When you develop your opinions on the basis of weak evidence, you will have difficulty interpreting subsequent information that contradicts these opinions, even if this new information is obviously more accurate,” said Nassim Nicholas Taleb, author of Antifragile: Things That Gain from Disorder.”

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/Bad-Good-Meter.jpg236402Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2025-02-28 09:00:152025-02-28 12:07:39February 28, 2025 - Quote of the Day

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

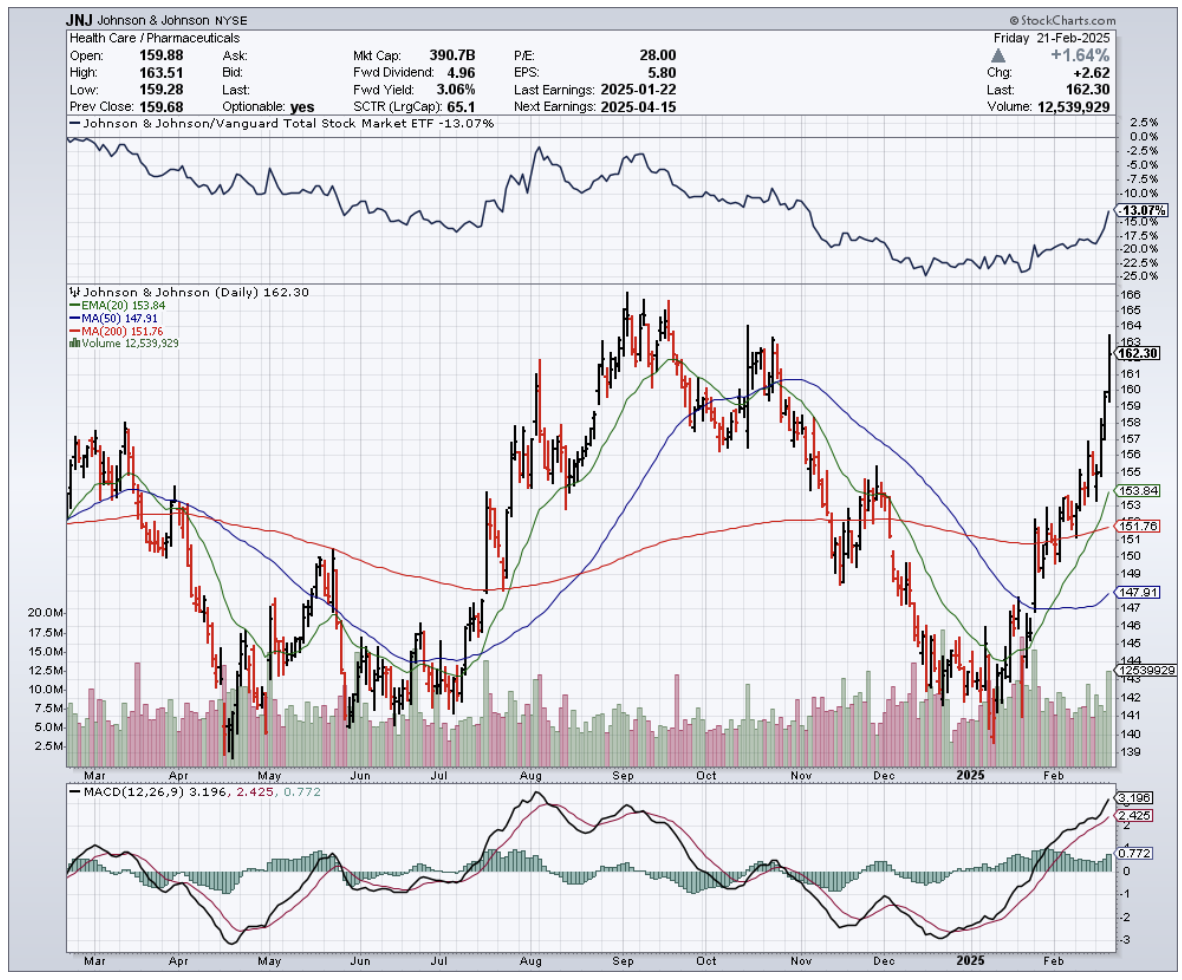

The other day, while sorting through my oldest trading records (yes, I keep everything), I found my first Johnson & Johnson (JNJ) dividend check from decades ago. It wasn't much—just enough for a nice dinner back then.

But here's the kicker: that dividend has grown every single year since, weathering oil shocks, dot-com bubbles, financial crises, and even pandemics. It got me thinking about what truly makes a fortress stock in today's market.

While everyone's chasing the latest biotech and healthcare moonshot, JNJ has been quietly building an empire.

With a market cap of $375 billion and revenue growing at an impressive 7.55% annual clip since the 1980s, this company has accomplished something few others have—long-term, consistent growth while raising dividends for over six decades. And then there's the balance sheet.

JNJ is sitting on $25 billion in cash against $38 billion in total debt, resulting in a covered ratio of 29.4. That means they could pay their debt service with spare change found in their corporate couch cushions.

Some investors dismiss JNJ as just another mature healthcare stock, but that perspective overlooks the quiet revolution happening within the company.

In the first two months of 2025 alone, JNJ secured multiple FDA approvals. The most notable? SPRAVATO, the first and only monotherapy for treatment-resistant depression. And they're not stopping there.

JNJ recently announced a $14.6 billion acquisition of Intra-Cellular (ITCI), securing CAPLYTA, a blockbuster drug for bipolar disorder and schizophrenia.

With the global Central Nervous System therapeutics market projected to grow at a 10.5% CAGR through 2034, JNJ is strategically positioning itself for future expansion.

What's particularly impressive is how JNJ has transformed its research and development approach. They're not just throwing money at problems—they're getting smarter about their investments.

Their R&D success rate has been climbing, with a higher percentage of late-stage trials making it to market compared to industry averages. This isn't by accident.

JNJ has been leveraging artificial intelligence and machine learning to better predict which compounds are most likely to succeed, potentially saving billions in development costs. It's like having a crystal ball in the lab, and it's giving them a significant edge over competitors who are still using traditional development methods.

Despite its fortress balance sheet and track record of reliability, JNJ is currently trading at a discount to historical averages.

Its forward P/E ratio sits at 15.8, compared to a five-year average of 17.9. The dividend yield is at 3.18%, higher than its 10-year average of 2.7%. Its price-to-sales (P/S) ratio stands at 4.4, below its five-year average of 4.8.

These numbers suggest the market is underpricing JNJ's resilience and growth potential.

Of course, no investment is risk-free. JNJ is facing looming patent expirations on key drugs, including Stelara, which generated $10.3 billion in 2024 sales, and Xarelto, which brought in $2.3 billion.

However, history suggests that patent cliffs aren't a new challenge for JNJ—they've successfully navigated them for decades. Their strong drug pipeline, along with strategic acquisitions, should help offset any revenue declines.

Beyond pharmaceuticals, JNJ's business diversification is a major advantage.

With roughly two-thirds of revenue coming from Innovative Medicine and the remainder from MedTech, and with 43% of total revenue sourced outside the U.S., this diversified revenue mix helps mitigate risks tied to any single product or market.

What many investors miss is how JNJ's MedTech division is quietly becoming a powerhouse in its own right.

The division has been making strategic moves in robotics and AI-enabled surgical tools, positioning itself at the intersection of healthcare and technology.

This isn't just about selling more medical devices—it's about creating entirely new categories of treatment options. In an aging global population, this kind of innovation could be worth billions in future revenue streams.

With a 16.7% return on invested capital (ROIC) over the last decade and a modest 49% payout ratio, JNJ's dividend isn't just stable—it's poised for growth. The market's current pessimism has created a 24% discount on a company that has delivered for generations.

That's the kind of opportunity that made me start buying JNJ decades ago—and why I'm still adding to my position today.

In a world where even tech giants stumble, owning a company that's been raising its dividend since the Kennedy administration isn't just smart—it's common sense.

The question isn't whether JNJ is a buy. The real question is whether you'll regret not buying the dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-02-27 12:00:072025-02-27 12:15:15The Kennedy-Era Stock That's Still Paying My Dinner Bills

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

While reviewing earnings reports last week at my mountain cabin, I couldn't help but chuckle at the stream of "Google is dead" headlines flooding my inbox.

Having covered technological disruptions since the early days of the personal computer revolution, I've learned that paradigm shifts rarely happen overnight. The reality is far more nuanced.

The bears would have you believe that Google (GOOGL) is about to become the next Yahoo!, destined for the tech graveyard as AI chatbots eat its lunch.

After decades of watching tech giants rise and fall, I've developed a nose for distinguishing between genuine disruption and market hysteria. This feels a lot like the latter.

Let me share something that might surprise you: Google's search business is still growing even as ChatGPT and its AI cousins grab headlines.

We're looking at a $2.25 trillion behemoth with $95.66 billion in cash, trading at a better valuation than its big tech peers. Now THAT's what I call a disconnect between perception and reality.

Here's why the Google-is-dead crowd has it all wrong.

For one, Google isn't sitting on its hands. I've analyzed enough tech transitions to know the difference between a company adapting and one in denial.

After a brief deer-in-headlights moment when ChatGPT launched, they've gone full throttle into AI. The difference? Google can actually afford the AI arms race.

While OpenAI burns through cash faster than a Silicon Valley startup during the dot-com boom, Google generates enough free cash flow from its search business to fund its AI future.

It's like having a money printer to fund your R&D - something I wish every promising tech company had back when I was analyzing startups in the '80s.

But here's the kicker that most people miss: Google has THREE aces up its sleeve that nobody else can match.

First, they have an ecosystem that would make any tech company envious.

Google is on virtually every smartphone worldwide. They've got 8.5 billion daily searches, millions of YouTube uploads, and more data points than there are stars in the Milky Way.

Second, they have data quality that puts everyone else to shame.

While OpenAI is scrambling to buy training data (word is they're running out of public data to train on), Google's got a fresh firehose of high-quality, real-world information flowing in daily.

Third, they have cash flow that won't quit.

With a $95.66 billion war chest and money-printing core business, Google can outspend and outlast virtually any competitor.

Speaking of money, let's talk valuation.

Google's enterprise value sits at $2.18T, but here's what makes it interesting - it's actually cheaper than Microsoft on an EV/EBITDA basis.

The company's been buying back shares like they're going out of style, reducing the share count by 10% in just five years. That's a sneaky 2% annual return right there, before we even talk about price appreciation.

Sure, there are risks. New players like Perplexity are popping up faster than NFT projects in a bull market.

But having witnessed multiple tech cycles, I can tell you that unseating an incumbent with Google's advantages is about as easy as climbing Mount Everest in flip-flops.

Don't get me wrong - Google needs to execute.

Their CAPEX spending shows they're serious, but it's still below Meta (META) and Microsoft (MSFT) as a percentage of revenue. That might need to change.

But with search revenues still growing and AI integration accelerating, Google looks more like a phoenix than a dinosaur.

The bottom line? Google is a buy on dips. The death of search has been greatly exaggerated, and the company's positioning in AI is far stronger than the market realizes.

Where will Google be in five years? Nobody knows for sure, but I've got a strong hunch those AI-powered searches will be making us all look smarter while making Google shareholders richer.

Now, if you'll excuse me, I need to go check if my AI assistant can help analyze these quarterly earnings faster than I can. Some disruptions are worth embracing.

https://www.madhedgefundtrader.com/wp-content/uploads/2025/02/Screenshot-2025-02-26-152554.png385675Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2025-02-26 15:16:382025-02-26 15:29:34AI Tech Letter

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.