Mad Hedge Technology Letter

August 30, 2024

Fiat Lux

Featured Trade:

(AI SQUEEZES OUT TECH WORK FORCE)

(AI), (NVDA)

Mad Hedge Technology Letter

August 30, 2024

Fiat Lux

Featured Trade:

(AI SQUEEZES OUT TECH WORK FORCE)

(AI), (NVDA)

Don’t be in denial about artificial intelligence.

The more you fight it – it will fight you back.

It is coming for us and you need to adjust your life accordingly.

That is largely the message I want to convey to readers because the existence of tech companies and how they function has never been changing at such warp speed until today.

Instead of getting all worked up about the hoopla of what it will bring like it is some shiny new Porsche in the garage, we need to get into the weeds to see how it will manifest itself inside the real world.

While the rest of the world still has no idea what artificial intelligence is, tech workers in the Philippines are already living and breathing the new reality every day for better or worse.

The spoiler here is that it is mostly bad for the local workforce in the beautiful island and sovereign nation of the Philippines but positive for the bottom line.

It’s not a shocker that foreign companies don’t like to pay high wages and will even skirt around the low-wage area if they have their way.

Until today, tech workers in the likes of Moldova, Montenegro, and the Philippines were irreplaceable because they represented good value for labor.

Now these workers are getting crushed by the dreaded AI substitute software.

All of the major players in its vast outsourcing industry, which is forecast to cross $38 billion in revenue this year, are rushing to roll out AI tools to stay competitive and defend their business models.

Over the past eight or nine months, most have introduced some form of AI “copilot.” These algorithms mainly work alongside human operators.

Avasant, an outsourcing advisory firm that works extensively in the Philippines, estimates that up to 300,000 business process outsourcing (BPO) jobs could be lost in the country to AI in the next five years.

In February, payments company Klarna Bank announced AI bots were conducting two-thirds of all customer service interactions, equaling the work of 700 full-time agents.

Readers cannot fall asleep at the wheel by downplaying this transition in the business model of tech companies.

This movement to bots has the potential to save many percentage points of expenses on labor.

I don’t know any CEO who is actively ignoring this hard pivot to software.

For every success story, there will also be failures because let's get this straight, not every CEO or COO knows how to implement and harness the powers of AI.

Not all managers are created equally.

I know it sounds cliché to look at big tech but they are the powerbrokers of the AI industry and unsurprisingly are the ones pouring the most capital into this new technology.

The end results are that only a handful of companies will secure the bounty of profits that AI will deliver.

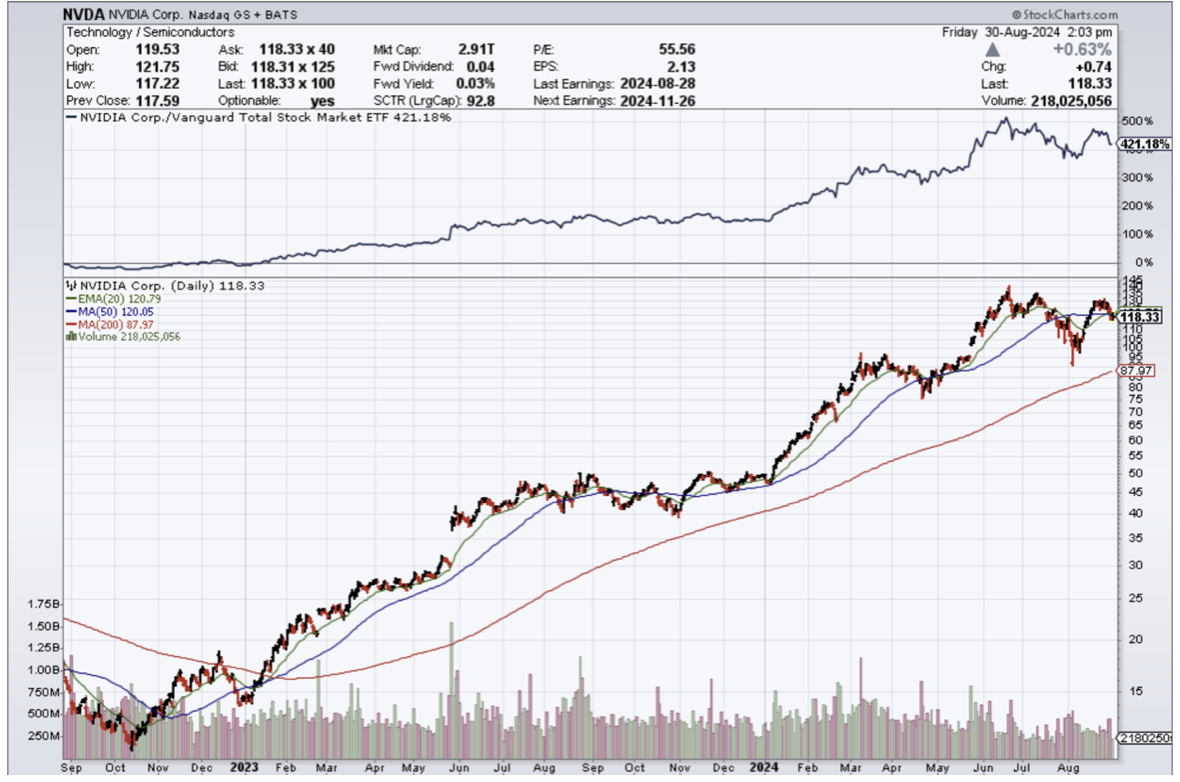

There will be surprises on the way but Nvidia relaying to investors that the AI narrative is still here is just as important as management talking about how great AI is.

The only caveat I would say is that the honeymoon phase of AI is definitely coming to a close.

Now the real tough sledding starts ahead of us.

For the time being, pick up shares in Nvidia on this nice dip.

(SUMMARY OF JOHN’S AUGUST 28, 2024, WEBINAR)

August 30, 2024

Hello everyone.

TITLE: Waiting for the Other Shoe to Fall

TRADE ALERT PERFORMANCE

August: +3.56% MTD

Average annualized return: +51.62%

Trailing one Year Return: +52.25%

Since inception: +710.24%

PORTFOLIO REVIEW

Risk Off

(TSLA) 9/$250-$260 put spread 10%

THE METHOD TO MY MADNESS

Markets are going into the worst month of the year overbought and begging for a correction.

September 18 interest rate cut now a sure thing, says John, but how much good news is already priced in?

A lot will depend on NVDA earnings out after the close today.

The next selloff is one you buy into.

US dollar is trash and could stay weak for years.

Technology stocks will recover after a much-needed correction.

Energy gets dumped on recession fears if the Fed acts too slowly.

Buy stocks and bonds on dips, but now it’s ALL sectors.

THE GLOBAL ECONOMY – NEW STIMULUS

Jay Powell says the “time to adjust policy is here.

Where did the 818,000 jobs go? Monthly job gains fell from 250,000 to 175,000. Is the message that the Fed waited too long to cut rates?

Goldman Sachs cuts recession risk to 20%

Consumer sentiment drops, to an eight-month low.

Price Index is a snore, at 0.2% MOM and 2.9% YOY.

US Producer Price Index fades, coming in at a weak 0.1%.

China Loan demand hits 15-year low.

UK grows by 0.6% in Q2, a far cry from the US 2.8% rate.

STOCKS – RECORD RALLY

Stocks mount record rally, up 11%, bringing the Magnificent Seven back to the fore.

Risk is now high, and you can still get 5.01% for 90-day T-bills.

The next dip is one you buy.

However, the bull market is finally broadening out with a big focus on interest sensitives like housing, builders, emerging markets, and small caps.

$6 billion poured into US equity funds last week.

Now it’s volatility that’s crashing, down a record $49 points from $65 to $14 in 9 trading days.

Global EV sales jump 21% YOY, in July thanks to a large rise in China.

Buy on dips: Netflix (NFLX), Caterpillar (CAT), Deere (DE), VISA (V)

BONDS – FROM STRENGTH TO STRENGTH

Market prices in 50-point basis cut for September, holding on to massive rally.

A cut of only 25 basis points on September 18 could give us a $5 sell-off.

The September 6 Nonfarm Payroll report and Unemployment rate will be crucial.

(TLT) could make it to $110 by yearend, keep all LEAPS.

It’s not too late to buy derivative fixed-income plays.

Buy (TLT), (JNK), (NLY), (SLRN), and REITS on dips.

FOREIGN CURRENCIES – DOLLAR IS TRASH

Dollar hits seven-month low, as US interest rate cuts loom. It could be a decade-long move.

The Yen carry trade is back, with hedge funds piling back into positions they baled on only two weeks ago.

It’s just a matter of math, now that the Bank of Japan has given up on raising interest rates anytime soon.

What this means is more leverage, risk, and volatility for global financial markets. I love it!

The prospect of falling interest rates means that the greenback is toast.

Buy (FXA), (FXE), (FXB), (FXC).

ENERGY & COMMODITIES – RECESSION DRAG

Oil collapses to $71 a barrel, taking the rest of the commodity space down with it.

Cut off of 1 million barrels/day of Libyan production gives oil a brief respite.

This is despite the support from multiple Middle Eastern wars.

No one wants to pay for storage during a recession, especially with the current high interest rates. The worst-performing asset class of the year just got worse.

Weak Chinese economic data was the gasoline on the fire.

Replacement by EV’s and the shift out of cars into planes are big factors.

Copper flips from shortage to surplus, as the Chinese economic recovery drags on.

PRECIOUS METALS – NEW HIGHS

Gold pennies new all-time highs as Chinese have no other savings alternative.

Silver takes a break from economic slowdown, and enters a sideways range.

Miners have started to outperform metals for the first time in years, indicating an increase in investor leverage.

A global monetary easing is at hand.

Buy precious metals on the dips because rates are now falling decisively.

Buy (GLD), (AGQ), and (WPM) on dips.

REAL ESTATE – SALES BUMP

Mortgage rates hit the new 2024 low. The average for a 30-year, fixed loan was 6.46%, down from 6.49% last week.

Existing Homes sales jump in July for the first time in five months, up 1.3% to 3.95 million units.

Inventory is up a whopping 20% YOY.

The median home price rose to $442,000, up 4.2% YOY, with some 27% of sales all-cash buyers.

Sales of home over $1 million are up 26% YOY because the supply is up over 30%.

New-home construction dives, in July to the lowest level since the aftermath of the pandemic as builders respond to weak demand that’s keeping inventory levels high.

Total housing starts decreased by 6.8% to a 1.2 million annualized rate last month.

TRADE SHEET

Stocks – buy the next big dip.

Bonds – buy dips

Commodities – stand aside

Currencies – sell dollar rallies, buy currencies

Precious Metals – buy dips

Energy – avoid

Volatility – sell over $30

Real Estate – buy dips

NEXT STRATEGY WEBINAR

12:00 EST Wednesday, September 11 from Lake Tahoe, Nevada

JACQUIE’S POST HOUSEKEEPING

The August Monthly Zoom Meeting will be next Tuesday, September 3rd. I will be sending out the Zoom invitation today.

Cheers

Jacquie

Mad Hedge Biotech and Healthcare Letter

August 29, 2024

Fiat Lux

Featured Trade:

(ONE TEST TO RULE THEM ALL)

(ILMN), (BAYRY), (LLY), (MRK), (BMY), (AZN), (RHHBY), (NVS), (GH), (TEM), (TMO)

“One test to rule them all, one test to find them, one test to bring them all, and in the lab bind them,” the scientists at Illumina (ILMN) whispered – probably.

Their latest creation just got the FDA nod, and it's set to turn the world of cancer diagnostics on its head. It's as if Gandalf himself handed oncologists a palantír that reveals tumors' deepest secrets.

For those less versed in Middle-earth lore, this is like inventing a universal remote for tumor profiling, and oncologists can't wait to start channel surfing.

Now, you might be thinking, "What's the big deal?" Well, let me break it down for you.

This test, called TruSight Oncology Comprehensive (TSO for short), is the first FDA-approved genomic in vitro diagnostic kit that can make pan-cancer companion diagnostic claims.

In plain English, that means it's a single test that can be used across multiple cancer types. We're talking about a game-changer in precision oncology here.

Let's get into the nitty-gritty. This TSO test is a beast. It screens for a whopping 517 genes and provides comprehensive information on tumor mutational burden (TMB) and microsatellite instability (MSI).

These are crucial biomarkers that help determine how a patient might respond to immunotherapies. The breadth of data this single FDA-approved test can collect is unprecedented.

Now, you might be wondering, "Haven't we had companion diagnostics before?" Sure, but they've typically been limited to specific drugs or cancer types.

This pan-cancer test from Illumina is different. It can be applied to a wider range of solid tumors, and let me tell you, oncologists are loving it.

In fact, about 39% of U.S. oncologists have already said they strongly prefer using multi-gene panels over single-gene tests for guiding treatment decisions. That's a clear signal that there's demand for comprehensive diagnostic solutions like TSO.

Illumina's been busy across the pond, too. A version of this test has been available in Europe since 2022. But the U.S. version's got some new tricks up its sleeve.

It can help identify patients who might benefit from specific immunotherapies, including Bayer's (BAYRY) Vitrakvi and Eli Lilly's (LLY) Retevmo. The latter is a new addition compared to the EU version of the test.

Let's talk about these therapies for a second. Vitrakvi is used for adult and pediatric patients with certain NTRK mutations, regardless of their type of cancer. That's pretty cool, right?

But here's the kicker - these NTRK gene fusions are only found in about 0.1% to 0.3% of solid tumors, and they're tough to detect.

TSO's ability to scan both RNA and DNA means it can find multiple forms of this biomarker. That's a big deal for companies like Bayer, who've sometimes struggled to find eligible patients for this targeted therapy.

But Illumina's not resting on its laurels. They've got a growing pipeline of companion diagnostic claims in development, working hand in hand with drugmakers. They're planning to seek these in future regulatory submissions.

You see, Illumina's been playing the long game, forging partnerships with big pharma to co-develop companion diagnostics that align with targeted therapies.

Take their 2019 partnership with Merck (MRK), for instance. They teamed up to develop and commercialize a companion diagnostic using Illumina's TruSight Oncology 500 assay.

The goal? To identify genetic mutations in cancer patients that would respond to Merck's cancer drugs like Keytruda. This partnership boosted the adoption of Illumina's NGS platform in clinical oncology settings, contributing to both companies' growth.

The market liked what it saw at the time. Illumina's stock got a nice bump following the partnership announcement. And why wouldn't it?

The deal strengthened Illumina's position in the oncology diagnostics market, which is projected to grow at a CAGR of 12.4% from 2023 to 2030.

But Merck's not the only dance partner Illumina's got. They've also teamed up with Bristol-Myers Squibb (BMY) to use their TSO 500 assay as a companion diagnostic for immuno-oncology therapies.

This collaboration expanded Illumina's reach into new oncology applications, allowing BMY to use the TSO platform to identify patients most likely to benefit from its immune checkpoint inhibitors.

And there's more - Illumina's also forged partnerships with AstraZeneca (AZN), Roche (RHHBY), and Novartis (NVS) to develop companion diagnostic tests.

Next, let's talk numbers. Each new FDA-approved indication could potentially add $100 million to $200 million annually to Illumina's revenue. That's no chump change.

Unsurprisingly, Illumina's not the only player in this game.

Companies like Foundation Medicine (a Roche subsidiary), Guardant Health (GH), Tempus (TEM), Caris Life Sciences, Thermo Fisher Scientific (TMO), and GRAIL (another Illumina subsidiary) are all working towards pan-cancer or multi-cancer diagnostics.

Still, Illumina's TSO test is the first to secure FDA approval for pan-cancer companion diagnostic claims. This lead could translate into a significant market advantage.

Actually, Illumina already holds more than 70% market share in the global NGS market as of 2022. This means it’s well-positioned to benefit from this growth, and this latest FDA approval could further consolidate its market dominance.

Speaking of the FDA, they’ve been busy too. They've ramped up their support for precision medicine in recent years, approving a growing number of companion diagnostics and genomic tests.

From 2017 to 2021, they approved over 25 new companion diagnostics, a significant increase from the 5-10 approvals per year in the early 2010s. And a substantial portion of these approvals has been for oncology-related tests.

In 2021 alone, 68% of the FDA's new drug approvals were for cancer treatments.

Now, let's zoom out and look at the bigger picture. According to the World Health Organization, there were an estimated 19.3 million new cancer cases and 10 million cancer deaths worldwide in 2020.

The global cancer burden is expected to rise to 28.4 million cases by 2040, a 47% increase from 2020.

In the U.S., about 1.9 million new cancer cases are expected to be diagnosed in 2023.

The economic impact is also staggering. The economic burden of cancer in the U.S. was estimated at $157 billion in 2020, and it's projected to increase to over $246 billion by 2030.

These numbers stress the growing need for early detection and personalized treatment solutions.

But, unlike other companies, here's where advanced diagnostics like Illumina's TSO can make a difference. By ensuring patients receive the most effective treatments based on their genetic profiles, these tests can reduce unnecessary treatments and improve outcomes.

Studies have shown that using precision diagnostics can lower overall healthcare costs by 15% to 20% by avoiding ineffective therapies and hospitalizations.

Essentially, what we're seeing here is more than just a new test. It's a glimpse into the future of cancer treatment - more precise, more personalized, and potentially more effective.

For patients, it could mean better outcomes. For healthcare systems, it could mean more efficient use of resources. And for us? Well, it could mean significant opportunities in a rapidly growing market.

As Gandalf might say, "All we have to decide is what to do with the time that is given us." Illumina's chosen to use their time crafting this powerful new tool.

The quest to conquer cancer continues, and Illumina’s TSO might just be the ring-bearer we've been waiting for.

Keep your eyes peeled, fellow adventurers. The journey into precision oncology is only just beginning, and it promises to be an epic saga indeed.

Global Market Comments

August 29, 2024

Fiat Lux

Featured Trade:

(SEVEN TECH STOCKS TO BUY AT THE ENXT MARKET BOTTOM),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (META)

Last weekend, I had dinner with one of the oldest and best-performing technology managers in Silicon Valley. We met at a small out-of-the-way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables.

The service was poor and the food indifferent, as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information I had to promise the utmost in confidentiality. If I mentioned his name you would say “Oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on these lowest-of-margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third-party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer, who once in, buys more services.

Apple (AAPL) is his second holding, the next AI stock. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 25X over the last several years. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third-party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from up-front sales to a lifetime subscription model will also give it a boost.

Half of these are more than four years old and positively geriatric in the tech world. More than half of these are outside the US. 5G will add a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over-the-top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 21 Emmys this year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world. Tech growth will accelerate in 2021 and 2022.

5G will enable better Internet coverage for everyone and will increase the competitiveness of telecom companies. Factory automation will be another big area for 5G, as it is reliable and secure, and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government-threatened breakups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies of its own, views big American tech companies simply as a source of revenue through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Meta (META) control 70% of the advertising market, which is inherently a slow-growing market, expanding at 5% a year at best. (META)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised the value of tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings it is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract service revenues from their cars, like Apple has. Tesla will grow revenues by 30%-50% a year for the next two or three years. They should sell several million of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. However, interest rates are much lower. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

When rates rise in a year or so tech stocks may have to come down. They have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your shortlist for LEAPS to buy at the coming market bottom.

“The French have more fun in one year than the English do in ten,” said John Adams, America’s second president, and one-time ambassador to Paris and London.

In the ever-evolving landscape of big data analytics and artificial intelligence, Palantir Technologies Inc. (PLTR) has emerged as a prominent player, garnering significant attention from investors and tech enthusiasts alike. Founded in 2003 by a group of Silicon Valley veterans, including Peter Thiel, Alex Karp, Joe Lonsdale, Stephen Cohen, and Nathan Gettings, Palantir has carved a niche for itself by providing cutting-edge software solutions for data integration, analysis, and visualization to government agencies and large enterprises.

This comprehensive article aims to delve into the intricacies of Palantir's business model, its financial performance, the factors driving its stock trends, and the potential challenges and opportunities that lie ahead.

Company Overview:

Palantir's core mission revolves around helping organizations make sense of massive and complex datasets, enabling them to derive actionable insights and make informed decisions. The company's flagship platforms, Gotham and Foundry, are designed to address the unique needs of different sectors.

Gotham, primarily used by government agencies and intelligence communities, focuses on counterterrorism, fraud detection, and cybersecurity. Foundry, on the other hand, caters to commercial clients across various industries, including healthcare, finance, and manufacturing, empowering them to optimize operations, enhance customer experiences, and drive innovation.

Financial Performance:

Palantir's financial trajectory has been a subject of intense scrutiny, with investors closely monitoring its revenue growth, profitability, and cash flow. The company went public in September 2020 through a direct listing, bypassing the traditional initial public offering (IPO) process. Since then, its stock price has experienced significant volatility, reflecting the market's evolving perception of its growth potential and risk profile.

In recent quarters, Palantir has demonstrated impressive revenue growth, driven by a combination of new customer acquisitions, expansion within existing accounts, and the successful launch of new products and services. However, the company has yet to achieve consistent profitability, as it continues to invest heavily in research and development, sales and marketing, and infrastructure expansion.

Stock Trends and Analysis:

Palantir's stock price has been on a rollercoaster ride since its public debut, influenced by a multitude of factors, including:

Future Prospects:

Despite the inherent volatility and uncertainties, Palantir's long-term prospects appear promising, underpinned by several key factors:

Challenges and Risks:

While Palantir's future looks bright, it is not without its share of challenges and risks:

Conclusion:

Palantir Technologies Inc. is a company at the forefront of the big data analytics and AI revolution, with a compelling value proposition and a strong track record of delivering innovative solutions to complex problems. Its stock has experienced significant volatility since its public debut, reflecting the market's evolving perception of its growth potential and risk profile.

While the road ahead may be bumpy, Palantir's long-term prospects appear promising, underpinned by a large and expanding market opportunity, a strong customer base, technological innovation, strategic partnerships, and international expansion. However, the company also faces several challenges and risks, including achieving sustainable profitability, navigating a competitive landscape, managing customer concentration, and addressing regulatory and legal concerns.

Investors considering Palantir stock should carefully weigh the potential rewards against the inherent risks, conduct thorough due diligence, and adopt a long-term investment horizon. The company's success will ultimately depend on its ability to execute its growth strategy, maintain its competitive edge, and deliver consistent value to its customers and shareholders.

Mad Hedge Technology Letter

August 28, 2024

Fiat Lux

Featured Trade:

(NOT SUPER BY SUPER MICRO)

(SMCI), (NVDA)