For 127 years, the Dow Jones Industrial Average has been a reliable indicator of Wall Street's health. As of late, with the Dow Jones pulling back from its 2023 high, it hints at some of its components being undervalued. To the discerning investor, this presents a compelling investment opportunity.

One company that stands out in this landscape is the healthcare behemoth, Johnson & Johnson (JNJ). Its P/E ratio, at a decade-low of 15, underscores its investment appeal. This becomes particularly significant given that, historically, this number hasn't dipped this low in the past ten years.

A primary concern for potential investors might be the litigation shadowing J&J regarding its now-discontinued talcum-based baby powder.

The company's stock has faced increased scrutiny, with close to 100,000 lawsuits alleging a link between the product and cancer. While J&J has attempted court settlements, bankruptcy judges have halted these efforts twice. This ongoing legal tussle has indeed infused a certain level of unpredictability into the stock's future trajectory.

However, regarding financial stability, J&J's financials are robust.

The company enjoys the highest credit rating (AAA) from Standard & Poor's, an S&P Global division. This accolade reflects immense trust in J&J’s ability to manage its debt efficiently.

One of the pillars of J&J's consistent performance over the last 35 years has been its gradual shift in revenue focus. The company has been directing an increasing share of its net sales towards pharmaceuticals.

These products not only have higher margins but also promise quicker growth than medical devices. But it's worth noting that as the global populace grows older and healthcare accessibility improves, J&J's medical devices still hold significant revenue potential.

The healthcare sector is witnessing a paradigm shift with the incorporation of artificial intelligence (AI). An area where this amalgamation is showing promise is drug discovery.

Johnson & Johnson subsidiary Janssen discovered that AI could make drug discovery 250 times more efficient. In the world of medical research, where vast data sets need meticulous scrutiny, AI's ability to predict potential high-performing compounds can revolutionize the drug approval process.

Traditionally, getting a drug approved can take years and drain resources, sometimes to the tune of nine figures. An optimized drug development process is not just an operational win but a significant cost-saving.

For J&J, this AI-driven efficiency aligns perfectly with its strategic direction. After the recent spin-off of its consumer health business, the company is doubling down on growth initiatives.

While J&J is grappling with the expiration of exclusivity rights for some of its flagship drugs, it has set ambitious targets. By 2025, the pharmaceutical giant aims to generate over $60 billion in sales, a considerable leap from the $52.6 billion revenue of 2022.

Leadership at J&J has also played a role in its long-standing market success. Since its founding in 1886, the company has seen only eight CEOs. This continuity ensures that long-term growth strategies are not only devised but also effectively executed.

Another critical aspect to consider is the inherent defensive nature of the healthcare sector.

Even during economic downturns or stock market volatility, the demand for medical devices, prescription drugs, and healthcare services remains consistent. Being essential services, their consumption isn't optional. This gives J&J an edge as it ensures a predictable cash flow.

While the market is teeming with dividend stocks, few match the reliability of Johnson & Johnson. The company’s consistent performance over 61 years, despite numerous challenges, including recessions, global pandemics, and drastic shifts in the healthcare landscape, stands as a testament to its resilience.

Johnson & Johnson has a rich history and a vast product portfolio spanning areas like oncology, immunology, and infectious diseases. However, past performance doesn't seal the future. What gives J&J its edge is its continuous innovation and its ability to meet the ever-evolving healthcare demands.

With global demographics skewing older and advancements in medicine increasing life expectancy, the demand for healthcare is only going to grow. Companies like J&J, with their extensive product range, are well-positioned to explore these growth avenues.

So, while J&J has its set of challenges, especially legal ones, they're unlikely to impede its long-term growth trajectory. For investors eyeing a blend of stability and growth in an otherwise unpredictable market, Johnson & Johnson stands out as a prime candidate.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

(LAST CHANCE TO ATTEND THE OCTOBER 31 MIAMI, FLORIDA STRATEGY LUNCHEON)

(THE REAL ESTATE MARKET IN 2030),

(XHB), (ITB), (LEN),

(INDUSTRIES YOU WILL NEVER HEAR FROM ME ABOUT)

A number of analysts, and even some of those in the real estate industry, think that there will never be a recovery in residential real estate. With 8.0% mortgage rates who can blame them.

Long time readers of this letter know too well that I went hugely negative on the sector in late 2005, when I unloaded all of my holdings.

However, I believe that “forever” may be on the extreme side. Personally, I believe there will be great opportunities in real estate that run all the way until 2030.

Let's back up for a second and review where the great bull market of 1950-2007 came from.

That's when a mere 50 million members of the “Greatest Generation”, those born from 1920 to 1945, were chased by 80 million baby boomers born from 1946-1962.

There was a chronic shortage of housing, with the extra 30 million never hesitating to borrow more to pay higher prices.

When my parents got married in 1948, they were only able to land a dingy apartment in a crummy Los Angeles neighborhood because my dad was an ex-Marine sergeant. This is where our suburbs came from.

Since 2005, the tables have turned. There are now 80 million baby boomers attempting to unload dwellings on 65 million generation Xers who earn less than their parents, marking down prices as fast as they can.

As a result, the Federal Reserve thinks that 20% of American homeowners still have either negative equity, or less than 10% equity, which amounts to nearly zero after you take out sales commissions and closing costs.

That comes to 30 million homes. Don't count on selling your house to your kids, especially if they are still living rent-free in the basement.

The good news is that the next bull market in housing has already started.

That's when 85 million Millennials have started competing to buy homes from only 65 million upwardly mobile Gen Xers. Add these two generations together, and you have a staggering 150 million buyers competing for the same housing at the same time!

Fannie Mae and Freddie Mac will soon be gone, meaning that the 30-year conventional mortgage will cease to exist. All future home purchases will be financed with adjustable-rate mortgages, forcing homebuyers to assume interest rate risk, as they already do in most of the developed world.

For you Millennials just graduating from college now, this is a best-case scenario. People will, no doubt, tell you that you are crazy, that renting is the only safe thing to do, and that home ownership is for suckers.

That's what people told me when I bought my first New York coop in 1982 at one-tenth its current market price.

Just remember to sell by 2035 because that's when the next intergenerational residential real estate collapse is expected to ensue. That will leave the next, Generation Z homeowners, holding the bag, as your grandparents are now.

Time to Buy?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/House-Fire.jpg242360Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-10-26 09:04:172023-10-26 09:55:28The Real Estate Market in 2030

The focus of this letter is to show people how to make money through investing in fast growing, highly profitable companies which have stiff, long term macroeconomic winds at their backs.

That means I ignore a large part of the US economy, possibly as much as 70%, whose time has passed and are headed for the dustbin of history.

According to the Department of Labor's Bureau of Labor Statistics, the seven industries listed below are least likely to generate positive job growth in the next decade.

As most of these stocks are already bombed out, it is way too late to short them. As an investor, you should consider this a “no go” list. I have added my comments, not all of which should be taken seriously.

1) Realtors - The number of realtors is only down 10% from its 1.3 million peak in 2006. I have always been amazed at how realtors who add so little in value take home so much in fees, still around 6% of the gross sales price. Someone is going to figure out how to break this monopoly.

2) Newspapers - these probably won't exist in five years, as five decades of hurtling technological advances have already shrunk the labor force by 90%. Go online or go away.

3) Airline employees - This is your worst nightmare of an industry, as management has no idea what interest rates, fuel costs, or the economy will do, which are the largest inputs into their business. Pilots will eventually work for minimum wage just to keep their flight hours up.

4) Big telecom - Can you hear me now? Nobody uses landlines anymore, leaving these companies with giant corroding copper networks that are costly to maintain. Since cell phone market penetration is 95%, survivors are slugging it out through price competition, cost cutting, and all that annoying advertising.

5) State and Local Government - With employment still at levels private industry hasn't seen since the seventies, firing state and municipal workers will be the principal method of balancing ailing budgets. Expect class sizes to soar to 80 or go entirely online, to put out your own damn fires, and keep the 9 mm loaded and the back door booby trap for home protection.

6) Installation, Maintenance, and Repair - I have explained to my mechanic that the motor in my new electric car has only eleven moving parts, compared to 1,500 in my old clunker, and this won't be good for business. But he just doesn't get it. The winding down of our wars in the Middle East is about to dump a million more applicants into this sector. The last refuge of the trained blue-collar worker is about to get cleaned out.

7) Bank Tellers - Since the ATM made its debut in 1968, this profession has been on a long downhill slide. Banks have lost so much money in the financial crisis, they can't afford to hire humans anymore. It hasn't helped that hundreds of banks have closed during the recession, with many survivors merging to cut costs (read fire more people). Your next bank teller may be a Terminator.

Out With the Old

And in With the New

https://www.madhedgefundtrader.com/wp-content/uploads/2021/07/client-facing.png350480Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-10-26 09:02:192023-10-26 09:54:49Industries You Will Never Hear from Me About

The weakness in stock prices is emblematic of the broader malaise in the Eurozone economy.

The positive here is that the US economy keeps chugging along and on a relative basis, is leaps and bounds stronger than its counterpart.

Why does that matter?

The less money invested into European tech can be diverted into the likes of Tesla (TSLA), Nvidia (NVDA), Apple (APPL), and the rest of the American tech companies.

I absolutely see this as a zero sum game in a world where all the low-hanging fruit has been plucked.

In a globalized world, investors can really just dabble in whatever national market they seek to profit from with ease.

It’s really just a few taps of the screen.

Silicon Valley is already heavily entrenched in Europe with sprawling workforces in many of the 27 countries in which they arbitrage lower wages to their benefit.

If one ever hoped a local rival would root out American variants, it’s a hard slog ahead.

France’s worldline shares plummeted a record 59%, erasing €3.8 billion ($4 billion) of market value, after the French payments company slashed future forecasts.

The stock’s plunge echoes August’s huge fall in peer Adyen NV and follows Tuesday’s 72% drop in fintech CAB Payments Plc. Shares in Adyen declined 7.5% on Wednesday, while another peer, Nexi SpA, slid 18%.

Since then, worries over lofty valuations and a broader slowdown in consumer spending have brought the high-flying stocks back to earth. Adyen, Nexi, and Worldline have lost more than $33 billion in market value combined in the year to date.

Worldline said it now sees full-year organic revenue growth of 6% to 7%, down from a previous forecast of 8% to 10%. The company’s third-quarter sales also missed estimates.

Small fintech companies growing in the single digits is one of the biggest fopaux an up-and-coming fintech company can commit.

Management also complained that European consumers are tapped out.

They don’t have the money to allocate to “non-discretionary” items.

Europeans are basically paying for shelter, energy, and food.

If there is anything else left over, it’s not much. That’s what happens when the cost of living rises between two and three times.

Management also emphasized an acute slowdown in German consumer spending which hurts since these consumers are some of Europe fintechs biggest customers.

I do believe that many investors aren’t going to stay invested in Europe’s fintech space and it is ripe for consolidation which ironically could come from America’s magnificent 7 who have the deep pockets.

It’s a fragmented sub-sector of tech with some operators pigeonholed into one microscopic area of Europe like Andorra or Slovenia.

Technology scales but Europe is hard in the sense it must cut through a vast language, sprawling bureaucracy, high tax regimes, and cultural barriers not to mention different laws. Throw into the mix that multinationals have stopped supporting work visas for non-EU citizens and it is easy to understand why Europe is not ideal for starting tech firms.

The narrow path is why a company like Worldline generates revenue of around $1.2 billion per quarter as opposed to an American PayPal (PYPL) which does $8 billion per quarter.

If we look at the big boys like Google, quarterly revenue goes up to $80 billion per quarter highlighting how far back Europe is from the real upper echelon of American tech.

If Europe is getting trounced by the likes of PayPal, then investors can’t get angry when they get labeled the bush leagues of global technology.

Look at Silicon Valley and especially the tier 2 firms like Uber (UBER) or AirBnb (ABNB) for the real growth instead of Europe’s suffocation of free market technology.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-10-25 14:02:052023-10-25 14:11:08America Shines While Europe Slumbers

(FINDING DEFENSIVE AND STABLE STOCKS AMONGST CHANGING GLOBAL FORCES)

October 25, 2023

Hello everyone,

There are many events taking place right now that will inevitably reshape the world in the near future.

Political instability, Climate change, advances in technology, government debt, and wars that may shift power dynamics amongst world powers are all playing out concurrently.

In five years, we could see a radically different world.

So, how do you cope with all these changes in relation to your stock market holdings?

You play defensive and lock in stable stocks.Let’s look at the three stocks here.

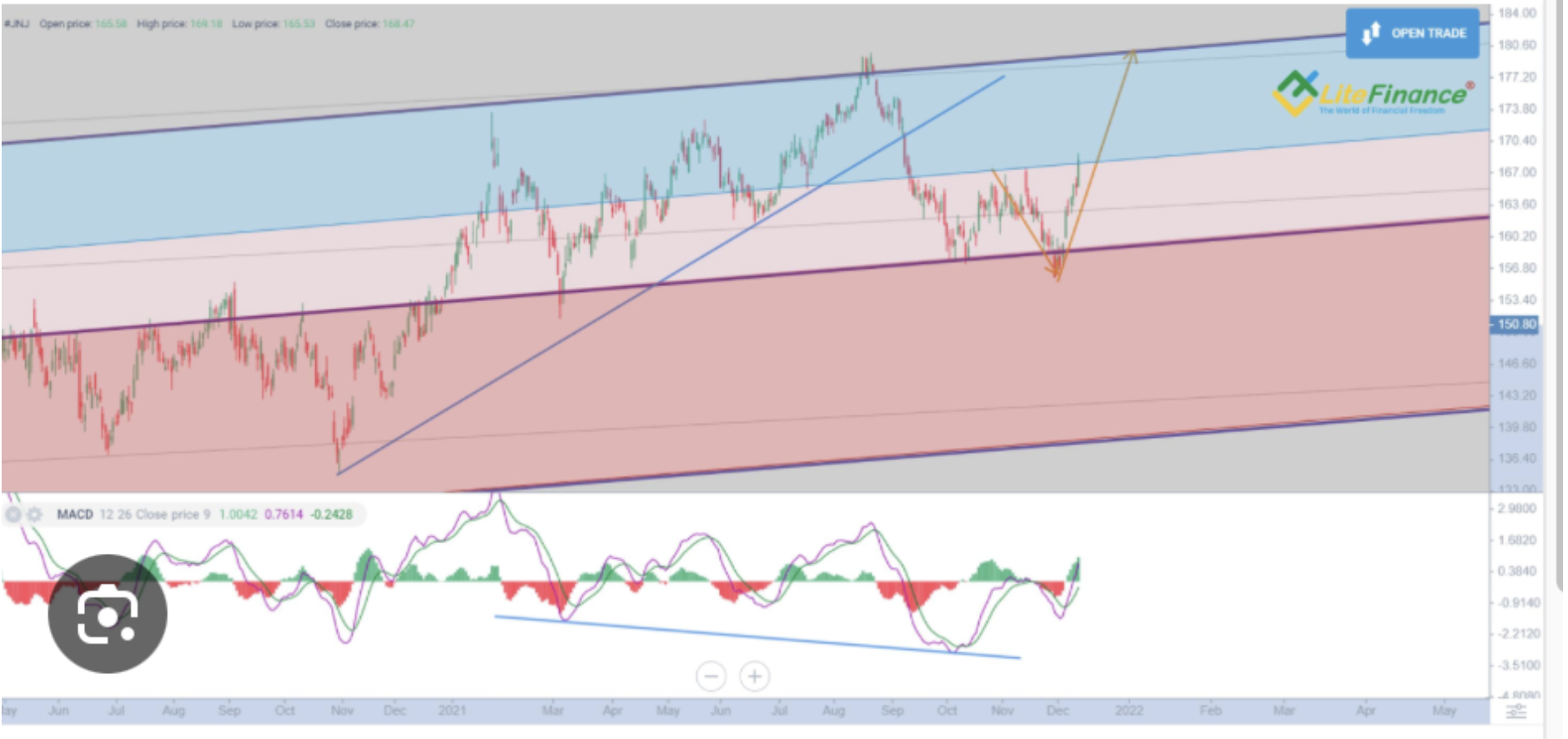

Johnson and Johnson (JNJ)

1/ It’s undervalued.13% decline this year.

2/ 3% dividend.60+ years of dividend growth.

3/ Extensive portfolio of medicines & medical devices.

4/ Analysts predict JNJ stock price could reach $168 by October 2024 & $187 in 2028.

5/ For the 21st year in a row, Fortune has named Johnson & Johnson as a Top 50 All-Star on its list of the World’s Most Admired Companies.

What could go wrong?

JNJ is facing legal action on its talc powder, opioid drugs, and surgical mesh products that could cost the company a lot of money, and impact sentiment on the company.

Earnings results:

Topped quarterly earnings and revenue estimates.

EPS: $2.66 vs $2.52 expected

Revenue: $21.35 billion vs. $21.04 billion expected.

Lifts full-year guidance as MedTech and pharmaceutical sales jump.

Johnson and Johnson stock forecast & price prediction for 2023 & 2024 & beyond.

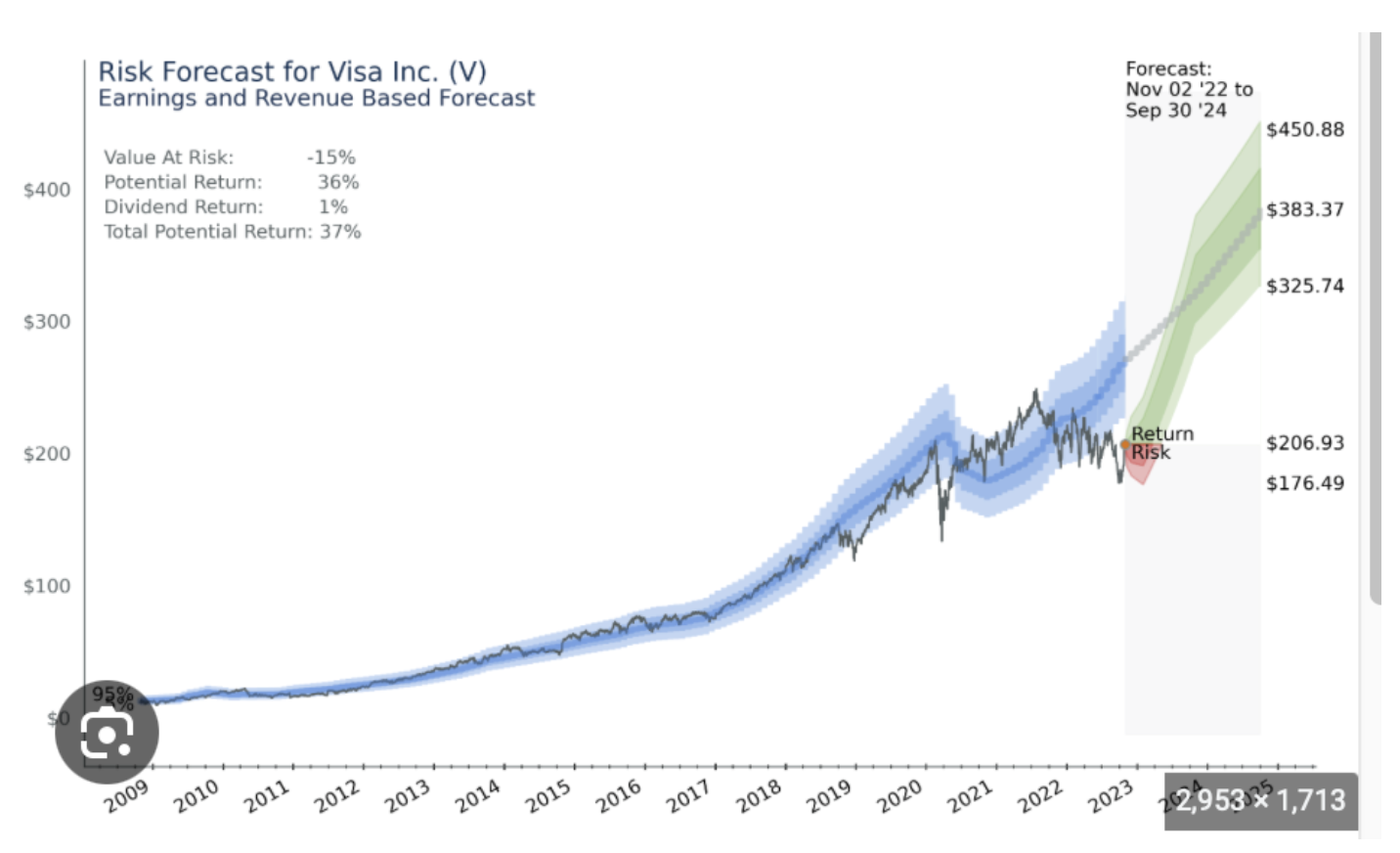

Visa (V)

1/ Dominant force in digital payments. Strong financial position.Healthy balance sheet.

2/ Proactively involved with fintechs.

3/ 0.76% dividend.

4/ 61% share of the credit card market.

5/ Visa is less volatile than 75% of U.S. stocks over the last three months.

6/ EPS have increased by around 20% a year over the last 5 to 10 years.

7/ Visa works with businesses in new and evolving industries, including fintech platforms, crypto projects, and content creators. These programs may help it find traction in new areas of growth.

8/ Credit and debit card penetration in emerging markets is still low, but disposable incomes are increasing.A possible growth opportunity for Visa.

7/ Analysts predict Visa stock price could rise to $250 by the end of 2024 and $300 by the end of 2025 and be at $500 in 2030.

What could go wrong?

A severe recession resulting in lower payment volumes.

Competing technologies taking market share from Visa.

Growth opportunities missed due to regional networks/alternative payment systems.

Regulators ending the Visa/Mastercard duopoly impacting fees.

Earnings Results:

Posted better than expected fiscal Q4 earnings and revenue as payments volume, cross-border volume, and payment transactions stayed resilient.

Visa boosted its dividend by 16%.

The company announced a $25 billion stock buyback.

Net revenue for the quarter climbed to $8.61B, topping the $8.55B consensus estimate.

Alphabet (GOOGL)

1/ Google has a monopoly on Search.At 93% worldwide market share, the company is well-positioned to profit from the search industry’s expansion in the coming years.

2/ The company has huge profit margins.

3/ Digital ad sales are set to rise.(Analysts argue that the digital ad market will grow by nearly 50% to $910 billion by 2027).

4/ Google Cloud will soon become a profitable vehicle.Google Cloud is the third largest provider of cloud infrastructure services, behind only Amazon Web Services and Microsoft’s Azure.Its highly regarded data analytics capabilities will advance Google Cloud’s growth.The cloud computing market is expected to exceed $1.5 trillion by 2030, according to Grand View Research, so Google Cloud is well positioned to be Alphabet’s next major profit driver.

4/ Stock buyback initiative.

5/ Analysts predict that the stock price could rise to around $490 by 2030.

What could go wrong?

a) Google faces headline risks over anti-trust lawsuits.

b) Regulatory challenges.

c) The company loses the AI war against rival Microsoft.

d) Google’s overreliance on advertising business (may soften during a recession)

Earnings Results:

11% revenue growth in the third quarter.

Shares dropped around 7% in extended trading – the cloud business missed analysts’ expectations.Cloud revenue came in below estimates at $8.41 billion, missing the mark by more than $20 million.Once Google Cloud becomes profitable it will propel the shares much higher.

Stock price forecasts for Google in 2023, 2024 and beyond.

The current chip war with China brings back memories of my five-decade-long relationship with the People’s Republic of China.

I normally avoid the diplomatic circuit, as the few non-committal comments and soggy appetizers I get aren’t worth the investment of time.

But I jumped at the chance to celebrate the 62nd anniversary of the founding of the People’s Republic of China with San Francisco Consul General Gao Zhansheng.

Happy Birthday, China!

When I casually mention that I survived the Cultural Revolution and interviewed major political figures like Premier Deng Xiaoping, who launched the Middle Kingdom into the modern era, and his predecessor, Zhou Enlai, modern-day Chinese are enthralled. It’s like going to a Fourth of July party and letting drop that I palled around with Thomas Jefferson and Benjamin Franklin.

Five minutes into the great hall, I ran into my old friend Wen, who started out her career with the Chinese Intelligence Service and had made the jump to the Foreign Ministry, as all their best people did. She was passing through town with a visiting trade mission.

When I was touring China in the seventies as a guest of the Bank of China, Wen was assigned as my guide and translator, and we kept in touch over the years. I was assigned a bodyguard who doubled as the driver of a tank-like Russian sedan.

The Cultural Revolution was on, and while the major cities were safe, we ran the risk of running into a renegade band of xenophobic Red Guards, with potentially fatal consequences.

I asked Wen when China was going to float the Yuan. She explained that this is something China knew it had to do, but it wasn’t going to be rushed into by some opportunistic foreign politicians.

If it moves too soon, millions will lose jobs, creating political instability, something the central government wants to avoid at all costs. Many of the largest scale employers were only marginally profitable, and a hike in the renminbi of only a few percent would force them out of business. I pointed out that that was exactly what was happening in the US.

Worth More Than Meets the Eye

I warned that if the Middle Kingdom waited too long, Washington would force them into an appreciation through punitive import duties and anti-dumping actions, as we did with Japan 50 years ago.

It was Nixon’s surprise ban on textile imports in 1971 that finally persuaded Japan to float the yen, then at ¥360. If that didn’t convince the Chinese, then imported inflation would. The longer China delays, the bigger the pop when their currency is finally set free.

Wen then went on the offensive, claiming that Chinese workers were being exploited by American companies keeping wages low. The product that China made for $1, and sold to the US for $2, was then sold by Walmart (WMT) for $20, which kept all the profits.

She pointed out that the Walton family had a combined net worth of $238 billion, more than the total worth of the lower 40% of the US population. This could never happen in China.

I told her that by selling the product at $20, Walmart wiped out another US company that used to make that product domestically and sold it for $40, throwing those people out of work.

Modern Times in China

I then asked Wen what were her country’s plans for its massive foreign exchange reserves, now at $3.2 trillion. She agreed that this was a problem because the reserves were pouring in so fast at an embarrassingly high rate of $10 billion a month and that it was the most rapid accumulation of wealth in history (click here for the data). In any case, reserves have been falling for the past year from a peak of $4.1 trillion.

While it had more than enough Treasury bonds, any attempt to sell might cause their value to collapse and freeze relations with the US. I suggested China should start hedging its gigantic holdings without selling them, or some managers would be facing a firing squad in the future.

China tried to recycle its surpluses by buying foreign companies that produce the natural resources it desperately needs. But takeover attempts were fought tooth and nail as a foreign invasion, or on national security grounds, such as the attempt to buy California’s Unocal in 2005 and Australia’s Oz Minerals in 2012.

It was now using a strategy of buying low profile minority stakes in foreign resource companies. China took a big stake in the Petrobras (PBR) secondary equity offering, which didn’t work out so well, as the company is now facing bankruptcy.

I asked her about the real estate bubble in China that was causing so many foreign investors to lose sleep. She said it was true that sales were slow at some luxury buildings in Beijing and Shanghai, but the great majority of developments were aimed at working people and were filling up as soon as they came on the market.

The 40% down payment demanded by the People’s Bank of China headed off the rampant speculation that brought the American financial system down. Buyers of second homes were required to pay entirely in cash.

Rooms With Views

Wen then complained about the aggressive military stance the US was taking towards China, ringing it in with the Seventh Fleet. Holding a knife so close to the country’s foreign supply line jugular vein made them nervous.

China was basically indefensible. All it would take was the sinking of a few grain ships, and 50 million would starve within a year.

Wen told me there is a school of thought in Beijing that as the country’s economic power grows- it passed Japan to become second in GDP in 2010– that the US will increasingly perceive it as a military threat. This would lead America to mete out the same hostile treatment to China as it has done to Russia since the Ukraine War began.

Walking Softly, But Carrying a Big Stick

I assured her that the Seventh Fleet was there to watch and listen, but to do nothing. It was really in a position to provide a security blanket for allies, like Japan and South Korea, but nothing more. China wasn’t engaging in the belligerent behavior that Russia was at the height of the Cold War, like blockading Berlin, basing missiles in Cuba, stationing fast attack nuclear submarines off our coasts, and invading Afghanistan.

I argued that if China truly has no expansionary intentions, the more we know about you, the better. It is always prudent for a potential adversary to conclude you are not a threat, and that no action is needed.

The more you help the US do that, the better. China is decades behind the US in military technology, and you really have nothing we want. Little more than 200 nuclear weapons without an ICBM or submarine delivery systems were hardly viewed as a major threat.

Wen seemed perturbed that I was aware of her country’s nuclear stockpiles, and asked how I knew this. I said that former CIA director Leon Panetta told me. She said “Oh.” I asked what was that test downing of a satellite in space about, anyway. She didn’t answer.

Looking at the world for the next 30 years, who is the Pentagon going to model and war game against, but China, with its 2.5 million-man army?

Wen countered that the People’s Liberation Army was purely a defensive force. With a 12,000-mile land border, an 11,000-mile coastline, and dubious neighbors like Russia, Iran, and India, they have no other choice. Its ability to project force over great distances, as the US can, is virtually nonexistent.

Its 1979 invasion of Vietnam was about reclaiming ten miles of lost territory. China got involved in Korea only after General Douglas MacArthur threatened to rain atomic bombs on the mainland, losing 2 million men, including Chairman Mao’s son. China could have done a lot more in the Vietnam War, but didn’t, limiting its participation to a supply, logistical, and advisory role.

That’s a Lot of Border to Defend

I then warned that if you really are worried about the Pentagon, you should stop hacking into our computers. She replied that the US started this by emptying out Chinese mainframes many times, and they were only responding in kind.

I said yes, but that China was targeting private companies, like Google (GOOG), Microsoft (MSFT), and Oracle (ORCL) that without military-grade software, were unable to defend themselves. The Chinese agencies involved then used the data to their own commercial advantage.

What Did You Say the Password Was Again?

By the time Wen married, China had already adopted its one-child policy. As much as she wanted more children, she understood the government’s need to adopt such a drastic policy. Without it, the population today would be 1.8 billion, not 1.2 billion, and all of the money that went into buying capital goods would have been spent on food imports instead.

The country would have stagnated at its 1980 per capita income of $100/year. There would have been no Chinese economic miracle. She was very proud of her one son, who was a software engineer at Microsoft (MSFT) in Beijing.

Her husband, a mid-level official at the Ministry of Commerce, fared less well, dying of lung cancer at a relatively early age. The US and Europe had exported their worst polluting industries to China to take advantage of lax environmental controls, turning the air in Beijing into a choking haze.

Sometimes her son would come home from school coughing and wheezing so badly that he couldn’t play outside. The two packs of cigarettes a day her husband smoked didn’t help either.

Imported From the USA

I asked if she recalled our first trip together and a dark cloud came over her face. We were touring a section of Fuzhou when three policemen marched up. They started shouting at Wen that we were in a restricted section of the city where foreigners were not allowed. They started mercilessly beating her with clubs.

I was about to intercede when my late wife, Kyoko, let go with a blood-curdling tirade in Japanese that froze them in their tracks. I saw from the fear in their faces that she had ignited their wartime fear of Japanese authority and the dreaded Kempeitai, or secret police, and they beat a hasty retreat.

To this day, I’m not exactly sure what Kyoko said. We took Wen back to our hotel room and bandaged her up, putting ice on the giant goose egg on her head. When I left, I gave her my copy of HG Well’s A Short History of the World, which she treasured, as the book was then banned in China.

Wen mentioned that she was approaching the mandatory retirement age of 60, and soon would be leaving the Foreign Service. I suggested she move to San Francisco, which offered a thriving Chinese community. She laughed. No matter how much prices had fallen, she could never afford anything here on a Chinese civil servant’s salary.

Wen told me that China was grateful for the billions of dollars that foreigners had poured into her country as a result of my writings. I replied that I was simply trying to show my readers where to make some money, nothing more. It was pure opportunistic self-interest.

One of my early recommendations, Chinese search engine Baidu (BIDU), was up more than tenfold in less than two years. Did she happen to know about any more future Baidu’s? Wen said that she wasn’t that close to the stock market, but that she would get back to me.

I asked Wen if she still had the book I gave her nearly five decades ago. She said it had become a family heirloom and was being passed down through the generations. As she smiled, I noticed the faint scar on her eyebrow from that unpleasantness so long ago.

In view of Wen’s comments, I think you have to pass on investing in China (FXI) for the short term.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/Chinese-Woman.jpg209366Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-10-25 09:02:072023-10-25 13:55:49An Evening With the Chinese Intelligence Service

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.