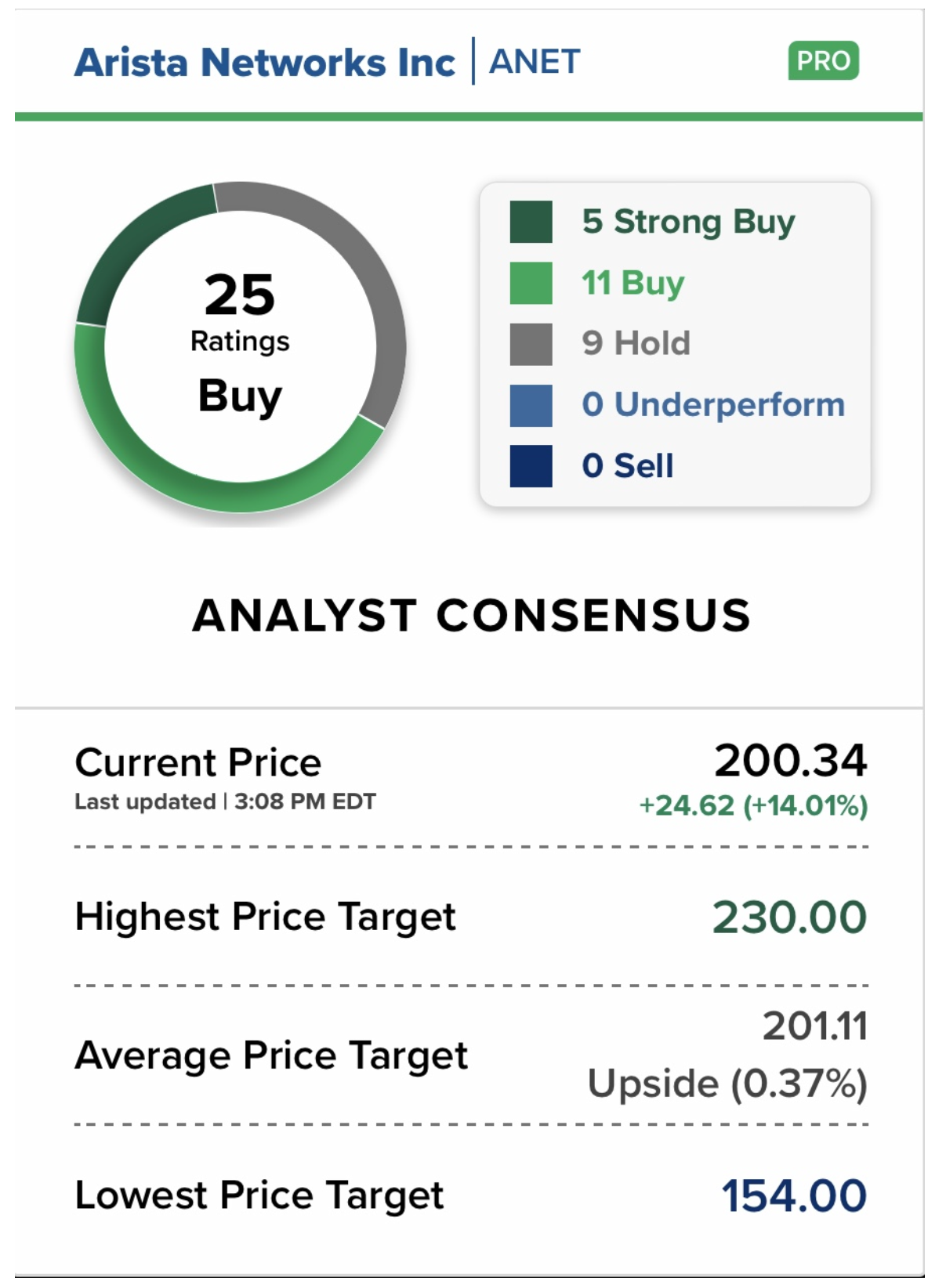

Wall Street is upbeat about an AI stock called Arista.

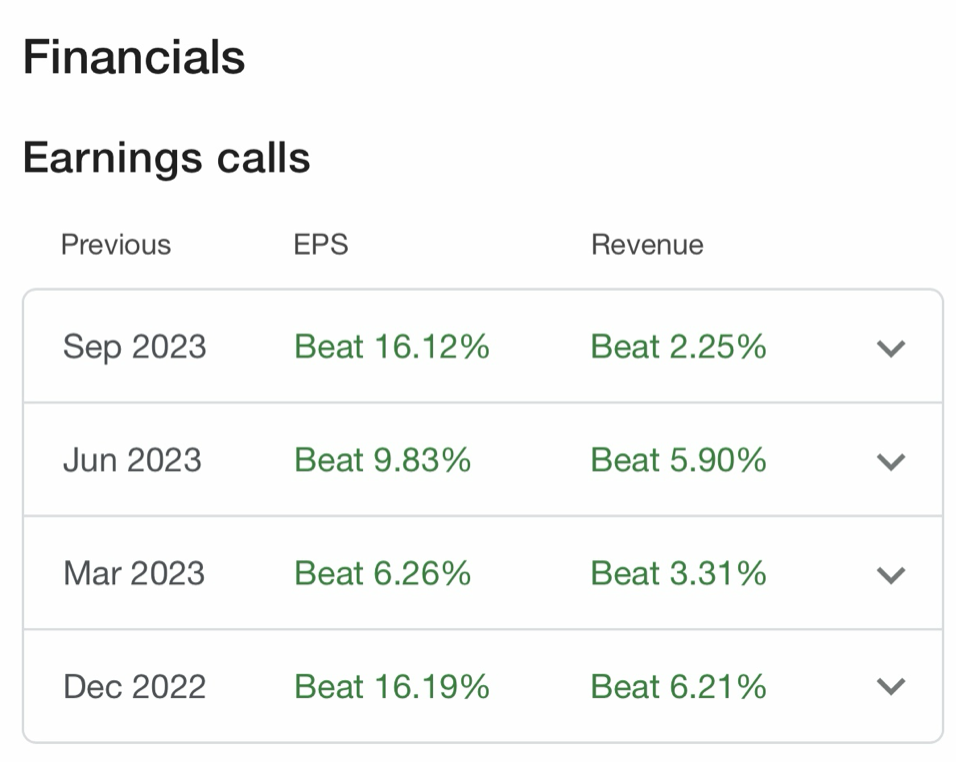

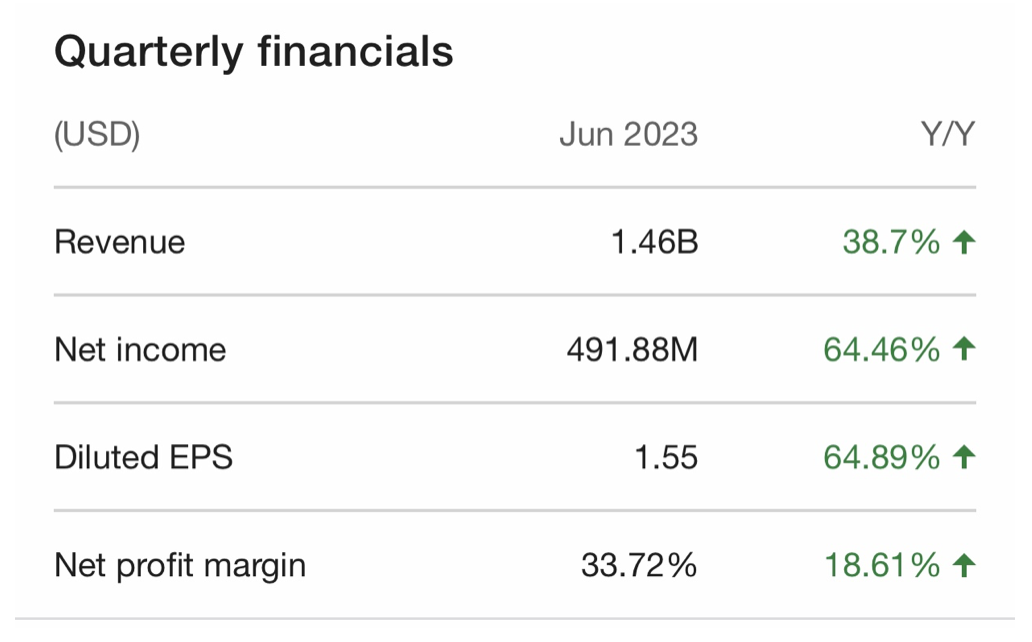

On Monday, the company earnings exceeded Wall Street expectations on both the top and bottom lines.

Earnings:$1.83/share

Revenue:$1.51

Analysts forecast:

Earnings:$1.58/share

Revenue:$1.48 billion

Arista also issued high-than-expected forward guidance, calling for fourth-quarter revenue in the range of $1.5 billion to $1.55 billion.

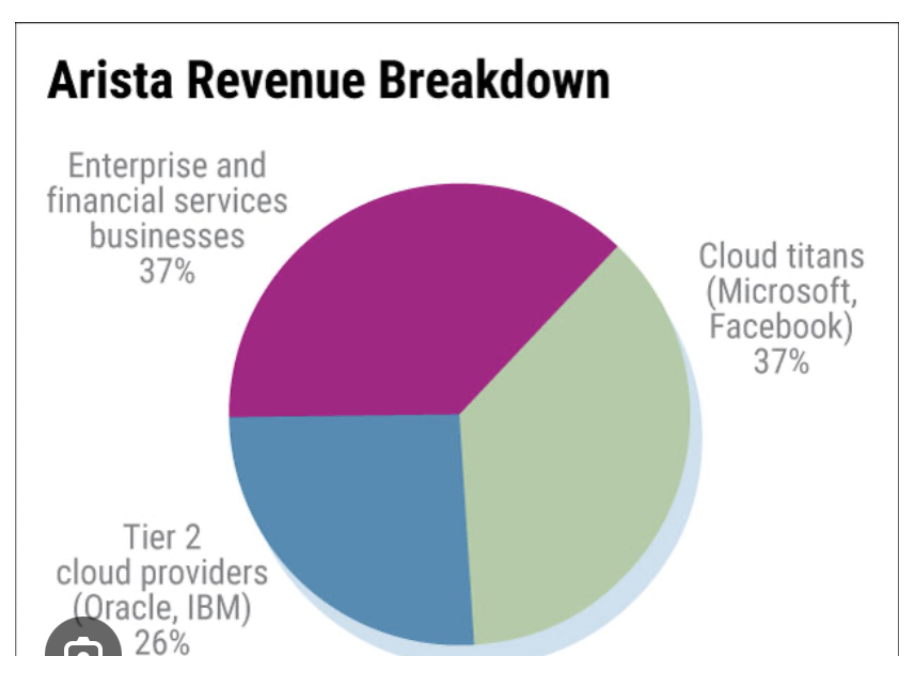

Arista’s focus is low-latency networks between clients and the cloud for large-scale data centres, exposing the company to growing investor interest in AI.

The stock is up 63% in 2023.

Analysts believe the company could be the top player in the Ethernet application of AI.Morgan Stanley and Wells Fargo, among others applauded the company report and highlighted the company’s potential AI catalyst for growth heading into 2024.

Morgan Stanley’s Meta Marshall believes growth will accelerate from the adoption of 800G Ethernet transceivers for data centres.Marshall upgraded Arista to overweight and gave the stock a price target of $220 which is more than 25% upside from Monday’s $175.72 close.

Market Update

U.S. 10-year Yields

We have been consolidating since reaching 5.0210% on October 23rd.But we may have another leg up before exhaustion.

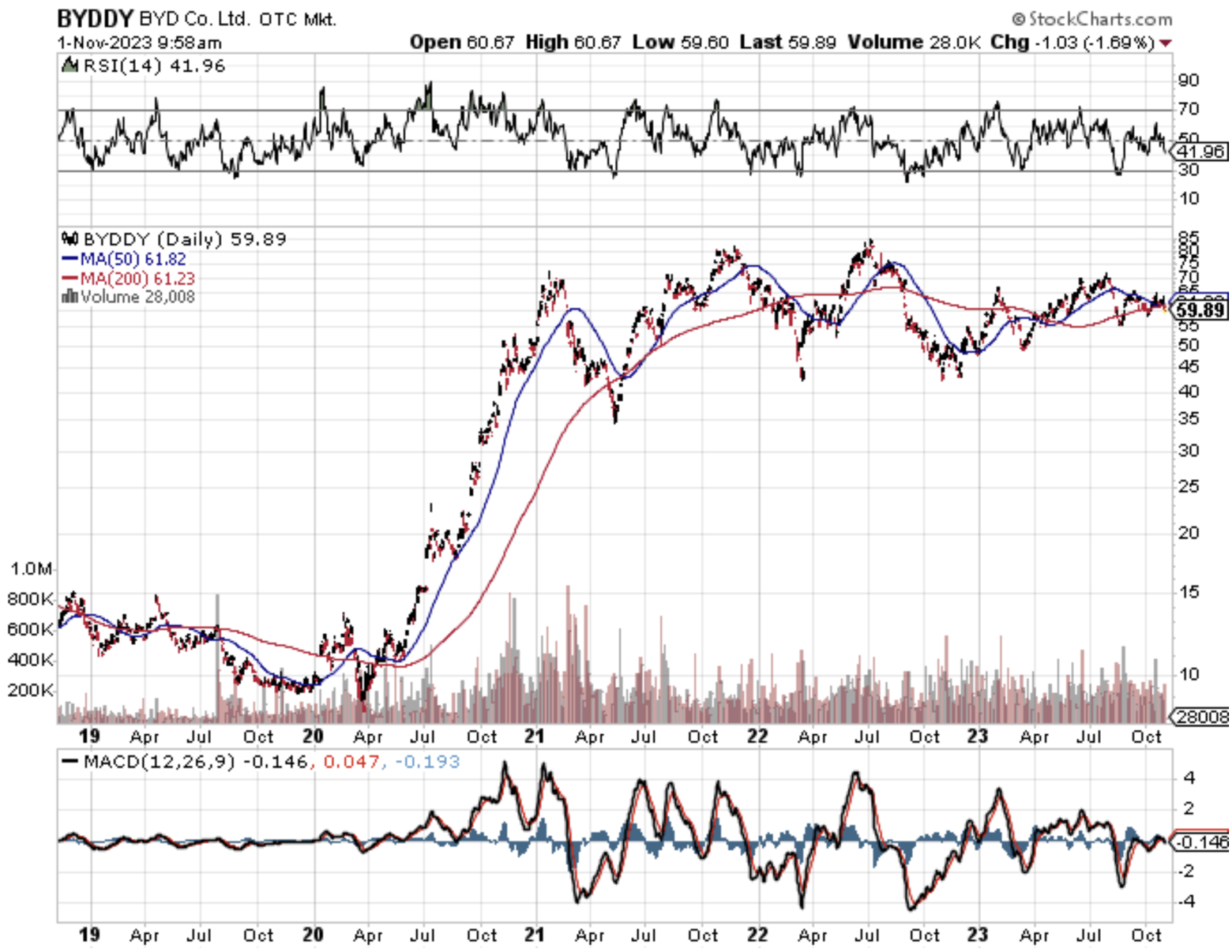

Tesla’s (TSLA) recent underperformance is a canary in the coal mine of what could become of the global EV industry.

EV makers better watch out because the race to zero is coming for all of them.

It could be yet another tech industry captured by the Chinese. The Chinese are quickly rising up the food chain of technological capabilities and these new developments are sure to rattle the White House.

I remember years ago when the Chinese tried their best at smartphones, they were terrible, but fast forward to today, and now they compare close to the iPhone with much better pricing.

Now, the Chinese are coming after electric cars and I also remember touring EVs in China in 2007 and they again were pretty terrible.

However, fast forward to today, and yet again they have achieved major inroads in terms of quality and reach. BYD Company Limited (BYDDY) even produces something comparable to Tesla which is no small feat.

Tesla’s disappointing third-quarter deliveries highlight the panic state side where the first mover advantage has served CEO Elon Musk well but eroded lately.

Tesla sold 435,000 electric cars last quarter, while BYD sold 431,000 battery-powered electric cars over the same period.

Expect BYD to surge past Tesla in delivered electric cars soon because they have access to a vastly bigger market while the Chinese communist party is doing everything to ruin American corporate business in the Middle Kingdom.

BYD is already far ahead when it comes to total sales. Including hybrids, BYD sold over 800,000 cars last quarter, almost twice as much as Tesla.

The Chinese company sold 1.8 million cars last year, over 911,000 of which were BEVs. Tesla, which only sells BEVs, sold 1.3 million cars.

Musk had previously warned that planned upgrades to manufacturing plants around the world may lead to lower deliveries for the rest of the year.

Tesla is also facing sluggish demand, forcing it to launch aggressive price wars in both China and the U.S.

BYD has surged ahead of its competitors in China by selling more affordable electric vehicles, unlike the premium models sold by Tesla and other EV companies like Nio and XPeng. BYD recently unseated Volkswagen as China’s top-selling car brand.

The company is expanding outside of China and is now the top-selling EV brand in markets like Thailand, Israel, and Singapore. It’s even expanding into more developed markets like Japan and Europe.

Watch out for China’s BYD to hijack Western markets moving forward including Europe, Canada, the United States, and the UK.

It’s finally time to stop ignoring that China does a good job producing EVs and other hard-to-manufacture technology.

My guess is that China will also surpass the United States in semiconductor chip technology, although that will take longer to achieve.

The Pentagon has sounded the alarm bells after noticing huge improvements in chip know-how by the Chinese.

Competition is finally here for Musk after so many years of taking a free ride in the US and it’s about time. Now the rubber finally meets the road.

Readers with a high threshold of risk tolerance should look at BYD’s ADR (BYD) if shares experience a big dip then allocating a small portion of a portfolio to this equity makes sense.

Don’t forget there is now a high probability of Tesla losing its Shanghai factory in China once China seizes American businesses on the mainland. It doesn’t matter how much Musk kowtows to the communist party because this issue is far bigger than him or the EV business.

That threat has gone from almost 0 just recently to becoming somewhat plausible although still quite low. The tech world is accelerating at warp speed in 2023.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-01 15:02:492023-11-01 16:38:15BYD is Here to Stay

With interest rates and inflation topic number one of the day, everyone has their favorite inflation indicator. The Fed has its, you have yours, and well, I have mine.

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its “Big Mac” index of international currency valuations.

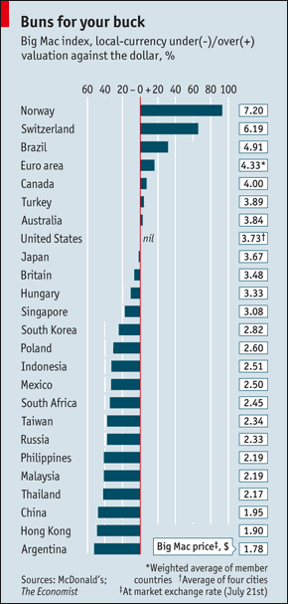

Although initially launched as a joke four decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success. The index counts the cost of McDonald’s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the the Chinese Yuan (CYB), and the Thai Baht are cheap.

I couldn’t agree more with many of these conclusions. It’s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my hip. Better to use it as an economic forecasting tool, than a speedy lunch.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/11/big-mac-yen.jpg312416Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-01 09:04:142023-11-01 15:31:16Where The Economist “Big Mac” Index Finds Currency Value

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.