Global Market Comments

April 29, 2025

Fiat Lux

Featured Trade:

(THE NEXT THING FOR THE FED TO BUY IS GOLD)

(GLD), (GOLD), (GDX), (NEM)

Global Market Comments

April 29, 2025

Fiat Lux

Featured Trade:

(THE NEXT THING FOR THE FED TO BUY IS GOLD)

(GLD), (GOLD), (GDX), (NEM)

A huge new buyer may eventually enter the gold market.

That could be a year off, maybe two, or three at the most.

I’ll give you a hint who: your taxes will pay for it.

If true, it could send the price of the barbarous relic soaring above $5,000, or even $50,000 an ounce, a target long led by the tin hat Armageddon crowd.

When I spoke to a senior official at the Federal Reserve the other day, I couldn’t believe what I was hearing.

If the American economy moves into the next recession with rising inflation, a near certainty, its hands will be tied. It dare not cut rates for fear of further fanning the flames.

At that point, our central bank’s primary tool for stimulating US businesses will become utterly useless, ineffective, and impotent.

What else is in the tool bag?

How about large-scale purchases of Gold (GLD)?

You are probably as shocked as I am by this possibility. But there is a rock-solid logic to the plan. As solid as the vault at Fort Knox.

The idea is to create asset price inflation that will spread to the rest of the economy. It already did this with great success from 2009-2014 with quantitative easing, whereby almost every class of debt securities was hoovered up by the government.

“QE on steroids” would involve large-scale purchases of not only gold, but stocks, government bonds, and exchange-traded funds as well.

If you think I’ve been smoking California’s largest cash export (it’s not almonds), you would be in error. I should point out that the Japanese government is already pursuing QE to this extent, at least in terms of equity-type investments.

And, as the history buff that I am, I can tell you that it has been done in the US as well, with tremendous results.

If you thought that President Obama had it rough when he came into office in 2009, it was nothing compared to what Franklin Delano Roosevelt inherited.

The country was in its fourth year of the Great Depression. US GDP had cratered by 43%, consumer prices had crashed by 24%, the unemployment rate was 25%, and stock prices had vaporized by 90%.

Mass starvation loomed.

Drastic measures were called for.

FDR issued Executive Order 6102 banning private ownership of gold, ordering citizens to sell their holdings to the US Treasury at a lowly $20.67 an ounce.

He then urged Congress to pass the Gold Reserve Act of 1934, which instantly revalued the government’s holdings at $35.00, an increase of 69.32%. These and other measures caused the value of America’s gold holdings to leap from $4 to $12 billion.

Since the US was still on the gold standard back then, this triggered an instant dollar devaluation of more than 50%. The high gold price sucked in massive amounts of the yellow metal from abroad creating, you guessed it, inflation.

The government then borrowed massively against this artificially created wealth to fund the landscape-altering infrastructure projects of the New Deal.

It worked.

During the following three years, the GDP skyrocketed by 48%, inflation eked out a 2% gain, the unemployment rate dropped to 18%, and stocks jumped by 80%. Happy days were here again.

However, in the 21st-century version of such a gold policy, it is highly unlikely that we would see another gold ownership ban.

Instead, the Fed would most likely move into the physical gold market, sitting on the bid for years, much like it did in the 2010s Treasury bond market for five years. Gold prices would increase by a multiple of current levels.

It would then borrow against its new gold holdings, plus the 4,176 metric tonnes worth $40 billion at today’s market prices already sitting in Fort Knox, to fund a multibillion-dollar tax cut.

Yes, this all sounds like a fantasy. But negative interest rates were considered an impossibility only a few years ago.

The Fed’s move on gold would be only one aspect of a multi-faceted package of desperate last-ditch measures to resuscitate the economy at some point in the future. The time to start buying gold is RIGHT NOW!

Persistent urban legends and Internet rumors claim that the vault is actually empty or filled with fake steel bars painted gold.

That is, until Treasury Secretary Steven Mnuchin visited the vault on his way to view the solar eclipse at government expense in August 2017.

He says the gold is still there. But only if you believe Steve Mnuchin. A lot don’t.

We’ll never know for sure. Visitors are not allowed.

(GLW), (LUMN), (T)

While cruising down Highway 1 last weekend, I received a call from an old friend who runs one of America's largest data centers. He sounded unusually animated, almost giddy.

"John, you wouldn't believe what's happening with our fiber requirements," he said, nearly shouting over the roar of his Tesla. "We're ordering three times more optical cable than last year, and we still can't keep up with demand."

Why the sudden surge? Two letters: AI.

If you thought the AI revolution was just about software, think again. That intelligence needs a nervous system, and Corning Incorporated (GLW) is perfectly positioned to be the backbone supplier of that infrastructure.

The numbers back this up. In Q4 2024, Corning's optical communications segment saw sales jump a stunning 93% year-over-year. Not a typo - ninety-three percent. This wasn't some fluke quarter either.

For the full year, the segment grew 16%, pushing revenue to $4.66 billion and making it Corning's largest business by sales.

I've been following Corning since my days in Japan in the 1970s when they were pioneering fiber optics. Back then, the technology seemed almost magical - glass strands carrying phone calls.

Today, these same glass threads (albeit vastly improved) are what's enabling AI to function at scale.

Let me break it down. Modern AI systems require absurd amounts of GPU computing power. These processors generate tremendous heat and need to communicate with each other at lightning speed. The faster the speed required, the more fiber connections you need.

It's a perfect storm for Corning.

The company's management team clearly recognizes the opportunity. They've launched what they call their "Springboard Plan" targeting over $4 billion in revenue and 20% operating margins by 2026.

The optical communication segment alone is projected to grow at a 30% CAGR through 2027. For context, the long-term average growth rate for the S&P 500 is 3%.

If you’re still not convinced, let's look at who's buying.

Lumen (LUMN) recently inked a deal to have Corning supply 10% of its global fiber optics for the next two years. AT&T (T) signed a deal worth over $1 billion in late 2024.

When telcos are throwing around billions, you know something significant is happening.

And Corning isn't just talking - they're innovating to meet the moment. In March, they launched their GlassWorks AI Solutions, which can dramatically increase data throughput. Their fiber enables 2-4 times more capacity in existing conduits.

That's crucial because nobody wants to tear up streets to lay new pathways if they can avoid it.

What I find particularly attractive about Corning is that it's not a one-trick pony. Yes, optical communications is driving growth, but the company has diversified segments in display glass, life sciences, automotive, and specialty materials. These provide steady cash flow that can fund R&D and growth initiatives.

In other words, Corning can place big bets on the AI revolution without betting the farm.

The latest earnings report confirms this financial strength. Q4 2024 sales jumped 18% year-over-year to $3.9 billion, but even more impressive was the EPS increase of 46% to $0.57.

Profitability is accelerating faster than revenue - the holy grail for any corporation. Free cash flow hit $1.25 billion for 2024, up a hefty 42% from the previous year.

All this would be moot if the stock was outrageously expensive, but it's not.

Corning trades at a forward P/E of 18.30x, slightly below the sector median of 19.04x and in line with the broader S&P 500 at around 18x.

The forward PEG ratio of 1.12x represents a 21.46% discount to the sector median of 1.42x, suggesting the market hasn't fully priced in Corning's growth potential.

There are risks, of course.

As a global supplier, Corning could face headwinds from President Trump's tariffs and ongoing US-China trade tensions. This could impact both demand for their products in China and the cost of raw materials.

But with 170 years of business experience, Corning has weathered far worse storms.

I remember visiting Corning's headquarters in upstate New York back in the 1980s when I was covering technology for a major business magazine. What struck me was their combination of cutting-edge science with old-school manufacturing discipline.

That culture persists today, and it's exactly what's needed to capitalize on the AI infrastructure boom.

So is Corning a worthwhile investment? At its current price, it offers an attractive risk/reward profile for long-term investors. I suggest you buy the dip.

Mad Hedge Technology Letter

April 28, 2025

Fiat Lux

Featured Trade:

(GOOGLE GIVES US SOME GOOD NEWS)

(GOOGL), (NVDA)

I am not saying that Google’s (GOOGL) earnings report will save the market; the market isn’t just GOOGL.

However, the company demonstrated there is still some positive performance out there in the tech sector when many out there are having a hard time.

It is clear that we are about to embark on a journey where big tech actively pulls the levers of shareholder returns to get over the low bar of expectations.

It is true that Google has not innovated for years and is still relying on its cash cow called the Google search engine, to drive ad revenue.

At some point, there will be competition as proprietary technology becomes beatable.

Competition is prompting the company and its rivals to spend heavily on infrastructure, research, and talent. While Google benefits from AI startups spending on its cloud and business tools, it’s also racing to present an answer to popular conversational AI chatbots, which consumers are beginning to think of as an alternative to using Google Search.

Google’s beginning of the answer to that threat — its “AI Overviews” and “AI Mode” in search, in which summarized responses are drafted by generative AI and highlighted ahead of Google’s web links — have seen mixed success. Meanwhile, Google’s AI changes to search have decimated traffic to independent websites across the open web.

Google Cloud brought in an operating profit of $2.18 billion, indicating that Google may be nudging out more profits from Cloud even as sales slow.

The cloud unit is so far the clearest indicator of how the AI boom is contributing to the company’s sales, as startups that require more computing power for their work become customers. Though Google Cloud still lags in third place behind Amazon and Microsoft offerings, it’s one of Alphabet’s most important growth areas.

Alphabet’s board authorized a $70 billion share buyback and boosted its dividend by 5%, to 21 cents a share.

With Google’s search business still holding up at a tough time in global business, I must conclude that Google is doing better than expected.

I believe that we will see a consolidated trend in 2025 of big tech dipping into their huge cash reserves to give back returns to shareholders. Google increasing its dividend by 5% is just the beginning, and we expect bigger returns as we move to the latter part of the year.

There is nowhere to invest in innovation right now in technology, which is why management is quick to buy back stock.

If there is some great project out there, management is keeping it close to its vest.

The long-term problem is that when you fire all the Americans with high wages who secured the company’s success to this point, replacing Americans with cost-cutting employees from India won’t deliver the same amount of innovation as the past in a mature environment.

American tech is supposed to set the bar in innovation, and now they are no,t which is why China is rapidly catching up to Americans on all cutting-edge technology, whether it be EVs or chip manufacturing.

Google is no longer a growth company, and that hurts the stock price.

We could experience a bear market rally that could propel Google along, but that depends on the whims of global politics, which Google has no control over.

If you look at the risk/reward scenario, Google is worth a bullish trade after the wild pullback.

(THE “SELL AMERICA” THREAD HAS TAKEN HOLD)

April 28, 2025

Hello everyone

WEEK AHEAD CALENDAR

MONDAY, APRIL 28

10:30 a.m. Dallas Fed Index (April)

Earnings: Universal Health Services, Domino’s Pizza

TUESDAY, APRIL 29

8:30 a.m. Wholesale Inventories preliminary (March)

9:00 a.m. FHFA Home Price Index (February)

9:00 a.m. S&P/Case Shiller comp. 20 HPI (February)

9:30 a.m. Australia Inflation Rate

Previous: 2.4%

Forecast: 2.2%

10:00 a.m. Consumer Confidence (April)

10:00 a.m. JOLTS Job Openings (March)

Earnings: Visa, Seagate Technology Holdings, Starbucks, Mondelez International, PPG Industries, First Solar, Extra Space Storage, Caesars Entertainment, Booking Holdings, Sysco, Corning, Sherwin-Williams, Altria Group, Kraft Heinz, Coca-Cola, American Tower, Pfizer, Regeneron Pharmaceuticals, Royal Caribbean Group, General Motors, United Parcel Service, Honeywell International, Hilton Worldwide, PayPal

WEDNESDAY, APRIL 30

8:15 a.m. ADP Employment Survey (April)

8:30 a.m. ECI Civilian Workers (Q1)

8:30 a.m. GDP Chain Price (Q1)

8:30 a.m. GDP first preliminary (Q1)

8:30 a.m. Chicago PMI (April)

10:00 a.m. Core PCE Deflator (March)

10:00 a.m. PCE Deflator (March)

10:00 a.m. Personal Consumption Expenditure (March)

10:00 a.m. Personal Income (March)

10:00 a.m. Pending Home Sales (March)

11:00 p.m. Japan Rate Decision

Previous: 0.5%

Forecast: 0.5%

Earnings: Prudential Financial, MGM Resorts International, Allstate, eBay, Qualcomm, Public Storage, Microsoft, Meta Platforms, Invitation Homes, Albemarle, Aflac, Hess, yum! Brands, Norwegian Cruise Line Holdings, Caterpillar, GE Healthcare Technologies, Stanley Black & Decker, Humana, Generac Holdings, Western Digital, Martin Marietta Materials, Automatic Data Processing

THURSDAY, MAY 1

8:30 Continuing Jobless Claims (04/19)

8:30 a.m. Initial Claims (04/26)

9:45 a.m. S&P PMI Manufacturing final (April)

10:00 a.m. Construction Spending (March)

10:00 a.m. ISM Manufacturing (April)

Earnings: Apple, Motorola Solutions, Live Nation Entertainment, GoDaddy, Airbnb, Monolithic Power Systems, Amazon.com, Ingersoll Rand, DexCom, Kellanova, McDonalds, Howmet Aerospace, Hershey, Quanta Services, KKR & Co, Eli Lilly & Co, Estee Lauder Companies, Moderna, IDEXX Laboratories, CVS Health, Mastercard

FRIDAY, MAY 2

8:30 a.m. Hourly Earnings preliminary (April)

8:30 a.m. Average Workweek preliminary (April)

8:30 a.m. Manufacturing Payrolls (April)

8:30 a.m. Nonfarm Payrolls (April)

Previous: 228k

Forecast: 130k

8:30 a.m. Participation Rate (April)

8:30 a.m. Private Nonfarm Payrolls (April)

8:30 a.m. Unemployment Rate (April)

10:00 a.m. Durable Orders (March)

10:00 a.m. Factory Orders (March)

Earnings: T. Rowe Price Group, Chevron, Exxon Mobil, Apollo Global Management

Since April 2, investors have been trying to see through the noise of a tariffed landscape – which has seemingly toppled the U.S. from its perceived position of power.

“Sell America” is now a theme in the macro landscape. U.S. equities have slumped, the U.S dollar has been pummelled, and bonds have sold off. This has forced investors into a rethink on the U.S. exceptionalism trade in the future.

Hiding away from the volatility is possible – diversify into a mix of short-term bonds, gold, utilities, and consumer staples. Think of stocks like Coca-Cola, Procter & Gamble, Walmart & Costco. Or you could also think about an ETF – Vanguard Consumer Staples ETF (VDC). This ETF holds Walmart & Costco. You could also look at the Swiss franc currency ETF – (FXF).

Last Friday, stocks closed out a winning week. The Dow Jones Industrial Average ended 2.5% higher on the week. The S&P 500 was up by 4.6%, while the Nasdaq Composite rose by 6.7%.

This week will be busy with more than 180 companies in the S&P 500 set to release results. Of those, 11 companies in the Dow Industrials are expected to report, as well as four of the Magnificent Seven companies – Amazon, Apple, Meta Platforms, and Microsoft.

The Mag 7 - not what they used to be –have been well and truly knocked off the top rung of the ladder – and investors would be wise to stop putting all their eggs in that one basket. While these companies are still expected to show strong earnings in 2025, mostly, the rest of the market, that is, the other 493 S&P 500 companies, are expected to post double-digit earnings growth next calendar year, catching up to the mega cap leadership.

On Wednesday, the Federal Reserve’s preferred inflation gauge – the personal consumption expenditure price index – is expected to show the annual rate of inflation eased to 2.2% in March from 2.5% in February.

Jobs data will be one to watch this week, as it could start to show signs that the labour market is slowing. Nonfarm payrolls on Friday are projected to show the U.S. added 150,000 jobs in April, down from 209,000 previously, according to FactSet data. The unemployment rate is expected to stay at 4.2%.

MARKET UPDATE

S&P500

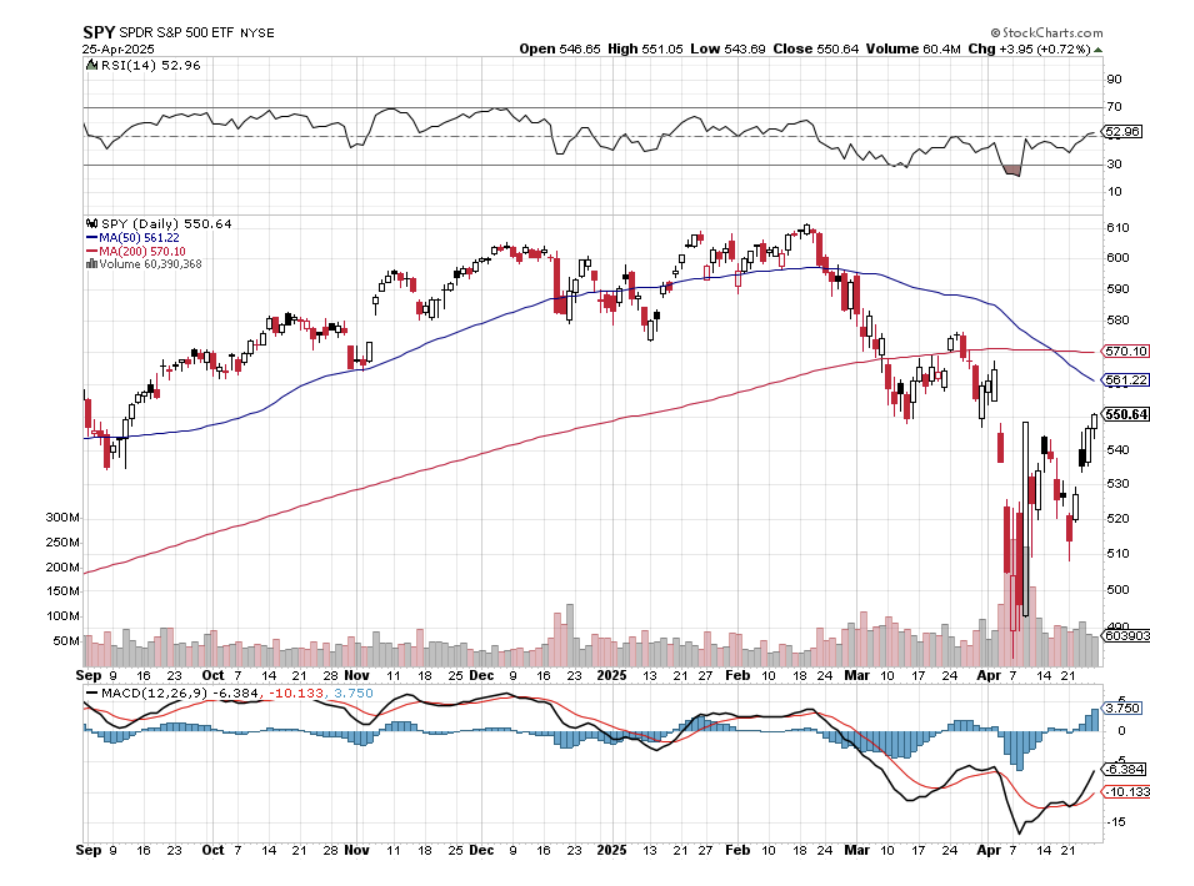

The index is near recent highs in the up move from the April 7th low at 4835, breaking above resistance at 5475/85. This is a near-term positive sign and, along with positive technical data, argues for further gains. We can’t be sure yet whether this will be a pattern of limited ranging or a run back to the Feb high at 6147.

Resistance: $5640/50

Support: $5475/85 & $5350/60 & $5185/95

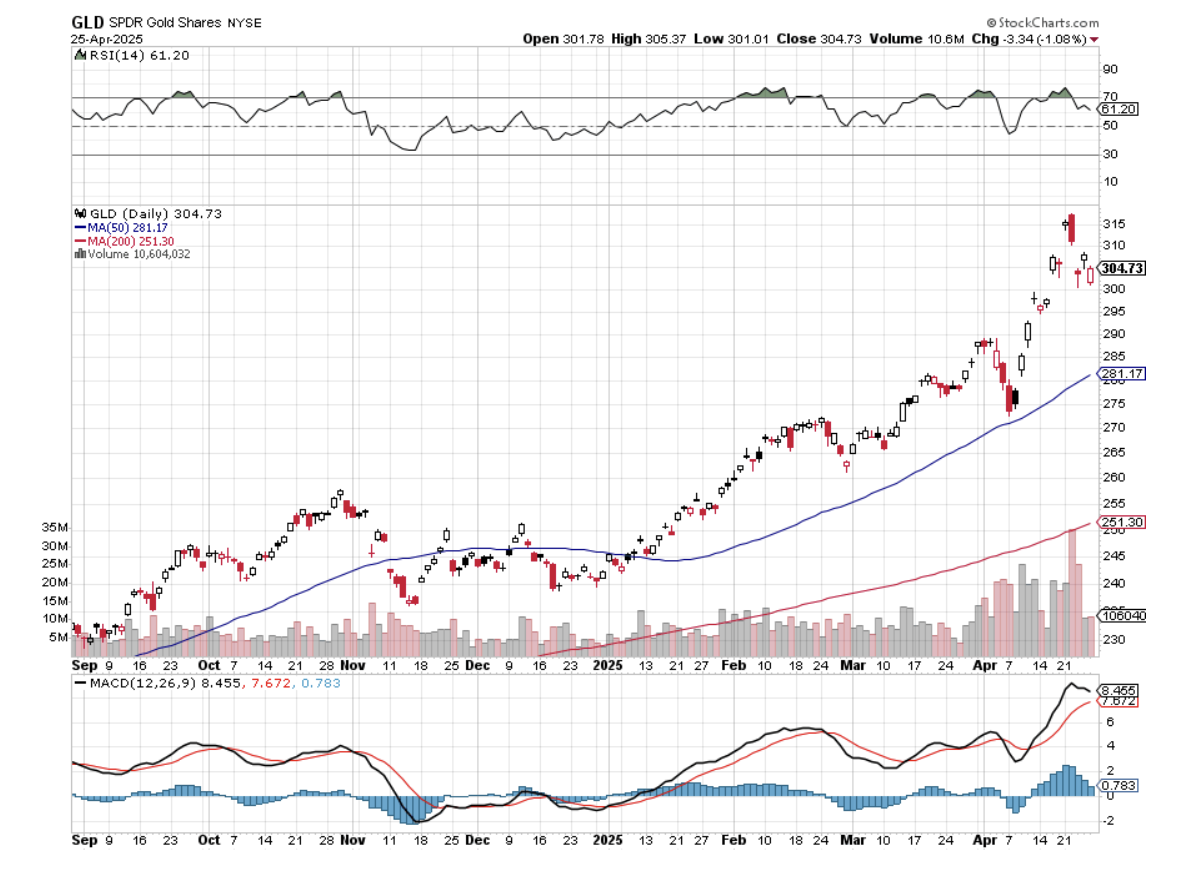

GOLD

Gold has fallen from the April 22 high at $3500. The market was extremely overbought, and this could be the top for at least a few weeks to a month or more. In the short term, there could be more retests towards the high before rolling over.

Resistance: $3367/77 & $3447

Support: $3305/15 & $3257/67 (recent lows) & $3218/28

BITCOIN

There has not really been much change in the big picture view over the last few months. We have seen a large bottoming taking place, with eventual gains above the Jan. peak at 109.40k expected.

The recent rally argues that the final low is likely in place. Bitcoin is now testing resistance at 95.9/96.4k, and this movement could trigger some consolidation for a week or two (not yet confirmed).

On March 17, I suggested several option trades in (IBIT) and (MSTR) that you could enter. A few of these are already in profit, and I expect the rest soon will be.

Further resistance: 98.9/99.4k

Support: 91.3/88.5k

QI CORNER

HISTORY CORNER

On April 28

SOMETHING TO THINK ABOUT

Cheers

Jacquie

Global Market Comments

April 28, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE’S THE BEST-CASE SCENARIO)

(SPY), (TLT), (NFLX), (COST), (NVDA), (TSLA), (MSTR)

Last week, a concierge customer asked me an excellent question. Having correctly called the top in this market to the hour, what would it take for me to go all in on the long side and get maximum bullish?

With everyone now laser-focused on downside risks, which was really a last February game, I thought I’d take the opportunity this morning to examine the upside possibilities, if there are any at all.

Let’s say that the trade war ends before the ninety-day deadline is up on July 9, and the Chinese tariffs are reduced from a trade embargo of 145% to, say, only 20%. Markets will instantly rally 10%, with possibly half of that move happening at a market opening, so you can’t participate.

That is in effect, as what happened last week, with investors willing to look through the trade war to a less onerous business environment sometime in the future. A 20% tariff still takes the US growth rate down to zero, but it at least takes a recession off the table. Problem number one: Zero-growth economies don’t command high earnings multiples.

The problem with that scenario is that we hit a wall of selling above 5,800, where the late entrants came in but are now trying to get out, at close to cost. To get above that level, we need a really powerful fundamental bull case, which is now nowhere on the horizon. That’s why it’s unlikely that the stock market will see any positive returns for 2025.

The reality is that the trade war is not the only place where the economy has been driven off the rails. Even a 20% tariff brings substantially higher prices. International trade is falling off a cliff. Massive cuts in government spending are highly deflationary. Deporting large numbers of immigrants reduces demand and shrinks the labor supply. Unless Congress can pass a budget bill soon, we are on track to see an automatic $5 trillion tax increase by yearend. The budget deficit will hit a new record for this year.

Needless to say, companies will continue to sit on their hands with this amount of uncertainty and wait for the many unknowns to play out. None of these commands higher multiples for equities, let alone the near record S&P 500 multiple at 20X that prevails now.

To really get maximum bullish like I was for most of the last 15 years, the economy would have to return to the conditions that took stocks to record highs like we had until three months ago. That would be a globalized free-trading economy with the US playing a dominant role. That’s an economy that deserves high earnings multiples.

We won’t see that for at least four more years, but markets may start to discount it in only three years as we run up to the next presidential election in 2028. Imagine a future presidential candidate who campaigns on a zero-tariff regime and a return to globalization.

To get a sustainable multi-year bull market in stocks, it would help a lot if we started from a much lower base first. New bull markets don’t start at 20X multiples. A 16X multiple is much more likely, or 20% lower than we are now. We may get that.

The government is currently trying to break up three of the Magnificent Seven with antitrust actions, which led the march to higher stock markets for years. Corporate earnings are now rapidly shrinking, but we won’t see the hard numbers until August. Until then, we only get forecasts. Lower earnings command much lower multiples. That leaves on the table my 4,500 forecast low for the (SPX).

We could well be stuck in a trading range for years. Stocks could continue to bump their heads up against a (SPX) 5,800 ceiling but also get talked up by the administration whenever it collapses towards 4,800. Some 1,000 (SPX) points is quite a wide trading range to play with and plenty enough to make money on.

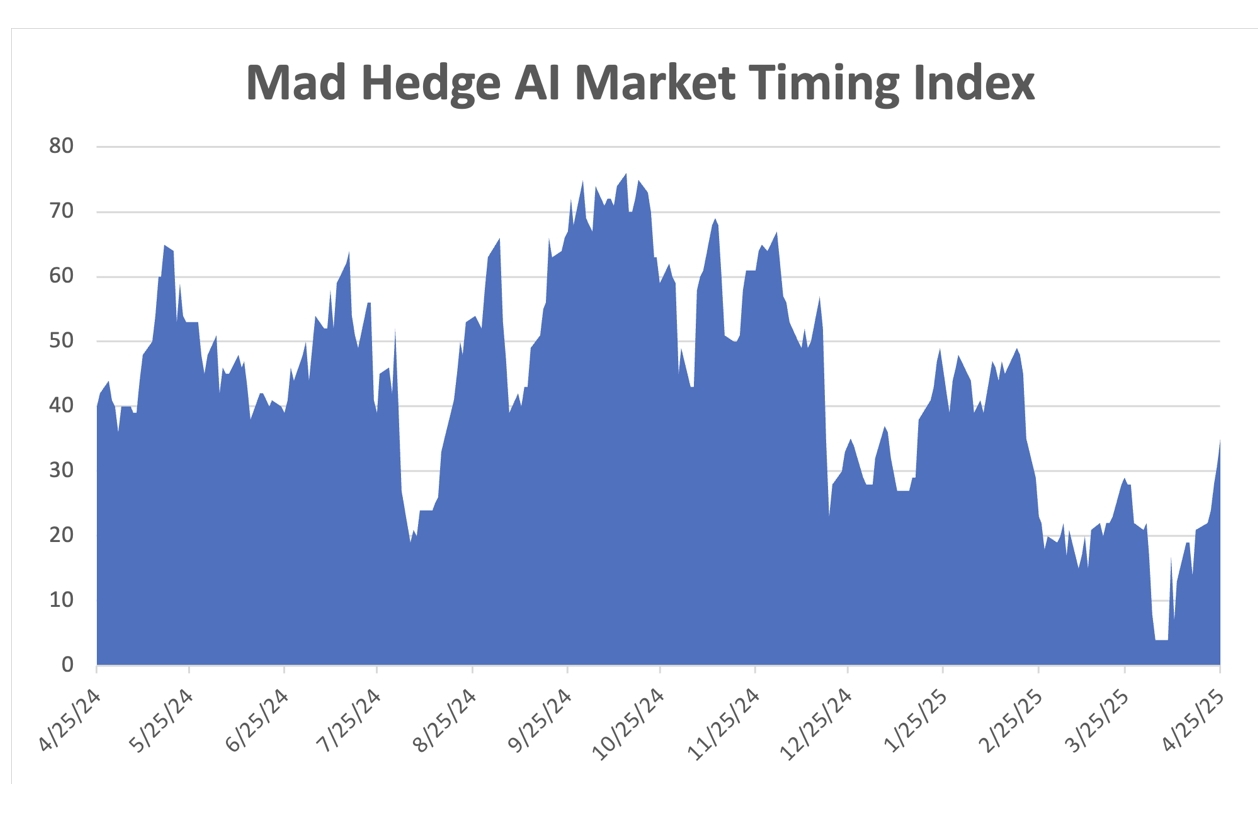

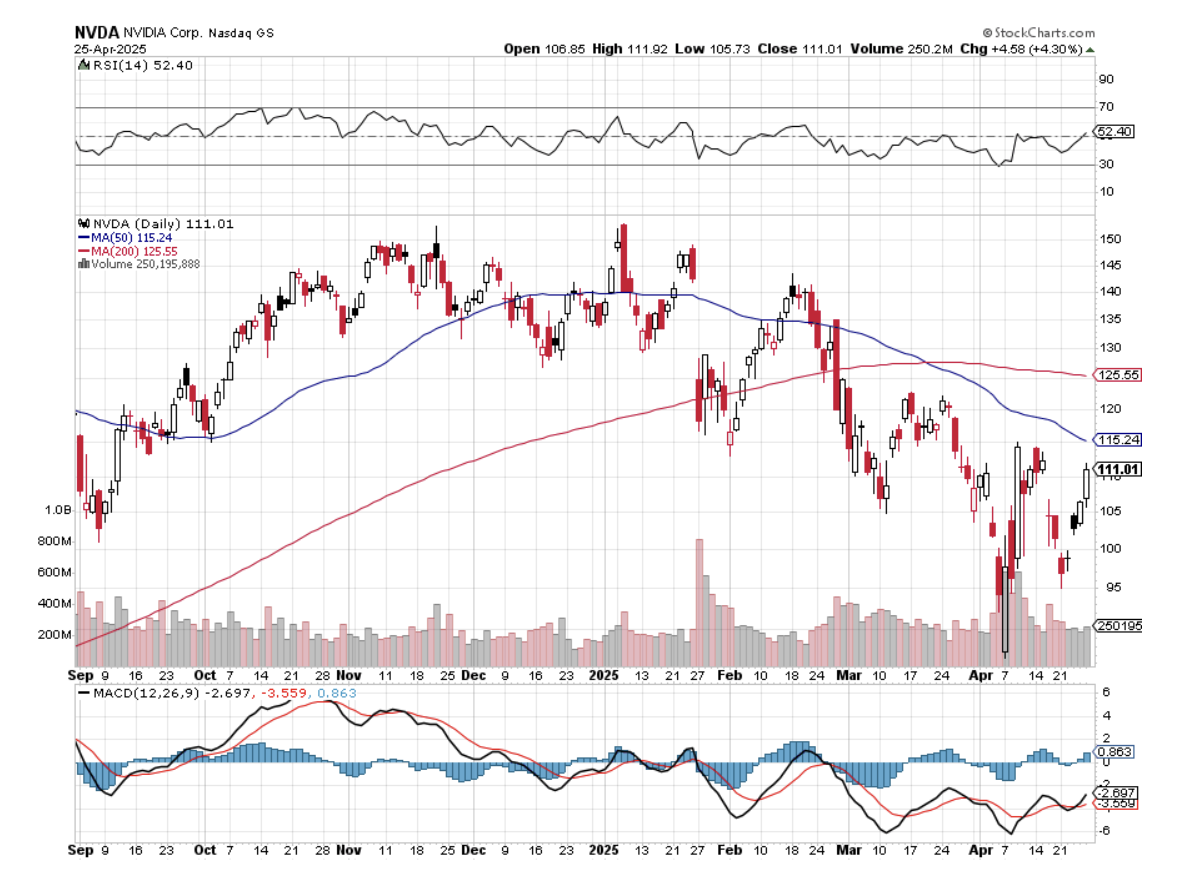

I did it only last week. You have to ignore the news flow and use the volatility index ($VIX) for your market timing. When the ($VIX) hit $54 last week, I piled on longs in (NFLX), (NVDA), (MSTR), and (JPM). By Friday, I gained 8.12% in new performance, my best weekly return in the 17-year history of Mad Hedge Fund Trader.

What if you just want to take a long-term view and not have to check the ($VIX) in between every putt on the golf course?

Gold (GLD) is looking pretty darn good right now. With the collapse of the US dollar ongoing, flight to safety assets is in short supply. American economic conditions will get worse before they get better. Central bank accumulation has continued at its torrid decade-long pace. And gold seems to have broken the link with interest rates that held it back for so long, eliminating opportunity cost as an issue. Even ultra-cautious JP Morgan expects the barbarous relic to reach $4,000 an ounce this quarter.

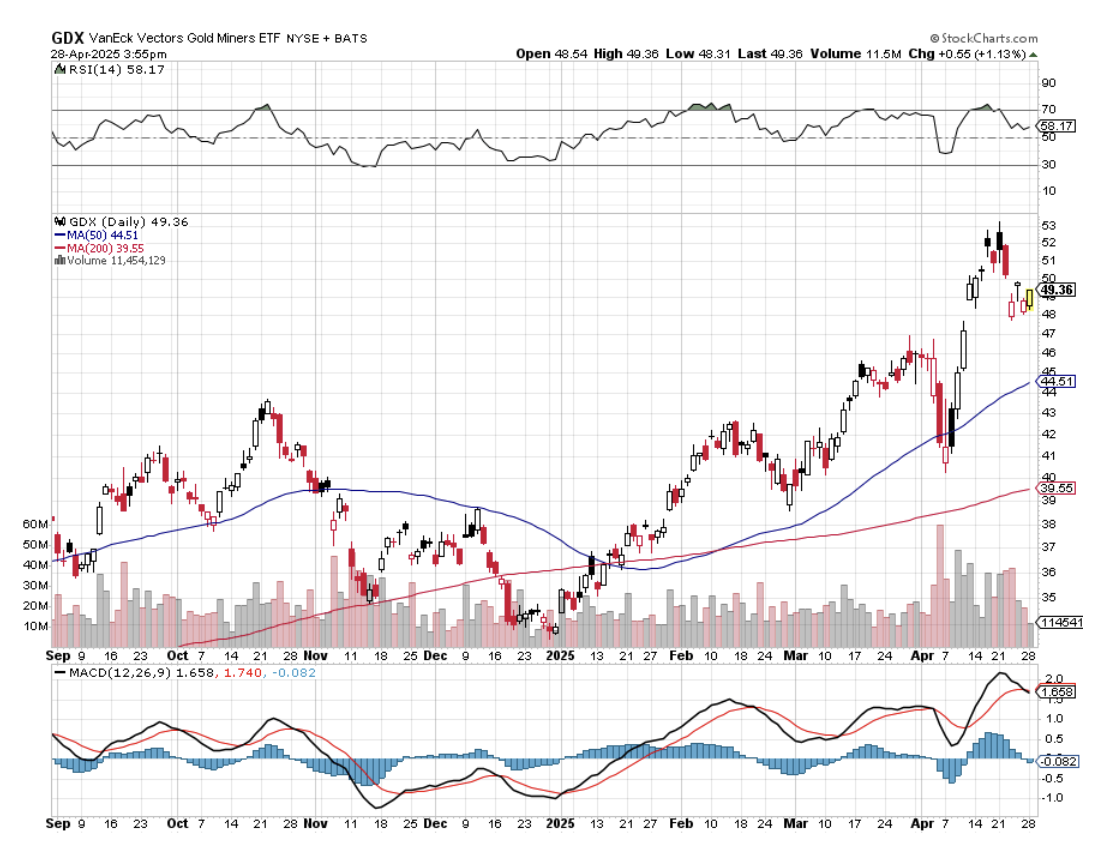

The great mystery in the sector has been the lagging performance of the gold miners. While gold doubled, the shares of Barrack Gold (GOLD) went nowhere.

Gold miners have yet to be taken seriously by mainstream institutional investors, as they are often the subject of excessive promotion, scams, and outright fraud. Token or non-existent dividends are another impediment. Millennials have clearly gravitated towards crypto instead. Miners also got a bad rap from the ESG investment trend as they are considered a “dirty” industry. Anything US dollar-denominated is being dragged down by the weak greenback. That’s why gold only accounts for 0.54% of global portfolios today, versus 2.48% in 1998.

That may all be about to change.

Last week, Barrack Gold, which mines gold at a cost of $1,600 an ounce and sells it at the recent $3,500, completed a monster 23% move in the shares. Newmont Mining (NEM) completed an incredible 32% move. Gold attractiveness is such that only a 5% decline was enough to pull me back in on the long side last week.

High prices atone for a lot of sins.

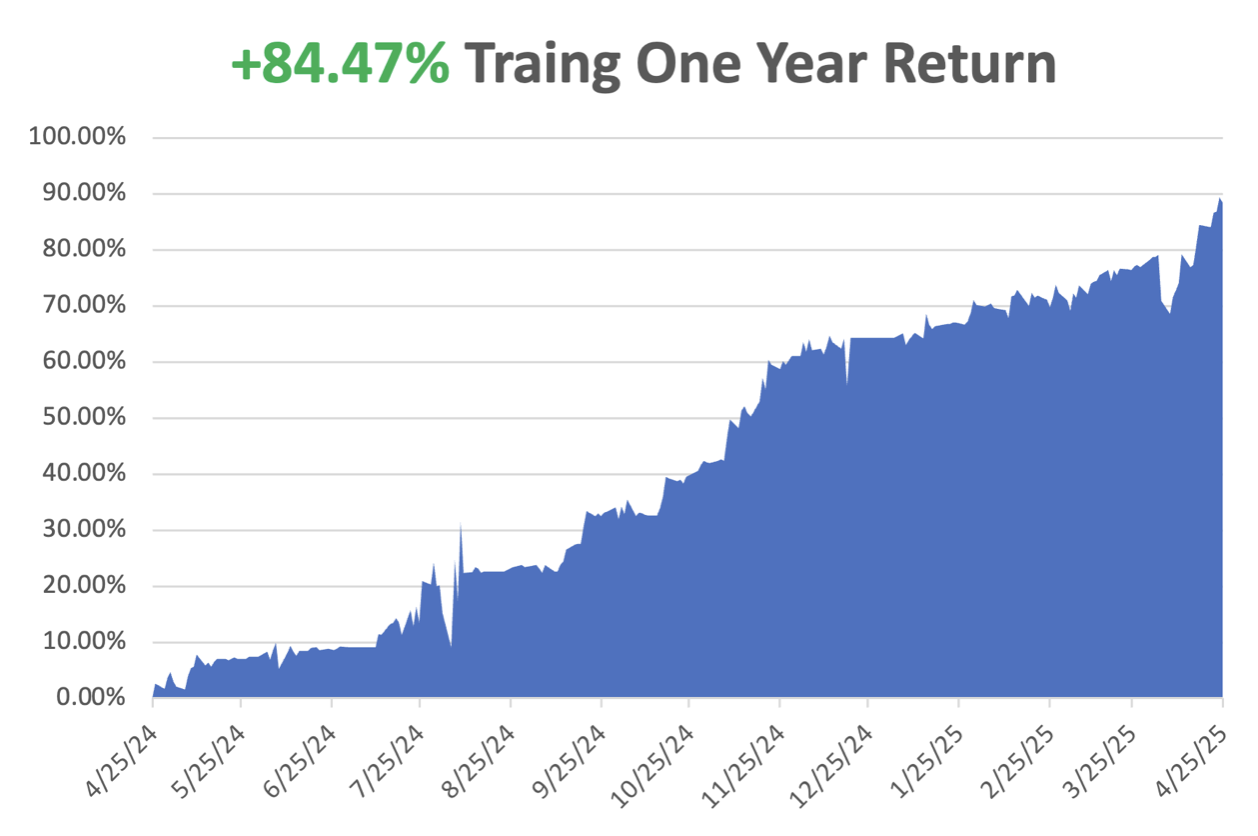

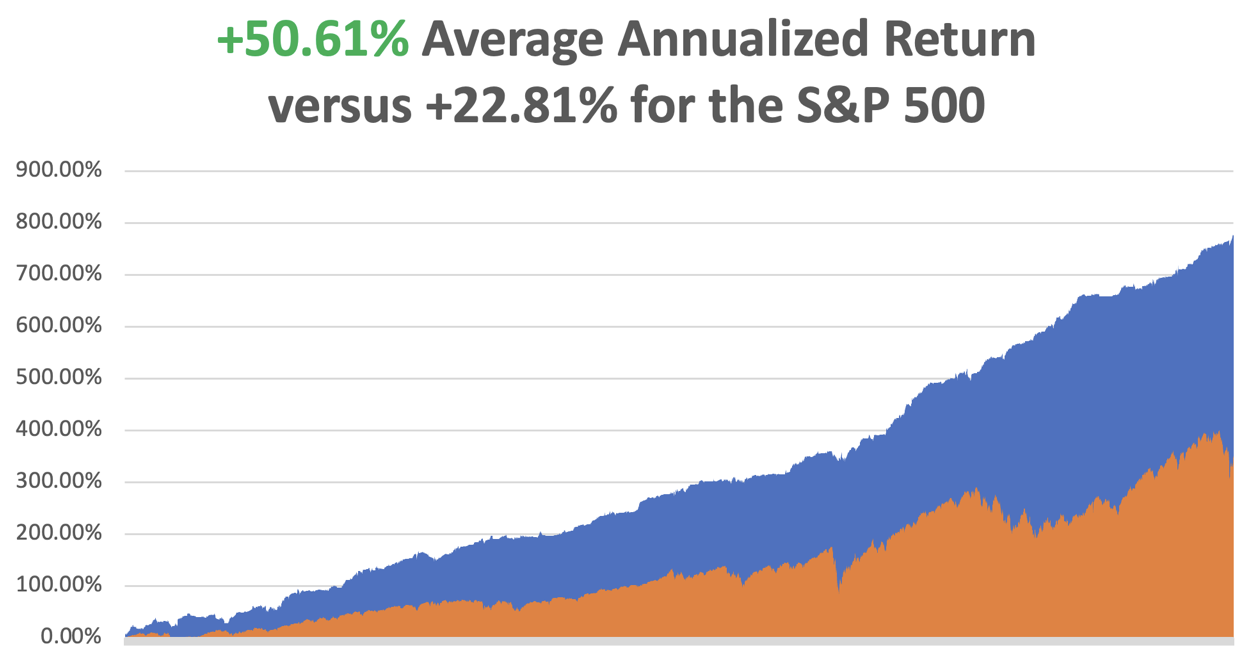

April is now up by a spectacular +10.31%. That takes us to a year-to-date profit of +24.14% so far in 2025. My trailing one-year return stands at a spectacular +84.47%. That takes my average annualized return to +50.61% and my performance since inception to +776.03%, a new all-time high.

It has been another wild week in the market. I used the 1,200-point meltdown in the Dow Average on Monday to add longs in (NFLX), (JPM), and (MSTR). I also quickly covered a short in (MSTR). After the market rallied 2,000 points, I added shorts in (TSLA), (SPY), and a new long in (GLD). That leaves me 40% long, 30% short, and 30% cash. If everything goes our way on the May 16 options expiration day, we will be up 30% on the year.

Some 63 of my 70 round trips in 2023, or 90%, were profitable. Some 74 of 94 trades were profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

Stock Market Suffers the Worst Start to a Year in History. April was the worst since 1932, and lower lows beckon. The Real “Trump Trade” was a “Sell America” trade, with stocks, bonds, energy, and the US dollar all collapsing.

Fed Beige Books Point to Stagflation. Prices are rising and economic activity has begun to slow across parts of the nation as businesses and households try to adapt to Trump’s erratic rollout of sweeping tariffs aimed at reshaping global trade, a report Wednesday from the Federal Reserve showed. Uncertainty around international trade policy was pervasive across reports, the U.S. central bank said.

Leading Economic Indicators Plunge, published Monday by research group The Conference Board, fell 0.7%, to 100.5, in March, following an upwardly revised 0.2% decline in February. Economists polled by The Wall Street Journal had expected a 0.5% decline for March. The recession is here, you just don’t know it yet.

Europe Lowers Interest Rates, down 0.25% to 2.25%, to head off a recession caused by Trump tariffs. The bank’s rate-setting council decided at a meeting in Frankfurt to lower its benchmark rate by a quarter percentage point to 2.25%. The bank has been steadily cutting rates after raising them sharply to combat an outbreak of inflation from 2022 to 2023.

Netflix Earnings rocket, setting the stock on fire, as an indication that the stock may be recession-proof. Netflix reported first-quarter adjusted earnings of $6.61 a share on revenue of $10.54 billion. Analysts surveyed by FactSet expected earnings of $5.67 a share on revenue of $10.5 billion. The stock climbed 3.4% in after-hours trading. As of the market close Thursday, it has risen 9.2% this year. Buy (NFLX) on dips.

IMF Cuts US GDP forecast for 2025 from 2.8% to 1.8%, and they are a deep lagging indicator. The prediction is part of a wide-ranging reduction in global growth. Tariffs are to blame.

US Dollar Hits Three-Year Low, as the flight from American trade accelerates. No trade with the US means no need to buy the greenback.

Gold Tops $3,424, the 1980 inflation-adjusted all-time high. A shortage of “Sell America” trades is driving everyone into gold all at once. The (GDX) gold miners ETF hit a 13-year high. Gold imports are now a major contributor to the US trade deficit.

JP Morgan Targets Gold at $4,000 in Q2, as the “Sell America” trade gathers steam. Central banks are the big winners here, which have been hoovering up the barbarous relic for years.

Tesla Bombs, with Q1 earnings down a gob-smacking 71%, a four-year low. Sales are in free fall globally. Tesla’s cost of making and selling vehicles dropped over 17% year over year, driven by lower raw material prices and reduced expenses of ramping up Cybertrucks production. Automotive gross margin for the period, excluding regulatory credits, was 12.5%, down from 30% a year ago, compared with expectations of 11.8%. Tesla short sellers have earned $11.5 billion so far this year, including myself, with the stock down 55%. The shares rose $10 on news that Elon Musk will spend significantly less time with DOGE. Buy only the biggest dips in (TSLA).

Record Funds are Pouring into Japan. Overseas investors have bought a net ¥9.64 trillion ($67.5 billion) of the Asian nation’s debt and equities so far in April, according to preliminary weekly figures released by the Ministry of Finance on Thursday. That level is already the most for any month on record, based on balance-of-payments data going back to 1996. What was the only thing Warren Buffett was buying last year? Japanese trading companies.

Existing Homes Sales Hit 16-Year Low. Sales of previously owned US homes fell 5.9% in March to an annualized rate of 4.02 million, the weakest March since 2009. The median sales price increased 2.7% from a year ago to $403,700, a record for the month of March and extending a run of year-over-year price gains dating back to mid-2023.

Apple to Move All iPhone Production to India. It is a move that has been underway for some time due to China’s soaring labor costs. Since I began covering China in the early 1970s, China's average annualized income has risen from $300 a year to $16,000, up 5,300%.

Alphabet (GOOG) Beats, after the company topped Wall Street estimates and showed growth in its advertising and search business. The company suggested that it’s too soon to tally the impact of Trump’s tariffs, but the ending of the de minimis loophole could create a “slight headwind” to its advertising business. The really interesting number was Alphabet’s estimate of a potential market size of 4 billion rides a year for its Waymo autonomous driving taxi service.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, April 28, at 8:30 AM EST, the Dallas Fed Manufacturing Index is announced.

On Tuesday, April 29, at 3:30 AM, the S&P Case Shiller National Home Price Index is released. We also get the JOLTS job openings report.

On Wednesday, April 30, at 8:30 PM, the Q1 GDP growth rate is published, as is the CPI for April.

On Thursday, May 1, at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, May 2, at 8:30 AM, we get the Nonfarm Payroll Report for April.

As for me, when I was shopping for a Norwegian Fjord cruise a few years ago, each stop at a port was familiar to me because a close friend had blown up bridges in every one of them during WWII.

During the 1970s at the height of the Cold War, my late wife Kyoko flew a monthly round trip from Tokyo to Moscow as a British Airways stewardess. As she was checking out of her Moscow hotel, someone rushed up to her and threw a bundled typed manuscript that hit her in the chest.

Seconds later, a half dozen KGB agents dog piled on top of Kyoko. It turned out that a dissident was trying to get her to smuggle a banned book to the West. She was arrested as a co-conspirator and bundled away to the notorious Lubyanka Prison.

I learned of this when the senior KGB agent for Japan contacted me, who had attended my wedding the year before and filmed it. He said he could get her released, but only if I turned over a top-secret CIA analysis of the Russian oil industry.

At a loss for what to do, I went to the US Embassy to meet with Ambassador Mike Mansfield, whom, as The Economist correspondent in Tokyo, I knew well. He said he couldn’t help me as Kyoko was a Japanese national, but he knew someone who could.

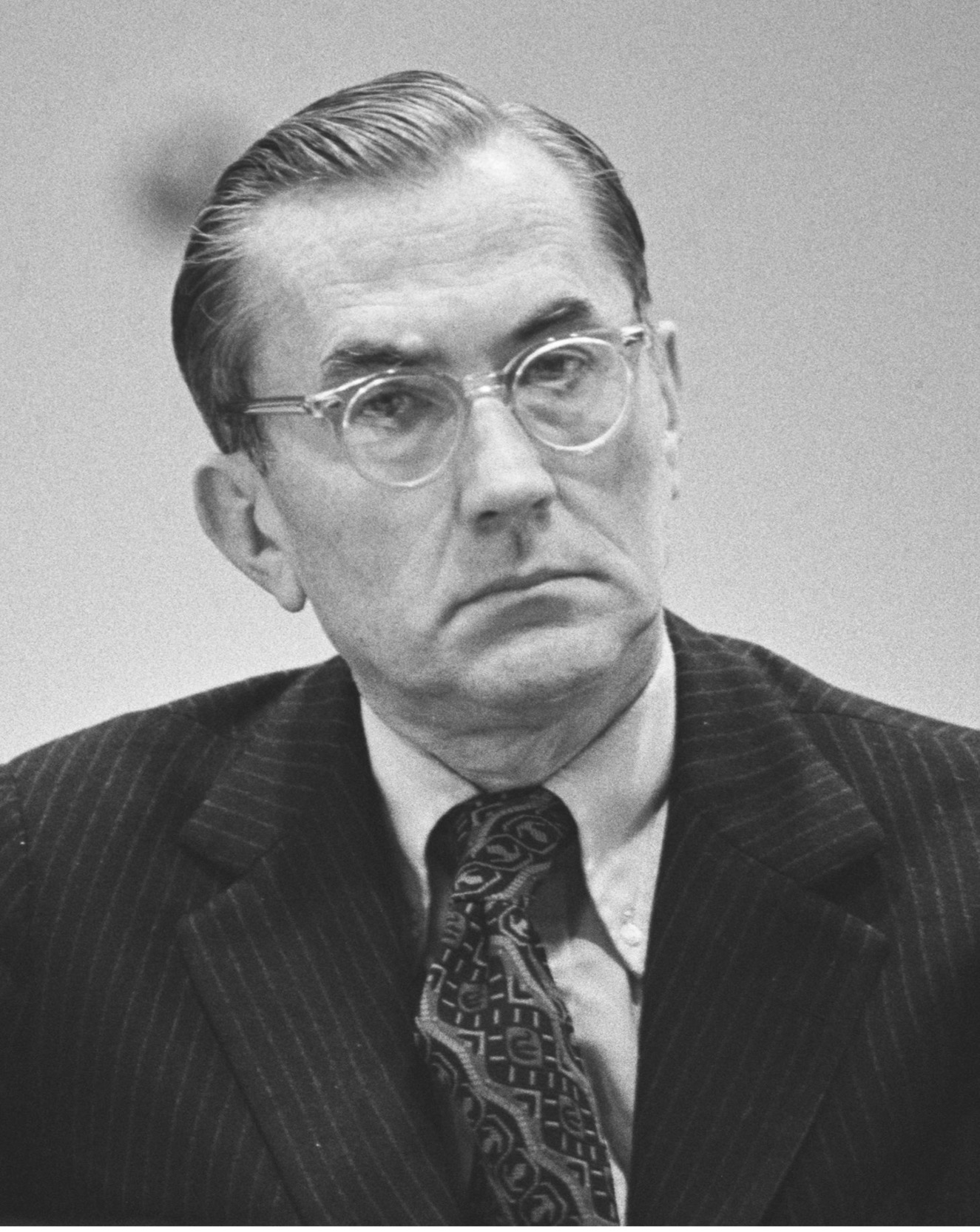

Then in walked William Colby, head of the CIA.

Colby was a legend in intelligence circles. After leading the French resistance with the OSS, he was parachuted into Norway with orders to disable the railway system. Hiding in the mountains during the day, he led a team of Norwegian freedom fighters who laid waste to the entire rail system from Tromso all the way down to Oslo. He thus bottled up 300,000 German troops, preventing them from retreating home to defend from an allied invasion.

During Vietnam, Colby became known for running the Phoenix assassination program. It was wildly successful.

I asked Colby what to do about the Soviet request. He replied, “Give it to them.” Taken aback, I asked how. He replied, “I’ll give you a copy.” Mansfield was my witness, so I could never be arrested for being a turncoat.

Copy in hand, I turned it over to my KGB friend, and Kyoko was released the next day and put on a flight out of the country. She never took a Moscow flight again.

I learned that the report predicted that the Russian oil industry, its largest source of foreign exchange, was on the verge of collapse. Only a massive investment in modern Western drilling technology could save it. This prompted Russia to sign deals with American oil service companies worth hundreds of millions of dollars.

Ten years later, I ran into Colby at a Washington event, and I reminded him of the incident. He confided in me, “You know that report was completely fake, don’t you?” I was stunned. The goal was to drive the Soviet Union to the bargaining table to dial down the Cold War. I was the unwitting middleman. It worked.

That was Bill, always playing the long game.

After Colby retired, he campaigned for nuclear disarmament and gun control. He died in a canoe accident on the lake in front of his Maryland home in 1996.

Nobody believed it for a second.

William Colby

Kyoko

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

April 25, 2025

Fiat Lux

Featured Trade:

(THIS TECHNOLOGY IS A FLOP)

(META), (AAPL), (MSFT)