Global Market Comments

September 21, 2022

Fiat Lux

Featured Trade:

(EXPLORING THE WORLD OF EXTREME LEAPS),

(TSLA)

Global Market Comments

September 21, 2022

Fiat Lux

Featured Trade:

(EXPLORING THE WORLD OF EXTREME LEAPS),

(TSLA)

Mad Hedge Biotech and Healthcare Letter

September 20, 2022

Fiat Lux

Featured Trade:

(A MONSTER BIOTECH ON ITS WAY TO ANOTHER BLOCKBUSTER)

(BMY), (AMGN), (VTYX)

This year's bear market has pushed a lot of businesses to their breaking points. The S&P 500, the benchmark of stock performance in the US, has fallen by 14.6% in 2022.

What’s making things look gloomier is that the tech-focused Nasdaq Composite Index, aka the bellwether growth stock index, has plummeted by 22% thus far. Even the Dow Jones Industrial Average, another leading indicator, has dipped by 11.5%. All these firmly place the entire market in the bear market territory.

In response to the headwinds, investors have spotlighted businesses with steady free cash flow, solid leadership teams, and virtually recession-proof sectors.

This is where Bristol Myers Squibb (BMY) shines as an excellent example of Wall Street’s reinvigorated desire to pour money on long-forgotten movers in the market.

As one of the leading biotechnology companies worldwide, BMY has once again piqued the interest of investors primarily for its ability to defy the bear market. In fact, the company’s stock is up 12% year to date, clearly outperforming the S&P 500 by roughly 29 percentage points.

BMY’s ascent has taken years, with the business benefitting massively from its $74 billion acquisition of another biotech stalwart, Celgene.

This deal granted BMY access to an extensive oncology and autoimmune diseases portfolio, with back-to-back blockbusters like Revlimid and Reblozyl sales practically paying for Celgene’s acquisition price.

Now, BMY has made another move that brought seismic rearrangement within the biopharma sector, particularly in the highly lucrative psoriasis treatments space.

Earlier this month, BMY disclosed that it received FDA approval for its oral plaque psoriasis treatment deucravacitinib. The company plans to market this new drug under the name Sotyktu.

More impressively, Sotyktu was not given any “black-boxed warning” on its label, which typically indicates that a treatment carries significant safety risks.

Unlike most therapies for psoriasis, which use Janus kinase inhibitors, BMY is the first to use and gain approval for a TYK2 inhibitor. Generally, treatments utilizing Janus kinase inhibitors come with “black-boxed warnings.”

The absence of which, in BMY’s candidate, indicates a cleaner label.

This is terrible news for Amgen’s (AMGN) Otezla, which is currently the leader in the psoriasis space. Since this drug uses Janus kinase inhibitors, it has become a “less safe” option for patients. More than that, Sotyktu managed to outperform Otezla in a head-to-head trial.

Aside from that, a “black-boxed warning” would have offered Amgen some defense in protecting Otezla’s market share.

Meanwhile, Sotyktu’s approval brings good news to smaller biotechnology companies, such as Ventyx Biosciences (VTYX), working on similar treatments that use TYK2 inhibitors.

Regarding costs, BMY’s list price for its psoriasis therapy is notably higher than Amgen’s. According to sources, Sotyktu will be given a price tag of roughly $75,000. In comparison, Otezla is priced at approximately $52,000 annually.

Needless to say, Sotyktu is projected to become another blockbuster in BMY’s arsenal. Simply basing the possibilities on Otezla’s recent sales reports would give us a good picture of this new drug’s future.

In 2021, Otezla raked in $2.2 billion in sales for Amgen. Despite the competition, Otezla is still projected to grow and reach $3.2 billion in annual sales by 2026.

Considering that BMY’s Sotyktu will be playing catch up in terms of marketing and distribution, this psoriasis drug is anticipated to reach $2 billion in yearly sales in 2026.

However, this was estimated before the FDA’s surprise approval. The consensus is that the absence of a “black-boxed warning” would significantly boost the projections.

Overall, BMY has always been quite the oddball among its peers. While the SPDR S&P Biotech ETF rose by a staggering 42% in 2021, the company was barely in positive territory.

Due to the impending patent cliffs at that time, BMY was considered a laggard in the biopharma world. Added to those concerns was the company’s move to buy Celgene for a jaw-dropping $74 billion, substantially increasing its debt-to-equity-ratio. Taken together, these threats made BMY an unfavorable investment from 2020 to late 2021.

By 2022, however, BMY will have transformed into a favorite on Wall Street. Investors have regarded it as a safe harbor amid the ongoing bear market.

Moreover, BMY shares have marched even higher thus far by an impressive 12.5%. Meanwhile, the SPDR S&P Biotech ETF has recorded a 21.4% loss this year.

While the rest of the market has been struggling to keep things afloat, BMY’s stock isn’t that far from hitting its 52-week high to date. Hence, it would be an excellent move to buy the dip.

Mad Hedge Bitcoin Letter

September 20, 2022

Fiat Lux

Featured Trade:

(THE SAVIOR)

(BTC), (FTX), (SKYBRIDGE)

Enigmatic crypto investor Sam Bankman-Fried, founder of crypto exchange FTX, acquired a 30% stake in Anthony Scaramucci’s SkyBridge Capital, an alternative investment firm.

I believe this deal highlights the desperation the crypto industry currently faces.

I also don’t see the value in it.

Bankman-Fried is essentially the only prominent investor liquid enough to bank mediocre crypto infrastructure mostly because he has skin in the game and would potentially get shellacked with monstrous losses if crypto as an industry goes under.

Doing his best to prop up the mess is in his interests, otherwise, his brainchild FTX would suffer too.

As harrowing as this sounds, I don’t think crypto as an industry will go under, but the wounds get rawer by the day.

The deal was inked through SBF's venture-capital firm FTX Ventures and will support growth initiatives for SkyBridge.

SkyBridge will deploy the capital from FTX to buy $40 million in cryptocurrencies, which it will hold on its balance sheet.

SkyBridge investors are demanding redemptions from the fund ever since the price of Bitcoin has tanked causing anyone involved with the crypto industry a world of pain.

Many are anointing Bankman-Fried as the savior of crypto, but I would argue that this shows the inferiority of crypto as an industry.

It’s signaling that no other big names are coming to save crypto. No Marc Andreesen or anyone of that magnitude.

Crypto has shown it’s only viable when liquidity is in the process of loosening, and currently, the opposite is happening.

In fact, it appears as if liquidity will get even tighter heading into year-end.

And if that wasn’t bad enough, the integrity of the crypto industry has been under attack from all directions for quite some time.

Yet another explosive headline came out saying that a founder of a cryptocurrency investment research firm was accused by the SEC of promoting an initial coin offering without disclosing that he had been given incentives to do so.

Ian Balina, 33, promoted the SPRK token on social media platforms including YouTube and Telegram without revealing that he had been compensated by the company that offered it, the Securities and Exchange Commission said in a suit filed Monday in federal court in Austin, Texas.

It’s certainly a bad look that crypto is attracting such bad actors and the brand name downgrade just keeps getting clearer.

I believe crypto will weather this crypto winter but for the 10s of thousands of other crypto products, let’s call them collateral damage.

The next question is at what point does Bankman-Fried stop whipping his savior capital around and at what point does the crypto infrastructure get so bad there’s no way back?

Considering Bankman-Fried has wealth of around $24 billion, a $50-$70 million investment in some marginal crypto hedge fund is just a drop in the bucket for him.

SkyBridge doesn’t do that much, it just sells a crypto ETF, takes in fees for it, and markets it as a safer pair of hands to handle crypto for the investor. Investors can just go and buy crypto on Bankman-Fried’s FTX for a more direct way to invest in the same thing.

I do believe it’s worth it for Bankman-Fried to save these small companies now, to later unload them for a profit when Bitcoin recovers. He can afford the carry costs as he can pay in cash and avoid the high interest debt markets.

However, I do believe he will abstain from billion dollar purchases.

Even with him, there’s a limit.

As for the crypto infrastructure, just save one coin and that’s Bitcoin and the rest can go to hell. If this scenario takes place, crypto will survive and strengthen after the crypto winter ends.

Until then, it’s about survival for just about everyone in the crypto industry until the next crypto bull market initiates.

“I don’t want to fight old battles. I want to find new ones.” – Said Current CEO of Microsoft Satya Nadella

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

September 20, 2022

Fiat Lux

Featured Trade:

(EXPLORING THE WORLD OF EXTREME LEAPS),

(TSLA)

I sent out a trade alert last week to my concierge members to buy Tesla LEAPS. What came back surprised me. I wasn’t taking on enough risk, there wasn’t enough leverage. In short, I wasn’t being extreme enough.

So, I thought “OK, I can do leverage. You want leverage? Here is an extreme LEAPS.

I sent them back the following trade alert:

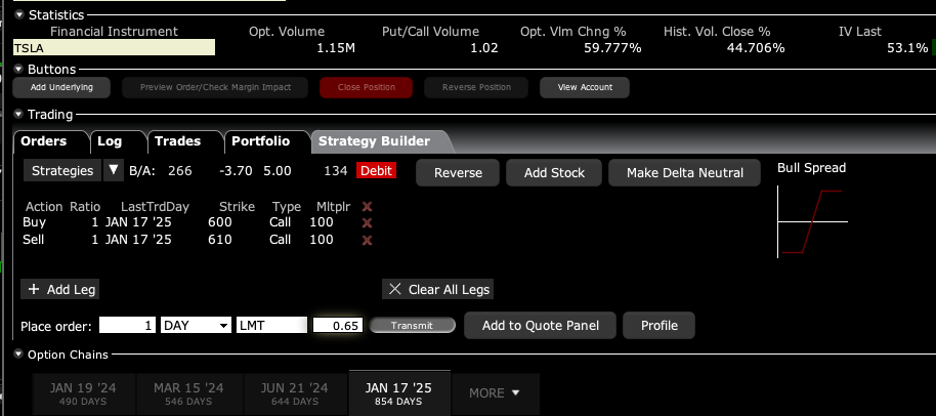

Trade Alert - (TSLA) – BUY

BUY the Tesla (TSLA) January 2025 $600-$610 out-of-the-money vertical Bull Call spread LEAPS at $2.00 or best

Opening Trade

9-16-2022

expiration date: January 17, 2025

Number of Contracts = 1 contract

If you are looking for a lottery ticket, then here is a lottery ticket.

While the chance of winning a real lottery is something like a million to one, this one is more like 2:1 in your favor. And the payoff is 14:1. That is the probability that Tesla shares will double over the next two years and four months.

You may not have noticed, but we have just entered the golden age of the electric vehicle, thanks to climate change and massive government support.

Tesla is the world’s largest electric vehicle manufacturer and will produce over 1.4 million cars this year. Demand is overwhelming supply, with the waiting list for the Model X stretching out over a year. The company is growing at 40% a year and plans to boost annual production to 20 million units by 2030.

Tesla is a far and away the most profitable automaker in the world with 30% profit margins, compared to only 10% for its competitors. Lithium-ion batteries are about to see a 20-fold improvement in cost per mile as the company moves towards solid-state technology. The effects on profits should be the same.

To learn more about the company (and to order a car), please visit their website at https://www.tesla.com

I am therefore buying the Tesla (TSLA) January 2025 $600-$610 very deep out-of-the-money vertical Bull Call spread LEAPS at $0.65 or best

Don’t pay more than $1.00 or you’ll be chasing on a risk/reward basis.

January 2025 is the longest expiration currently listed. If you want to get more aggressive with more leverage, use a pair of strike prices higher up. This will give you a larger number of contracts at a lower price.

Please note that these options are illiquid, and it may take some work to get in or out. Start at my price and work your way up until you get done.

Look at the math below and you will see that a 101% rise in (TSLA) shares will generate a 1,438% profit with this position, such is the wonder of LEAPS. That gives you an implied leverage of 14.4:1 across the $600-$610 space.

Only use a limit order. DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES. Just enter a limit order and work it.

You don’t need to buy your entire position on day one. The day-to-day volatility of LEAPS is miniscule as the time value at two years plus is so great, so you have the luxury of picking up a new position over days, if not weeks.

I tend to buy just one or two a day every day until I have a full position. That way, I won’t get THE bottom, but I will get close to the bottom.

This is a bet that Tesla will not fall below $610 by the January 17, 2025 options expiration in 2 years and 4 months.

Here are the specific trades you need to execute this position:

Buy 1 January 2025 (TSLA) $600 calls at………….………$50.00

Sell short 1 January 2025 (TSLA) $610 calls at………..…$49.35

Net Cost:………………………….………..…………............….....$0.65

Potential Profit: $10.00 - $0.65 = $9.35

(1 X 100 X $9.35) = $935 or 14.35% in 2 years and 4 months.

If you are uncertain about how to execute an options spread, please watch my training video by clicking here.

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep-in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Keep in mind that these are ballpark prices at best. After the alerts go out, prices can be all over the map.

![]()

A New Theory of Tesla, or Why I’m Raising My Target to $1,000

I’ve been battling shorts in Tesla for a decade….and you won.

Look at the price of Tesla shares today and I have to laugh. From the $2.35 I paid for the shares after its IPO bombed in 2010, the price is up more than 100 times. Back then, even Elon Musk gave the company only a 10% chance of surviving.

My first Tesla, chassis no 125, was scrapped for parts a long time ago, thanks to a drunk driver in a GM Silverado on Christmas Eve. A lot of people talk about Tesla, but few have completely taken them apart, as I have…. twice.

Yes, it’s still true that if you buy the stock, you get the car for free, possibly a fleet of them.

I set my target at $1,000 a decade ago. My assumption was that the company would take over a large part of the global car market, about 90 million vehicles a year, and 15 million in the US alone. Tesla’s own plans have it manufacturing about 20 million units a year by 2030.

Add in an eye-popping $15,000 upgrade for fully autonomous street-to-street driving, and Tesla should be making tons of money by then.

That looks on track to happen and is already reflected in the current share price. But what if there is more to Tesla? A lot more?

In fact, after making the rounds in Silicon Valley, it’s clear that Tesla is just getting started. Tesla will become the largest publicly listed company in the world, surpassing Apple, and account for an important share of US GDP.

It might even become the world’s first $10 trillion company.

Yes, it will even grow larger than Saudi Aramco, which manages the kingdom’s oil riches. The irony is rich.

Let’s say that it reaches its ambitious 2030 goal of 20 million units. Then what?

For a start, when Tesla goes solid-state, battery efficiencies will increase 20-fold, costs will drop by 95%, and vehicle ranges will double. This could happen in as soon as two years. They already have the solid-state batteries. All they need now is to understand economical mass production.

The company has already said it is dropping the price of its cars to $25,000 in three years, but much more is possible.

Converting the car bodies from aluminum to carbon fiber, which the wheel wells are made of now, will further cut costs, increase ranges, and improve safety. Carbon fiber is five times stronger than steel at one-tenth the weight.

To reach that goal, the total Tesla fleet will have grown from 1.5 million units today to 100 million by 2030 and account for one-third of all the cars on the road. Those cars are going to need one heck of a lot of electricity to run.

Step in Tesla.

The company already has 20,000 superchargers in the US and that figure is doubling every year. No place in the country today is more than 100 miles away from a supercharger.

A Tesla Model 3 with a 100W battery pack driving 20,000 miles a year costs $720 to power at current prices. The entire fleet would cost $54 billion a year to run at a national average price of 12 cents/kWh.

Ring the cash register for Tesla….again.

Let’s say that rather than paying for electricity at an external charger at some distant shopping mall, you’d rather get the power at home for free.

Enter Tesla.

Finally, after a decade of waiting, Solar City, a Tesla subsidiary, is manufacturing cost-competitive solar roof tiles, or photovoltaic tiles. I have several readers already installing them at this moment. With a 15-year head start in silicon and battery technology, there is no reason why Tesla shouldn’t dominate in this industry as it already has with cars.

To keep the calculations simple, if 75 million homeowners buy solar roofs at an average of $36,000 each, the gross sales would reach $2.7 trillion. Kaching! To get a quote for your new solar roof, please click here.

To get the most out of your solar roof, you really need to buy a couple of 13.5W Tesla Powerwall storage batteries which would cost $25,000 installed. That way, the solar tiles will charge the batteries during the day, which will then power your house at night. You will become grid independent forever, as I have been for years.

Where do Powerwalls come from? Not the stork. They are recycled batteries from old Tesla cars. You can recycle silicon. You can’t recycle CO2.

That will protect you from soaring electric power costs driven by coming cascading bankruptcies of public utilities around the country, all caused by global warming. You also have your own power supply for the ten days a year the grid is down from wildfires on the west coast, or hurricanes on the east coast.

When the neighborhood lights go out, I charge my neighbors a bottle of wine for a cell phone charge. It’s not a bad racket, but I’m getting more than I can drink. In fact, I am producing enough excess electricity to power my entire neighborhood, about 20 houses.

Under the current law, the federal government will pay for 30% of your cost with alternative energy tax credits.

Naturally, you are going to want highspeed WIFI so all of the elements of your integrated solar solution can talk to each other and upgrade whenever they want. So, you’re going to need a Tesla Starlink satellite connection. The system now in beta testing will eventually deliver a 500 megabyte a second WIFI connection anywhere in the world. Starlink is already running the Internet in Ukraine….for free.

The global WIFI market is expected to grow to $7.2 trillion by 2025 (click here for the link). Give half of that to Tesla and you get another $3.6 trillion in sales. Oh, and if you want to sign up as a beta tester for Starlink, please click here.

Did I mention that Musk also owns a rocket company, Space X, which can launch satellites into space at one-tenth the cost of all competitors? Elon’s goal is to cut costs 100-fold. Musk has already taken over a lot of launch business from Europe which used to go to Russia.

Looking at Elon’s big picture as an engineer and scientist, I am amazed to find so many 10X and 100X improvements going on all at the same time!

Add all this together and you might get a market capitalization for Tesla of $10 trillion. Elon Musk would become worth $2 trillion. Then he really can afford that trip to Mars.

This prompts me to raise my target for Tesla shares to $1,000.

That’s not a particularly bold prediction. It’s only 3.6X the current share price, compared to the 117X gain seen since the IPO.

Hey, I got the last 117X right, what’s another 3.6X?

Nobody ever accused me of thinking small.

And if Tesla really does become a $10 trillion company, you’d be right to raise antitrust concerns. But as anyone who has done the math on breaking up these big companies can tell you, such a move would double their value. Tesla at $2,000 a share, anyone?

And as incredible as it may seem, Elon Musk outlined all of his grand global vision to me personally in great detail when I first met him in 1999 pitching me for an investment in X.com, which later became PayPal (PYPL).

Then the bright-eyed, fresh-faced overconfident kid was only 27 and worth a mere $10 million. But he had a nice car, a million-dollar 618 hp McLaren F-1 with a V-12 engine.

A pittance really.

I passed, which is why I am still working today.

No kidding.

Tesla’s Solid State Batter Design

What its Modeled After

Chassis No. 125….R.I.P.

My Latest Set of Wheels

Like-Minded Found in Chicago

At the Pebble Beach Car Show

Going All-Electric

13.5 kWh Powerwall, Enough Juice to Run My House for a Day

This Lot of 300 Cars in Fremont Gets Filled and Emptied Out Three Times a Day

Back in 2010, the First Tesla They Had Ever Seen

“In the next recession, the US will be the worst-performing stock market in the world. We won’t see new highs again in my lifetime,” said Doubleline Capital’s Jeffrey Gundlach.