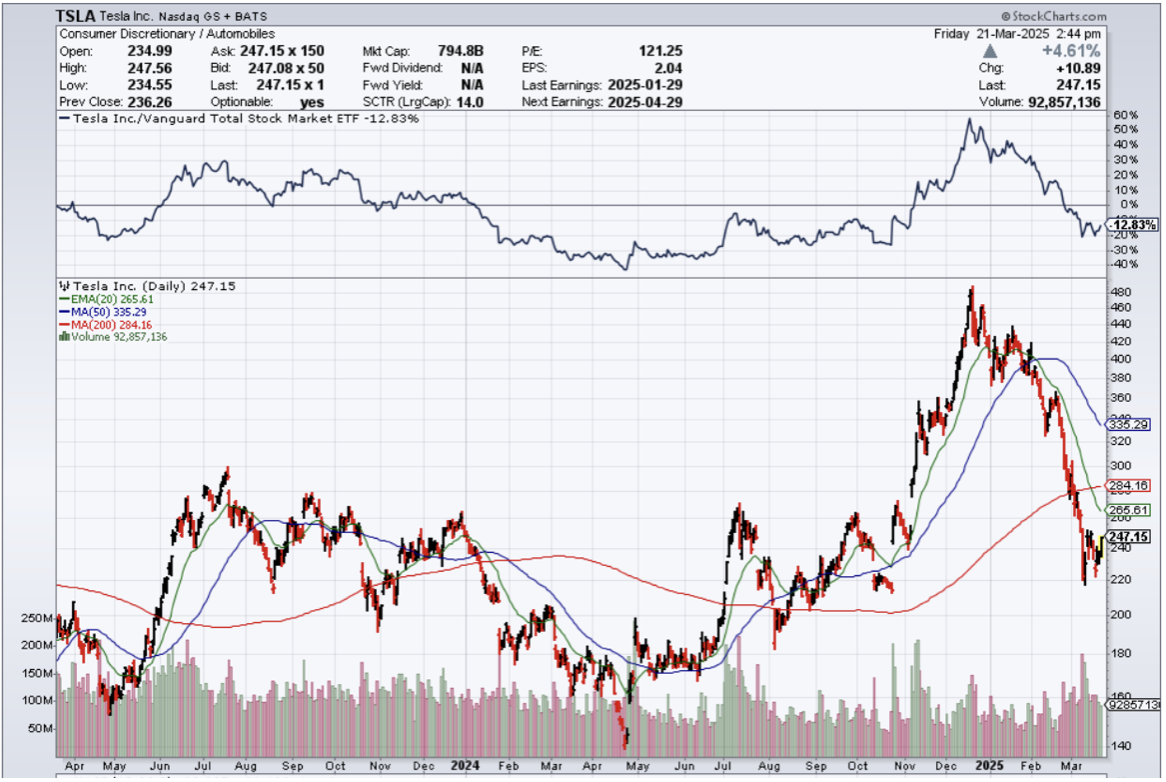

It is a bad look for Tesla (TSLA) when every time you look at a TV and you see Tesla products either getting slyly keyed or engulfed in flames.

That is the type of figure Elon Musk to American society.

Through one lens – he could be considered one of the greatest technologists of all time.

Through another lens – he could be considered a man preventing the flow of Democratic party funding to its NGOs and other party apparatus entities.

Either way – this guy is going to be controversial and his stock has suffered immensely in the short-term.

That being said, one of the richest venture capitalists in the world Peter Thiel who is a remarkable man himself said to never bet against Elon. He might even dislike Musk as well.

Those words are hard to forget as Musk held an impromptu company all-hands meeting on Thursday night, giving an update on the progress of a number of products while also attempting to assuage fears that the CEO is ignoring his post.

Tesla stock has been in free fall since the start of the year, with sales slipping in key regions like Europe and China and even in the US. The changeover to the new Model Y SUV has been seen as a drag on sales.

Overall, Musk maintained that the news was "good" for Tesla and urged employees and others to hold onto their Tesla stock because, in his eyes, the future is bright.

The bet on robo-taxis and autonomous driving is one of the key catalysts for Tesla's future growth, and Musk again laid out his audacious vision.

Key to the company's autonomous vision is the Cybercab robo-taxi, slated for production in 2026. Musk said the factory was already beginning preparations for production using its "unboxed" assembly technique, which would resemble a "high-speed consumer electronics line," rather than an automotive production line.

Speaking of future product production, Musk said Tesla built the "first Optimus at the Optimus production line in Fremont," adding that the humanoid robot would be available for sale in 2026, initially to Tesla employees, after internal company use.

Turning back to the here and now, Musk predicted the Tesla Model Y — the company's most important current product — would once again be the top-selling car in the world following its new update.

To me, it is clear that Musk went the political route because he sensed his robo-taxi and Optimus robot projects were about to be drowned out by bureaucracy.

He probably understands more than anyone that America has become overregulated and it is hard to get stuff done, even if it is a lot more efficient than a place like Europe.

Being in agreement with the current administration has to boost his humanoid robot and robo-taxi project by at least 75% and I wouldn’t be surprised he is attempting to get as much regulatory approval in the next 4 years.

These two projects are what will quadruple the stock in the next 5 or 10 years. He knows that investors know that, and he is doing everything in his power to force the impossible to become possible.

Perhaps Peter Thiel will say that is something Elon Musk would and can achieve.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-21 14:02:442025-03-21 15:29:02Tech Burns Down On TV

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

The U.S. economy is now in recession, but it won’t be confirmed by the data until August.

Stocks have given up all gains since September, losing $5 trillion in market cap in a month.

Interest rate plays are back in favour as recession fears drive rates down.

Deregulation plays take the biggest hits as it never showed.

U.S. dollar enters free fall with declining rates cutting it off at the knees.

Big Technology was the most expensive and saw the biggest falls.

Energy sells off on global recession fears with oil hitting four-year lows.

Cash is king - $1 at market top is worth $10 at the bottom.

THE GLOBAL ECONOMY – GLOBAL FEARS

The economy is now solidly moving into recession.

University of Michigan Consumer Confidence Collapses at 57.0 versus an estimated 63.2 – a four-year low.

Consumer Price Index slows - CPI increased 2.8%.

Small Business Confidence falls off a cliff.

Government to change GDP calculations, knocking out government spending.

Nonfarm payroll report comes in weak at 151,000.

Layoffs hit a five-year high.

Germany passes massive $1.3 trillion spending stimulus devoted to defense spending and infrastructure.

STOCKS – WELCOME TO THE BEAR MARKET

Stocks lost 10% in a month and there is another 10% to go.

NASDAQ is down 14%.

The Volatility index peaked at $30, but there are higher highs to come.

Biggest degrossing since the pandemic has taken place, cutting back of total positions longs and short.

Nvidia was the first stock to attract serious institutional buying.

Tesla has become a no-touch on global boycotts and falling sales.

Markets have flipped from FOMO to capital preservation.

The average American now must work seven more years to get his retirement funds back to where they were a month ago.

Any 3% rally should invite heavy selling and new lows.

Sell first and ask questions later.

China is up 36% this year and German DAX is up 30%.Follow stimulus spending -> China and Germany.

If John had to recommend Chinese stocks to buy, it would be the following: Baidu and Alibaba.

What do you buy at the bottom?

John says buy financials, cyber security stocks, NVDA, AMZN, META, GOOGL, etc.

THE ULTIMATE DEFENCE – Defensive stocks only go down at a slower rate.90-day US Treasury Bills (Warren Buffet owns $300 billion)

Government Guaranteed principal

Endless liquidity, trade like water

100% collateral value for margin

Lock in guaranteed income

Can be sold at any time to earn full interest.

Will survive any bear market.

Ask your broker how to buy.

WORST CASE SCENARIOS

The Bull Case

John says we are now in a recession that will probably cost us -6%, -7% over 2-3 quarters and then ends with a renewal of a $5 trillion tax cut for 2026 (SPY) down 20%-30%, (SPY) multiple drips from 22X to 18X last seen in 2018.

The Bear Case

No tax cut means we enter a depression and lose 25% of GDP over four years.(SPY) down 60%.If (SPY) PE falls from 22X to 9X 240% of stock gains since 2009 have been multiple expansion.

JOHN’S DOWNSIDE TARGETS – S&P500

Depression Worst Case = $250/60% PE 9x.

$535, -12.7% = 1st support

$500, -18.4% = 2nd support

Sell on any rally, add downside protection, and buy outright puts.

SDS – 12%/year = cost of carry, but it is no cost over a 2–3-day period.

BONDS – New Bull Market

Rising recession risks put bonds back in the spotlight.

If the recession happens, the (TLT) easily rises above $100.

During the pandemic recession, the (TLT) rose to $165.

Interest payments on the National Debt already top $1 trillion per year, will become the largest budget item topping Social Security at $1.2 trillion.

Recession risks have suddenly moderated providing more bond support.

Fed will eventually have to cut interest rates, but not now.

Buy (TLT), (JNK), (NLY), (SLRN) and Reits on dips.

FOREIGN CURRENCIES

Prospect of falling interest rates is demolishing the US dollar.

Yen Carry Trade unwind sends Japanese currency soaring.

Expected interest rate differentials are the principal foreign currency driver.

Recession fears are bringing forward Fed interest rate cuts.

The Trump economy is forcing investors to flee all US assets, including stocks and currency.

Massive cash flight is running away from the US and into Europe and China.

Buy (FXA), (FXE), (FXB), (FXC), and (FXY)

ENERGY & COMMODITIES – GLOBAL RECESSION FEARSA

The Oil Market is in turmoil, with crude prices dropping below $66, a four-year low.

A global recession is looming large.

The administration has pulled Chevron out of Venezuela, losing 300,000 barrels a day there.

Tax-subsidized overproduction and increased OPEC quotas are overwhelming demand.

Oil prices have already fallen below 2026 downside targets.

Avoid all energy plays like the plague.

PRECIOUS METALS – NEW HIGH

Falling interest rates have given gold a new lease on life.

The opportunity cost of owning gold has fallen sharply.

Central bank buying never stopped.

Now Silver is starting to play catch-up.

Gold is still the favoured saving means by Chinese who don’t trust their own currency, banks, or government.

That’s why the metals have outperformed the miners which the Chinese don’t buy.

Looking for $5000 by 2028.

Buy (GLD), (SLV), (AGQ), and (WPM) on dips.

REAL ESTATE – STAY AWAY

Pending Home Sales hit an all-time low in January – down 4.6% MOM and 5.2% YOY.

Inventories are rising but affordability is at record lows.

Exceptionally cold weather was a factor.

Homebuilder Sentiment plummeted to 42, a two-year low, amid tariff concerns.

Our drywall comes from Mexico and our lumber comes from Canada.

Avoid all real estate plays like the plague.

TRADE SHEET – THE RECESSION TRADE

Stocks – sell rallies

Bonds – buy dips

Commodities – stand aside

Currencies – buy dips

Precious Metals – buy dips

Energy – stand aside

Volatility – sell over $30

Real Estate – stand aside

NEXT WEBINAR

12:00 EST Wednesday, April 2, 2025, from Incline Village, NV.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-21 10:58:362025-03-21 11:21:10Trade Alert - (GM) March 21, 2025 - EXPIRATION AT MAX PROFIT

Below please find subscribers’ Q&A for the March 19 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: I tried to get into ProShares Short S&P500 (SH), it seems pretty illiquid. How did you get in?

A: Well, before I actually sent out the trade alert, I tested the liquidity of the SH seeing if you could get anything done. This is an easy thing to buy on up days in the market when others are taking profits. It is a really difficult thing to get into on down days in the market because you have so many long-only mutual funds trying to hedge their exposure through buying the (SH). We literally had just one up day at the beginning of the month, and I was able to increase my position tenfold and had no trouble getting my price on the LEAPS at $0.50. If you waited one day, you would have had to pay $0.60 for the same position, and that’s because the volatility explodes on this thing. If you look at the charts, the 1x short play has actually delivered enormous returns, as well as the 2x. It’s outperforming 2 to 1. So you have to buy when other people are selling, that’s the only way to get in and out of the (SH). Of course, I’m buying these things with the intention of running these to expiration.

Q: Is it time to sell US stocks?

A: Yes but only on the up days like today. Don’t sell into a pit, don’t sell into bottoms—wait for rally days like today. That's a good place to reduce risk and add some short positions like the ProShares Short S&P500 (SH) and the ProShares UltraShort S&P500 (SDS).

Q: How did you miss the rotation to Europe and China in emerging markets?

A: Very simple—if you ignore something for 15 years, it’s easy to miss a turn. I also missed the turn in Japan, which I ignored for 35 years. The real reason though is that I underestimated the extremity of this government, its economic policies, and the chaos it would create. I think almost everyone underestimated what the new government would actually do and how it would affect the stock market. If I knew ahead of time that the government would adopt recessionary policies, I would have done everything to get my money out of the US and into Europe and China, but this kind of unfolded with a shock a day, sometimes a shock an hour, and markets don’t like shocks and surprises, so they sold off. The more a stock had gone up in the last six months, the more it went down when the new government came into office.

Q: What are your downside targets for the market?

A: Now that we are in recession, I think any 5% rally off the recent low at 5500, you want to sell. The market could rally 3-5% off the bottom—that would be half of the recent loss. Then you’d want to get rid of more longs, cut your portfolio down to a few very high-quality positions, and add downside protection by buying the ProShares Short S&P500 (SH), the ProShares UltraShort S&P500 (SDS), doing buy rights on the calls and buying outright puts. That would be my recommendation. Eventually I see the S&P 500 falling to 5,000 by the summer, and if I’m wrong, it’s going down 30% to 4,500. That is a deep recession scenario, which we are on the track for unless the government suddenly reverses its draconian policies. This is the most extreme government in American history.

Q: Are you going to use the selloff to get into Costco (COST) after a 20% selloff?

A: Absolutely. I’ve been trying to get into Costco for years and it’s just always been too expensive. They keep increasing earnings every year —investors are willing to pay very high multiples for that. This time around, I am going to get into Costco because they are an absolutely outstanding company. By the way, my mentor at Morgan Stanley was a guy named Barton Biggs, who created the asset management division some 40 years ago. He was close friends with Sam Walton, the founder of Walmart, and Sam Walton was a huge admirer of Costco, which was just starting up then. I’m surprised they never took over the company, which is too big to take over now.

Q: What to buy at the bottom?

A: You want to buy what was leading right before we went into this collapse. Those are financials, and the highest quality profit making of the Mag7 which include Nvidia (NVDA), Amazon (AMZN), Alphabet (GOOGL), Meta (META), as well as cybersecurity stocks like Palo Alto Networks (PANW), Fortinet (FTNT), Zscaler (ZS) and so on.

Q: Why are you making your recession call when we have no evidence of that fact?

A: If you wait for proof of recession, that often is the market bottom. And that could be August of this year. You know, I talk to hundreds of businessmen around the world, and everyone is saying business is slowing. Companies stop making decisions. Customers stop buying. Everyone's afraid of the tariffs. Nobody knows what's going to happen next. Business confidence is terrible. That adds up to a recession, but data tends to move very slowly, so we won't see it in the data for months. If you're a stock trader, you don't have the luxury of waiting for confirmation of the data. By the time you get it, the move is over. But if you cut half of government spending or 12% of GDP, the recession outcome is guaranteed. It's not a speculation. That is the government's goal: to cause a recession, so they can have a recovery going into the next election to take credit for.

Q: If Alphabet (GOOGL) is broken up, what will happen to the company?

A: With all of these big tech breakups, the parts will be worth a lot more than the whole. The individual pieces can be sold off at much bigger premiums creating new companies with more stock liquidity. This is what happened with AT&T (T) in 1982. I participated in that, and the parts were worth more than the original AT&T was within two years. I expect that to happen to Alphabet, and I expect that to happen if Amazon (AMZN) is broken up— eventually, these companies become so big, they become too big to manage. And if the management sees they can get 100% premium on a spinoff, they'll take it so fast it makes your head spin.

Q: None of the 90% gain in stock prices during the Biden administration was a result of his policies.

A: That's absolutely correct. He stayed out of the way, which is the best thing that governments can do—get the hell out of the way. American capitalism on its own will innovate and create profits far faster than any other economic system in history. Biden did quite a good job of staying away.

Q: Why are credit spreads still okay to do in this environment?

A: Because the implied volatility on the options are so high, you can get insane amounts of money—in the money like 30% or 40% —and get trades done and have a 0% chance of taking a loss on that. Suddenly you're being paid double to take risks on these option trades. The classic example is the $88-$90 call spread in Nvidia (NVDA), which we have expiring on Friday, March 21. We never even got close to $90, but the implied volatility on the day we added that trade was a ridiculous 75%. So, it's almost impossible to lose money when you put on trades with implied volatility in the options of 75%.

Q: What's your long-term target on gold now that your last long-term target of 3,000 finally got hit?

A: Yes, we've been recommending gold (GLD) for seven years now. In that time, it's doubled: $1,500 to $3,000. I'm now looking for $5,000 in gold by 2030, in five years. I got a feeling that flight-to-safety plays are going to be very popular in the world going forward. And by the way, people who did look for Bitcoin to protect them in any downturns: Bitcoin actually went down three times faster than the S&P 500 in the last month.

Q: Will stocks rise if the Fed cuts interest rates?

A: No, they won't, because the only reason the Fed will cut interest rates is if inflation falls, and right now, inflation is about to see a big upturn as those import duties of 25% or 50% work their way through the system. A lot of companies are front-running price increases before they even pay the tariffs and try to carve out some extra margin for themselves in advance. On Wednesday, Jay Powell said he expects inflation to rise from 2.5% to 2.8% by yearend and this will prove to be a low number. That is his “president breathing down the back of his next” forecast.

Q: What are your favorite Chinese stocks?

A: Well, a lot of these leading stocks have already gone up 50% or more since the beginning of the year as capital flees the United States and goes abroad. But if you held a gun to my head and said you had to buy two, I would buy Baidu (BIDU), and I would buy Alibaba (BABA). Those would be my Chinese picks. Alibaba is the closest thing you get to an Amazon in China.

Q: Has the dollar hit its lows this year?

A: No. Risk of the next Fed rate move is an interest rate cut. That is going to hang over the dollar and the currency markets for the entire year. And I don't see any recovery in the dollar this year. In fact, it's easy to see much lower lows, and higher highs in the foreign currencies. Buy (FXA), (FXE), (FXC), and (FXB) on dips.

Q: How do you feel about natural gas?

A: I would not be a buyer here. I think we've had a terrific run off of extreme cold weather—believe me, we got some of that in Nevada too—and that is starting to fade now. This is historically when that gas starts to fade for the year. Long term, my view on gas is bullish because of increased exports to China. We have a very pro-energy administration here; that means taking off the export restraints on natural gas, which can only be good for the gas companies and the gas price. China has basically told us they'll take all the natural gas they can get from us because every shipload of gas they buy (LNG) means less coal they have to burn.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Day to day, the stock market is a voting machine; in the long term, it’s a weighing machine,” said the legendary stock analyst Benjamin Graham.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/weighing-scale.jpg212284Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2025-03-21 09:00:152025-03-21 11:00:13March 21, 2025 - Quote of the Day

I was camped out in Kyiv the other month when news of Organon's (OGN) earnings hit my phone.

While Russian drones buzzed overhead, I was studying pharmaceutical balance sheets—talk about surreal. Did I mention I've led a strange life?

In mid-February, Organon pleasantly surprised me with Q4 2024 results. Hadlima, their biosimilar to Humira, rocketed to $44 million in quarterly sales, up 83.3% year-on-year.

Meanwhile, Organon's dividend yield sits at a whopping 7.32%, blowing away the healthcare sector average.

Let me be blunt: this is an income investor's dream hiding in plain sight.

Organon emerged in 2021 when Merck (MRK) spun off its women's health, biosimilars, and off-patent drugs businesses. This allowed Merck to focus on its immunology and oncology pipeline while Organon became a pure-play commercial entity.

These spinoffs often create enormous value that the market misses in the early years.

Organon's share price has been trading sideways since early 2025 despite several wins: commercializing Hadlima, acquiring Dermavant, and maintaining a 23% operating margin even as some medications face generic competition.

The market clearly isn't paying attention. When stocks with this kind of dividend yield maintain solid margins, my antennae start twitching.

Their recent Phase 3 ADORING 3 study showed that even 79.8 days after stopping Vtama treatment, atopic dermatitis remained mild. That's patient retention gold, folks.

When patients can stop medication and still see benefits almost three months later, that's the kind of sticky customer base pharmaceutical execs dream about.

Revenue hit $1.59 billion in Q4 2024, down just 0.63% year-over-year but up 0.63% quarter-over-quarter.

Renflexis sales reached $64 million, down 16.9% due to competition from other Remicade biosimilars and superior new medications like AbbVie's (ABBV) Skyrizi.

But here's where things get interesting—this sales decline was expected and already priced in. Organon isn't being valued in Renflexis's future.

The real stars? Nexplanon and Vtama. Nexplanon sales reached $258 million in Q4, up 11.7% year-on-year.

Even better, its patent protection runs until August 2030. CEO Kevin Ali expects it to "comfortably get beyond $1 billion in 2025."

When a CEO uses words like "comfortably" about billion-dollar projections, I tend to listen.

Vtama, acquired in the $1.2 billion Dermavant purchase, brought in $12 million in partial Q4 sales.

The FDA expanded its label in December 2024 to include atopic dermatitis in patients over age 2—a condition affecting 31.6 million Americans. This approval significantly expands its market potential.

Remember, blockbuster drugs don't announce themselves with trumpets—they sneak up on you through expanded indications and growing prescriber bases.

Now, many folks will point to Organon's debt—$8.36 billion at 2024's end. But that's lazy analysis.

Look deeper and you'll see its net debt/EBITDA ratio improved from 5.01x to 4.74x over 12 months. They're steadily strengthening their financial position.

I've watched this happen before with pharma spin-offs—initial debt concerns gradually fade as strong cash flows tackle the balance sheet.

Management knows what they're doing. For 2025, they forecast a slight revenue dip but improved EBITDA margins of 31-32%, outperforming competitors like Perrigo, Alvotech, and Amneal.

In the broader pharmaceutical landscape, Organon competes with heavyweights like Roche (RHHBY), Ferring Pharmaceuticals, Bayer (BAYRY), Pfizer (PFE), and AstraZeneca (AZN)—but with a more specialized focus that gives them maneuverability these giants lack.

Wall Street's average price target is $20.50, suggesting a 33.9% upside. When was the last time you saw a 7.32% dividend yield with 33.9% upside potential?

I project non-GAAP EPS to reach $4.52 by 2029, slightly above analyst estimates, driven by Hadlima, Nexplanon, and Vtama growth, plus upcoming biosimilars HLX14 and HLX11. My friends at major healthcare funds are starting to take notice, but the broader market hasn't caught on yet.

At $15.31 per share, Organon trades at a non-GAAP P/E of 3.39x—80.8% below the sector median and 25.7% below its 5-year average. That's not just cheap—that's backing up the truck cheap.

You know what they say about bears and bulls making money, while pigs get slaughtered? Well, at these valuations, even a pig could make money on Organon.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-20 12:00:112025-03-20 11:51:38Even A Pig Could Make Money Here

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.