In a world where the longing for personalized cancer treatments echoes the craving of superheroes for justice, Thermo Fisher Scientific (PFE) and Pfizer (PFE) have forged an alliance to expand the global reach of next-generation sequencing technologies.

Their ambitious mission? To bring a ray of hope to patients by advancing a more accurate technology that can be used against cancer.

Cancer treatment is evolving at lightning speed, shaking up the status quo and dazzling experts worldwide. In the past, most treatment options revolved around traditional approaches like radiation. But now, a new kid on the block is changing the landscape: genomics.

Genomics might sound like a fancy scientific term, but it's a captivating branch of molecular biology that holds the key to unlocking the secrets deep within our genes. By studying our genetic profile, we can diagnose cancer more precisely than ever.

One breakthrough advancement that's causing quite a stir is genomic sequencing.

This technique allows doctors to analyze an individual's genetic sequence and pinpoint their unique genetic makeup. With this information, they can devise treatments finely tuned to each person's needs.

In fact, studies have shown that genomic sequencing can help match cancer patients to the most effective treatments based on their unique genetic makeup, significantly improving survival rates and treatment outcomes.

A recent study even showcased that patients who underwent genomic-guided therapy experienced an astonishing 35% higher overall response rate than those receiving conventional treatments.

Imagine a world where there are no more blanket treatments, only personalized care that targets the source of individual cancers.

In terms of the target market, the projected size of the global genomics market is a staggering $29.1 billion by 2025, and the profound impact on cancer, as the primary target for genomic analysis, is nothing short of colossal.

Here is the next question: Is this technology truly available, accessible, and sustainable in the long run? The resounding answer is yes.

The rise of next-generation sequencing as the gold standard in selecting cancer treatments has put the spotlight on access and affordability. Sequencing technology, once the sluggish tortoise in the race, has transformed into a lightning-fast hare.

Remember the mythical "$1,000 genome?" Well, it's no longer a myth.

Thanks to the groundbreaking unveiling of the $100 genome by Ultima Genomics in 2022, the cost of whole-genome sequencing has plummeted to a fraction of its former self. As costs continue to nosedive and swiftness skyrockets, the stage is unequivocally set for a genomic revolution, with cancer patients emerging as the ultimate beneficiaries of this scientific triumph.

Consequently, the biotechnology and healthcare market stands on the precipice of a seismic shift as Thermo Fisher and Pfizer join forces to democratize genomic sequencing.

With an initial focus on lung and breast cancer patients across more than 30 countries in Latin America, Africa, the Middle East, and Asia, this duo aims to shatter the barriers that have limited access to cutting-edge testing resources.

That is, more lives are about to be touched by the power of precision medicine.

This collaboration also unveils a compelling investment opportunity. As the demand for next-generation sequencing technologies skyrockets, Thermo Fisher Scientific, the vanguard of sequencing equipment and reagents, stands poised to ride this wave of progress.

Envision sales figures soaring as they equip local laboratories, guaranteeing the possession of indispensable technology, robust infrastructure, and expertly trained personnel to orchestrate these genomic symphonies.

Meanwhile, Pfizer, not content with just making blockbuster drugs, seeks to make DNA tests more affordable for patients and enlighten healthcare providers about the tremendous benefits of genomic screening.

As the costs of sequencing continue to decrease, even enabling the elusive $1,000 genome to become a reality, the accessibility and adoption of genomic sequencing are poised to expand, paving the way for personalized cancer therapies and transforming the landscape of oncology. Can you hear the sound of stock prices ascending?

So hold onto your lab coats and stethoscopes; Thermo Fisher and Pfizer's collaboration is about to reshape the landscape of cancer treatment.

As investors, consider the potential windfall of increased demand for sequencing technologies and expansion into emerging markets.

As humanity, marvel at the possibilities that arise when genomic superheroes unite. The era of personalized medicine is dawning, and these two trailblazers may just be your ticket to ride the genomic wave of the future.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-11 16:00:262023-05-31 18:31:54Unleashing Genomic Superpowers

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-11 12:42:242023-05-11 12:46:19Trade Alert - (ZM) May 11, 2023 - TAKE PROFITS - SELL

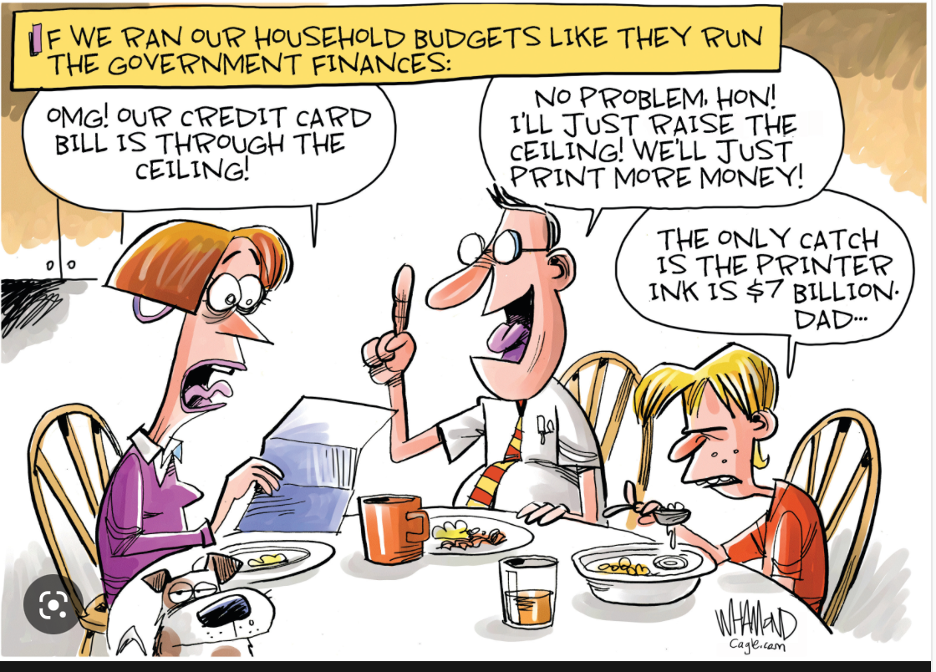

The debt ceiling is on everyone’s mind now and is a constant topic of discussion in the financial media. So, I thought I would provide everyone with a Q & A on the issue - which I researched from several articles - to enlighten you. Enjoy.

What is the debt ceiling?

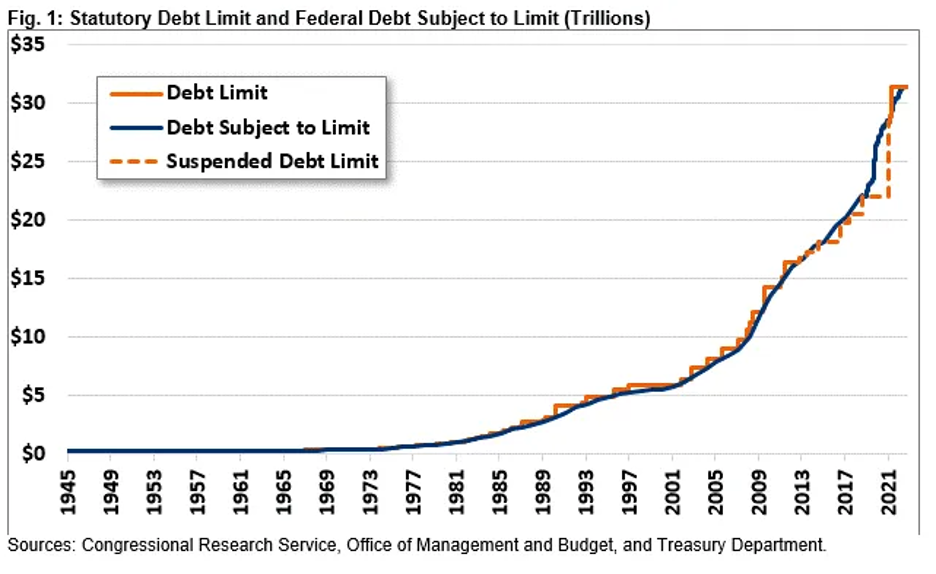

It is the total amount of money that the United States government is authorised to borrow to fulfill its financial obligations. The limit applies to almost all federal debt, including the rightly $24.6 trillion of debt held by the public and the roughly $6.8 trillion the government owes itself because of borrowing from various government accounts, like Social Security and Medicare, and trust funds. As a result, the debt continues to rise due to both annual budget deficits financed by borrowing from the public and from trust fund surpluses, which are invested in Treasury bills with the promise to be repaid later with interest.

When was the debt ceiling established?

The debt ceiling was first enacted in 1917 through the Second Liberty Bond Act and was set at $11.5 billion. In 1939, Congress created the first aggregate debt limit covering nearly all government debt and set it at $45 billion, about 10% above total debt at the time.

How much has the debt ceiling grown?

Since the end of World War II, Congress and the President have modified the debt ceiling more than 100 times, according to the Congressional Research Service. During the 1980s, the debt ceiling was increased from less than $1 trillion to nearly $3 trillion. Over the course of the 1990s, it was doubled to nearly $6 trillion and in the 2000s it was gain doubled to over $12 trillion. The Budget Control Act of 2011 automatically raised the debt ceiling by $900 billion and gave the President authority to increase the limit by an additional $1.2 trillion (for a total of $2.1 trillion) to $16.39 trillion. Lawmakers have suspended the debt limit, rather than raising it by a specific dollar amount, seven times since the beginning of 2013. The debt limit was increased – not suspended – twice in 2021, mostly recently in a December 2021 bill that formally increased the limit to $31.381 trillion.

What are extraordinary measures?

When the debt limit is reached, the Treasury Department both relies on cash on hand and uses a variety of accounting maneuvers, known as extraordinary measures, to avoid defaulting on the government’s obligations. For example, the Treasury has prematurely redeemed Treasury bonds held in federal employee retirement savings accounts (and replaced them later with interest), halted contributions to certain government pension funds, suspended state and local government series securities, and borrowed from one set aside to manage exchange rate fluctuations. The Treasury Department first used these measures in 1985, and there have been nine distinct “debt issuance suspension periods” since enactment of the Budget Control Act in 2011, including the current one.

Can hitting the debt ceiling be avoided without Congressional action?

The Treasury Department’s use of extraordinary measures simply delays when the debt will reach the statutory limit. Spending more than incoming receipts has already been legally obligated; that spending will push debt beyond the ceiling. There is no plausible set of changes that could generate the instant surplus necessary to avoid having to raise or suspend the debt ceiling indefinitely.

Some believe the Treasury Department could buy more time by engaging in other unprecedented actions such as selling large amounts of gold, minting a special large-denomination coin, issuing IOUs that could be sold and traded in private markets, or invoking the Fourteenth Amendment to override the statutory debt limit. Whether any of these tools is truly available is in question, and the potential economic and political consequences of each of these options are unknown. Realistically, once extraordinary measures are exhausted, the only option to avoid defaulting on our nation’s obligations is for Congress to change the law to raise or suspend the debt ceiling.

What happens if the debt ceiling is hit?

Once the government hits the debt ceiling and exhausts all available extraordinary measures, it is no longer allowed to issue debt and soon after will run out of cash-on-hand. At that point, given annual deficits, incoming receipts would be insufficient to pay millions of daily obligations as they come due. Therefore, the federal government would have to default on many of its obligations at least temporarily, from Social Security payments and salaries for federal civilian employees and the military to veterans’ benefits and utility bills, among others.

So-called “prioritization” of payments, or making sure certain obligations among the more than 80 million that get paid per month are paid before others – such as servicing debts to bondholders before making other payments in order to avoid technical default – has been criticized as unrealistic by Treasury officials and economists. A Treasury Inspector General report from 2012 outlined scenarios that were considered during the 2011 debt ceiling run-up and found that delay of payments, which suspended all government payments until they could all be paid on a day-to-day basis, was the least harmful scenario.

How bad are the consequences of default?

A default, or even the perceived threat of one, could have serious negative economic implications. An actual default would roil global financial markets and create chaos, since both domestic and international markets depend on the relative economic and political stability of U.S. debt instruments and the U.S. economy. Interest rates would rise, and demand for Treasuries would drop as investors stop or scale back investments in Treasury securities if they are no longer considered perfectly safe. Even the threat of default during a standoff increases borrowing costs. The Government Accountability Office (GAO) estimatedthat the 2011 debt ceiling standoff raised borrowing costs by a total of $1.3 billion in Fiscal Year (FY) 2011, and the 2013 debt limit impasse led to additional costs over a one-year period of between $38 million and more than $70 million.

If interest rates for Treasuries increase substantially, interest rates across the economy would follow, affecting car loans, credit cards, home mortgages, business investments, and other costs of borrowing and investment. The balance sheets of banks and other institutions with large holdings of Treasuries would decline as the value of Treasuries dropped, potentially tightening the availability of credit as seen most recently in the Great Recession.

A Moody’s Analytics report released in early 2023 estimated that a default could have similar macroeconomic consequences to the Great Recession: a 4 percent Gross Domestic Product (GDP) decline, nearly 6 million lost jobs, and an unemployment rate of more than 7 percent. In addition, Moody’s predicted a $12 trillion loss in household wealth, with stocks dropping by as much as one-third at the depths of the selloff.

The White House Council of Economic Advisers (CEA) has warned that the macroeconomic effects stemming from default – or even getting too close to one – can last months or even years. A CEA report found that following the debt limit run-up in 2011, mortgage rates rose 0.7 to 0.8 percentage points for two months following the crisis and rates for auto and other consumer loans also remained elevated for months. In the event of an actual default, increased unemployment rates could persist for two to four years, the report warned.

In addition, default could also ultimately add significantly to the national debt in the form of increased borrowing costs.

How does a shutdown differ from a default?

A shutdown occurs when Congress fails to pass appropriations bills that allow agencies to obligate new spending. As a result, the government temporarily stops paying employees and contractors who perform government services (see Q&A: Everything You Should Know About Government Shutdowns). However, many more parties are not paid in a default. A default occurs when the Treasury does not have enough cash available to pay for obligations that have already been made. In the debt ceiling context, a default would be precipitated by the government exceeding the statutory debt limit and being unable to pay all its obligations to its citizens and creditors. Without enough money to pay its bills, any of the payments are at risk, including all government spending, mandatory payments, interest on our debt, and payments to U.S. bondholders. While a government shutdown would be disruptive, a government default could be disastrous.

Have policymakers used the debt ceiling to pursue deficit reduction in the past?

Although policymakers have often enacted “clean” debt ceiling increases, Congress has also coupled increases with other legislative priorities. In several cases, Congress has attached debt ceiling increases to budget reconciliation legislation and other deficit reduction policies or processes.

Indeed, most of the major deficit reduction agreements made since 1980 have been accompanied by a debt ceiling increase, although causality has moved in both directions. On some occasions, the debt limit has been used successfully to help prompt deficit reduction, and in other cases, Congress has tacked on debt ceiling increases to deficit reduction efforts. For example, the 2011 Budget Control Act was enacted along with a debt ceiling increase, as was the Gramm-Rudman-Hollings Balanced Budget and Emergency Deficit Control Act of 1985.

In nearly all instances in which a debt limit increase was either accompanied by deficit reduction measures or included in a deficit reduction package, lawmakers have generally approved temporary increases in the debt limit to allow time for negotiations to be completed without the risk of default. For example, Congress approved a modest increase in the debt limit in December of 2009 while negotiations over statutory pay-as-you-go (PAYGO) and the establishment of the National Commission on Fiscal Responsibility and Reform were ongoing. Similarly, during the negotiations and consideration of the 1990 budget agreement, Congress approved six temporary increases in the debt limit before approving a long-term increase as part of the reconciliation bill implementing the deficit reduction agreement.

The Appendix contains further discussion of provisions attached to debt ceiling legislation, including bills in 1993, 1997, 2013, 2015, 2018, and 2019.

What should policymakers do?

Policymakers should work promptly to raise or suspend the debt ceiling by the deadline. Failing to raise the debt ceiling would be disastrous. It would result in severe negative consequences that experts are not capable of fully predicting in advance. Even threatening a default or taking the country to the brink of default could have serious implications. Importantly, though, failing to control the national debt would also have negative consequences; rising debt could ultimately stunt economic growth, reduce fiscal flexibility, and increase the cost burden on future generations. Thus, lawmakers should consider accompanying a debt ceiling increase with measures to begin addressing the debt.

To be sure, political advantage should not be sought by threatening default, and the debt ceiling must be raised or suspended. Lawmakers must not jeopardize the full faith and credit of the U.S. government. At the same time, the need to raise the debt ceiling can serve as a useful moment for taking stock of our fiscal state and for pursuing revenue increases, entitlement reform, and/or spending reductions.

What are the options for improving the debt ceiling?

Increasing the debt ceiling requires frequent and often contentious legislative action. While several increases have been used to enact fiscal reforms, many increases are not necessarily tied to fiscal health. For instance, debates regarding the debt ceiling often take place after the policies producing the debt have already been put in place. The debt ceiling also measures gross debt, which means that even if the budget was balanced, the debt ceiling would still have to be raised if surpluses accumulated in government trust funds like Social Security.

In The Better Budget Process Initiative: Improving the Debt Limit and subsequent publications, we have suggested reforms to the debt ceiling, grouped in four major categories:

• Linking changes in the debt limit to achieving responsible fiscal targets, so that Congress would not need to increase the debt ceiling if fiscal targets are met.

• Having debate about the debt limit when Congress is making decisions on spending and revenue levels, not after those decisions have been made.

• Applying the debt limit to more economically meaningful measures, such as debt held by the public or debt as a share of GDP.

• Replacing the debt limit with limits on future obligations.

Wishing you all a great week.

Cheers,

Jacque

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-10 22:00:302023-06-21 16:03:55May 10, 2023

I remembered the moniker data was the new oil and there is a salient argument that still holds true, especially with software companies.

However, the CEO of Tesla Elon Musk has something to say about that when he described lithium batteries as the new oil.

Musk said that as he was hyping up a new lithium-ion factory Tesla intends to construct in Corpus Christi, Texas.

The EV leader plans on a $375 million facility so it can produce more domestic battery-grade lithium than the rest of North America is currently capable of.

Given lithium is a key component of the batteries that power Tesla’s cars, and EVs are set to gain widespread adoption over the coming years, Tesla is obviously an outsized winner here.

Here are two other companies that could participate in the lithium gains as well:

Microvast Holdings (MVST)

The company’s advanced battery solutions are designed to power a wide range of electric vehicles, from small passenger cars to heavy-duty trucks and buses.

The stock is up around 50% today after yesterday’s earnings.

The companies delivered better-than-expected results and announced record-breaking backlogs of delivery orders.

Sitting at $2 per share, it’s still cheap to jump in.

Li-Cycle Holdings (LICY)

Next is Canadian company Li-Cycle Holdings, a specialist in advanced lithium-ion battery resource recovery.

Essentially, the firm recycles lithium-ion batteries, reintroducing the materials back into the supply chain, and the proprietary tech is designed to recover up to 95% of the materials used in the battery manufacturing process, including lithium, cobalt, nickel, and other valuable metals.

Li-Cycle has also secured several partnerships with other companies, including Kion, Glencore, and Renewance.

The transportation and energy markets are evolving in unpredictable ways, but most prognosticators agree: no matter what happens, battery recycling will be crucial.

LICY still strikes me as an investable option in this segment; the company has a multi-year head start, as well as a growing list of strategic partners (including KION, a German multinational that manufactures 1.7 million forklifts per year).

Perhaps most importantly, a $375M loan from the Department of Energy helps de-risk Li-Cycle’s balance sheet, so unlike many asset-intensive peers in the battery supply chain, LICY should have no problem funding its expansion.

If readers want to take a broader approach to investing and reach for a basket of lithium-based exposure then one of the most popular ETFs providing exposure to lithium is the Lithium & Battery Tech ETF (LIT).

It invests in the full lithium cycle, from mining and refining the metal, right through to battery production.

There are options for the reader because these small companies are highly speculative and aren’t a sure thing.

Going with LIT is a safer way to ride the lithium trend but by reducing risk by a great deal.

EVs aren’t going away anytime soon, and the heaps of policies introduced to the global economy mean that car manufacturers will be forced to pump out more EVs in the future.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-10 15:02:292023-05-31 22:03:54Front-Run the Lithium Pivot

"The greatest enemy of knowledge is not ignorance, it is the illusion of knowledge," said the late Professor Stephen Hawking.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/hawking-1.png345474Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-10 15:00:252023-05-10 20:08:12Quote of the Day - May 10, 2023

We need to look back to the ancient world to discover the origins of robots. During the industrial revolution, humans developed the structural engineering capability to control electricity so that machines could be powered with small motors.

The idea of the humanoid machine was developed in the early 20th century. The first uses of modern robots were in factories as industrial robots. A car company - General Motors - paved the way here first.

General Motors (GM) introduced the first industrial robot, called "The Unimate," back in 1959. It was just a simple hydraulic arm that did some repetitive welding tasks. Seven years later, "The Unimate" made a friendly appearance on The Tonight Show with Johnny Carson, where it played not such a bad imitation of golf.

As technology has improved and become cheaper, robots have become more prevalent. Robot sales in North America have hit record highs for the last three consecutive quarters. We now encounter robots in our daily lives in various forms: they vacuum floors (Zoomba), mow lawns, make coffee, and even provide companionship (see the movie Her).

Additionally, they help combat supply chain disruptions and inflation. Automation allows employees to focus on higher-value tasks and work efficiently. Robots now work successfully alongside humans.

So, the robotics industry looks like a savvy investment.

Why?

The global robotics market is expected to grow at an impressive CAGR of 23% from 2021 to 2026, eventually hitting a cool $186.7 billion by the end of that span.

The range of robotics applications continues to expand at lightning speed and has become evident in everything from manufacturing to healthcare, logistics to agriculture, and beyond. It's all driven by many factors behind the scenes, like advancements in AI and machine learning, growing demand for automation, and improvements in sensor technologies. More and more companies are tapping into robotics R&D, and the stock market is taking notice.

One company that is particularly well-positioned to benefit from the growth of robotics is Intuitive Surgical (ISRG).

Intuitive Surgical is a pioneer in the field of robotic surgery, with its flagship da Vinci Surgical System being used in over 7 million surgeries worldwide. The company has a market cap of $125.6 billion, and its stock has been surging in recent years, growing by over 800% in the last decade.

Presently, about half of all robotic procedures are used in urological and gynecological procedures, but robotic surgery has applications across the medical field. Currently, only 3% of all surgeries are done robotically, so there is a lot of potential for growth in this area.

Another company that benefits from the growth of robotics is ABB (ABB), a Swiss-Swedish multinational corporation specializing in robotics, power, and automation technology.

ABB has a market cap of $67.2 billion and is a leader in industrial robotics, with applications ranging from welding and painting to packaging and palletizing. The company's robotics division has seen double-digit growth in recent years, and it is well-positioned to capitalize on the continued expansion of the global robotics market.

Of course, the growth of the robotics industry isn't limited to these two companies. Other publicly traded firms that are likely to benefit from this trend include Teradyne (TER), Yaskawa Electric (YASKY), and Fanuc (FANUY), among others.

Logistics is also benefiting from robotics. As online shopping and same-day delivery become more popular, companies need help to keep up and must find ways to streamline their supply chains and reduce costs.

Robotics play a major role in solving these problems. Autonomous robots can zip around warehouses, grab products off shelves, and even help load and unload trucks.

A company that is leading the charge in this area is Amazon (AMZN).

Amazon has been investing heavily in robotics for years, and its acquisition of Kiva Systems in 2012 has been instrumental in the company's ability to scale its logistics operations. The company now has over 200,000 robots deployed in its warehouses, and it is constantly experimenting with new ways to use robotics to increase efficiency and reduce costs.

An additional reason that robots are becoming more in demand involves the transportation industry.

People keep coming up with state-of-the-art ways to make cars and trucks, and these new production technologies require lots of robots. Moreover, factories worldwide are getting upgrades, so they need revolutionary robots to help them improve.

In 2020, BMW AG (BMWYY) and industrial robots and systems manufacturer KUKA (KUKAF) signed a deal to provide more than 5,000 robots to new production lines and factories worldwide. KUKA stated that these industrial robots would be utilized globally at the BMW Group's overseas manufacturing facilities to produce present and future vehicle models.

Industrial robot costs have become much more reasonable over the past thirty years. They have dropped by an average of 50%. This decrease makes adopting robotics technology in various industries a feasible option.

Robots are not replacing factory workers. Instead, they're working alongside their human counterparts to free up their time for more critical tasks. The Institute for Operations Research and the Management Sciences backs the idea that investments in robotics technology equaled firm employment.

Science fiction robotic concepts have arrived in our modern-day environments and investors will now be able to profit handsomely from this industry.

In the wise words of Warren Buffett, "Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble."

While the growth of robotics may lead to job displacement in some sectors, it's important to remember that this is a natural evolution of technology. As new jobs are created in various areas, such as robotics engineering and data analysis, we must adapt and embrace these changes.

In the meantime, savvy investors can capitalize on the continued expansion of the robotics market. Companies such as Intuitive Surgical, ABB, and Amazon are just a few examples of publicly traded firms well-positioned to benefit from this trend.

However, let's remember that the robotics industry is still in its early stages, and there are bound to be new players emerging in the coming years.

As with any investment, it's essential to do your due diligence and invest wisely. But the rewards could be massive for those willing to take the risk. So take Buffett’s advice and put out the bucket, to catch some of that golden rain.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/money.png243432Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-10 09:02:132023-05-10 15:45:08Why the Robotics Industry is Raining Gold

Mad Hedge Biotech and Healthcare Letter May 9, 2023 Fiat Lux

Featured Trade:

(WEIGHT LOSS DRUGS: THE NEXT BIG THING OR JUST HYPE?) (LLY), (NVO), (PFE), (JNJ), (AMGN), (ALT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-09 17:02:182023-05-09 18:17:39May 9, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.