BUY the United States Treasury Bond Fund (TLT) January 17, 2025 $95-98 at-the-money vertical Bull Call spread LEAPS at $1.25 or best

Opening Trade

1-23-2024

expiration date: January 17, 2025

Number of Contracts = 1 contract

An $8 selloff in the (TLT) is the best entry point we are going to get for this LEAPS. This is a gift from the Federal Reserve which has indicated it may cut interest rates 3-6 times this year.

While the chance of winning a real lottery is something like a million to one, this one is more like 10:1 in your favor. And the payoff is a double in a year. That is the probability that (TLT) shares will rise by only 1.28% over the next 12 months.

The logic behind this LEAPS is fairly simple.

After keeping interest rates too low for too long, and then raising them too far too fast, what does the Fed do next? It then lowers interest rates too far too fast. In other words, a mistake-prone Jay Powell will keep on making mistakes. That’s what you get with a Fed chair who only has a degree in political science.

The rate of interest rate rises has been the most rapid in history. Keep it up and a recession in 2024 is a sure thing.When recession hits, demand for money will dry up and interest rates will collapse. For that reason, the Fed has to start its interest-cutting cycle sooner than later.

Yields on ten-year US Treasury bonds that bottomed at 0.32% in 2020 and reached a peak of 5.08% in October 2023 will easily fall back down to 3.00% by the time this LEAPS matures. That will take the (TLT) at least back up to $120.

I am using the very conservative $95-$98 strike price in case bonds continue bouncing along a bottom before turning higher in a few months. If a double in a year is not enough for you, perhaps you should consider another line of business.

I am therefore buying the United States Treasury Bond Fund (TLT) January 17, 2025 $95-98 at-the-money vertical Bull Call spread LEAPS at $1.25 or best.

Don’t pay more than $1.80 or you’ll be chasing on a risk/reward basis.

I am going out to only a January 17, 2025 expiration because I think this trade will work fairly quickly. Please note that these options are illiquid, and it may take some work to get in or out. Executing these trades is more an art than a science.

Let’s say the United States Treasury Bond Fund (TLT) January 17, 2025 $95-98 at-the-money vertical Bull Call spread LEAPS are showing a bid/offer spread of $1.10-$1.50, which is typical. Enter an order for one contract at $1.10, another for $1.20, another for $1.30 and so on. Eventually, you will enter a price that gets filled immediately. That is the real price. Then enter an order for your full position at that real price.

A lot of people ask me about the appropriate size. Remember, if the (TLT) does NOT rise by 1.28% in 12 months, the value of your investment goes to zero. The way to play this is to buy LEAPS in ten different names. If one out of ten increases ten times, you break even. If two of ten work, you double your money, and if only three of ten work, you triple your money.

You never should have a position that is so big that you can’t sleep at night, or worse, need to call John Thomas asking if you should sell at a market bottom.

There is another way to cash in. Let’s say we get half of your double in the next three months, which from these low levels is entirely possible. Then you could earn half of the maximum potential profit in months. You can decide whether to keep the threefold return or go for the full five-bagger. It’s a nice problem to have.

Notice that the day-to-day volatility of LEAPS prices is minuscule since the time value is so great, usually sporting implied of less than 10%. This means that the day-to-day moves in your P&L will be small. It also means you can buy your position over the course of a month just entering new orders every day. I know this can be tedious but getting screwed by overpaying for a position is even more tedious.

Look at the math below and you will see that a 1.28% rise in (TLT) shares will generate a 100% profit with this position, such is the wonder of LEAPS. That gives you an implied leverage of 68:1 across the $95-$98 space.

Only use a limit order. DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES. Just enter a limit order and work it.

This is a bet that the (TLT) will not fall below $98 by the January 17, 2025 option expiration in 12 months.

Here are the specific trades you need to execute this position:

Buy 1 January 2025 (TLT) $95 calls at………….………$5.00

Sell short 1 January 2025 (TLT) $98 calls at…….……$3.75

Net Cost:………………………….………..………….…...........$1.25 Potential Profit: $3.00 - $1.25 = $1.75

(1 X 100 X $1.75) = $175 or 140% in 12 months.

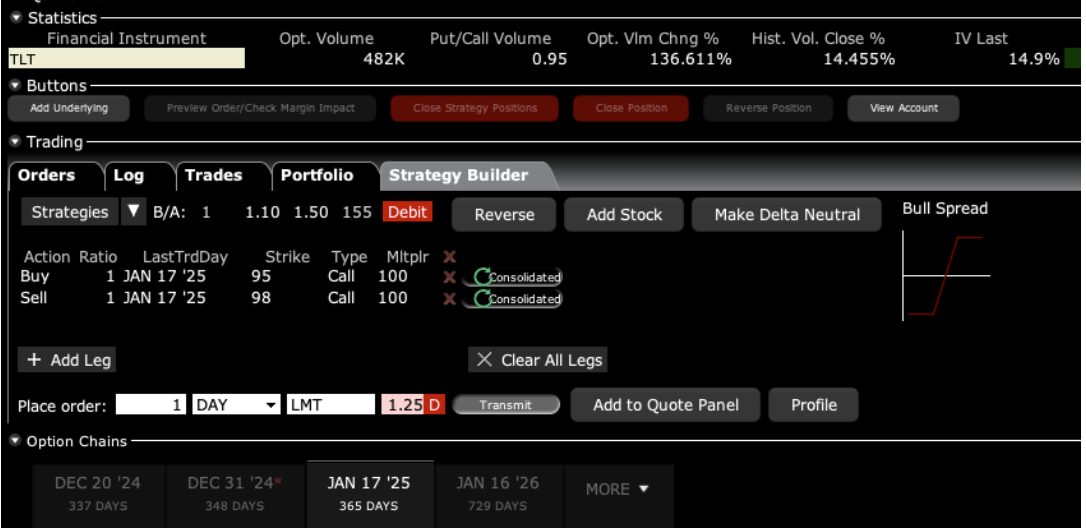

To see how to enter this trade in your online platform, please look at the order ticket below, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Debit Spread”by clicking here at

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep-in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

In the tempestuous arena of artificial intelligence (AI), whispers of a challenger echo on the horizon. Sam Altman, the enigmatic visionary behind OpenAI and former president of Y Combinator, has ignited a fiery debate with his proposition – a network of custom chip factories dedicated solely to accelerating AI development. This audacious gambit threatens to disrupt the established order, casting NVIDIA, the reigning king of graphics processing units (GPUs), in the uncertain glare of potential dethronement.

NVIDIA's Throne: Built on GPU Supremacy

NVIDIA's grip on the AI hardware landscape is undeniable. Their high-performance GPUs, optimized for tasks like parallel processing and matrix multiplication, have become the de facto standard for training and running complex AI models. This dominance owes largely to two factors:

Performance Prowess: NVIDIA's GPUs boast superior computational power and memory bandwidth compared to traditional CPUs, making them ideal for the computationally intensive demands of AI algorithms.

Ecosystem Advantage: NVIDIA has cultivated a thriving ecosystem of tools and software libraries specifically designed for their GPUs. This makes it easier for developers to deploy and optimize their AI models on NVIDIA hardware.

However, NVIDIA's fortress, while formidable, is not impregnable. Cracks have begun to appear, whispering of potential vulnerabilities:

Costly Crown: NVIDIA's high-end GPUs come at a steep price, limiting access to smaller research labs and startups. This creates a barrier to entry and slows down the democratization of AI development.

Flexibility Famine: GPUs, while powerful, are designed for a specific set of tasks. This lack of flexibility can bottleneck the development of specialized AI models for unique applications.

Altman's Gambit: Tailored Silicon for AI's Leap

Enter Sam Altman, the Silicon Valley disruptor, with a bold counter-offensive. His proposed network of chip factories wouldn't simply compete with NVIDIA; it would rewrite the rules of the game. Here's the crux of his strategy:

Custom-Crafted Chips: Forget one-size-fits-all. Altman envisions chips specifically designed for the unique computational needs of AI algorithms. This could lead to significant performance gains and efficiency improvements.

Democratizing Access: By lowering production costs and simplifying chip design, Altman aims to make AI hardware more accessible to a wider range of researchers and developers. This could unleash a wave of innovation from previously sidelined players.

Open Hardware Ecosystem: To counter NVIDIA's software advantage, Altman proposes an open-source ecosystem for AI chips. This would foster collaboration and accelerate the development of tools and libraries specifically optimized for his custom hardware.

The Clash of Titans: Uncertainties and Opportunities

But is Altman's plan a masterstroke or a fool's errand? The path ahead is fraught with uncertainties:

Execution Complexity: Building and operating a network of chip factories is a monumental undertaking, requiring billions of dollars and navigating the treacherous landscape of semiconductor manufacturing.

Technical Hurdles: Designing and fabricating custom chips for highly specialized applications is no easy feat. The technical challenges involved are considerable, and success is far from guaranteed.

Competitive Landscape: NVIDIA is not resting on its laurels. They are actively investing in new AI-specific hardware and software solutions, ensuring a fierce battle for market share.

Despite these challenges, the potential rewards are tantalizing:

Faster AI Development: Custom chips could lead to dramatic reductions in AI training times, unlocking faster experimentation and quicker breakthroughs.

Lowering the Barriers: Increased accessibility to AI hardware could democratize the field, fostering innovation and attracting new talent.

Diversifying the Landscape: A healthy competition in the AI hardware market could lead to a wider range of solutions optimized for different needs and applications.

Beyond the Binary: A Symbiotic Future?

Ultimately, the battle between Altman and NVIDIA might not be a zero-sum game. Both players have the potential to contribute significantly to the advancement of AI. Here are some intriguing possibilities:

Coexistence and Cooperation: NVIDIA and Altman's factories could coexist, catering to different segments of the market and fostering an environment of healthy competition and collaboration.

Hybrid Solutions: Both custom chips and general-purpose GPUs could find their place in the AI hardware landscape, each playing to their respective strengths for specific tasks.

Shifting Paradigms: The focus on specialized AI hardware could spur further innovation in chip design and architecture, leading to entirely new approaches to computing optimized for the demands of artificial intelligence.

The Verdict: A Catalyst for Change, Not a Guaranteed Revolution

While it's too early to predict the outcome of this silicon showdown, one thing is clear: Sam Altman's gambit has thrown a stone into the AI hardware pond, sending ripples of excitement and apprehension across the industry

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2024-01-22 16:52:542024-01-22 16:57:28Silicon Showdown: Can Sam Altman's AI Chip Factories Topple NVIDIA's Reign?

When John identifies a strategic exit point, he will send you an alert with specific trade information on what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-22 15:28:122024-01-22 15:36:19Trade Alert - (SPY) January 22, 2024 - STOP LOSS - SELL

Stocks and firms tethered to artificial intelligence won’t always have a one-way joyride to profits.

The honest truth is that the road will be met with drawbacks some years and the sector will need time to digest the new developments.

Mainstream tech has made most people believe that AI can do no wrong in the short-term future.

There is a consensus that it’s the panacea for everything and anything.

The Magnificent 7 tech firms are priced for an AI boom and the hype is there, but it will take some time for AI to really filter into meaningful balance sheet development.

We are still in the beginning stages.

It’s not surprising that the Massachusetts Institute of Technology published a study that sought to address fears about AI replacing humans in a swath of industries and found that artificial intelligence can’t ACTUALLY replace the majority of jobs right now in cost-effective ways.

It’s important to note this report because much of AI has been celebrated with no mention of cost control or benefit versus the price or expenses incurred.

Any corporate tech will need to evaluate whether it’s worth gutting whole divisions to replace it with AI.

In many cases in early 2024, this type of strategy to a workforce could turn into an unmitigated disaster.

For instance, a new AI study found only 23% of workers, measured in terms of dollar wages, could be effectively supplanted. In other cases, because AI-assisted visual recognition is expensive to install and operate, humans did the job more economically.

The adoption of AI across industries accelerated last year after OpenAI’s ChatGPT and other generative tools showed the technology’s potential. Tech firms from Microsoft and Alphabet in the US to Baidu and Alibaba in China rolled out new AI services and ramped up development plans which could serve as a canary in the coal mine for things to come. Fears about AI’s impact on jobs have long been a central concern.

Computer vision is a field of AI that enables machines to derive meaningful information from digital images and other visual inputs, with its most ubiquitous applications showing up in object detection systems for autonomous driving or in helping categorize photos on smartphones.

The cost-benefit ratio of computer vision is most favorable in segments like retail, transportation, and warehousing.

The study was funded by the MIT-IBM Watson AI Lab and used online surveys to collect data on about 1,000 visually assisted tasks across 800 occupations. Only 3% of such tasks can be automated cost-effectively today, but that could rise to 40% by 2033 if data costs fall and accuracy improves.

When getting academic about the subject, many projections feel way too ambitious.

AI won’t take over the workforce in the next few years and will struggle to make inroads before 2030.

That doesn’t mean firms like Nvidia, AMD, Qorvo, and Broadcom will not sell AI-based chips promising better AI.

That doesn’t mean firms like Google, Apple, Microsoft, Amazon, and Meta won’t feel a small AI bump in revenue.

There certainly will be some changes, but wholesale transformation is a ways off.

I believe the AI hype has gotten too far over its skis.

Tech needs to slow down and make sure it’s properly implemented and the real effects will be seen after 2030.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-22 14:02:212024-01-22 15:18:21Take A Deep Breath With AI

“The only true wisdom is in knowing you know nothing.” – Said Greek Philosopher Socrates

https://www.madhedgefundtrader.com/wp-content/uploads/2023/11/socrates.png560398april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-22 14:00:162024-01-22 15:18:00January 22, 2024 - Quote of the Day

(BUFFETT INVESTMENT LESSON 101 HAS TWO KEY PRINCIPLES)

January 22, 2024

Hello everyone,

It’s been a very wet and stormy January in Queensland this year.And we now have a cyclone lurking off the Queensland coast about to create havoc with the coastal communities in far north Queensland. The weather might be all over the place, but the stock market appears to be seeing things very clearly.

Welcome to a new bull market which started back in October 2022.Bull markets on average last more than 1,700 days, or longer than four years, the data shows.The median length of a bull is just north of 1,500 days.

The current run has lasted about 15 months, or under a year and a half, thus far.Investors are optimistic and excitement is almost palpable about the Fed cutting interest rates later this year.This excitement has pushed stocks higher in recent months.

Bull markets do not show uniform performance numbers.The longest bull run lasted between 2009 and 2020 – nearly 4,000 calendar days – with an overall gain of more than 400%.The shortest bull run on this list, which started when the index was just 14 points, was less than two years and resulted in a 22% advance.

Despite the market’s strength, the investor has some concerns in 2024.The exact path the Federal Reserve will take to lowering interest rates, the presidential election as well as the prospect of possible weakness in U.S. consumer spending.Data released this week could go a long way toward determining which way the central bank policymakers could lean on policy.Gross domestic product will be released on Thursday and the personal consumption expenditure prices reading on inflation is out on Friday.

Don’t rule out a pullback and some choppiness in the first few months of 2024.

Earnings this week:

Nearly 70 S&P500 companies are due to report earnings this week.Among the biggest reports are Tesla, Netflix, and Intel.

Monday:United Airlines (UAL)

Tuesday: Procter & Gamble (PG), Netflix (NFLX)

Wednesday:IBM (IBM), Tesla (TSLA)

Thursday: Alaska Air Group (ALK), Intel (INTC)

Did you know _

That one of Buffett’s many investments throughout his illustrious career has included the purchase of a farm.This farm is situated around 50 miles north of Omaha and was purchased in 1986.It cost Buffett $280,000, and he estimated that the return from the farm would be about 10% owing to improved productivity and higher crop prices.Years later Buffett advises us that the farm has “tripled its earnings and is worth five times or more what I paid.” He went on to say that he still “knows nothing about farming and recently made just my second visit to the farm.”

Buffett’s lesson to followers is that what matters most to any investment is its future earnings.Another key message from this example is having a long-term horizon for investments.He advises that “when promised quick profits, respond with a quick ‘no.’”

He explains that “income from the farm will probably increase in decades to come, and the investment will be a solid holding for my lifetime, and for my children and grandchildren.”

Both Warren Buffett and Bill Gates love farmland as an investment.

In north Queensland, you can’t really swim in the ocean without a stinger suit.You don’t want to get bitten by an Irukandji jellyfish.It is a potentially deadly sting that can cause cardiac arrest in under 30 minutes.To date, in south-east Queensland, on the Gold Coast (shown above) and Sunshine Coast, we can swim in the ocean without concerns about these jellyfish.

I don’t lose money in the market very often, but when I do, I really hate it. I also take each attack of red ink as a learning opportunity. Do this for 55 years and you get pretty good at it.

So what did I learn from my ill-timed double short in the S&P 500 last week? It turns out a lot.

The stock market was in the process of backing out six Fed rate cuts this year, which was never realistic, and returning to only three, which is much more realistic. The March tightening got pushed back at least until May.

You see this in the sectors that got hammered last week, big borrowers like airlines, cruise lines, and construction. Net creditors to the financial system, i.e. big tech rose almost every day. That lasted about two days.

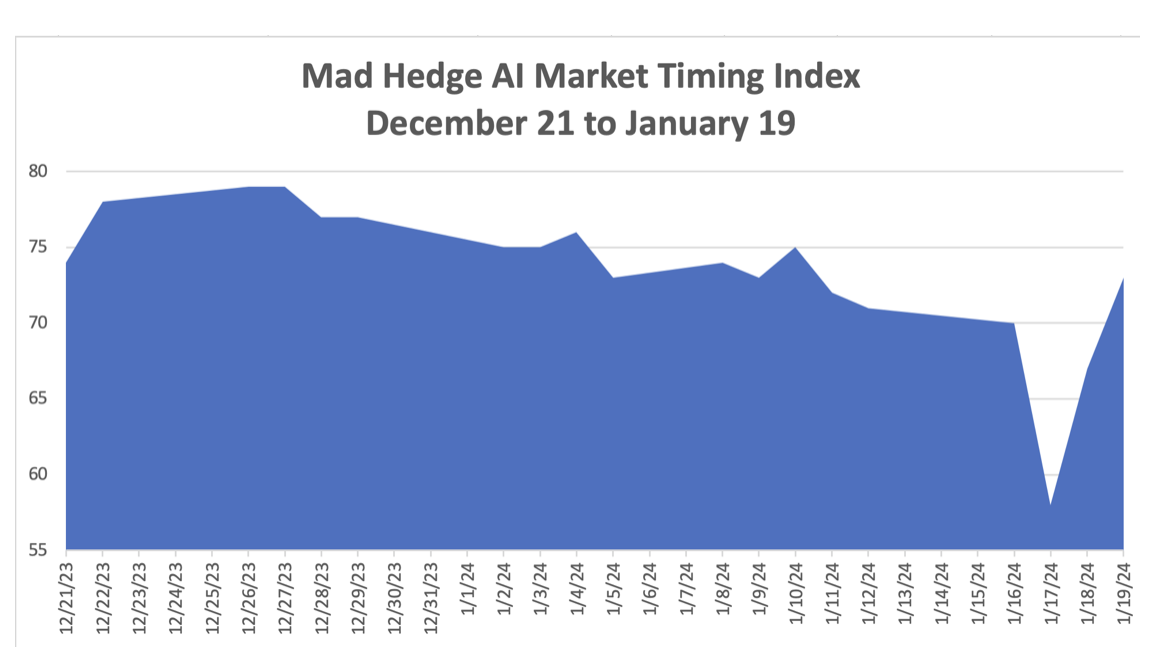

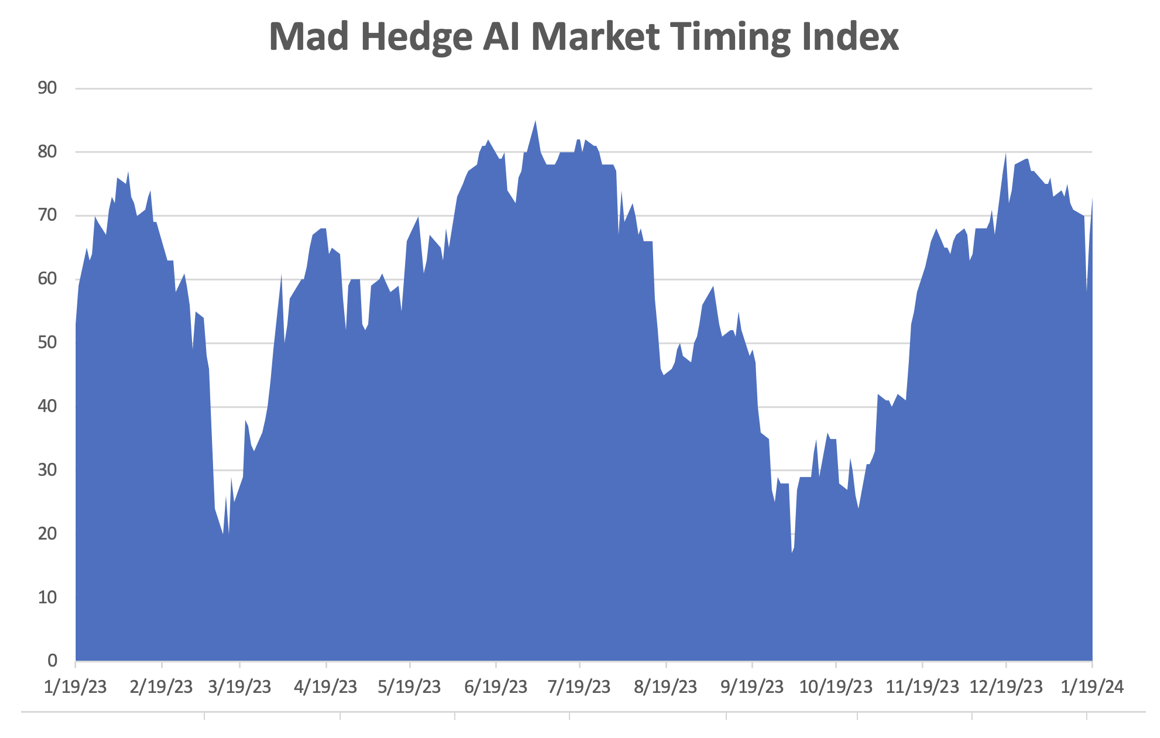

It turns out that the Mad Hedge AI Market Timing Index led me astray. I already knew that it was not perfect, but I had to be reminded from time to time of a loss. After the timing index peaked at a six-month high of 78 on December 26, it plunged all the way down to 58 on January 17, the classic sign of a market that is rolling over and dying.

So what did it do after that? A red-hot University of Michigan Consumer Sentiment Index hit an out-of-the-blue 2 1/2 year high, causing my own index to shoot up to 73. Ouch! Never underestimate the ability of the American consumer to spend money!

That triggered the mother of all short-covering rallies. It turns out that I am not the only one using an algorithm-driven market timing index these days, all of which drew the same conclusions on Wednesday and went short the (SPY). A January Friday options expiration added gasoline to the fire.

Fortunately, I had eight other long positions that will more than offset my short losses well before the February 16 option expiration in 20 trading days, such is the nature of my long/short strategy. But a hit is a hit, nonetheless.

It’s easy to get too aggressive and overconfident when you’ve had two back-to-back 80% plus years such as the case at the Mad Hedge Fund Trader. Occasionally, you have to get slapped in the face to dial it back down.

What is important here is to understand the broader message of what the market is trying to tell us. That artificial intelligence is worth far more than we understand. While the current market capitalization of the top AI leaders, (MSFT), (GOOGL), (TSLA), (META), and (NVDA) is now at $10 trillion, I bet that they will top $40 trillion in a decade. Markets are already discounting that target.

Once again that makes my own decade forecast of a Dow Average at 240,000 positively conservative.

And while NVIDIA now looks insanely expensive, with the doubling weighting I had gaining another 25% in 2024, it is in fact still the cheapest AI stock in the market. That’s because its earnings are growing far faster than its stock price….by a large margin.

It's definitely looking like a different market so far in 2024. We are going to have to work harder….and smarter.

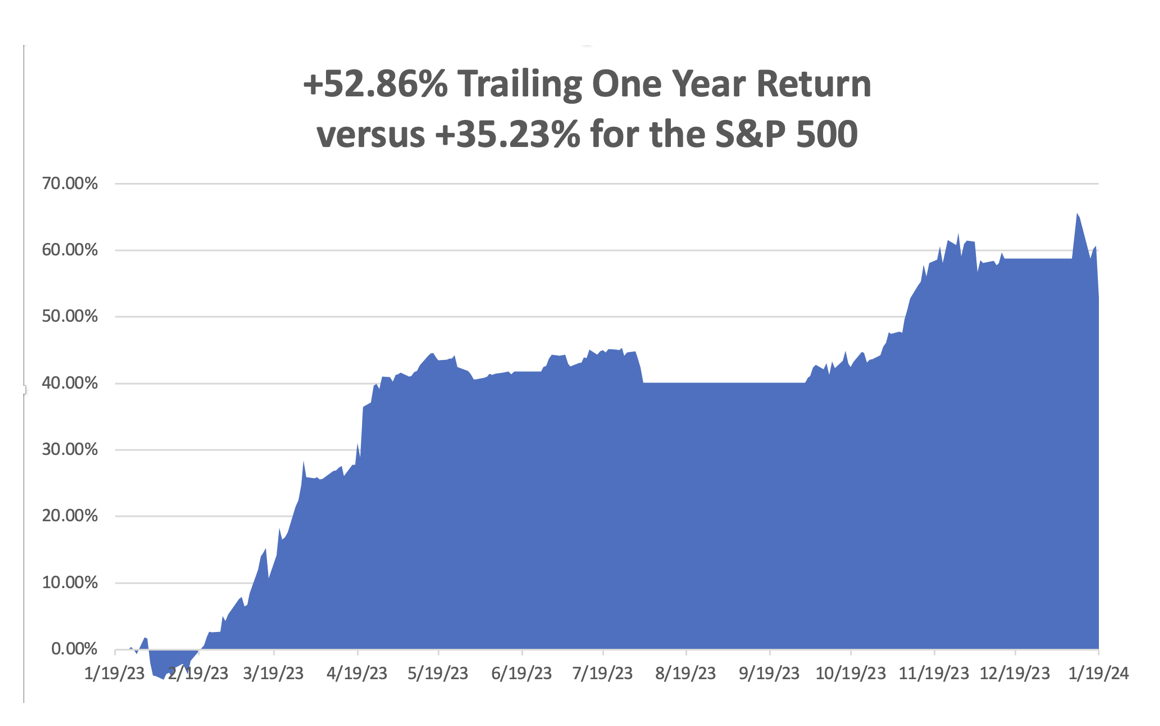

So far in January, we are down -5.89%. My 2024 year-to-date performance is also at -5.89%.The S&P 500 (SPY) is up +1.14%so far in 2024. My trailing one-year return reached +xx% versus +xx%for the S&P 500.

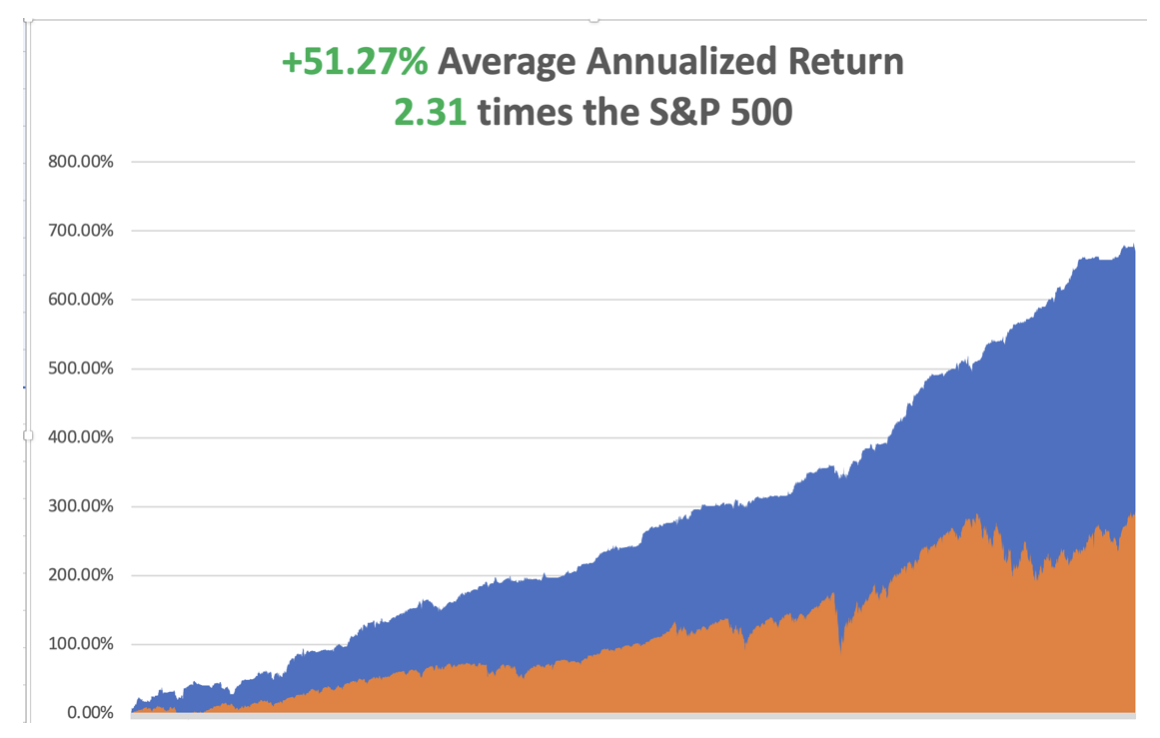

That brings my 15-year total return to +670.74%. My average annualized return has retreated to +51.27%,another new high.

Some 63 of my 70 trades last year were profitable in 2023. In 2024 100% of my trades have been profitable.

After a round of profit-taking, I am maintaining longs in (MSFT), (AMZN), (V), (PANW), (CCJ), (TLT). I am regrettably short the (SPY).

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

US Budget Funded for Two More Months, kicking the can down to March 8. Given byelections and their current death rate, Republicans may no longer have a majority by then. Those numbers include $1.59 trillion for fiscal year 2024, with $886 billion for defense spending and $704 billion in non-defense spending. Schumer and Johnson also agreed to a $69 billion side deal in adjustments that will go toward non-defense domestic spending. Not that markets care.

University of Michigan Consumer Index surged, up to 78.8 for January, its highest level since July 2021. Consumer sentiment has improved amid a drop in gasoline prices and solid stock market gains.

Building Permits Improve, at 1.50 million, up 1.9%.But the latest New Monthly Residential Construction report, released this morning jointly by the U.S. Census Bureau and the U.S. Department of Housing and Urban Development, is 7.6% above the December 2022 rate of 1.357 million. Declining mortgage rates are translating into mixed improvements in home production.

Homebuilder Sentiment Jumps, by seven points to 44, the most in nearly a year. Lower mortgage rates boosted customer traffic, sales, and the demand outlook. The US is short 10 million homes which will take a decade to build. Buy (KEN), (PHM), and (KBH) on dips. US Retail Sales Come in Best in Three Months, up 0.6% in December, as analysts continue to underestimate the American consumer. Clothing, general merchandise, and e-commerce led gains. The “soft landing” is looking like a sure thing. Buy all major dips in stocks.

Weekly Jobless Claims plunged to 187,000, a 17-month low, underlining the “soft landing” scenario. Continuing claims stand at 1.80 million. Labor strength has persisted despite attempts by the Federal Reserve to slow the economy, and the jobs market in particular, through a series of interest rate hikes. Bonds and other interest rate plays sold off on the news. On Monday, January 22, nothing of note is announced.

On Tuesday, January 23 at 8:30 AM EST,the Richmond Fed Manufacturing Shipments Index is released.

On Wednesday, January 24 at 2:00 PM, the S&P Global Flash PMI is published.

On Thursday, January 25 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Q4 US GDP first read.

On Friday, January 26 at 2:30 PM, the December Core PCE Index is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I recall my last trip around the world in 2018. I took the trip because I feared climate change would soon make visits to the equator impossible because of intolerable temperatures and the breakdown of civilization. As it turned out, the global pandemic began six months later, making such travel out of the question for two years.

I beat Phileas Fogg by 55 days, who needed 88 days to complete his trip around the world to settle a gentleman’s bet. But then he had to rely on elephants, sailing ships, and steam engines to complete his epic voyage or at least the one imagined by Jules Verne.

I actually took a much longer route, using a mix of Boeings and Airbuses to fly 80 hours over 40,000 miles on 18 flights through 12 countries in only 33 days. Incredibly, our baggage made it all the way, rather than see its contents sold on the black markets of Manila, New Delhi, or Cairo.

It was a trip around the world for the ages, made even more challenging by dragging my 13 and 15-year-old girls along with me. I have always considered my most valuable asset to be the trips I took to Europe, Africa, and Asia in 1968. The comparisons I can make today some 55 years later are nothing less than awe-inspiring.

I wanted to give the same gift to them.

It began with a 12 ½ hour flight from San Francisco to Auckland, New Zealand. Straight out of the airport I rented a left-hand drive Land Rover and drove three hours to high in the steam-covered mountains of Rarotonga where we were dinner guests of a Māori tribe. To earn my dinner of pork and vegetables cooked underground I had to dance the haka, a Māori war dance.

The Haka

Of course, with kids in tow, a natural stop was the Hobbit Village of Hobbiton 1½ hours outside of Auckland. I figured the owners of the idyllic sheep farm were earning at least $25 million a year showing tourists the movie set.

In all, I put 1,000 miles on the car in four days, even crossing New Zealand’s highest mountain range on a dirt road. The thick forests were so primeval my daughter expected to see a dinosaur around every curve. We reached our southernmost point at Mt. Ruapehu, a volcano used as the inspiration for Mt. Doom in Peter Jackson’s Lord of the Rings.

The focus of the Australia leg was ten strategy lectures which I presented around the country. I was mobbed at every stop, with turnout double what I expected. The Mad Hedge Fund Trader and the Mad Hedge Technology Letter picked up 100 new subscribers in the Land Down Under in five days.

Maybe it was something I said?

My kids’ only requirements were to feed real kangaroos and koala bears, which we duly accomplished on a freezing cold morning outside Melbourne. We also managed to squeeze in a tour of the incredible Sydney Opera House in between lectures, dashing here and there in Uber cabs.

I hosted five Mad HedgeGlobal Strategy Luncheons for existing customers in five days. The highlight was in Perth, where eight professional traders and I enjoyed a raucous, drunken meal. They had all done well off my advice, so I was popular, to say the least. Someone picked up the tab without me even noticing.

After that, it was a brief ten-hour flight to Manila in the Philippines, with a brief changeover in Hong Kong, where massive protest demonstrations were underway. Ever the history buff, I booked myself into General Douglas MacArthur’s suite at the historic Manila Hotel. The last time I was here I interviewed President Ferdinand Marcos and his lovely wife Imelda. After lunch with my enthusiastic Philippine staff, I was on my way to the airport.

I took Malaysian Airlines to New Delhi, India, which has lost two planes over the last five years and where the crew was definitely on edge. I asked why a second plane was lost somewhere over the South Indian Ocean and the universal response was that the pilot had gone insane. Security was so tight that they confiscated a bottle of Jamieson Irish Whiskey that I had just bought in duty-free.

India turned out to be a dystopian nightmare. If climate change continues this is your preview. With temperatures up to 120 degrees in 100% humidity people here dying of heat stroke by the hundreds. Elephants had to be hosed down to keep them alive. It was so hot you couldn’t stray from the air conditioning for more than an hour. The national radio warned us to stay indoors.

In Old Delhi, the kids were besieged by child beggars pawing them for food and there were mountains of trash everywhere. In the Taj Mahal, my older daughter passed out and we had to dump our remaining drinking water on her to cool her down and bring her back to life. We spent the rest of the day sightseeing indoors at the most heavily air-conditioned shops. The hand-woven Persian carpet should arrive any day now.

If global temperatures rise by just a few more degrees you’re going to lose a billion people in India very soon.

On the way to Abu Dhabi were flew directly over the tanker war at the Straits of Hormuz, one of my old flight paths during my Morgan Stanley days. It was too dusty to see any action there. We got a much better view of Sinai and the Red Sea, which, I told the kids, Moses parted 5,000 years ago (they’ve seen Charlton Heston in The Ten Commandments many times).

Upon landing at Cairo, Egypt’s ever-vigilant military intelligence service immediately picked me up. Apparently, I was still in their system dating back to my coverage of Henry Kissinger’s shuttle diplomacy for The Economist in 1976. That was all a long time ago. Having two kids with me meant I was not there to cause trouble, so they were very friendly. They even gave us a free ride to the downtown Nile Hilton.

After India, Cairo, and the Sahara Desert were downright pleasant, a dry and comfortable 100 degrees. We did the standard circuit, the pyramids, and the Sphynx followed by a camel ride into the desert.

If you are the least bit claustrophobic don’t even think about crawling into the center of the Great Pyramid on your hands and knees as we did. I was sore for two days. We spent the evening on a Nile dinner cruise, looking for alligators, entertained by an unusually talented belly dancer.

The next stage involved a one-day race to Greece, where we circled the Acropolis in all its glory, and then argued with a Greek taxi driver on how to get back to the airport. We ended up taking an efficient airport train, a remnant of the 2000 Athens Olympics. If impoverished and bankrupt Athens has such a great airport train, why doesn’t New York or San Francisco?

It was a quick hop across the Adriatic to Venice, Italy, where we caught an always exciting speed boat from the Marco Polo to our Airbnb near St. Mark’s Square. We ran through the ancient cathedral and the Palace of the Doges, admiring the massive canvases, the medieval weaponry, and of course, the dungeon.

One of the high points of the trip was a performance of Vivaldi’s Four Seasons in the very church it was composed for. A ferocious thunderstorm hit, flooding the plaza outside and causing the lead violinist’s string to break, halting the concert (rapid humidity change I guess).

When we got home with soggy feet, the Carabinieri had cordoned off our block with police tape because a big chunk of our 400-year-old roof had fallen into the street. It taxed my Italian to the max to get into our apartment that night. The Airbnb host asked me not to mention this in my review (I didn’t).

The next day brought a circuitous trip to Budapest via Brussels. Budapest was a charm, a former capital of the Austria-Hungarian Empire, and the architecture to prove it. The last time I was here 55 years ago the Russian Army was running the place and it was grim, oppressive, and dirty.

Today, it is a thriving hot spot for Europe’s young, with bars and nightclubs everywhere. Dinners dropped from $150 in Venice to $30. We topped the night with a Danube dinner cruise with a folk dancing troupe. I’m told you can live there like a king for $1,000 a month.

Visiting the Golden Age in Budapest

The next morning we drew closer to our final destination of Switzerland. A four-hour train ride brought us to my summer chalet in Zermatt and some much-needed rest. At the end of a long valley and lacking any cars, Zermatt is one of those places where you can just give the kids 50 Swiss francs and tell them to get lost. I spent mornings hiking up from the valley floor and afternoons getting caught up on the markets and my writing.

There’s nothing like recharging my batteries in the clean mountain air of the Alps. The forecast was rain every day for two weeks, but it never showed. As a result, I ended up hiking ten miles a day to the point where my legs were made of lead by the end.

The only downer was watching helicopters pick up the bodies of two climbers who fell near the top of the Matterhorn. As temperatures rise rapidly the ice holding the mountain together is melting, leading to a rising tide of fatal accidents.

I caught my last flight home from Milan. Anything for one more great dinner in Italy, which I enjoyed in the Galleria. At the train station, I chatted with a troop of Italian Boy Scouts in blue uniforms headed for the Italian Alps. The city was packed with Chinese tour groups, and there was a one-month wait to buy tickets for Leonardo DaVinci’s The Last Supper. Another Airbnb made sure I stayed up all night listening to the city’s yellow trolleys trundle by.

Finally, an 11-hour flight brought me back to the City by the Bay. Thanks to two sleeping pills of indeterminate origin I went to sleep over England and woke up over Oregon, preparing for a landing. It seems that somewhere along the way I proposed marriage to the Arab woman sitting next to me, but I have no memory of that whatsoever. At least that’s what the head flight attendant thought.

I am now planning this summer’s trip. After the Queen Mary and the Orient Express should I climb the Matterhorn again? Or should I summit Mount Kilimanjaro in Africa first? No transatlantic trip should ever be wasted. And I have to get home in time to join a 50-mile hike with the Boy Scouts in New Mexico and then cart two kids off to college.

What a great problem to have.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/01/JOhn-thomas-mountain.png8121080april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-01-22 09:02:572024-01-22 12:59:41The Market Outlook for the Week Ahead or Learning from Your Losers

At CES 2024, artificial intelligence (AI) was not just part of the buzz; it was the pulsating heart of the entire show.

This event wasn't your typical tech fest. It was like stepping into a future crafted by AI. The future looked so vivid and real that, even I, usually a skeptic, found myself drawn in.

Starting with NuraLogix's (NURX) Anura MagicMirror, which is no ordinary mirror.

Imagine a mirror that doesn't just reflect your image but also divulges your health secrets. This groundbreaking tech can analyze facial blood flow to check vitals like blood pressure and heart disease risk. Currently eyed for gyms and clinics, it signifies AI's expanding role in health diagnostics.

Needless to say, the potential here is staggering. The AI healthcare market is expected to reach $173.55 billion by 2029, growing at an annual rate of 40.2%.

The RPM segment, where MagicMirror could be a star, is looking at a neat $4.3 billion by 2027. The idea of a mirror giving you health updates in your home or a quick health check at an airport kiosk isn't just convenient; it's revolutionary.

In this burgeoning field, companies like Empatica Inc. are carving out a niche with wristbands and smartwatches that use AI to track everything from sleep to stress and medical conditions such as epilepsy.

iRhythm Technologies (IRTC) also steps up with their Zio Patch, an AI-enabled wearable patch for monitoring heart rhythms, while Bio-Rad Laboratories (BIO) brings clinical research and medical diagnostics into the future with AI-driven tools for analyzing physiological data.

Meanwhile, giants like Apple (AAPL) are integrating AI into their Watch Series for health monitoring, Johnson & Johnson (JNJ) is diving into AI for medical imaging and personalized medicine, and Alphabet Inc.'s (GOOGL) Google Health subsidiary Verily is pushing the boundaries with wearables and data analysis for disease detection.

From health, we drift into the world of sleep with China’s DeRucci's smart mattress and anti-snore pillow. This isn't just about sleeping well; it's about sleeping smart.

The mattress is embedded with 23 sensors that adapt to every little whim of your body – temperature, position, heart rate – ensuring optimal support.

And the pillow? It claims to reduce snoring by up to 89%. But good things come with a price – the pillow and mattress together could set you back about nine grand.

Yet, given that the global sleep tech market is a giant, estimated at $55 billion in 2023 and expected to balloon over $130 billion by 2030, DeRucci is onto something big.

The smart mattress sector is projected to hit $3.2 billion by 2026, and the anti-snoring device market is expected to reach $600 million by 2028. This is a market that's not just about comfort; it's about health and technology intertwining to improve quality of life.

From the bedroom, we move to personal computing with HP's (HPQ) Spectre x360 14. Here's where AI meets everyday technology, transforming our mundane tasks into something extraordinary.

Equipped with Intel's (INTC) latest processors, complete with a neural processing unit, this laptop is not just a gadget; it's a glimpse into the future of AI-infused computing.

Keep in mind that the AI consumer electronics market is huge. It's projected to reach $71.8 billion by 2027, growing at a strong 20.4% CAGR.

Within this, AI-driven laptops and PCs are set to grow at a dizzying 25.2% CAGR. HP, with its Spectre x360 14, is not just riding the wave; it's helping create it.

This fusion of AI into our everyday devices seamlessly bridges into another intriguing aspect of AI’s growing footprint: the entertainment industry. The intersection of AI and voice acting, highlighted by the SAG-AFTRA and Replica Studios agreement, brings a new dimension to AI's expanding influence.

This recent agreement is a milestone. It ensures voice actors are compensated for AI replicas of their voices in video games. It's a significant step in balancing technological advancement with performer rights.

Companies like Veritone (VERI), Resemble AI, and Super AI are leading this charge. Veritone is a titan in AI media, managing large-scale audio and video content across various sectors. Resemble AI is making strides with AI voice cloning and deepfakes, while Super AI is focused on emotional AI, striving to capture not just the sound but the essence of human speech.

This quest to humanize technology is a testament to how AI is not just imitating life but becoming an integral part of it.

Speaking of integration, let's pivot to Google's vision for AI in smartphones, echoed by giants like Apple and Samsung. It's not just about smart features; it's about transforming the core of how phones operate.

With powerful processors like Google's Tensor and Qualcomm's (QCOMM) Snapdragon 8 Gen 3, smartphones are evolving into something more powerful and intuitive.

The AI consumer electronics market predicted to exceed $150 billion by 2026, with smartphones as a driving force, is unassailable proof of the potential of Google's AI strategy.

But AI's influence doesn't stop at gadgets and health; it extends to our furry friends too. The Oro Dog Companion Robot is a perfect example of AI's foray into pet care.

Equipped with features like two-way audio, video, treat dispensers, and a ball thrower, it's designed to be a pet's new best friend.

The pet care industry is booming, expected to hit $305.1 billion by 2030, with smart pet products like the Oro Robot eyeing a $19.8 billion market by 2025. So far, companies like Chewy (CHWY), iRobot (IRBT), and PetIQ (PETQ) are key players in this emerging market.

Shifting gears from our furry friends to the automotive world, Volkswagen's integration of ChatGPT into its EV lineup marks a bold move in AI application in vehicles. This isn't just about adding a feature; it's about redefining the driving experience.

The global AI automotive market is estimated to reach $26.88 billion by 2027, with voice assistants, autonomous driving, and personalized experiences leading the charge. Aside from Volkswagen, Tesla (TSLA), Ford (F), and General Motors (GM) are already making significant strides in this field.

Overall, AI at CES 2024 was more than a series of exhibits; it was a vivid demonstration of how AI is reshaping our world – from health and pet care to smartphones and cars. As we stand at the threshold of this AI revolution, it's clear that we're just beginning to uncover its potential. The future is AI, and it's a future that's here to stay.

https://www.madhedgefundtrader.com/wp-content/uploads/2024/01/Screenshot-2024-01-19-162432.jpg667664Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2024-01-19 16:25:552024-01-19 16:25:55SIRI, MEET YOUR COUSINS

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.