(THE U.S. IS FACING AN INCREASING STAGFLATION THREAT)

April 28, 2023

Hello everyone,

Stagflation could be knocking on your door for quite a lengthy visit soon. Thursday’s gross domestic product reading for the first quarter showed lackluster economic growth and high inflation.

First quarter growth came in at a 1.1% annualized pace, much slower than the 2% growth expected by economists polled by Dow Jones. Data inside the report showed the personal consumption expenditures price index, an inflation measure that the Federal Reserve closely follows, increased by 4.2%, higher than estimates.

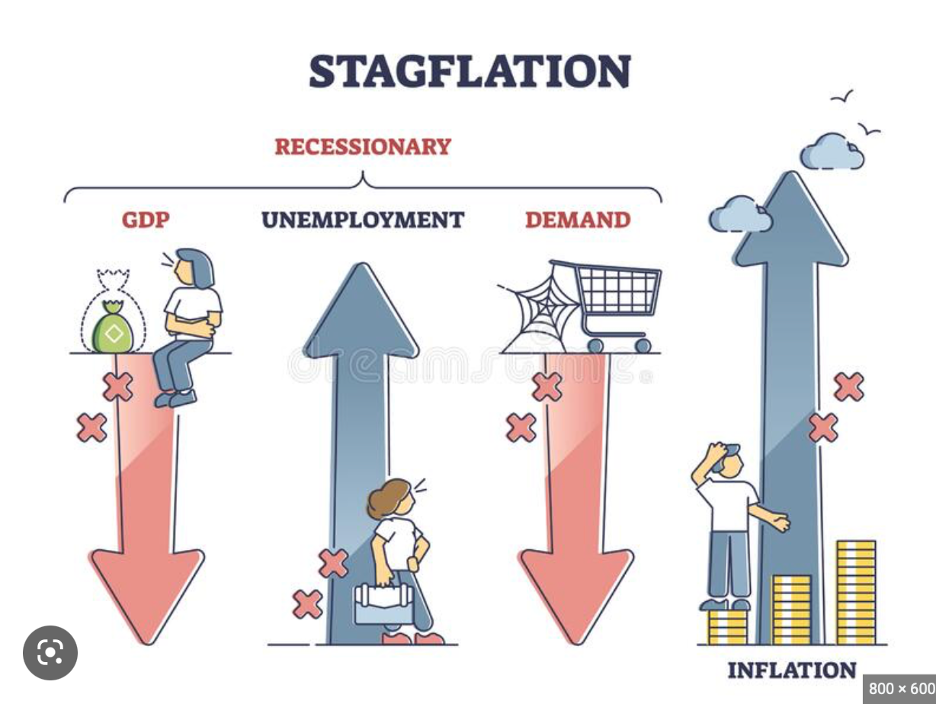

So, you might be scratching your head, wondering what Stagflation is.

Let me enlighten you.

Stagflation is an economic condition the U.S. experienced in the 1070s, characterized by slow economic growth and elevated inflation, along with high unemployment. The one ingredient missing today is the high unemployment, but mounting layoffs are raising fears that will change soon too. Cases in point, Lyft has just announced it will lay off 26% of its workforce and Dropbox also has announced it will lay off 16% of its workforce.

With most economists expecting the economic picture to darken further in the second half, what can you do as an investor?

It’s reasonable to assume that certain stocks with pricing power and resilient revenue sources could outperform in this kind of environment.

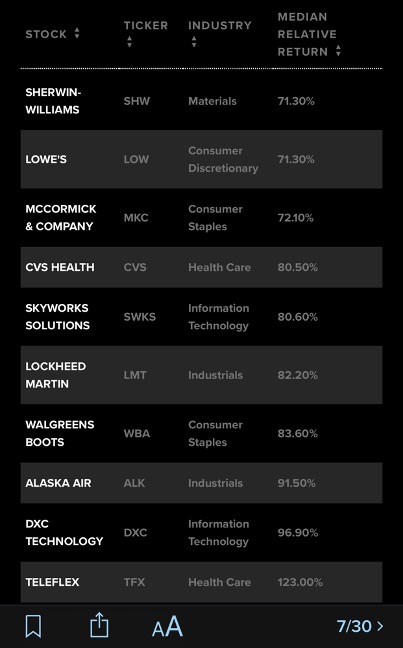

Bank of America ran a screen earlier this year to find stagflation beneficiaries. The firm looked for S&P 500 companies with the best relative performance during periods of “below-trend growth with above-trend but decelerating inflation, an environment that we will likely be in this year.”

Here are the top 10 stocks from that screen of the past 50 years.

STAGFLATION SCREEN

On that cheery note, I will wish you all a wonderful weekend.

Cheers,

Jacque

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 22:00:492023-05-17 10:35:24April 28, 2023

The one sound bite that really jumped out at me on Amazon’s earnings calls that sums up the zeitgeist right now in the tech sector is when CEO Andy Jassy said “customers are looking for ways to save money however they can right now.”

Savings money is foreign to growth tech, but investors should get used to the new Silicon Valley.

When the success of a tech firm is utterly reliant on mass volume of sales, this isn’t the type of trend that will drive earnings higher in the future.

I am not blaming Amazon for customers pinching pennies.

It has more to do with the generally macro malaise that US consumers are facing with the explosive price rises of the last few years.

There is no point to rehash about inflation, but the net effect is that there is less opportunity for these ecommerce companies to flog products.

The US consumer is even more reliant on debt to finance purchases than before and smart companies like Apple (APPL) have rolled out savings accounts because they are aware that the fight for deposits is up for grabs after the banking contagion.

Even though AMZN delivered us a great quarter in terms of profitability and top line growth, the larger takeaway was the uncertain path going forward.

Amazon CFO Brian Olsavsky told investors on the company's earnings call AWS customers are continuing "optimizations" in their spending.

The CFO described the first quarter as “tough economic conditions.

Revenue in Amazon's AWS unit grew 16% during the first quarter, down from an annual growth rate of 37% seen in the same quarter last year.

Disclosure that sales growth at AWS had slowed further in April sets the stage for AWS’s weakest growth rate since Amazon began breaking out the unit’s sales.

Amazon’s advertising business continues to deliver robust growth, largely due to ongoing machine learning investments that help customers see relevant information when they engage.

US customers are moderating spending on discretionary categories as well as shifts to lower-priced items and healthy demand in everyday essentials, such as consumables and beauty.

A little bit of a mixed bag, but disappointing guidance in AWS really sticks out like a sore thumb.

As we exit the bulk of big tech earnings, it is clear there is quite a bit of runway left for big tech shares to go higher.

I can’t say the same for every tech stock, because growth stocks have a different set of challenges that they haven’t been able to overcome.

Amazon still posted great earnings and investors should absolutely look to buy shares on the dip.

Even at less than 100%, AMZN is still worth owning over a lot of SPACs, growth tech, or emerging tech.

What we are seeing now are these behemoth tech companies leveraging their balance sheet in an interest rate matters world which is why small companies can’t compete anymore.

Although not technically monopolies, some of these tech firms are getting darn close with their closed “ecosystems.”

Buy AMZN on the next dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 14:02:142023-05-02 00:49:49Buy Amazon on the Dip

“Most Americans agree that technology is going to eliminate many more jobs than it is going to create.” – Said American entrepreneur and former presidential candidate Andrew Yang

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/andrew-yang.png346384Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 14:00:102023-05-01 05:17:18Quote of the Day - April 28, 2023

Below please find subscribers’ Q&A for the April 26 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Las Vegas, NV.

Q: Would you start adding to The Russell 2000 (IWM) around here?

A: No, the Russell 2000 is the most sensitive to market action and the most sensitive to an economic downturn, which it seems we have already entered. And you don’t add positions one week into the downturn, you do it like 3-6 months into the downturn. So, I would not touch (IWM) right around here.

Q: Are you buying more First Republic Bank (FRC) down here?

A: No, at this point the stock is a no-go. It is a ripe takeover target for someone, and the risk is, the takeover price is lower than your cost. I don’t understand why First Republic is down this far—like 97% — and when I don't understand things, I stay away. I had never seen a bank go under before that didn’t have bad loans, nor has anyone else. A lot of people were asking if they should double up, we went from $16 to $6 in a day, and the firm answer is that I just don’t know. The fundamentals of the company by no means justify that discount, it must be discounting something terrible that we haven’t heard yet. So I’m going to stay away and look for better trades to do.

Q: I missed the Tesla (TSLA) trade on Friday, should I be looking to buy the dips down here?

A: Yes, I would. I put out a May $110-$120 vertical bull call debit spread on Tesla, which is now only 3 weeks to expiration. Remember, at Tesla’s growth rate, the company is now 12% larger than it was when it hit the $104 bottom in January. I should point out that once our trade alert went out, it literally triggered billions of dollars worth of market action and crushed volatility. It took the implied volatility on Tesla options down 10% on that one day. So, with implied volatility this low, I’m not sure you can get Tesla done at any price that makes sense—but if you can, I’m all for it. As for the short, we’re almost in max profit on our Tesla short position. It’s cratered about $35 since we put it on, so I wouldn’t be chasing that one.

Q: Is there a reason why Freeport McMoRan (FCX) is not progressing upwards?

A: Recession fears—the long-term case for copper is spectacular— I’m looking for $100 in (FCX) a couple years down the road. With the short term, all they see is recession and US government debt default, and as long as those two things are overhanging the market, all of the economically sensitive plays are going to go down. You’re not going to get gains, you’re going to get losses. If you want to know how the debt default is working out, you can write a letter to Kevin McCarthy in Washington DC and ask him what he’s going to do. The stock market doesn’t like it for sure, so I’m inclined to go back to 100% cash and duck that whole cluster.

Q: Can China survive without foreign investment?

A: Yes, with a much lower standard of living, and technology that is greatly lagging behind the US. The Chinese use all the foreign investment going on to upgrade their own technology—it's very common for a Chinese worker to work for an American company for a year and then walk across the street and work for their main Chinese competitor. That is a major means of technology transfer. Without that, they fall way behind, and they know it. You can’t copy your way to leadership, as Japan found out to their great expense in the 1990s. You can add that to the long list of reasons why China will never invade Taiwan. Not only have they cut off their food and energy supply, but also their technology supply.

Q: Would it be safe to deposit my money with Apple (APPL) who’s offering a 4.15% interest rate?

A: Yes, Apple has about $150 billion in cash on the balance sheet to back up any deposit runs. I imagine Apple financially is probably far safer than any small regional bank in the US. But, there are better things to do than Apple, and that’s the good old 90-day US T-bill. That bill never defaults; it’s offering 5.2% — it may even be a little bit higher after May 3 when the Federal Reserve raises interest rates by 25 basis points.

Q: Aren’t earnings coming in better than expected?

A: Yes they are, however, the earnings season was frontloaded with the best-performing sector in the market—i.e. the banks—which you were 100% long of until last week, and the weaker performers are next. That seems to be what the stock market is telling us with the selloff, and of course, the weaker performers are technology stocks. So that's why I piled on the shorts (especially in the Invesco QQQ Trust), that’s why I cut back position sizes, it’s time to take the money and run.

Q: How much longer do you plan to do this?

A: Well Warren Buffet is 92 and he seems to be doing just fine. Joe Biden plans to be President of the United States until he is 86. Work for these men is their lives and they will never quit. The same is true for me. If they can do that, I can certainly run Mad Hedge Fund Trader until I am 92, or for 21 more years. Besides, what else would I do? I’m terrible at golf, I hate pickleball, Bingo is boring and is usually rigged, and all the other stuff that people my age do doesn’t appeal in the least.

Q: Are there ETFs that mirror the rates of 90-day T-bills, or is it better just to buy direct through my broker?

A: It’s always better to buy T-bills directly because your ETF does not work for free. They’re taking out fees somewhere, even if you can’t see them, even if they’re not in the marketing material—nobody works for free; except the US government, it would seem. So buy directly from the US government. If you own the T-bills and your institution goes bankrupt, you can always get your T-bills back in a couple of days. If you own their ETF that mirrors the T-bill, that can become a complete loss and you’ll get tied up in bankruptcy proceedings that last three years (and you may or may not get your money back.) So T-bills directly are the gold standard, I would buy those if you’re looking for a cash alternative.

Q: What about Rivian (RIVN)?

A: It’s red meat in this kind of market—don’t touch it. If the entire car industry is rolling over, including Tesla, don’t expect Rivian to outperform in that situation. As for Amazon (AMZN), like all tech stocks, I’m going to wait for the current selloff to work its way for its system, but then it’s probably a great long term buy and a two-year LEAPS.

Q: What’s your estimate for S&P earnings?

A: I’m at $220 a share which today gives us a multiple of 18.73, which is the middle of the recent range. We may drop a point or two from there, but that’s close enough for the cigar.

Q: Won’t wider credit spreads hurt iShares iBoxx $ High Yield Corporate Bond ETF (HYG)?

A: Yes, for the short term, but you’re being compensated for that by the 8% yield; and you’re buying junk bonds not for where they are for the next month or two, but where they are for the end of the year, which would be at least 10$-15% higher than they are now, so your total “all in” return might be as much as 25%. Not bad.

Q: What’s your thought on the Salesforce (CRM) drop?

A: I’ll buy it in about 3 months, once the next tech washout is finished and they’re throwing these things out with the bathwater.

Q: Do you think iShares 20 Plus Year Treasury Bond ETF (TLT) will trade higher if the market collapses?

A: Yes it will; that is your classic flight to safety out of stocks into bonds. We haven’t seen it in quite a while because both of them have been moving up and down together.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Playing the Penny Slots in Las Vegas is Definitely NOT my Retirement

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/john-thomas-penny-slots.jpg212260Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 13:02:442023-04-28 14:27:44April 26 Biweekly Strategy Webinar Q&A

“I try not to let the urgent take over the day,” said Tim Cook, the CEO of Apple.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/tim-cook.jpg300450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 13:00:122023-04-28 14:25:23Quote of the Day - April 28, 2023

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 11:51:262023-04-28 11:51:26Trade Alert - (ZM) April 28, 2023 - BUY

Here’s a question to test your biotechnology and healthcare knowledge: Can you think of a company that doubled its earnings during the pandemic yet currently trades at a lower valuation than it did at the beginning of 2020?

The answer might surprise you. It’s Thermo Fisher Scientific (TMO).

Despite benefiting from Covid-related demand, Thermo Fisher's stock price has not kept pace with its strong sales growth. Perhaps you weren't aware of Thermo Fisher and its role in supplying researchers with essential tools for developing life-saving drugs and tests. Regardless, it's a company worth paying attention to now.

Based in Waltham, Massachusetts, this healthcare supplier is one of the world's most prominent analytical instrument, reagent, consumables, software, and service providers, catering to industries like biotechnology, clinical diagnostics, pharmaceuticals, environmental monitoring, and food safety.

With a market capitalization of over $210 billion, the company benefited greatly from Covid-19 testing, resulting in earnings per share skyrocketing from $12.35 in 2019 to over $25 in 2021.

Thermo Fisher's earnings have declined as the pandemic subsides, leading to a corresponding dip in stock price. However, this downturn looks to be temporary. Moreover, the company is still poised for growth.

Looking at the turn of events, it’s clear that investors tend to be overly fixated on the company's performance during the pandemic, which represented only a tiny part of its overall business. This should no longer be the case, especially since Thermo Fisher has already provided strong guidance, which is more critical than short-term fluctuations.

Thermo Fisher Scientific's full-year guidance was offered in February following the announcement of impressive fourth-quarter results. The healthcare supplier expects to earn $23.70 per share in 2023, alongside revenue of $45.3 billion, exceeding the average analyst projections of $23.07 per share in earnings and $43.8 billion in revenue. Nevertheless, the predicted per-share profit is lower than the previous year's $25.13.

Due to the two-year decline in earnings since the pandemic boom, the company's shares have fallen by 14% since the end of 2021. As expected, this has led to investors being spooked by the problematic comparisons to the pandemic period. Consequently, the stock is currently trading at 24 times forward earnings, which is about its five-year average and below its pandemic high of 26.6 in December of 2021.

By 2024, however, Thermo Fisher is expected to surpass its all-time high earnings, with estimated earnings per share of $26.70. This figure is expected to continue to increase, with a projection of more than $30 per share in 2025.

Given these metrics, it’s evident that Thermo Fisher is a stock worth holding onto for the long term. More importantly, its current valuation makes it an attractive option for new investors.

Despite being categorized as a growth stock, Thermo Fisher benefits from consistent, recurring revenue from customers engaged in complex research and development. This makes the shares appealing in light of recent market volatility.

Thermo Fisher is a beacon of hope in the healthcare industry, where creating drugs is complex and requires advanced tools and technologies.

For example, newer products, such as biologics and larger molecule drugs, which are produced differently and require specialized equipment, provide Thermo Fisher with excellent opportunities to shine. The company is positioned to benefit from this trend as it provides researchers and developers the necessary tools and equipment.

Notably, Thermo Fisher is agnostic to specific drugs or the success of individual companies in the industry. Hence, regardless of the focus of healthcare companies, the company remains a staple in their laboratories.

In the company's latest earnings report, the confidence that comes with supplying a range of growing healthcare end markets was evident, thanks to an aging population and increasing treatment options. Additionally, the company raised its dividend by almost 17%, and its guidance suggests 7% core organic revenue growth, excluding acquisitions.

Discussing Thermo Fisher's acquisition strategy is almost inevitable when examining the company. Through this strategy, Thermo Fisher has broadened its revenue streams, customers, geographical reach, and business segments.

For context, ten years ago, the company was more instrument-focused. If a recession had occurred during that period, it would have had a much more significant impact on the company. Today, the business is less cyclical and less vulnerable to severe downturns.

Thermo Fisher executed its acquisition strategy without raising its debt ratios too high. At the end of 2022, the company's net debt to Ebitda ratio was 2.2 times, its second lowest level since 2013. Its total debt to Ebitda ratio of 2.9 times is also below the pre-pandemic period dating back to 2013.

Furthermore, Thermo Fisher's free cash flow is expected to increase to $7.2 billion this year, nearly twice the amount in 2018. This allows the company to pursue additional acquisitions and return more cash to shareholders in the form of dividends and share repurchases, as it has been doing in recent years.

Overall, Thermo Fisher holds a winning formula. It has good returns and a management team that makes the right decisions with its cash. On top of these, the company has more than ample room for long-term growth.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-27 18:00:342023-05-02 00:43:41The Underappreciated Giant

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.