Mad Hedge Technology Letter

March 12, 2025

Fiat Lux

Featured Trade:

(SHOULD I CARE ABOUT ORACLE?)

(ORCL), (AAPL), (META), (AMZN)

Mad Hedge Technology Letter

March 12, 2025

Fiat Lux

Featured Trade:

(SHOULD I CARE ABOUT ORACLE?)

(ORCL), (AAPL), (META), (AMZN)

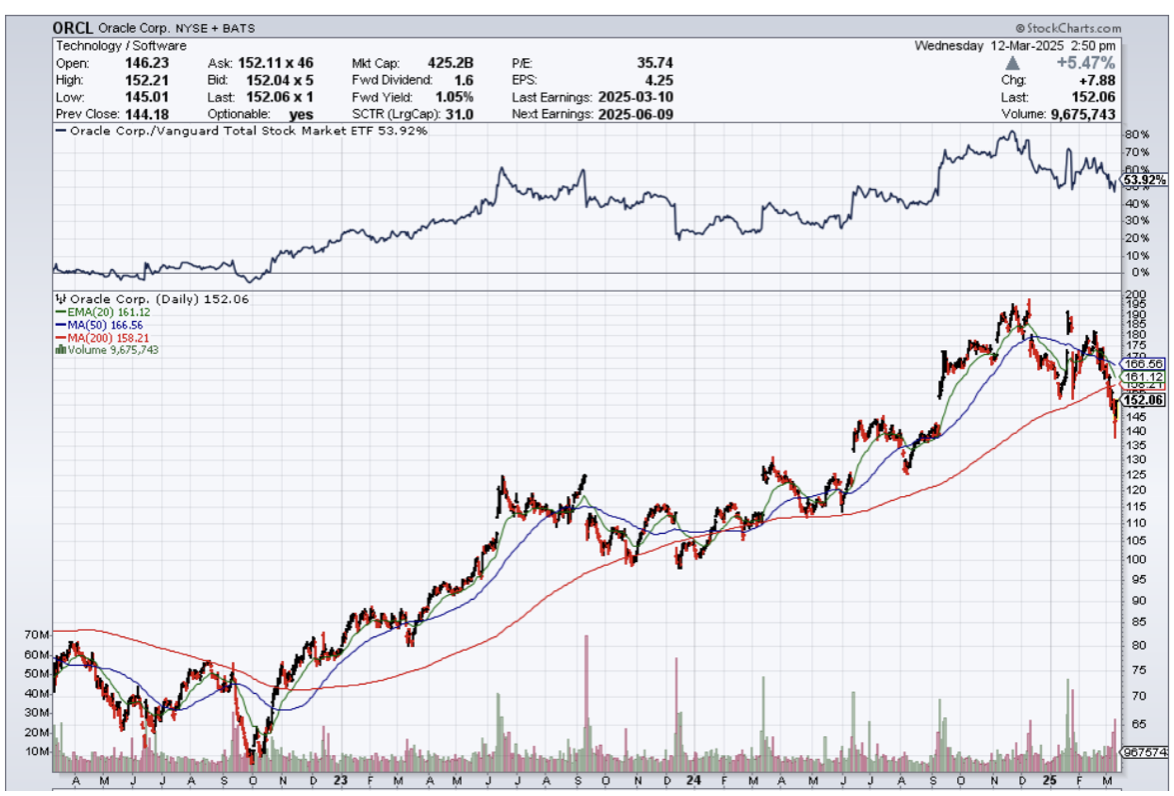

If readers want to know if the Oracle AI story is dead or not, then listen here.

The story is still alive, so don’t give up on a good thing.

Oracle is getting swept up with the wider macroeconomic scare that has been triggered by geopolitics.

The fear porn has reached fever pitch and is causing tech stocks to detour from their usual self.

The question now is if the sabre-rattling will result in the economic recession we have been waiting 6 years for.

The flood of government money for at least 4 of those years carried spending habits even if those jobs were unproductive or fraudulent.

As it relates to Oracle’s business model, there is no recession in the sub-sector they are in, but I believe they chose to tank the earnings result since all equities were getting dragged down.

The truth is that Oracle’s business is experiencing great growth in the cloud, and AI demand is accelerating sales growth.

The macroeconomic volatility gave Oracle’s management the perfect excuse to guide down since a high forecast would have resulted in a selloff anyway.

Oracle's leadership encouraged investors to focus on the potential for its cloud business to benefit from enterprise AI spending.

A growing backlog for cloud services is giving the company clear visibility for beating growth metrics.

Meanwhile, sales of Oracle's closely watched cloud-infrastructure business increased 49%, compared with 52% growth for the segment in Oracle's November-ended quarter. Oracle's guidance for the May-ending quarter of 9% revenue growth missed previous forecasts of 9.5% growth.

Oracle's cloud infrastructure business is racing to build out computing capacity for AI startups and other users of the cloud. The Oracle Cloud Infrastructure business rents computing power to other companies, competing against much larger hyperscalers Amazon.com (AMZN), Microsoft (MSFT), and Alphabet's (GOOGL) Google.

Chairman and Chief Technology Officer Larry Ellison said that Oracle is on track to double its data-center capacity during the calendar year. The company now expects capital expenditures to grow to $16 billion for its May-ending fiscal 2025, roughly doubling from a year earlier.

Ellison appeared at the White House in late January with President Donald Trump, OpenAI leader Sam Altman, and SoftBank Chief Executive Masayoshi Son to announce an AI infrastructure effort costing $100 billion called Stargate.

While tight data center capacity has demanded some patience from investors, I believe that we move past some of the capacity constraints in the second half of this calendar year.

The deep selloff from $190 per share to $140 has to hurt.

It was just only a short time ago when Oracle was a deadbeat tech stock left behind by the likes of Apple and Facebook.

They have reinvented themselves as an AI infrastructure company, and that has done wonders for their stock.

When they were down in the dumps, ORCL stock was trading below $50, so we are a far cry from that.

Once the tech market gets its mojo back, ORCL will definitely return back in form to that buy the dip stock that did so well in 2023 and 2024.

Just bide your time until we can jump back into ORCL.

“The key to making things affordable is design and technology improvements, as well as scale.” – Said Elon Musk

(THE POSSIBILITY OF A U.S. RECESSION IS NOW BEING ACKNOWLEDGED)

March 12, 2025

Hello everyone

The shift is on from bull to bear as the “R” word becomes a discussion topic.

After a few months of me warning everyone about an impending down move/bear market, going against the grain of most professional analysts and all the “talking heads”, Ed Yardeni now comes out and says it is “possible a bear market has already started.”

As recently as February, he said the U.S. economy could go a decade without a recession. In January, he said investors are in a “roaring 2020” market.

The shift in his view comes after the whiplash of back-and-forth changes in trade policy from President Donald Trump, and early signs of economic weakness, and highlighted concerns of a recession, itself defined as two consecutive quarters of economic contraction.

Yardeni points out that Trump is testing the limits of the economy and the markets. His administration’s rapid-fire policy initiatives have been testing every limit imaginable, and so far, there has been a good measure of resiliency, but recession fears are definitely rising.

Trump has gone ahead and done it.

He has introduced 25% tariffs on Australian aluminium and steel. Our Prime Minister described the move as “unfriendly and unjustified” and an “act of economic self-harm.” Europe, also, did not escape similar tariffs. But Europe plans to retaliate with tariffs on U.S. goods.

Australia will not retaliate. But there could be implications down the track. Interestingly, economists say the tariffs have more “bark than bite.”

Trump’s tariffs could take the U.S. on a dangerous journey with unforeseen implications.

Ray Dalio has commented that a severe U.S. supply-demand problem could lead to ‘shocking developments.’ He is focused on the debt issue and believes we could see unexpected developments in terms of how it’s going to be dealt with.

Where to hide and protect your portfolio while Trump wages a tariff trade war.

Within the fixed income market, you can find a source of stability with U.S. Treasury Inflation-Protected Securities (TIPS), which should outperform in both high-inflation and recession environments.

TIPS are sold by the U.S. Treasury with 5-, 10-, and 30-year terms. Unlike traditional government bonds, the principals on TIPS – the amount the government agrees to pay back to the bond holder – can move higher or lower over the maturity term of these instruments. At the end of the term, if the principal is higher than the original agreed rate, the holder gets the increased amount. If the principal is equal to or lower than the original rate, the TIPS holder is paid the original agreed principal.

Corporate credit markets are also an option.

Brian Mangwiro, managing director of global sovereign debt and currencies at Barings, has suggested Investors can focus on sectors less exposed to tariffs such as financials, construction, and defence, and avoid those in the line of fire such as autos and potentially technology.

By now, you should have insurance in place, such as (SDS) or (SH) to cover what you wish to keep in your portfolio.

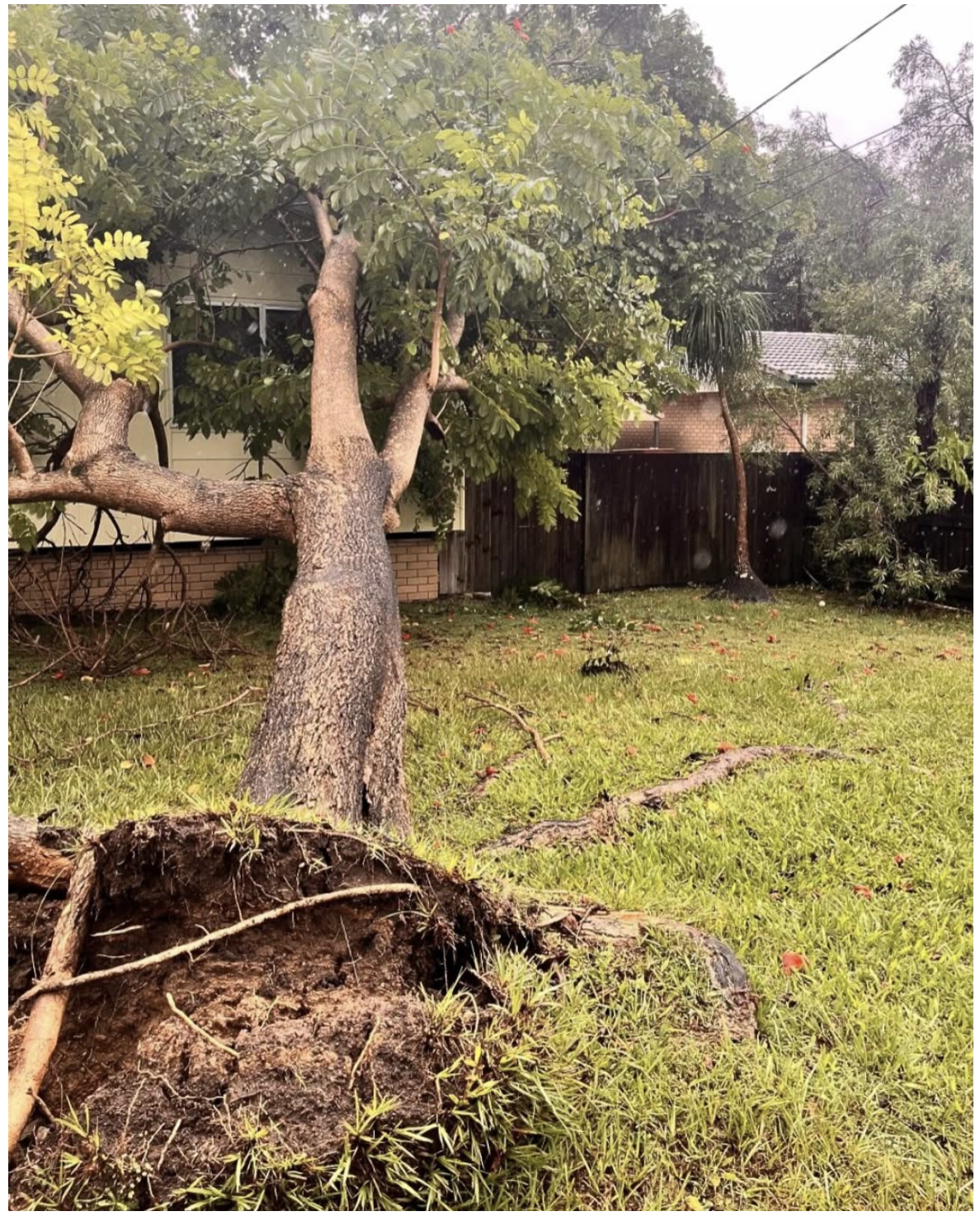

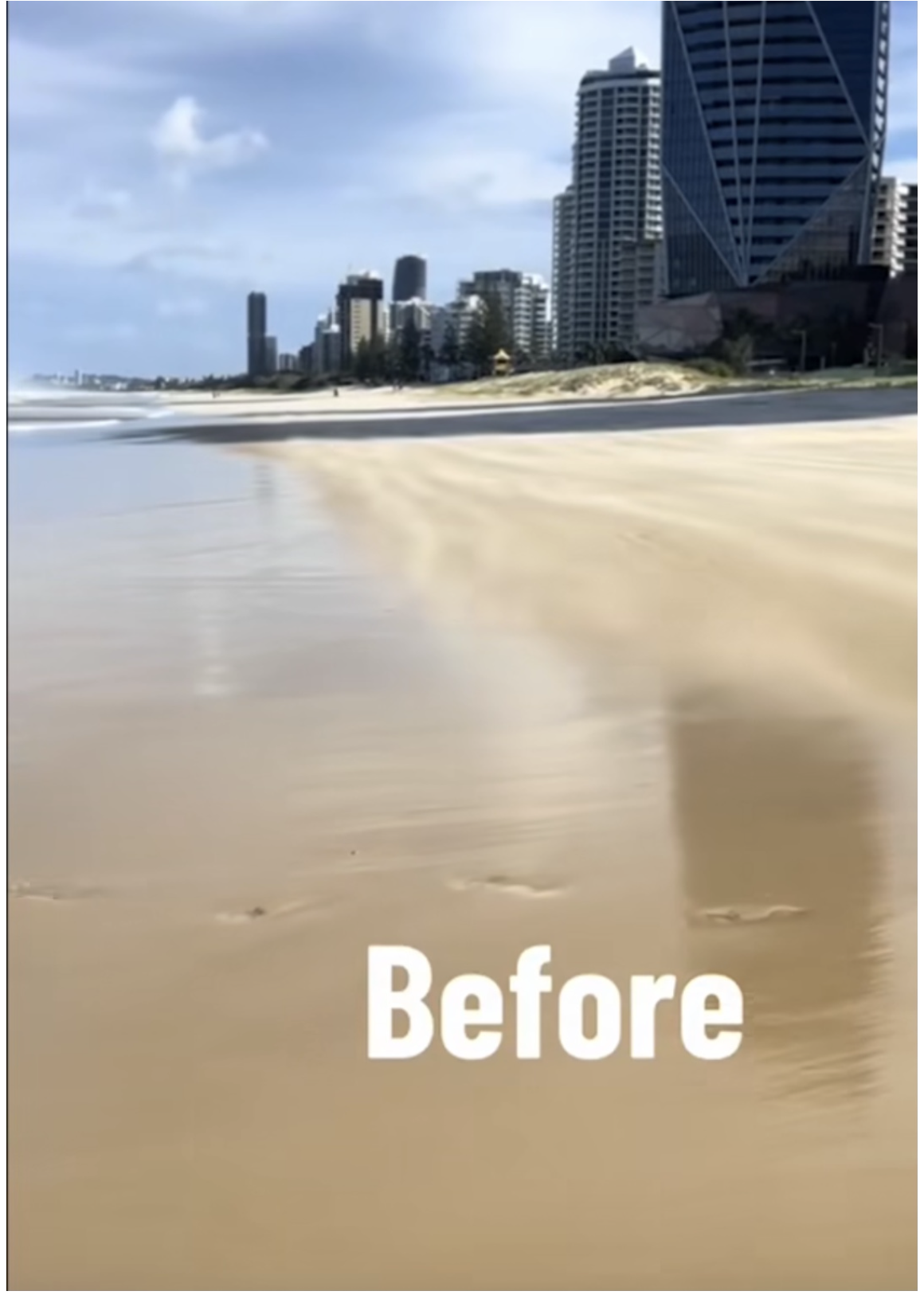

MY CORNER OF THE WORLD IN PHOTOS AFTER CYCLONE ALFRED

Powerlines down across roads in multiple areas across Brisbane, Gold Coast, and Sunshine Coast and as far inland as Toowoomba (a two-hour drive from the Gold Coast).

This has been a common sight in every neighbourhood across the Gold Coast. Some people also lost their roofs.

A huge cliff has formed right along the coastline after Cyclone Alfred battered the coast and eroded our beautiful beaches. Millions of cubic metres of sand have been gauged from 500km of coastline.

QI CORNER

SOMETHING TO THINK ABOUT

Cheers

Jacquie

Mad Hedge Biotech and Healthcare Letter

March 11, 2025

Fiat Lux

Featured Trade:

(WHEN INSIDERS GO SHOPPING, PAY ATTENTION)

(MRNA), (MRK)

In 1815, Nathan Rothschild made his legendary fortune buying British securities when they were deeply discounted after Waterloo. “Buy when there's blood in the streets,” he allegedly said. That kind of contrarian wisdom has made fortunes across centuries.

Two centuries later, I find myself applying this timeless principle to Moderna (MRNA). The biotech darling has shed over 90% of its value since the pandemic peak, plummeting from $400+ to under $30. And now, insiders are quietly loading up.

The shift in insider activity at Moderna has been striking. Over the past year, insiders unloaded more than 602,000 shares, with the heaviest selling in 2024 when the stock was trading above $120.

One director alone offloaded 202,832 shares in a single transaction, pocketing $30 million. But as Moderna’s share price took a nosedive, insider selling slowed to a trickle. By the time the stock fell below $100, most trades involved fewer than 1,000 shares.

Then, on March 3, the narrative took a dramatic turn: two insiders — including CEO Stéphane Bancel — scooped up nearly 200,000 shares, investing about $6 million. Bancel accounted for $5 million of that sum.

This move is telling. Bancel already controls over 21 million shares. You don’t drop another $5 million into a stock unless you believe you're buying Manhattan for beads and trinkets. The contrast is stark: when prices were high, executives couldn’t sell fast enough. Now, they’re buying.

The timing of these insider purchases is even more intriguing. Moderna had just slashed its 2025 revenue target by $1 billion, bringing guidance down to $2.5 to $3.5 billion. Yet, insiders chose that precise moment to buy, signaling confidence that sales will bottom out this year.

The company's drug pipeline isn't barren, either. Ten drugs are expected to receive FDA approvals by 2027, including a skin cancer vaccine developed with Merck (MRK) slated for a 2027 launch, pending Phase 3 data.

These ten anticipated drugs collectively target a market exceeding $30 billion, with analysts projecting Moderna's revenue to climb to $3.3 billion in 2027 and $4.77 billion by 2028.

On their Q4 '24 earnings call, President Stephen Hoge underscored the cancer vaccine’s potential: "As for INT, obviously, we're all looking forward to the melanoma -- adjuvant melanoma Phase 3 readout. As you know, and as I mentioned, there are additional Phase 3s as well as two randomized Phase 2s, including bladder cancer, renal cell carcinoma, which, depending on the rate of approval of events, could have readouts that we would be updating on as well in the coming years."

Still, the road ahead isn’t without challenges. Moderna expects to burn up to $3.5 billion in cash during 2025, reducing its cash position to $6 billion. Estimated cash costs for 2025 stand at $5.5 billion, projected to decline to $5 billion in 2026.

To reach breakeven by 2028, the company needs to generate $6+ billion in sales at 80% gross margins or implement further cost-cutting measures.

Despite these financial hurdles, Moderna's market cap is a mere $14 billion — practically pocket change for a company with multiple promising vaccine candidates.

There's undeniable risk in buying Moderna at these levels, but historically, the most profitable investments come before the financials improve. The company has effectively announced that its numbers will likely deteriorate further before rebounding — and yet, insiders are still buying.

Speaking of gathering valuable insights from industry leaders, I’ve been preparing for our Mad Hedge Traders & Investors Summit on March 11-13.

After decades in the markets, I’ve learned there’s something uniquely valuable about getting multiple perspectives in one place. It reminds me of my time in Tokyo during the '70s, where real opportunities often emerged from late-night conversations between veteran traders.

Even in today’s volatile environment, the wisdom of those who’ve navigated every market cycle remains invaluable.

In the end, Moderna presents a textbook contrarian opportunity. The stock is deeply out of favor, yet insider buying suggests a potential shift in sentiment as shares hover around $30.

The real question isn’t whether Moderna will recover but whether investors have the stomach to buy when others are still heading for the exits.

As for me, I’m keeping Moderna firmly on my watchlist, right next to my dog-eared copy of "Extraordinary Popular Delusions and the Madness of Crowds."

Some things never change.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

March 11, 2025

Fiat Lux

Featured Trade:

(The Mad Hedge March traders & Investors Summit is ON!)

Global Market Comments

March 11, 2025

Fiat Lux

Featured Trade:

(PROSHARES SHORT S&P 500 ETF LEAPS),

(SH), (SPY)

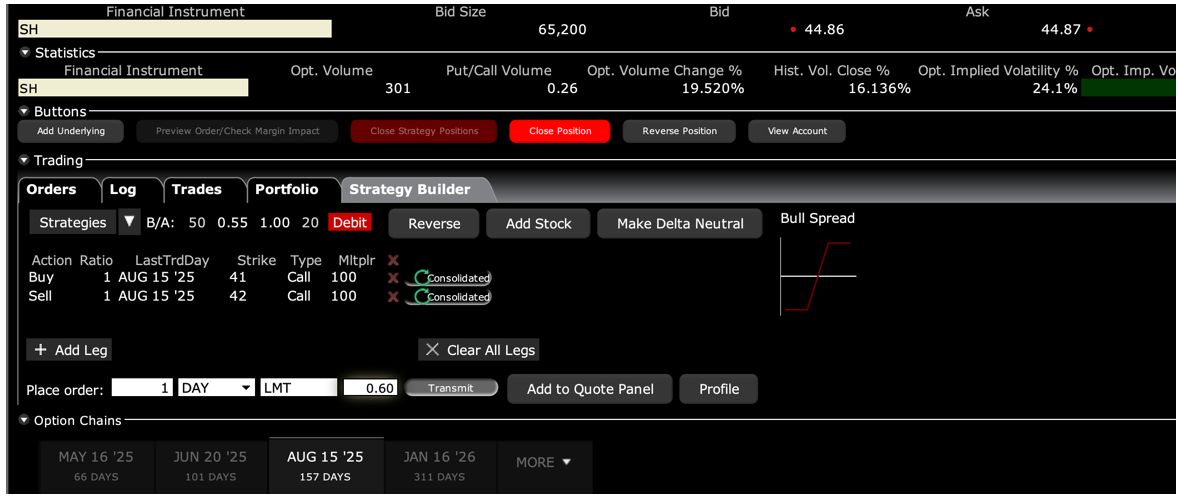

Trade Alert - (SH) – BUY LEAPS

BUY the ProShares S&P 500 ETF LEAPS (SH) August 2025 $41-$42 in-the-money vertical Bull Call debit spread LEAPS at $0.60 or best

If we get any kind of rally over the next few days, you need to add this position, which offers a 66.66% profit in five months.

Opening Trade

3-11-2025

expiration date: August 15, 2025

Number of Contracts = 1 contract

I spent the weekend shopping for downside protection for US equity portfolios, and this is the best one I could find. There are a lot of them designed to do nothing more than pick your pocket, but I think I found a good one.

If the last two weeks have been painful for your long-only portfolio, this is a way to protect it from additional losses. It may also help you sleep better at night. It will also reduce the day-to-day volatility of the net asset value of your account. But like all insurance policies these days, it doesn’t come cheap.

The best thing about this LEAPS is that if we close anywhere above the upper $42 strike price by expiration in five months, you double your money.

Not bad.

Ideally, you will add this position on a day when the stock market is up and the early players are taking profits.

The ProShares S&P 500 (SH) is an inverse ETF that rises in value when the index falls on a one-to-one basis. Its current NAV is $863 million. It makes an excellent hedge for tech-heavy stock portfolios, with a hefty 32.6% exposure to the sector and 7% in Apple (AAPL) alone. If the (SPY) drops by 15% from here by the August 16 option expiration, this fund should rise by 10% to over $46.

I am therefore buying the ProShares Short S&P 500 ETF (SH) August 2025 $41-$42 in-the-money vertical Bull Call spread LEAPS at $0.60 or best.

DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES.

Simply enter your limit order, wait for a few hours, and if you don’t get filled, cancel your order and increase your bid by 5 cents with a second order.

This is a bet that ProShares S&P 500 ETF (SH) will not fall below $42 by the August 15, 2025 option expiration in a little more than 5 months.

There is a catch.

Inverse ETFs have their own special problems and are ideally designed to be traded intraday. They are not cheap. There can be tracking errors, although the (SH) has tracked pretty well over time. There is a contango because the fund managers have to borrow money at around a 6% annual interest rate to buy the futures contracts that the fund invests in.

You also have to cover the cost of paying dividends for the S&P 500, now at a 1.2% annualized rate. There is a derivative risk in that the futures contracts that the fund buys, in theory, could default.

You also have a compounding risk because the fund is reset at the end of every day. That means that if the (SPY) goes up and down frequently over a short period of time, the value of the (SH) will fall.

All in all, the S&P 500 has to drop about 5% by August 16 just to cover all of the costs associated with this short position.

I did take a close look at another ETF, the ProShares Ultrashort S&P 500 ETF (SDS), a leveraged -2X short ETF. The problem here is that with twice the short position, you are paying twice the expenses. The borrowing cost goes from 6% to 12% annualized, and the short dividends go from 1.2% to 2.4%. The (SPY) would have to drop a lot just to cover these expenses unless the drop happens immediately.

It’s great for catching short, sharp selloffs. If you bought the (SDS) on February 18 bottom, you would have made a quick 12% profit on a 6% decline in the (SPY). But for a five-month hold, you are giving up the first 12% move to expenses.

To learn more about the (SH) ETF, please visit their website at https://www.proshares.com/our-etfs/leveraged-and-inverse/sh

Don’t pay more than $0.70, or you’ll be chasing on a risk/reward basis.

Please note that these options are illiquid, and it may take some work to get in or out. Executing these trades is more an art than a science.

Let’s say the Proshares S&P 500 ETF (SH) August 2025 $41-$42 in-the-money vertical Bull Call debit spread LEAPS are showing a bid/offer spread of $0.40-$0.60. Enter a good-until-cancelled order for one contract at $0.50, another for $0.55, another for $0.60, another for $0.65, and so on. Eventually, you will enter a price that gets filled immediately. That is the real price. Then, enter an order for your full position at that real price.

Notice that the day-to-day volatility of LEAPS prices is miniscule, less than 10%, since the time value is so great, and you have a long position simultaneously offset by a short one.

This means that the day-to-day moves in your P&L will be small. It also means you can buy your position over the course of a month just by entering new orders every day. I know this can be tedious but getting screwed by overpaying for a position is even more tedious.

Look at the math below, and you will see that no move in (SH) shares over 6 months will generate a 100% profit with this position, such is the wonder of LEAPS. LEAPS stands for Long Term Equity Anticipation Securities.

Here are the specific trades you need to execute this position. You must place an order for this single vertical debit spread.

Buy 1 August 2025 (SH) $41 calls at………….………$5.60

Sell short 1 August 2025 (SH) $42 calls at…………$5.00

Net Cost:………………………….………..……………......$0.60

Potential Profit: $1.00 - $0.60 = $0.40

(1 X 100 X $0.40) = $40 or 6.67% in 5 months.

To see how to enter this trade in your online platform, please look at the order ticket below, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Debit Spread” by clicking here at

https://www.madhedgefundtrader.com/ltt-vbcs/

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep in-the-money spread trades can be enormous.

Don’t execute the legs individually, or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Keep in mind that these are ballpark prices at best. After the alerts goes out, prices can be all over the map.