Mad Hedge Biotech and Healthcare Letter

January 23, 2025

Fiat Lux

Featured Trade:

(THE HARD TRUTH ABOUT THIS BIOTECH'S PIPELINE THAT WALL STREET DOESN'T GET)

(MRK), (AMGN), (AAPL)

Mad Hedge Biotech and Healthcare Letter

January 23, 2025

Fiat Lux

Featured Trade:

(THE HARD TRUTH ABOUT THIS BIOTECH'S PIPELINE THAT WALL STREET DOESN'T GET)

(MRK), (AMGN), (AAPL)

Earlier this month, while reviewing my biotech holdings during a layover at Chicago O'Hare, I got an interesting call from a long-time reader.

He was panicking about Merck (MRK) after seeing it trading near its 52-week lows, convinced the pharmaceutical giant was headed for trouble.

"Have you seen what Medicare negotiations did to Januvia?" he asked, referencing the 79% price reduction. "And Keytruda's patent expires in 2028!"

Here's the hard truth about this biotech's pipeline that Wall Street doesn't get: while everyone's fixated on Keytruda's patent cliff, Merck has quietly tripled their late-stage pipeline in just over three years.

We're talking more than 20 unique assets in late-stage development, plus another 50 in early stages.

The last time I saw this kind of pipeline expansion was during the early days of Amgen (AMGN), which turned out pretty well for investors who saw past the obvious.

Actually, Merck's current "crisis" also reminds me of the time I bought Apple (AAPL) right after Steve Jobs announced the iPhone. Everyone worried about the risk, while I saw the opportunity.

Merck just posted Q3 2024 numbers that would make most CEOs envious: revenue up 7% year-over-year to $16.7 billion.

Keytruda, their cancer blockbuster, grew 21% to $7.4 billion. Even their Animal Health division jumped 11%. These aren't the numbers of a company in trouble.

Speaking of investors, they've enjoyed a 126% total return over the past decade with Merck, despite more ups and downs than my last flight through turbulence.

The company's 5-year average Return on Equity sits at 25% (recently climbing to 28%), with Return on Invested Capital steady at 20%.

With a Weighted Average Cost of Capital around 8%, there's plenty of room for growth.

Yesterday, I was discussing these numbers with a former FDA commissioner (who shall remain nameless) over coffee.

He pointed out something fascinating: Merck's R&D spending is increasing alongside revenue growth. That's like a tech company doubling down on product development – exactly what you want to see in pharma.

For dividend hunters (and I know many of you are), Merck offers a 3.3% yield with a 7% five-year dividend growth rate.

The payout looks sustainable too, consuming 68% of earnings and 55% of free cash flow. It's not going to make you quit your day job, but it's better than the 1.4% you'll get from the S&P 500.

Looking at valuation, Merck trades at a P/E of 20.5, below its historical average of 22.3.

My own growth projections suggest a 13% annual rate going forward. Optimistic? Perhaps. But with their robust pipeline and near-term analyst projections, I've seen crazier things work out.

The company just announced a $15 billion share repurchase program, including plans to spend $7.5 billion over the next 12 months. When management puts that kind of money where their mouth is, I tend to pay attention.

Yes, Keytruda's patent cliff in 2028 is real. But so is Merck's late-stage pipeline of antibody-drug conjugates (ADCs) – think smart missiles in the war against cancer.

And unlike some biotechs, Merck has the financial muscle to weather any storm, with decreasing net debt and a solid cash position.

Remember what I always say about buying straw hats in winter? Merck right now is like finding a premium pharma stock in the discount bin.

Just like my friend who panicked and sold everything after the November 8 election (and missed the subsequent rally), sometimes the best opportunities come disguised as problems.

As for me, I'm looking at Merck as a potential long-term hold. The company's fundamentals remind me of other great turnaround stories I've traded successfully over the years.

With the healthcare sector currently out of favor and Merck trading near its 52-week lows, this might be one of those moments we look back on and wish we'd bought more.

And speaking of patents, maybe I should patent my strategy: “Buy great companies when everyone else is afraid.” Though I suspect Warren Buffett already beat me to that one.

Global Market Comments

January 23, 2025

Fiat Lux

Featured Trades:

(WHY WATER WILL SOON BE WORTH MORE THAN OIL),

(CGW), (PHO), (FIW), (VE), (TTEK), (PNR),

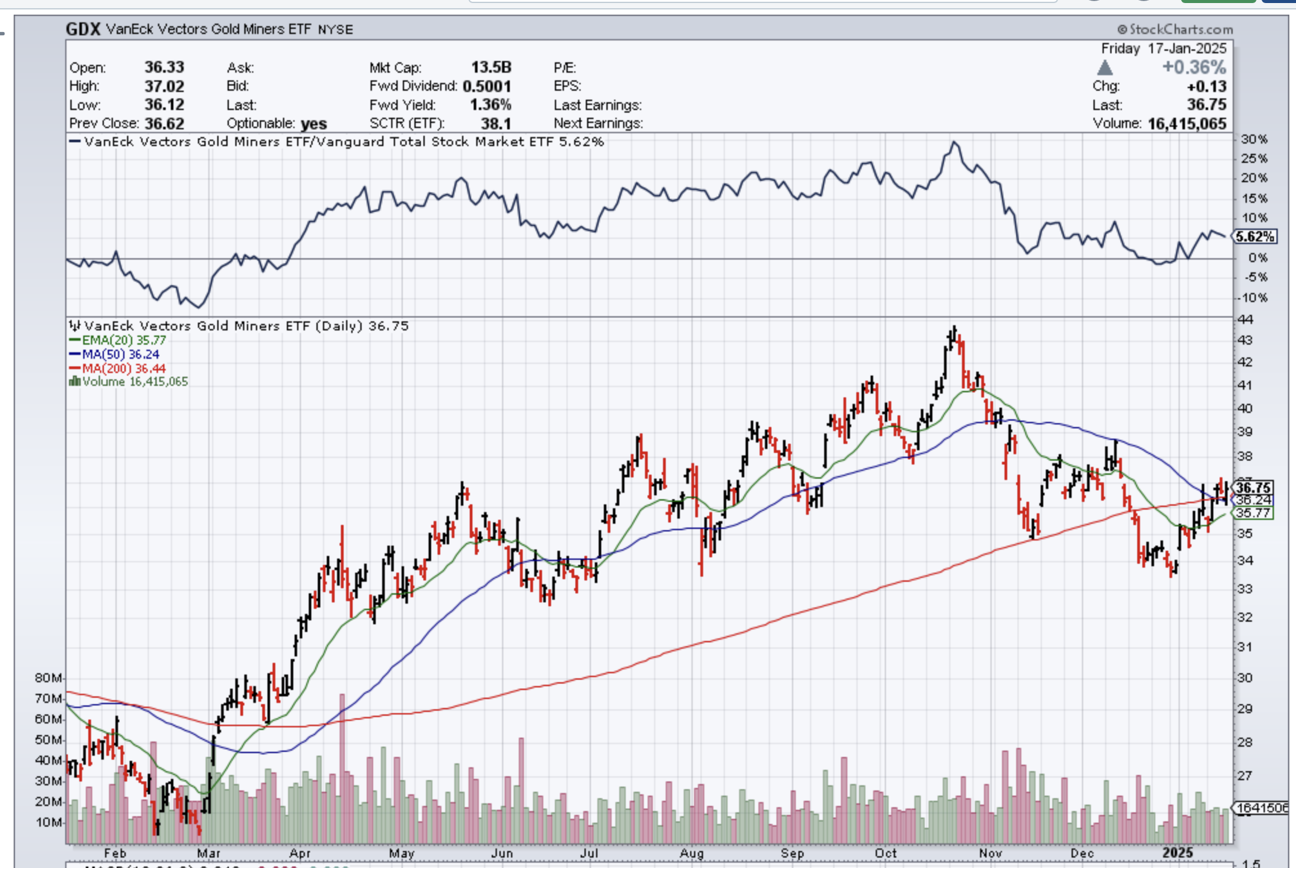

(WHY WARREN BUFFETT HATES GOLD),

(GLD), (GDX), (ABX)

After seven years in the penalty box, gold is finally starting to come alive, and the Armageddon crowd is absolutely loving it. Maybe after ten years of rising, stocks are finally expensive on a relative basis?

These are the guys who are perennially predicting the collapse of the dollar, the default of the US government, hyperinflation, and the end of the world.

Better to keep all your assets in gold and silver, store at least a year’s worth of canned food, and keep your untraceable guns well-oiled and supplied with ammo, preferably in high-capacity magazines.

If you followed their advice, you lost your shirt.

I have broken many of these wayward acolytes of their money-losing habits. But not all of them. There seems to be an endless supply emanating from the hinterlands.

The “Oracle of Omaha” Warren Buffet often goes to great lengths to explain why he despises the yellow metal.

The sage doesn't really care about the gold, whatever the price. He sees it primarily as a bet on fear. I imagine he feels the same about Bitcoin, the modern tulips of our age.

If investors are more afraid in a year than they are today, then you make money on gold. If they aren't, then you lose money.

The only problem now is that fear ain’t working.

If you took all the gold in the world, it would form a cube 67 feet on a side, worth $5 trillion. For that same amount of money, you could own other assets with far greater productive earning power, including:

*All the farmland in the US, about 1 billion acres, which is worth $2.5 trillion.

*Seven Apple’s (AAPL), the second largest capitalized company in the world at $731 billion.

Instead of producing any income or dividends, gold just sits there and shines, making you feel like King Midas.

I don't know. With the stock market at an all-time high and oil trading at $75/barrel, a bet on fear looks pretty good to me right now.

I'm still sticking with my long-term forecast of the old inflation-adjusted high of $2,300/ounce.

It is just a matter of time before emerging market central bank buying pushes it up there. And who knows? Fear might make a comeback too.

(PLTR), (MSFT), (AMZN), (GOOG), (ORCL)

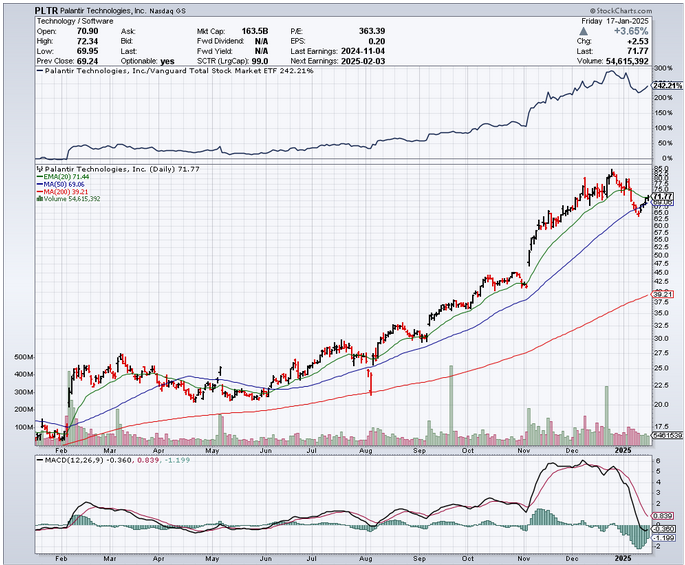

Back in the early days of my career, I watched countless "revolutionary" tech companies come and go, each promising to change the world with their shiny new algorithms. But Palantir (PLTR) caught my eye for an entirely different reason - they were actually getting their hands dirty with real-world problems while everyone else was still writing whitepapers.

Let me put this in perspective. While most tech firms were trying to convince their first customers to sign proof-of-concept agreements, Palantir was already knee-deep in the kind of work that makes three-letter agencies sit up and take notice.

Their Gotham platform became such a fixture in intelligence circles that it's practically government-issued equipment now, like those ubiquitous office coffee machines, only significantly more sophisticated.

The numbers tell the story better than I ever could. In their latest quarter, Palantir raked in $727 million in revenue, up 30% year-over-year.

That translated into a GAAP net income of $144 million - not bad for a company that some skeptics dismissed as just another government contractor with a fancy PowerPoint deck.

But here's where it gets interesting. Their U.S. commercial business shot up 54% compared to last year.

That's not just growth - that's the kind of acceleration that makes venture capitalists spill their artisanal lattes. It reminds me of the early days of Microsoft (MSFT), when suddenly every business decided they needed Windows, whether they understood it or not.

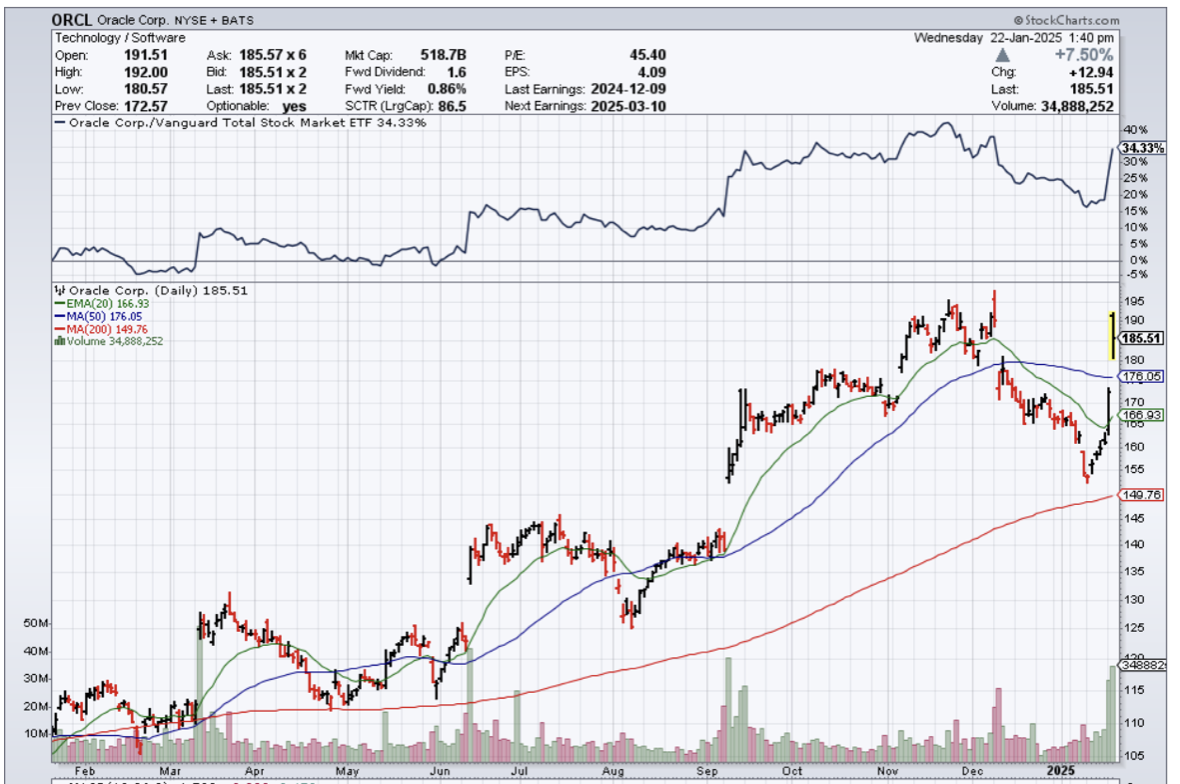

Speaking of relationships, Palantir has been building quite the rolodex. They're working with everyone from Amazon's (AMZN) AWS to Microsoft's Azure, Google's (GOOG) GCP, and Oracle's (ORCL) Cloud. It's like being invited to all the cool kids' parties and actually showing up to each one.

This Switzerland-of-software approach has helped them spread their AI capabilities faster than a viral tweet.

The government business, though - that's their secret weapon. Remember when I mentioned those three-letter agencies? Palantir's Gotham platform has become so embedded in the intelligence community that trying to remove it would be like trying to extract coffee from the Pentagon's budget.

They're not just selling software – they're providing the digital infrastructure that modern intelligence operations run on.

Meanwhile, their commercial "boot camp" approach to onboarding new clients is pure genius.

While other tech companies treat implementation like a drawn-out Victorian courtship, Palantir gets companies up and running faster than you can say "digital transformation."

I've seen so many enterprise software rollouts in my day, and most of them move at the pace of continental drift. Not Palantir's.

And the numbers? They're even better than the execution. Their adjusted free cash flow exceeded $1 billion on a trailing 12-month basis.

Their "Rule of 40" score - a metric that combines revenue growth and profitability - hit 68. For those keeping score at home, that's like batting .400 in the major leagues.

Looking ahead, Palantir isn't just positioned for growth - it's positioned for dominance.

They're expanding into next-generation autonomous solutions, JADC2, and manufacturing OS modules. It's like watching a chess player who's already thinking five moves ahead while everyone else is still learning how the pieces move.

The question isn't whether Palantir is good at what they do - they clearly are. In a market where AI capabilities separate the winners from the also-rans, Palantir isn't just playing the game - they're changing the rules.

But at $153 billion with a heart-stopping forward P/E of 176, even the best technology can make for a terrible investment.

And let's not forget - their heavy reliance on government contracts means they're just one budget cut away from a really bad quarter.

I've watched too many market cycles to chase stocks at these levels. The time to back up the truck on Palantir will come - probably during the next tech selloff when the momentum crowd dumps everything indiscriminately.

That's when you'll want to pounce on this AI powerhouse. For now, keep your powder dry and put this one on your shopping list for when prices better match reality.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

January 22, 2025

Fiat Lux

Featured Trade:

(A.I. BUBBLE CONTINUES TO INFLATE)

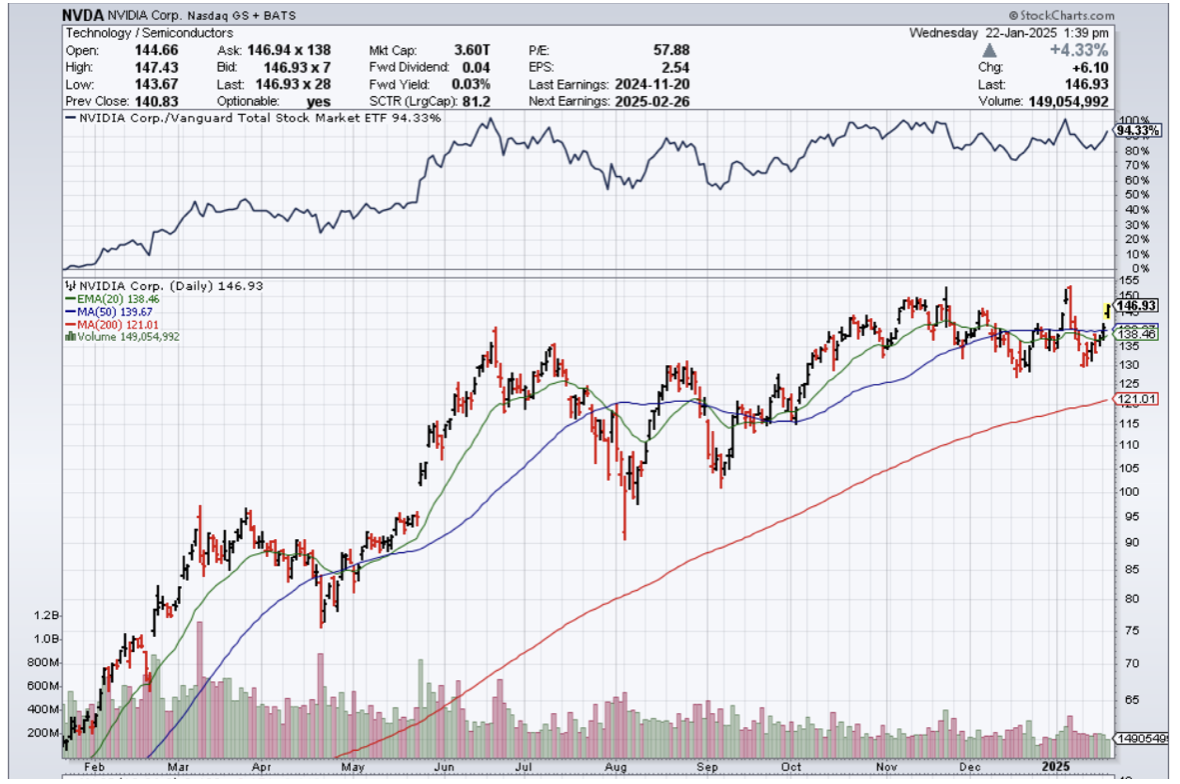

(ORCL). (ARM), (NVDA)

Expect a half a trillion dollar investment into data centers.

This should propel AI stocks higher and the new administration understands the last leg the tech market is standing on is the AI bubble.

It is debatable to say if these tech stocks are in a bubble, but they aren’t cheap and today’s announcement puts fuel in the fire forcing stock prices to go nowhere but up.

OpenAI says that it will team up with Japanese conglomerate SoftBank and with Oracle to build multiple data centers for AI in the U.S.

The joint venture, called the Stargate Project, will begin with a large data center project in Texas and eventually expand to other states. The companies expect to commit $100 billion to Stargate initially and pour up to $500 billion into the venture over the next four years.

SoftBank chief Masayoshi Son, OpenAI CEO Sam Altman, and Oracle co-founder Larry Ellison were in attendance.

Microsoft is also involved in Stargate as a tech partner. So are Arm and Nvidia.

The data centers could house chips designed by OpenAI someday. The company is said to be aggressively building out a team of chip designers and engineers, and working with semiconductor firms Broadcom and TSMC to create an AI chip for running models that could arrive as soon as 2026.

Abilene, Texas will be Stargate’s first site, and OpenAI says that Stargate, by 2029, could scale up to 20 data center installations.

Microsoft, which recently announced it is on track to spend $80 billion on AI data centers showing it’s an industry-wide trend.

It’s clear to everyone and also investors that propping up the AI tech world is a must because the drop in shares would be devastating to not only the retail holders but also to corporate America.

Much of the recent inflation has been paid by stock appreciation and history has shown that the current US president highlights accelerating stock prices as a barometer of US economic health.

The interesting part of this is building a slew of data centers doesn’t translate into revenue one-to-one.

The jury is still out there whether there will be a revenue windfall out of it.

At the very minimum, we know that data centers will make the price of electricity higher for everyone because they guzzle energy non-stop.

The revenue accrued will need to be higher than the cost of electricity or this is just another massive transfer from retail consumers to the corporate tech world.

Ironically, Elon Musk tweeted that the money isn’t available right now leading the investor to believe this is more about keeping the AI bubble alive than anything else.

Rumor has it that Musk doesn’t really like OpenAI CEO Sam Altman who took OpenAI from non-profit to for-profit and harvesting a multi-billion dollar payday.

Until now, kicking potential revenue creation can down the road is the order of the day, and as long as investors can buy this idea that AI data centers will mean higher revenue opportunities, then shareholders will still pile into this bubble until they don’t.

That is why stocks like Nvidia, Oracle, and ARM are seeing double digit gains in just one day.

Buy these three companies on the dip until the AI bubble pops.

“Great companies are built on great products.” – Said CEO of Twitter Elon Musk

(TRUMP’S FIRST DAY)

January 22, 2025

Hello everyone

The U.S. now has a convicted felon for a President.

That’s a first.

He has survived two impeachment trials; two assassination attempts and an indictment for trying to overturn his 2020 election loss.

But who cares?

The world keeps turning and businesses, and the country itself, are set to make extra greenbacks with Trump’s business-friendly policies.

So, all is well, right? What could possibly go wrong?

On his first day, Trump did the following:

-declared a state of emergency on the US-Mexico border

-pardoned nearly all those charged with crimes related to the 2021 attack on the US Capitol.

-made the (DOGE) Department of Government Efficiency official

-withdrew from the Paris Climate Agreement

-exited from the World Health Organization

-signed an order(temporarily) suspending the sale of TikTok

-froze government hiring

- drafted measures to support racial equity and combat gender-based discrimination were thrown out

-signed an order “restoring free speech and ending federal censorship”.

-signed an order “protecting women from radical gender ideologies.”

- robustly declared that he was aiming at “defeating America’s enemies.”

##############################################################

Trump will seek to end birthright citizenship for US-born children whose parents lack legal status.

Trump will restore the death penalty.

Trump will require that official US documents such as passports reflect citizens’ gender as assigned at birth.

Trump said he “was saved by God to make America great again.” We can argue then, that we have a President portraying himself as a national saviour.

On stage with Trump was the business elite

Tesla and SpaceX CEO, Elon Musk, Amazon CEO Jeff Bezos, and Meta CEO Mark Zuckerberg. All had prominent seats on stage, next to cabinet nominees and members of Trump’s family.

Biden’s last official act

Biden pardoned several people, whom Trump has targeted for retaliation, including former White House chief medical advisor Anthony Fauci, former Republican US representative Liz Cheney, and former chairman of the Joint Chiefs of Staff General Mark Milley.

Now, to the markets…

Netflix earnings came out Tuesday, and they were a blockbuster. Stocks rallied strongly.

Do you have this stock in your portfolio?

I recommended it on January 17, 2024, when it was sitting at $480. The stock is now sitting at $994.80 (in extended hours) just shy of $1000.

The company surpassed 300 million paid memberships during the quarter, adding a record 19 million subscribers. The company beat on the top and bottom lines for the 4th quarter and raised its 2025 revenue forecast.

In 2025, the company says it plans to improve its core business with more series and films, enhance its product experience, and continue to grow its ads business. On top of that, Netflix is expected to explore the live event space and games, too.

Portfolio Update

After the holidays, in the first newsletter of the year, (01/06/25) I recommended that you scale into two Uranium Energy plays.

(VST) Vistra Energy at $163.95. At close today (01/21), the stock price is $$185.35.

(SMR) Nu-Scale Power Corporation at $23.66. At close today (01/21), stock price is $25.61

Cheers

Jacquie