(CEOs ARE SELLING INTO THIS MARKET RALLY – IS SOMETHING BREWING…?)

March 27, 2024

Hello everyone,

Insiders are selling the market rally.

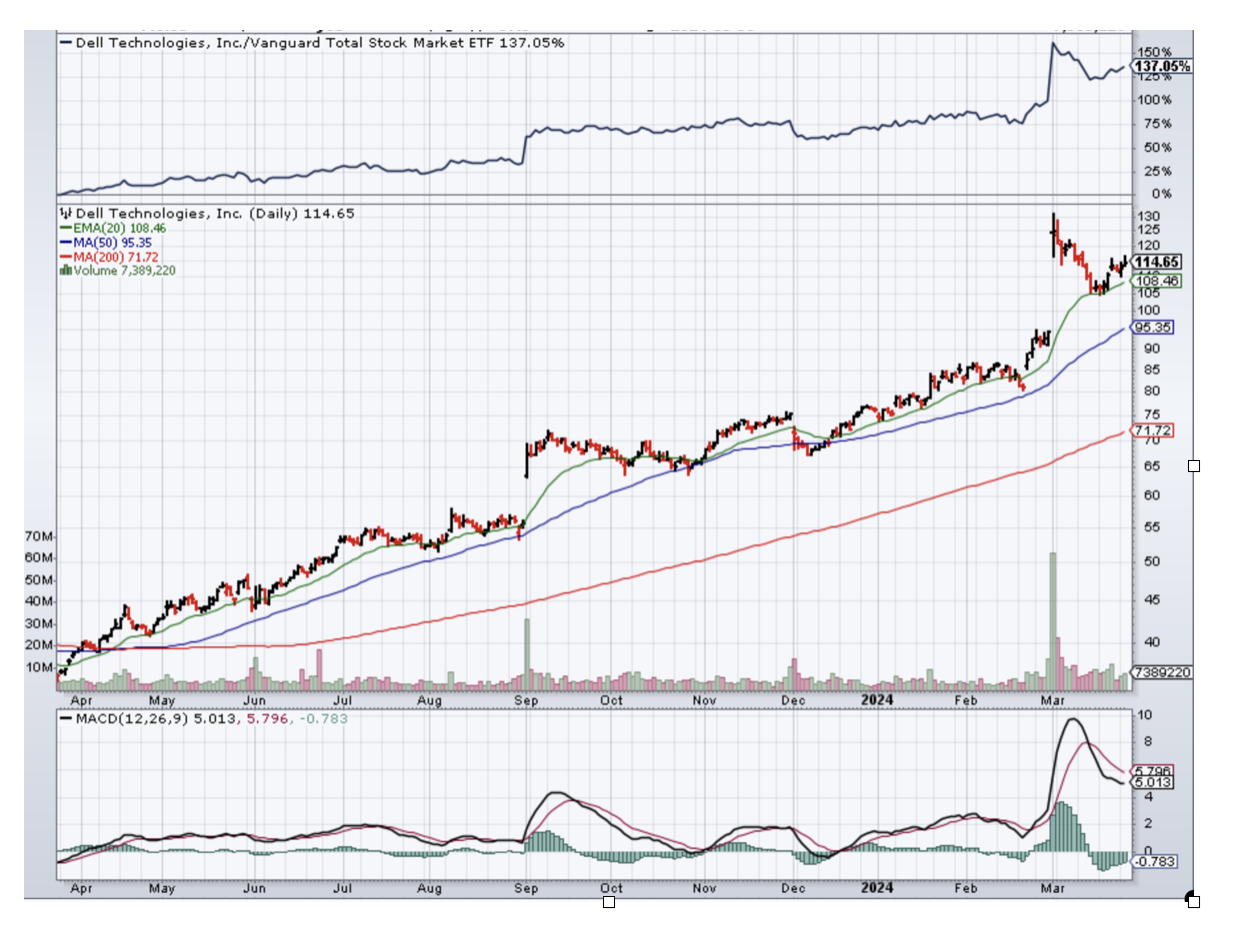

CEOs of technology companies and other firms have been cashing in on this market rally, including a massive sale last week from Michael Dell, founder and CEO of Dell Technologies.

Dell, who took his namesake company public for a second time in 2018, racked up $468 million in stock sales over the past week, according to securities filings and Verity Data.Those moves bring Dell’s total sales this month to nearly $800 million.

If you look at Dell’s stock chart it appears to have topped out, at least in the short term.Shares of Dell are up 200% over the past year, but the stock has fallen over the past three weeks.

Mark Zuckerberg has also been selling off stock.Securities filings and Verity Data show that roughly $114 million has been sold of late.

It seems that Zuckerberg’s moves were done as part of a 105b-1 plan, which is a document filed with the Securities and Exchange Commission to schedule stock sales for executives.His sales also came from several entities, including the Chan Zuckerberg Initiative, a charitable foundation Zuckerberg runs with his wife, Priscilla Chan.

Like Dell, Zuckerberg’s sales come after a massive run-up for his stock.Shares of the company formerly known as Facebook are up more than 40% year to date.

CEOs in the following companies have sold off significant parcels of stocks.

Cadre Holdings - $50.3 million

Arista Networks - $40.9 million

Ares Management - $32.7 million

Gitlab - $16.5 million

Cadence Design Systems - $14.7 million

AppLovin - $9.5 million

Cleanspark - $9 million

As I have been saying, it’s always good to have insurance on your portfolio, and taking some profits is always a good idea.

Is a Boeing turnaround expected soon?

The shake-up at Boeing this week with the CEO set to step down by year-end may have sparked optimism among investors.Boeing has faced significant challenges over the years with the latest incident involving a door plug on an Alaska Airlines 737 Max 9 in January.Numerous groundings and substantial financial losses have come as a result.The stock is down by more than 27% since the start of the year.

The chart of Boeing above shows basically a double bottom.Instead of buying the stock outright, we could purchase a bull call spread to lessen the risk.For a short-term spread trade, you could buy a $190 call and sell a $195 call with an expiration on April 19.If BA trades at or above 195 by the expiration date, this trade could yield a good return.

To get creative with your trades, either change the strikes or change the expiration.If you place your strikes toward $200 you are being more aggressive.If you place your strikes underneath the stock price, (in the money), you are being more conservative.

Tesla is out of favour.

Bernstein has cut its Tesla’s price target from $150 to $120, citing growing demand constraints.The new forecast implies a downside of 30% over the next 12 months.

This quarter to date, Tesla has experienced soft China/Europe demand and constrained US Model 3 production. Bernstein expects lukewarm growth in 2024, as well as 2025, bringing into question the company’s growth narrative.Tesla has lost 30.5% in 2024, making it the worst-performing S&P 500 stock.

With US deficits exploding, the National Debt racing towards $35 trillion, and the velocity of money (or the turnover) ticking up, one particularly industry is suddenly doing particularly well.

Business is fantastic at the money printers. The only problem is that there is no way you can participate in this boom as an individual investor, unless you want to marry into a certain family.

All of the high-grade paper used by the US Treasury to print money is bought from a single firm, Crane & Co., which has been in the same family for seven generations.

Last year, the Feds printed 38 million banknotes worth $639 million. Although they briefly saw the Great Recession cause the velocity of money to decline, recent hyper reflationary efforts have spurred a big increase in demand for paper for $100 dollar bills.

The US Treasury first issued paper money in 1861 to help finance the Civil War, and Crane has been supplying them since 1879.

The average life of a dollar bill is 21 months. M1, or notes and coins in circulation, is already exploding. Is this a warning of an imminent jump in inflation? It could be.

In the meantime, check out the new 3D $100 bill. It includes the latest anti-counterfeiting techniques, like a new blue security strip, tiny liberty bells that morph into the number 100, and “United States of America” micro printed on Franklin’s jacket collar.

The new bills started entering circulation in 2013 to frustrate industrial scale North Korean counterfeiting efforts.

No matter what efforts the US Treasury undertakes to keep this 19th century form of exchange alive, its days may be numbered. It is just a matter of time before blockchain technology replaces the greenback with all digital, and unprintable currencies. I hope the Crane family has a nice retirement nest egg.

It’s ironic that the balanced scales on the dollar, a symbolic reference to the founding fathers’ commitment to maintaining a balanced budget, are still on the new Benjamin.

Old Ben must be turning over in his grave.

Out With the Old

In With the New

https://www.madhedgefundtrader.com/wp-content/uploads/2024/03/new-dollar.png352796april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-27 09:04:282024-03-27 15:14:50Why Business is Booming at the Money Printers

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

You've likely witnessed a scene like this: You're at the park, and you see a young couple playing fetch with their golden retriever.

The dog is absolutely loving life, jumping and bounding after the ball, tail wagging furiously. It's a heartwarming scene, and it's one that's becoming more and more common these days.

In fact, just the other day, over coffee, a veterinarian buddy of mine spilled the beans.

"You wouldn't believe how people are pampering their pets these days," she said, shaking her head in amusement. "It's no longer just about the basics—food and health. Nope, we're talking top-tier, VIP treatment. They're ready to drop serious cash to ensure their furry friends are living their best lives."

It's a whole new world for pets, and their owners are leading the charge, wallets wide open.

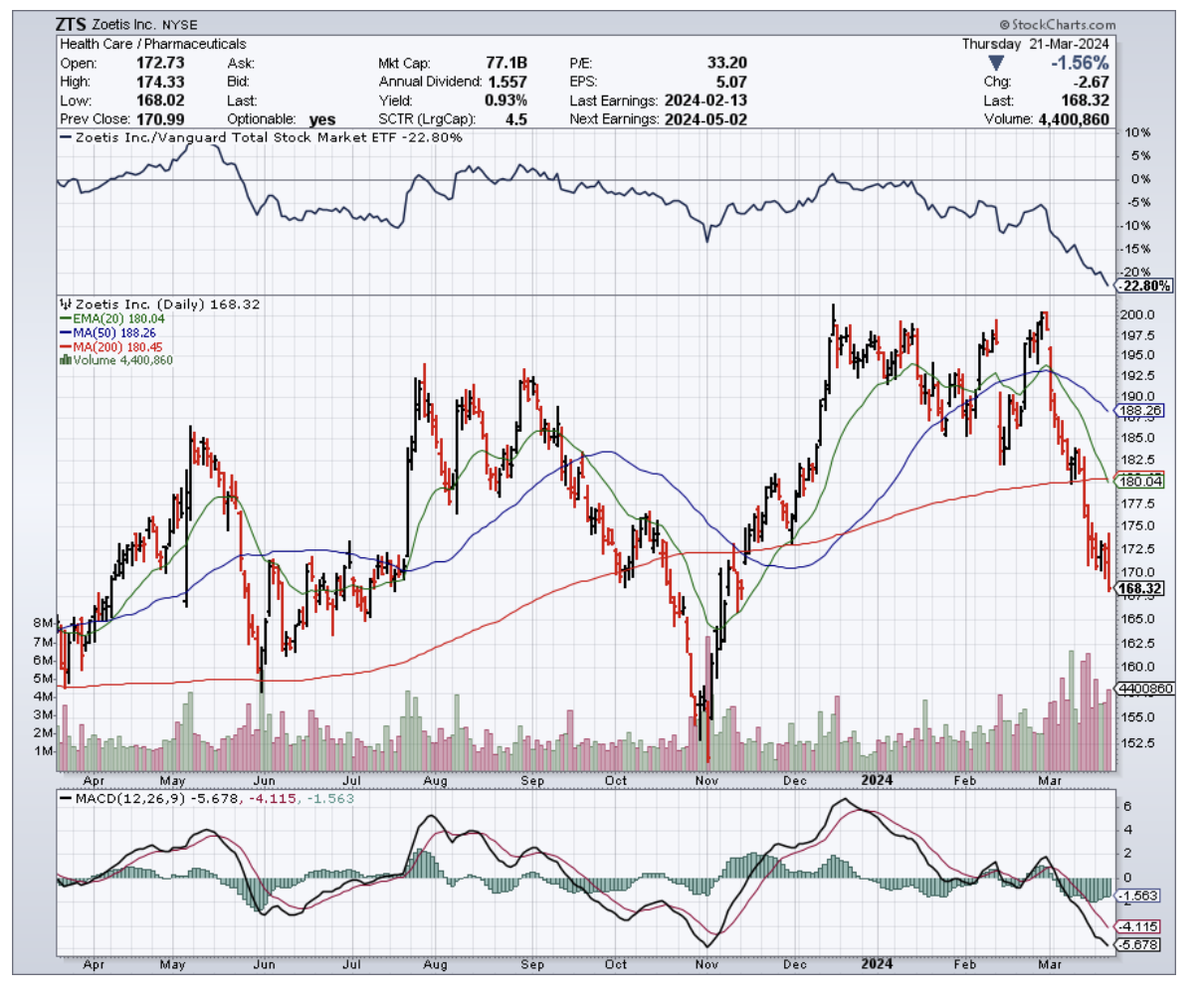

And that is where Zoetis (ZTS) comes in. This company is the top dog (pun intended) in the animal healthcare space, and it's been making some serious waves in the market lately.

Now, I know what you're thinking - "What about those big-shot human healthcare stocks like Amgen (AMGN), Johnson & Johnson (JNJ), and Pfizer (PFE)?"

Well, let me tell you, Zoetis has been giving them a run for their money since spinning off from Pfizer back in 2013. This company has been posting positive annual EPS growth every single year, with an average annual EPS growth rate of a whopping 15.9%.

But that's not all — Zoetis has also been dishing out some seriously impressive dividend growth, with a CAGR of nearly 25% since it was spun off. That's right, this stock is checking all the boxes for dividend growth investors.

And if you think this is just an income play, think again.

Zoetis has been absolutely crushing the S&P 500, posting price returns of 492% compared to the market's measly 176% gains over the last decade.

So, what's the secret behind Zoetis' success?

Well, it all comes down to our furry (and sometimes scaly) friends. You see, people are lonelier than ever these days, and they're turning to pets for that much-needed companionship.

The US Surgeon General even called loneliness an epidemic, sounding the alarm on its dire impacts on health, likening its risks to smoking up to 15 cigarettes a day.

From the gripping claws of loneliness among young adults to the isolation felt by mothers with young children, the pandemic has only deepened this crisis, affecting a staggering 36% of Americans.

More than that, this loneliness trend isn't just about having a buddy to binge-watch Netflix (NFLX) with. It's actually impacting our species' survival. Studies show that sexual activity is on the decline, and technology is distorting the way we interact with each other.

It's a bit of a downer, I know, but here's where Zoetis shines through. As people turn to pets for love and affection, they're also shelling out some serious cash to keep their furry friends healthy and happy.

The American Pet Products Association says that nearly 87 million U.S. households own pets (roughly 66%), and it's not just the younger generations who are getting in on the action. Baby Boomers and Gen Xers are also big-time pet owners.

What does all this pet love mean for the industry? Well, the pet industry is expected to be a $150 billion behemoth in 2024.

Now, what really sets Zoetis apart from the pack? It all comes down to pricing power and growth potential.

In the animal health market, drug prices aren't determined by pesky regulations, government buyers, or PBMs. That means Zoetis can charge premium prices for their trusted, name-brand drugs without having to jump through hoops.

Plus, with less competition in the animal health space, Zoetis' products have longer growth runways and aren't constantly battling generic copycats.

For context, Elanco (ELAN), Zoetis' pure-play competitor, only managed to bring in $4.4 billion in sales.

So, what's the bottom line here?

Zoetis is a best-in-breed play on the booming animal healthcare market, with a safe and growing dividend to boot. As this sell-off continues, Zoetis keeps climbing higher on my personal watch list. I'm ready to back up the truck and load up on shares come April when I put my March dividends to work.

If you're looking for a unique way to play the healthcare space with a company that's got plenty of bark and bite, Zoetis might just be the stock for you.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-26 12:00:242024-03-26 12:53:40The Top Dog In Animal Healthcare

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

Malls are dying. Commerce is moving online at a breakneck pace. Investing in retail is a death wish.

No less a figure than Bill Gates, Sr. told me before he died that in a decade, malls would only be inhabited by climbing walls and paintball courses, and that was a decade ago.

Except it didn’t quite work out that way. Lesser quality malls are playing out Mr. Gates’ dire forecast. But others are booming. It turns out that there are malls, and then there are malls.

Let me expand a bit on my thesis.

We are just entering a decade-long decline in interest rates, probably starting in June. Malls are highly leveraged entities that often are financed by Real Estate Investment Trusts) REITS. That makes some mall-based REITS some of the most attractive investments in the market.

Technology is moving forward at an exponential rate. As a result, product performances are improving dramatically, while costs are falling. Commodity and energy prices are also rising, they are but a tiny fraction of the cost of production.

In other words, DEFLATION IS HERE TO STAY!

The nearest hint of real inflation won’t arrive until the late 2020s, when Millennials become big spenders, driving up the cost of everything.

So, let's go back to the REIT thing. Real Estate Investment Trusts are a creation of the Internal Revenue Code, which gives preferential tax treatment for investment in malls and other income-generating properties.

There are 1,100 malls in the United States. Some 464 of these are rated as B+ or better and are concentrated in the biggest spending parts of the country (San Francisco, North New Jersey, Greenwich, CT, etc).

Trading and investing for a half-century, I have noticed that most managers are backward-looking, betting that existing trends will continue forever. As a result, their returns are mediocre at best and terrible at worst.

Truly brilliant managers make big bets on what is going to happen next. They are constantly on the lookout for trend reversals, new technologies, and epochal structural changes to our rapidly evolving modern economy.

I am one of those kinds of managers.

These are not your father’s malls. It turns out the best quality malls are booming, while second and third-tier ones are dying the slow painful death that Mr. Gates outlined.

It is all a reflection of the ongoing American concentration of wealth at the top. If you are selling to the top 1% of wealth owners in the country, business is great. If fact, if you cater even to the top 20%, things are pretty damn fine.

You can see this in the top income-producing tenants in the “class A” malls. In 2000, they comprised J.C. Penney. Sears, and Victoria’s Secret. Now Apple, L Brands, and Foot Locker are sought-after renters. Put an Apple store in a mall, and it is golden.

And what about that online thing?

After 25 years of online commerce, the business has become so cutthroat and competitive that profit margins have been beaten to death. You can bleed yourself white watching Google AdWords empty out your bank account. I know, because I’ve tried it.

Many online-only businesses are now losing money, desperately searching for that perfect algorithm that will bail them out, going head-to-head against the geniuses at Amazon.

I open my email account every morning and find hundreds of solicitations for everything from discount deals on 7 For All Mankind jeans, to the new hot day trading newsletter, to the latest male enhancement vitamins (although why they think I need the latter is beyond me).

Needless to say, it is tough to get noticed in such an environment.

It turns out that the most successful consumer products these days have a very attractive tactile and physical element to them. Look no further than Apple products, which are sleek, smooth, and have an almost sexual attraction to them.

I know Steve Jobs drove his team relentlessly to achieve exactly this effect. No surprise then that Apple is the most successful company in history and can pay astronomical rents for the most prime of prime retail spaces.

It turns out that “Clicks to Bricks” is becoming a dominant business strategy. A combination of the two is presently generating the highest returns on investment in retail today.

People start out by finding a product online and then going to the local mall to try it on, touch it, and feel it. Apple does this.

Research shows that two-thirds of Millennials prefer buying their clothes and shoes at malls. Once there, the probability of a serendipitous purchase is far greater than online, anywhere from 20% to 60% of the time.

This explains why pure online businesses by the hundreds are rushing to get a foothold in the highest-end malls.

Immediate contact with a physical customer gives retailers a big advantage, gaining them the market intelligence they need to stay ahead of the pack. In “fast fashion” retailers like H&M and Uniqlo, which turn over their inventories every two weeks, this is a really big deal.

There’s more to the story. Malls are not just shopping centers they have become entertainment destinations as well. With an ever-increasing share of the population chained to their computers all day, the demand for a full out-of-the-house shopping, dining, and entertainment family experience is rising.

Notice how Merry Go Rounds have started popping up at the best properties? Imax Theaters are spreading like wildfire. And yes, they have climbing walls too. I haven’t seen any paintball courses yet, but the guns and accessories are for sale.

And notice that theaters are now installing first-class adjustable heated seats and will serve you dinner while the movie is playing. (Warning: if you eat in the dark, you will end up wearing half of it home).

This is why all of the highest-rated malls in the country are effectively full. If you want space, there you have to wait in line. REIT managers pray for tenant bankruptcies so that can jack up rents on the next incoming client or pivot their strategy towards the newest retail niche.

Malls are also in the sweet spot in the alternative energy game. Lots of floor space means plenty of roof space. That means they can cash in on the 30% federal investment tax credit for solar roof installations. Some malls in sunny southwestern states are net power generators, effectively turning them into min local power utilities. By the way, the cost of solar has recently crashed.

Fortunately for us investors, we are spoiled for choice in the number of securities we can consider, most which can now be bought for bargain basement prices. Many have a return on investment of 9-11%, a portion of which is passed on to the end investor.

There are now 25 REITs in the S&P 500. The sector has become so important that the ratings firm is about to create a separate REIT subsector within the index.

According to NAREIT.com (click here for the link), these are some of the largest mall-related investment vehicles in the country.

Simon Growth Property (SPG) is the largest REIT in the country, with 241 million square feet in the US and Asia. It is a fully integrated real estate company that operates from five retail real estate platforms: regional malls, Premium Outlet Centers, The Mills, community/lifestyle centers, and international properties. It pays a 4.88% dividend.

Macerich Co. (MAC) is a California-based company that is the third largest REIT operator in the country. It has been growing through acquisitions for the past decade. It pays a 5.31% dividend.

Mind you, REITs are not exactly risk-free investments. To get the high returns you take on more risk. We remember how disastrously the sector did when the credit crunch hit during the 2009 financial crisis. Many went under, while others escaped by the skin of their teeth.

There are a few things that can go wrong with malls. Local economies can die, as it did in Detroit. Populations age, shifting them out of a big spending age group. And tax breaks can be here today and gone tomorrow.

These are all highly leveraged companies, so any prolonged rise in interest rates could be damaging. But as I pointed out below, there is little chance of that in the near future.

The bottom line here is that we are seeing anything but the death of the mall. It just depends on the mall.

All in all, if you are looking for income and yield, which everyone on the planet is currently pursuing, then picking up some REITs could be one of your best calls of the year.

See You At the Mall

https://www.madhedgefundtrader.com/wp-content/uploads/2016/04/Mall-e1461879279977.jpg303400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2024-03-26 09:04:412024-03-26 12:20:27The Death of the Mall

I know it’s been two years since the US dumped its reflationary policy of quantitative easing. However, Japan and Europe are still pursuing it with a vengeance. So, it’s best to be familiar with what it is. For a quick tutorial please watch this highly insightful and humorous video.

Click on the link below to watch a six-minute animation explaining quantitative easing to a 12-year-old, using cute little cuddly figures. Was Ben Bernanke a plumber who was called to fix a pipe only to break it more? Does he have a cute beard? Is he trying to blow up the entire world economy?

Since the video has gone viral, some 5.7 million viewers found out by watching by clicking here.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/09/QE-Explained-youtube.jpg334443Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-03-26 09:02:382024-03-26 12:20:05Quantitative Easing Explained to a Twelve Year Old

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.