with Regeneron (REGN), while the other, BNT122, is an approach developed alongside Genentech (DNA).

Aside from these programs, the company has also been busy working on developing mRNA-based treatments for various types of cancers.

If you’re one of the people who thought that the rise of the COVID-19 vaccine stocks is done the moment the entire US population gets vaccinated, then you’re not alone in that assumption.

You’d be surprised though at the strength of the staying power of companies like BioNTech have, especially when some things work out in their favor.

For context, BioNTech is only second to Volkswagen (VWAGY) in terms of profitability in Germany.

That means that a 13-year-old biotech company with fewer than 2,000 employees has grown so much in the past year that it’s now in the same conversation with a company employing over 600,000 people and has a history that predates World War II.

While COVID-19 upended the world, BioNTech has been granted the opportunity to show off its skills and grow its business

From being a virtually unknown company, it has become one of the fastest-growing biotech globally.

Looking at its performance in the past 12 months and its pipeline programs, it’s clear that BioNTech still has so much room for growth.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

July 1, 2021

Fiat Lux

Featured Trade:

(A VERY BRIGHT SPOT IN REAL ESTATE)

I feel obliged to reveal one corner of this bubbling market that might actually make sense.

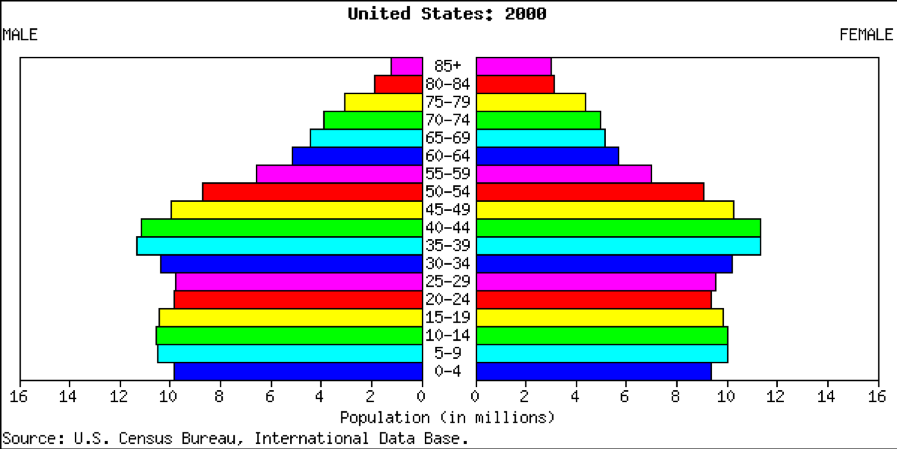

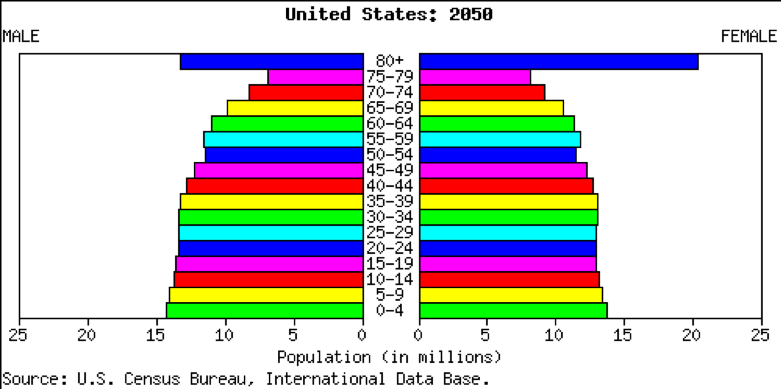

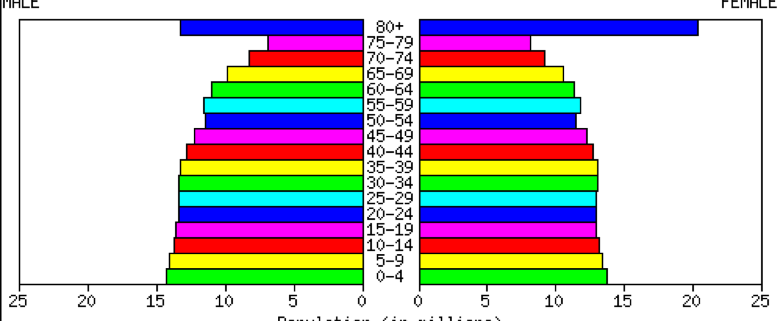

By 2050, the population of California will soar from 39 million to 50 million, and that of the US from 330 million to 400 million, according to data released by the US Census Bureau and the CIA Fact Book (check out the two population pyramids below).

That means enormous demand for the low end of the housing market, apartments in multi-family dwellings.

Many of our new citizens will be cash-short immigrants. They will be joined by generational demand for limited rental housing by 65 million Gen Xers and 85 million Millennials enduring a lower standard of living than their parents and grandparents.

These people aren't going to be living in cardboard boxes under freeway overpasses.

If you have any millennial kids of your own (I have three!), you may have noticed that they are far less acquisitive and materialistic than earlier generations.

They would rather save their money for a new iPhone than a mortgage payment. Car ownership is plunging, as the “sharing” economy takes over.

This explains why the number of first-time homebuyers, only 32% of the current market now, is near the lowest on record.

It’s not like they could buy if they wanted to.

Remember that this generation is almost the most indebted in history, with $1.6 trillion in student loans outstanding.

They don’t care. Coming of age since the financial crisis, to them, homeownership means falling prices, default, and bankruptcy. Bring on the “renter” generation!

The trend towards apartments also fits neatly with the downsizing needs of 85 million retiring Baby Boomers.

As they age, boomers are moving from an average home size of 2,500 sq. ft. down to 1,000 sq ft condos and eventually 100 sq. ft. rooms in assisted living facilities.

The cumulative shrinkage in demand for housing amounts to about 4 billion sq. ft. a year, the equivalent of a city the size of San Francisco.

In the aftermath of the economic collapse, rents are now rising dramatically, and vacancies rates are shrinking, boosting cash flows for apartment building owners.

Fannie Mae and Freddie Mac Financing is still abundantly available at the lowest interest rates on record. Institutions combing the landscape for low volatility cash flows and limited risk are starting to pour money in.

Run the numbers on the multi-dwelling investment opportunities in your town. You’ll find that the net after-tax yields beat almost anything available in the financial markets.