Global Market Comments

October 30, 2024

Fiat Lux

Featured Trade:

(TAKE A LEAP INTO LEAPS)

Global Market Comments

October 30, 2024

Fiat Lux

Featured Trade:

(TAKE A LEAP INTO LEAPS)

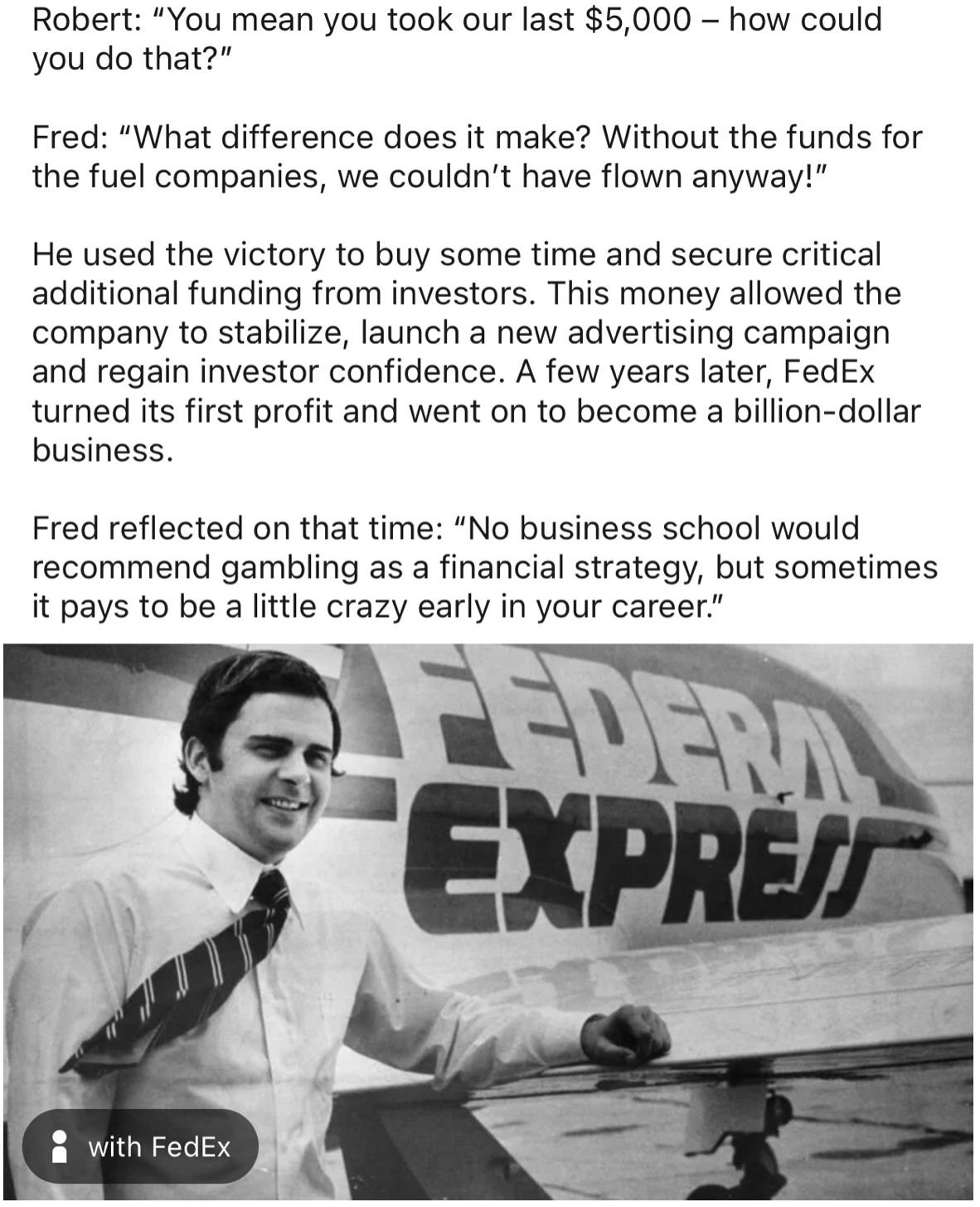

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Biotech and Healthcare Letter

October 28, 2024

Fiat Lux

Featured Trade:

(WHEN WALL STREET MET PHARMA)

(PFE), (TSLA), (AAPL)

If corporate America were a dinner party (and let's face it, sometimes it absolutely is), Pfizer (PFE) would be that guest who showed up fashionably late with an award-winning bourbon pecan pie during the pandemic, and is now being quietly judged for bringing Trader Joe's crackers to the latest soirée. The pharmaceutical giant, which briefly enjoyed the kind of celebrity usually reserved for Tesla (TSLA) and Apple (AAPL), finds itself in the midst of what we might delicately call a boardroom intervention. With its stock price taking a dive, Pfizer attracted the attention of Starboard Value, a hedge fund with a billion dollars' worth of opinions about how to run things better.

Unfortunately for Starboard, these problems are not that simple to fix. Here's the thing about making breakthrough drugs: 9 out of 10 fail, each costs about $2 billion to develop, and even the most brilliant scientists can't tell you which one will work until the very end. This uncertainty sits at the heart of Pfizer's current predicament. After delivering a ratings blockbuster with its COVID-19 vaccine and Paxlovid treatment, the company now faces the pharmaceutical industry's dreaded sophomore album syndrome.

On top of that, every successful drug faces the same issue: it comes with its own expiration date. Patents run out, generic competitors swoop in, and suddenly everyone's asking, "What's next?"

And here's where it gets more interesting, in the way that all corporate power plays are interesting if you enjoy watching incredibly wealthy people disagree about how to become even wealthier. Take Starboard's critique of Pfizer's performance. It has all the subtlety of a CNN town hall debate, spiced up with the potential involvement of former Pfizer CEO Ian Read and CFO Frank D'Amelio — a plot twist as unsurprising as finding a filibuster in the Senate.

Having previously applied its corporate reconstruction techniques to the restaurant industry (think less Thomas Keller, more Olive Garden optimization), the hedge fund now fancies itself as something of a pharmaceutical expert. This is like suggesting that because someone successfully managed a food truck, that same person is qualified to run a three-Michelin-star restaurant.

Granted, Starboard has an impressive track record in corporate makeovers, much like the HGTV stars of Wall Street. Still, renovating a pharmaceutical company isn't the same as flipping a restaurant chain. There's something uniquely challenging about applying fast-casual dining turnaround principles to the development of life-saving medications. Some processes simply can't be rushed unless you enjoy explaining to the FDA why you thought clinical trials were more of a suggestion than a requirement.

As we try to figure out what's happening with the pharma giant right now, it helps to keep in mind that the key question isn't just whether Pfizer needs a makeover (though that's certainly part of it), but whether Wall Street's "time is money" philosophy can successfully coexist with the "science takes time" reality of drug development. It's the corporate equivalent of trying to teach quantum physics to a day trader - theoretically possible, but likely to result in some interesting misunderstandings along the way.

So, what's the play here? Looking at Pfizer's current stock price of around $28.45 (down 2.47%), the chart looks about as exciting as a waiting room magazine collection.

While the stock hovers below its 50-day moving average and sits near the lower end of its $25.20 - $31.54 yearly range, there are a few bright spots: a healthy 5.91% dividend yield and several promising projects in the pipeline - an RSV vaccine and an obesity treatment that could have customers lining up around the block again.

But here's my recommendation: Keep this one on your watchlist, but hold off on placing your order just yet.

Think of Pfizer as that once-trendy restaurant that's neither closing its doors nor winning any new Michelin stars - it's simply simmering on medium heat while the new chef (courtesy of Starboard) debates menu changes with the original kitchen staff.

Will Starboard's intervention prove to be the corporate equivalent of a breakthrough drug, or more like one of those miracle cures you see advertised at 3 AM?

The answer, like most things in the pharma world, will take time to develop. And in this battle of wits within corporate America, sometimes the hardest pill to swallow is patience - though I suspect Starboard would prefer it in fast-dissolving form.

After all, when Wall Street meets Pharma, it's less about whether the patient needs the medicine and more about timing the market's appetite.

For now, let's keep this one in the "worth watching" category until we see some signs of the stock's vital signs improving.

Global Market Comments

October 29, 2024

Fiat Lux

Featured Trade:

(RIGHT SIZING YOUR TRADING)

In an era where artificial intelligence is reshaping nearly every aspect of our lives, retirement planning stands on the cusp of a dramatic transformation. The traditional model of retirement planning – annual meetings with financial advisors, static spreadsheets, and one-size-fits-all investment strategies – is giving way to a more dynamic, personalized, and AI-driven approach that promises to democratize financial planning for millions of Americans

Financial technology experts predict that by 2030, the majority of Americans will rely on AI assistants as their primary tool for retirement planning. These digital advisors won't just crunch numbers; they'll serve as personal financial coaches, available 24/7 to help individuals navigate the complex landscape of retirement preparation.

"We're moving from a world where retirement planning was something you thought about quarterly or annually to one where it's an ongoing, dynamic conversation," says Dr. Sarah Chen, Director of Financial Technology Research at Stanford University. "AI assistants will continuously monitor your financial situation, making micro-adjustments to your retirement strategy in real-time."

One of the most significant advantages of AI-powered retirement planning is the ability to create highly personalized strategies. Traditional financial planning often relies on broad demographic categories and general rules of thumb. In contrast, AI systems can analyze thousands of variables specific to each individual, including:

Spending patterns and habits

Career trajectory and earning potential

Health data and life expectancy predictions

Family circumstances and obligations

Regional economic conditions

Personal risk tolerance and financial goals

Mark Rodriguez, CEO of RetireTech Solutions, explains: "AI assistants can process and analyze data points that human advisors simply don't have the capacity to consider. This means retirement strategies can be tailored not just to broad demographics, but to the individual level – down to suggesting specific timing for major purchases or identifying the optimal moment to begin Social Security benefits."

Unlike traditional retirement planning tools, AI assistants can provide continuous monitoring and adjustment of retirement strategies. These systems can:

Automatically rebalance investment portfolios based on market conditions

Adjust savings recommendations based on spending patterns

Modify investment strategies in response to major life events

Provide immediate guidance during market volatility

Optimize tax strategies throughout the year

"The days of static retirement plans are over," notes Financial Planning Association President Jennifer Wong. "AI assistants can detect subtle changes in your financial situation and make immediate adjustments to keep you on track for your retirement goals."

Perhaps the most revolutionary aspect of AI-powered retirement planning is its potential to make sophisticated financial guidance accessible to a broader population. Traditional financial advisors often require minimum investment amounts or charge fees that put their services out of reach for many Americans.

"AI assistants are democratizing access to high-quality financial planning," says Dr. Michael Patel, an economist at the Brookings Institution. "These tools can provide professional-grade retirement planning advice at a fraction of the cost of traditional advisors, making comprehensive retirement planning accessible to millions of Americans who previously couldn't afford it."

Despite the growing capabilities of AI assistants, experts emphasize that they won't completely replace human financial advisors. Instead, the future will likely involve a partnership between AI systems and human professionals.

"AI assistants excel at data analysis, pattern recognition, and continuous monitoring," explains Rachel Martinez, CFP, of Fidelity Investments. "But human advisors bring emotional intelligence, complex problem-solving abilities, and the capacity to understand nuanced family dynamics that AI systems might miss."

This hybrid approach is already emerging, with many financial advisory firms incorporating AI tools into their practice while maintaining the human relationship aspect of their service.

One of the most promising aspects of AI-powered retirement planning is the ability to help individuals overcome common behavioral biases that can derail long-term financial planning. AI assistants can:

Identify and alert users to emotional decision-making patterns

Provide behavioral nudges to encourage better financial habits

Offer context-aware guidance during market volatility

Help users maintain long-term perspective during short-term market events

"Financial decisions are often emotional decisions," says Dr. Lisa Thompson, a behavioral economist at MIT. "AI assistants can help identify when emotions might be clouding judgment and provide objective, data-driven recommendations to keep retirement plans on track."

As AI assistants become more integral to retirement planning, privacy and security concerns take center stage. The industry is developing robust frameworks to protect sensitive financial data while maintaining the effectiveness of AI systems.

"Security isn't just about protecting data; it's about maintaining trust," says cybersecurity expert David Chang. "The future of AI-powered retirement planning depends on creating systems that are both powerful and secure, giving users confidence that their financial information is protected."

As AI assistants take on greater responsibility in retirement planning, regulatory frameworks are evolving to ensure appropriate oversight. The Securities and Exchange Commission and other regulatory bodies are developing new guidelines for AI-powered financial advice.

"We're working to strike the right balance between innovation and consumer protection," says former SEC Commissioner Elizabeth Barrett. "The goal is to harness the benefits of AI while maintaining the high standards of fiduciary responsibility that consumers expect and deserve."

As we look toward the future, experts predict several key developments in AI-powered retirement planning:

AI systems will become increasingly sophisticated at predicting future financial needs and market conditions, allowing for more accurate long-term planning.

Retirement planning AI will seamlessly integrate with other financial services, from banking to insurance, creating a more holistic approach to financial management.

AI assistants will become more conversational and intuitive, making complex financial concepts more accessible to the average user.

AI systems will offer even more personalized recommendations, taking into account an expanding array of personal and economic factors.

The future of retirement planning is being reshaped by AI assistants that offer unprecedented levels of personalization, accessibility, and continuous optimization. While these tools won't completely replace human financial advisors, they will democratize access to sophisticated financial planning tools and help millions of Americans better prepare for retirement.

"We're entering an era where quality retirement planning isn't just for the wealthy," concludes Dr. Chen. "AI assistants are making it possible for everyone to have a personal financial advisor in their pocket, working around the clock to help them achieve their retirement goals."

As these systems continue to evolve and improve, they promise to help address the retirement savings crisis facing many Americans by making expert-level financial guidance more accessible, affordable, and effective than ever before. The future of retirement planning isn't just about better technology – it's about creating a more financially secure future for everyone.

Mad Hedge Technology Letter

October 28, 2024

Fiat Lux

Featured Trade:

(THE FUTURE OF TECH STOCKS)

(AI), (NVDA), (XLU), (XLE), (AAPL), (GOOGL), (AMZN), (META), (MSFT)

Through the vast whole spectrum of public markets, the U.S. stock market, and specifically technology stocks, are dominating versus their peers from other countries.

Heck, even Apple, just one company from a small suburb in California, is valued at a price that is greater than the entire German economy.

Does that speak to how bad the German economy is, or does it speak to the potency of public tech companies in America?

The truth is probably a bit of both.

Then, take a second and try to absorb the fact that Apple hasn’t even integrated AI into its own products yet.

The future is bright for many tech stocks, and the rally will broaden out to non-Magnificent 7 stocks.

More granularly, the US will continue to lead by market cap share as artificial intelligence benefits expand beyond a few large tech names that have dominated the market rally over the past year to companies in various industries.

Revenue production and margin improvement will be the critical levers of expansion.

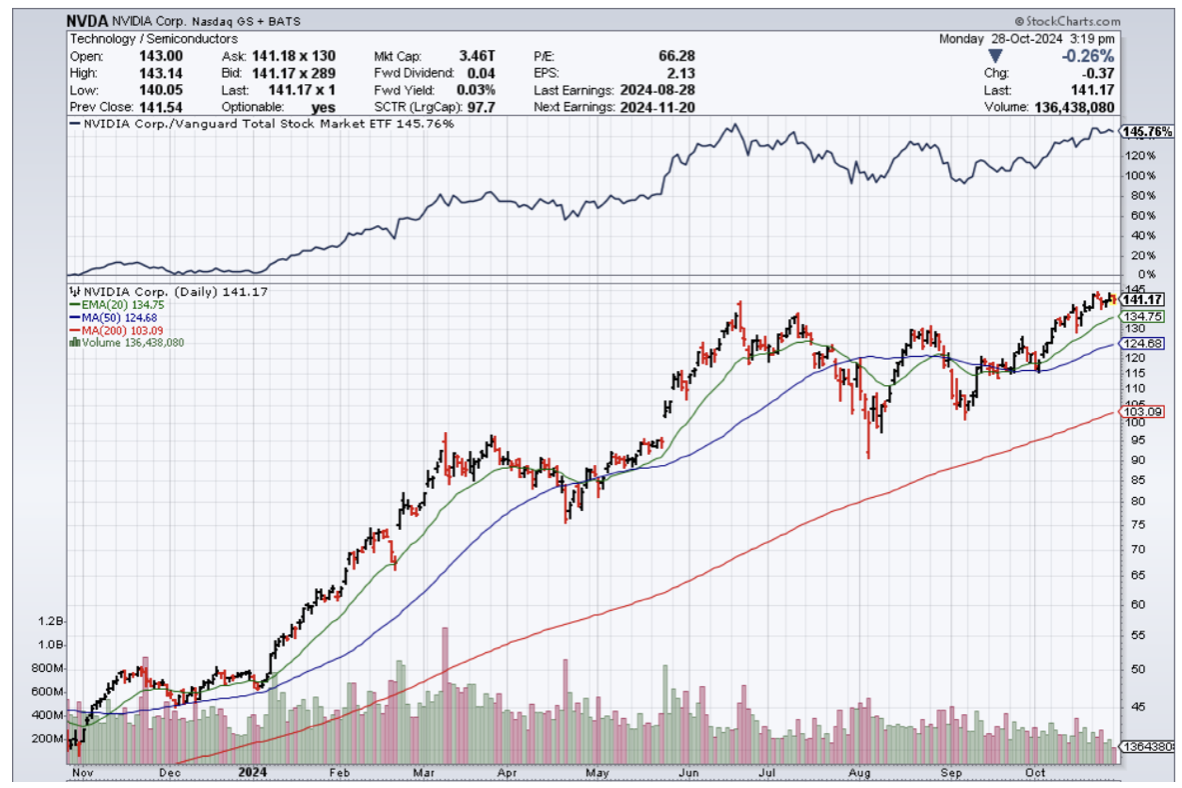

The first will come from the money pouring into AI benefiting companies outside of Big Tech. This plays out as tech companies buy AI chips from the likes of Nvidia (NVDA), and as they need more power, these AI operators are forced to spend with companies in the Utilities (XLU) and Energy (XLE) sectors.

As AI makes companies more efficient and eliminates the simplest work, eventually cutting down costs, US corporates should get a boost to profit margins.

Global equity markets, including retirement allocations to equities, are basically leveraged to Nvidia.

A non-US tech company will rise over the next decade and unseat the large tech companies currently driving the US market share, like Apple (AAPL), Nvidia, Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), and Meta (META) are almost zero.

When we look at the revenue possibilities and understand that AI will directly cut expenses by creating efficiencies, it’s hard to see tech stocks do anything but go higher in the long term.

Even then, there will be some dips, and they should absolutely be characterized as buying opportunities.

Just look at a 3-month chart of Apple, and each month has presented a dip buying opportunity on August 6th, September 16th, and October 7th.

Apple stock is up 7.5% in the past 3 months.

When everyone complains that tech stocks are too expensive, well, they will get more expensive.

As long as leverage is able to be tapped, institutions will tap it and look for that asymmetric trade to the upside.

Tesla has also proved how hard it is to bet against tech and Elon Musk.

It usually is a terrible idea.

The setup to Tesla’s earnings meant a very low bar, and Musk jumped over it to the tune of a 22% pop in Tesla stock.

Tech is clearly in a secular bull trend, and trying to get artsy to squeeze in a microdip on the short side usually has meant a loss-taking event.

Why even try?

It’s my job to tell readers to bet on tech going to the upside, especially the quality companies that accelerate revenue by harnessing the superpowers of AI.

(TIME TO STEEL YOURSELF FOR A NEWSY WEEK JUST BEFORE THE ELECTION)

October 28, 2024

Hello everyone

WEEK AHEAD CALENDAR

Monday, Oct. 28

10:00 a.m. Richmond Fed Index (October)

10:30 a.m. Dallas Fed Index (October)

7:30 p.m. Japan Unemployment Rate

Previous: 2.5%

Forecast: 2.5%

Earnings: Ford Motor, On Semiconductor

Tuesday, Oct. 29

8:30 a.m. Wholesale Inventories preliminary (September)

9:00 a.m. FHFA Home Price Index (August)

9:00 a.m. S&P/Case Shiller comp. 20 HPI (August)

10:00 a.m. Consumer Confidence (October)

10:00 a.m. JOLTS Job Openings (September)

8:30 p.m. Australia Inflation Rate

Previous: 3.8%

Forecast: 2.9%

Earnings: Visa, Chipotle Mexican Grill, First Solar, Caesars Entertainment, Advanced Micro Devices, McDonalds, Pfizer, Royal Caribbean Group, PayPal, D.R. Horton, Alphabet.

Wednesday, Oct 30

8:15 a.m. ADP Employment Survey (October)

8:30 a.m. GDP Chain Price first preliminary (Q3)

8:30 a.m. GDP first preliminary (Q3)

10:00 a.m. Pending Home Sales Index (September)

10:00 a.m. Pending Home Sales

Earnings: Microsoft, Meta Platforms, Starbucks, Kraft Heinz, Caterpillar, Eli Lilly, GE Healthcare Technologies, Clorox, Bookings Holdings.

Thursday, Oct. 31

8:30 a.m. Continuing Jobless Claims (10/19)

8:30 a.m. ECI Civilian Workers (Q3)

8:30 a.m. Initial Claims (10/26)

8:30 a.m. Core PCE Deflator (September)

8:30 a.m. PCE Deflator (September)

8:30 a.m. Personal Consumption Expenditure (September)

8:30 a.m. Personal Income (September)

9:45 a.m. Chicago PMI (October)

Earnings: Apple, Amazon.com, Norwegian Cruise Line Holdings, Uber Technologies, The Estee Lauder Companies, Mastercard, Generac.

Friday, Nov. 1

8:30 a.m. Jobs Report (October)

Previous: 254k

Forecast: 140k

9:45 a.m. S&P PMI Manufacturing final (October)

10:00 a.m. Construction Spending (September)

10:00 a.m. ISM Manufacturing (October0

Earnings: Exxon Mobil

It’s a data heavy week. Big Tech reports earnings, and expectations are high, but many analysts are still beating the table on these tech stocks, particularly Meta (META), Apple (AAPL) and Microsoft (MSFT) believing they have further room to run.

The employment report on Friday takes on additional significance ahead of next week’s FOMC meeting. Market participants will also closely monitor Q3 GDP estimates and PCE inflation figures throughout the week. These high impact releases could reshape market sentiment heading into the US election. In fact, any deviation from the recent streak of robust economic data could potentially lead to significant moves in the US dollar.

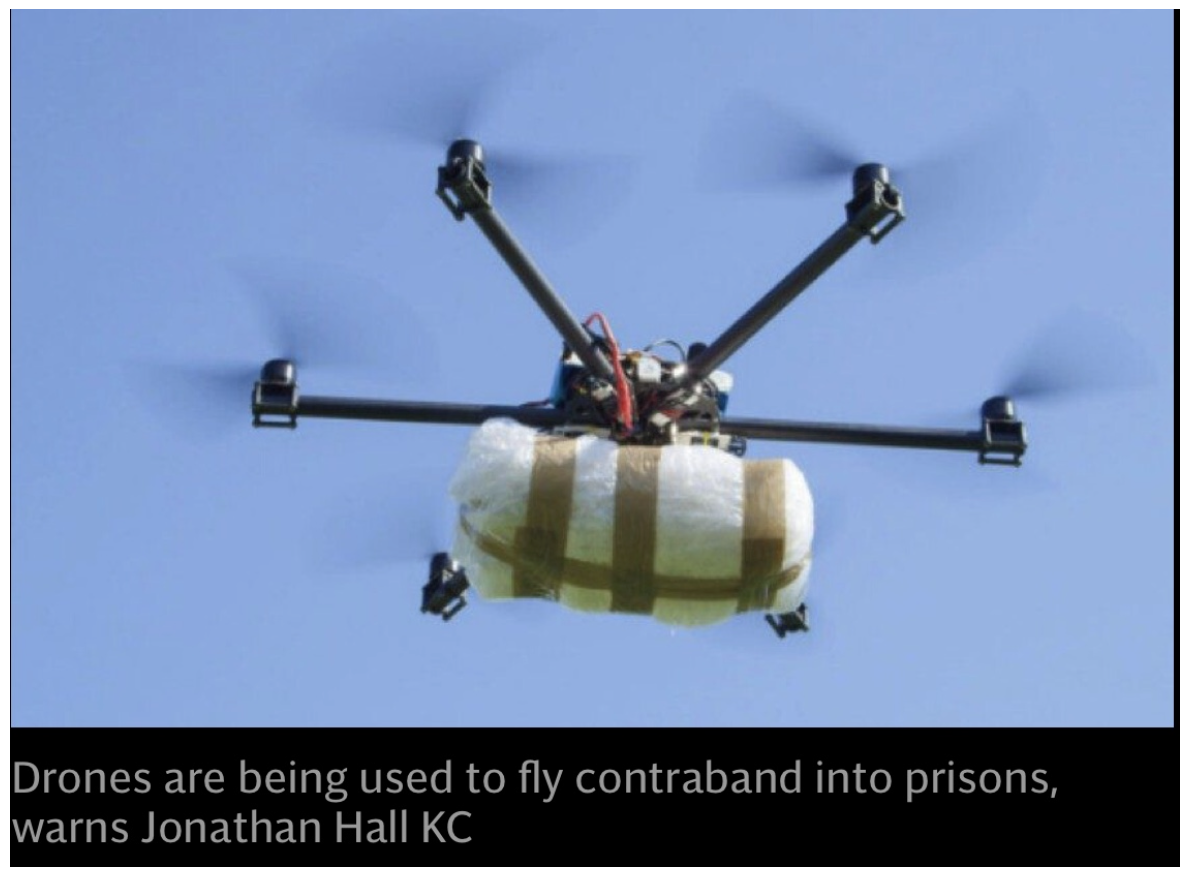

‘Toy’ Drones Could Be A ‘Real’ Tool for Terrorists

Britain’s streets could be transformed into chaos if Extremists use “toy drones”. This is the warning from the Government’s counter terrorism management team.

Current rules enforced by the Civil Aviation Authority (CAA) require people operating drones weighing more than 250g to be registered and pass a theory test. However, lighter devices are widely available and are not subject to the same rules.

The world’s biggest drone company DJI sells multiple models advertised as weighing 249g.

In the UK there is regulation affecting the use of drones and it includes some provision for licensing users, but the regulation does not apply to ‘toy’ drones.

The Gold Boom

We all know that gold’s value is driven by interest rates, inflation and geopolitical fears; it is the insurance of choice for investors seeking security. When interest rates fall and returns on some assets slide with them, gold can be a safe bet. When inflation erodes a currency’s purchasing power, the price of gold rises like everything else. Furthermore, it is also a haven commodity for investors, who are concerned about war and global tensions.

This boom seems a little different, particularly the drivers of the gold price.

Central banks of emerging nations have been the big buyers of the past couple of years. Many of these nations are hostile to the United States and see hoarding more gold as financial protection. Others just think that the days when the dollar was the dominant means of global exchange is waning.

That’s a big wake up call for the West. Mohamed El-Erian believes that we could be witnessing a fragmentation of the international financial system based on the dollar. And that would mean eroding US power.

Central bank gold buying hit a record high in the first three months of 2024, according to the World Gold Council. India, Uzbekistan, Qatar, Russia, Iraq, and Jordan were among the biggest purchasers. China has increased its buying too.

It appears many countries are calling time on America’s “weaponisation” of the dollar. Collectively, these countries may conclude that they might be better off with an alternative currency to use for international trade. And holding more gold could be a foundation for a new payments system.

Russian president Vladmir Putin has long envisioned the creation of a gold-backed alternative to the dollar, and last week he had a chance to push his agenda. At a three-day economic summit, which included the latest gathering of the BRICS group of emerging economies – Brazil, Russia, India, China and South Africa – Putin shared his vision for a BRICS currency. Egypt, Ethiopia, Iran, the United Arab Emirates, Turkey, Pakistan, Thailand, Venezuela, Senegal and Saudi Arabia are seen as potential members.

At the Summit, Putin showed a symbolic banknote, “The Unit” featuring the flags of BRICS countries.

Even if the BRICS members and their partners never find a way to circumvent the dollar, no one stocking up on gold appears to be losing money at this time.

MARKET UPDATE

S&P 500

Uptrend intact. Could be a volatile week with Big Tech earnings out and the Jobs Report.

Next Target: ~$5,900

Support: ~$5750/$5720

GOLD

Rally set to continue after time correction.

Next Targets: $2765/$2850

BITCOIN

Bullish structure still intact.

Next Targets: $72,560/$75,240/$81,340

QI CORNER

SOMETHING TO THINK ABOUT

Cheers

Jacquie

Global Market Comments

October 28, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE IS YOUR POST-ELECTION PORTFOLIO

plus THE LAST SILVER BUBBLE)

(NVDA), (META), (CRM), (TLT), (JNK), (CCI), (DHI), (LEN), (PHM),

(GLD), (SLV), (NEM), (FXE), (FXB), (FXA), (TSLA), (JPM), (BAC), (GS)