“If horses could have voted, there never would have been cars,” said my friend, Tom Friedman, a columnist at the New York Times.

“If horses could have voted, there never would have been cars,” said my friend, Tom Friedman, a columnist at the New York Times.

Argentina’s financial sector is in the midst of a profound transformation, driven by a unique blend of economic necessity and technological innovation. For decades, a history of high inflation, currency controls, and economic uncertainty has shaped a complex environment where traditional banking models have struggled. This has created a perfect storm for the rise of fintech, with software developers and artificial intelligence (AI) now partnering to revolutionize the industry. This collaboration isn’t just about efficiency; it’s a fundamental shift that is empowering new digital banks and forcing traditional institutions to adapt rapidly to avoid losing market share.

Argentina’s turbulent economic history has been an unexpected catalyst for its robust fintech ecosystem. With the value of the peso constantly under threat, many Argentinians have sought alternatives to traditional savings and payment methods. Digital solutions that offer stability, accessibility, and protection against inflation have found a receptive audience. For instance, the use of digital wallets and stablecoins, which are cryptocurrencies pegged to the U.S. dollar, has grown significantly.

This demand has been met by a burgeoning fintech scene. The number of fintech companies in Argentina more than doubled from 2019 to 2024, a clear sign of the sector’s rapid growth. The Argentine Central Bank has also contributed to this shift by introducing initiatives like Transferencias 3.0, an interoperable digital payment system that has made real-time transactions a common reality. This regulatory support, combined with a populace eager for new financial tools, has made Argentina a key player in the regional fintech landscape.

At the core of this transformation is the symbiotic relationship between skilled software developers and cutting-edge AI. Rather than replacing human talent, AI is acting as a force multiplier, allowing developers to build and deploy innovative financial products at an unprecedented speed.

AI-powered developer tools, such as GitHub Copilot, are at the forefront of this partnership. Developers use these assistants to write and test high-quality code faster, which is crucial in the fast-paced financial industry. For example, when Banco Galicia needed to enable free dollar transactions in its app, its developers leveraged an AI tool to expedite the coding process, a task that would have taken significantly longer otherwise. A similar story comes from Naranja X, where developers report saving several hours a day on troubleshooting and writing code, allowing them to focus on more complex, strategic work.

This collaboration enhances more than just speed. It also boosts quality and security. In an industry where a single error can have major consequences, AI can help developers identify potential vulnerabilities and bugs in their code, ensuring that financial applications are robust and secure. AI also democratizes expertise, as a developer can use an AI assistant to tackle a task outside their usual area of specialization, increasing the team’s agility and capacity for innovation. By automating routine tasks, AI frees up developers to concentrate on creative problem-solving and building more sophisticated financial products, from personalized investment tools to more effective fraud detection systems.

The integration of AI is having a profound and dual impact on Argentina’s financial sector, affecting both agile startups and established institutions.

New digital banks like Ualá and Brubank, along with fintech giants like Mercado Pago, have built their business models on the pillars of efficiency and customer-centricity, powered by AI.

Argentina’s traditional banks are not standing still. Faced with fierce competition from fintechs, they are rapidly accelerating their digital transformation efforts.

Argentina’s financial technology sector is set for continued growth. The ecosystem is home to influential players, including unicorn startups and major software development firms that are at the cutting edge of AI implementation. The country is also a regional leader in cryptocurrency adoption, with many citizens using digital assets as a hedge against inflation.

Looking ahead, the collaboration between developers and AI is poised to become even more ingrained. As generative AI becomes more sophisticated, it will take on even more complex tasks, such as generating financial reports and automating compliance checks. The biggest challenge will be ensuring that this technology is used ethically, preventing algorithmic bias and ensuring that the benefits of this digital transformation are accessible to all Argentinians.

In a country where economic uncertainty has long been a constant, AI and software developers are providing a beacon of stability and a pathway to a more inclusive, efficient, and innovative financial future. They are proving that in the face of chaos, technology is the most powerful tool for building a better tomorrow.

Mad Hedge Technology Letter

August 20, 2025

Fiat Lux

Featured Trade:

(CONCERNS ABOUT UBER)

(UBER), (TSLA)

I wouldn’t classify the ride-sharing tech company Uber (UBER) as a tier 1 tech company.

That means they are more susceptible to the twists and turns of the variables they cannot control.

The market got slammed this morning, and there was a general risk-off move that hit tech hard.

The issue I have with non-AI stocks is that they usually don’t rebound as fast nor furiously as tech stocks that fetch the AI premium.

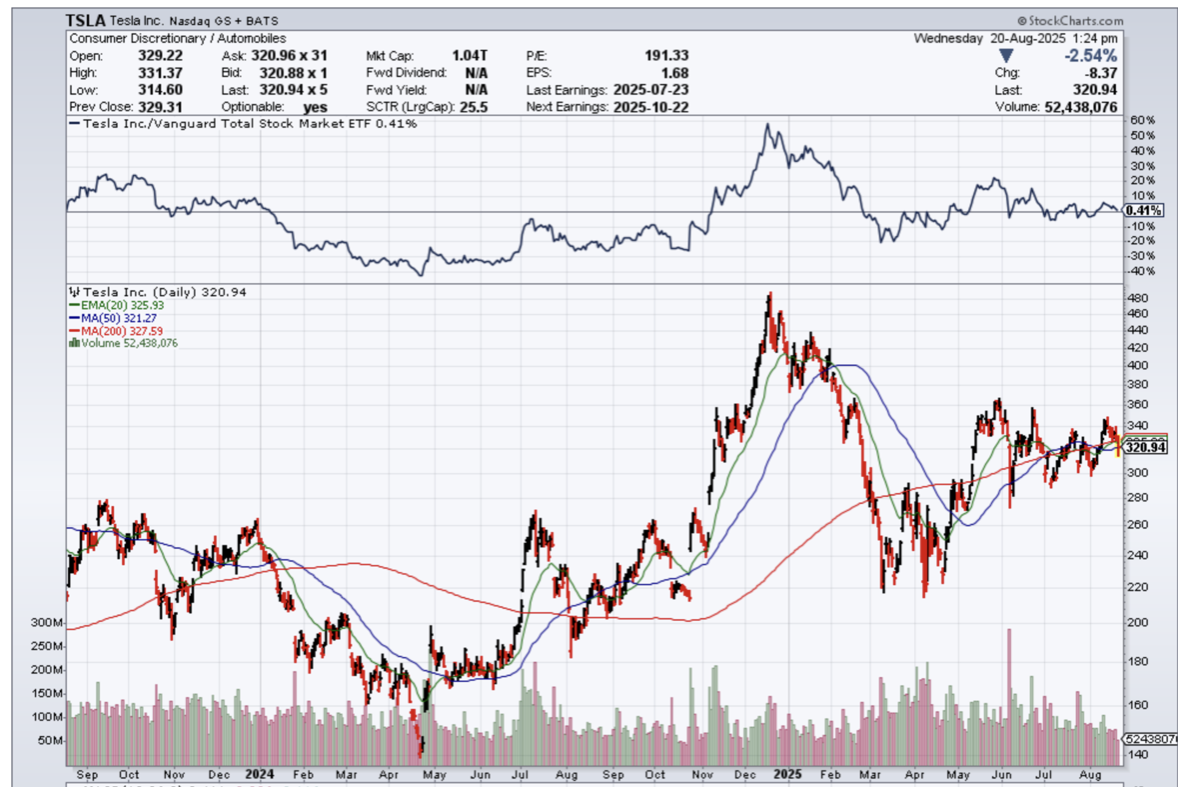

As I write this, Uber is going through an existential crisis with Tesla threatening their business model.

Tesla’s robo taxi business is essentially Uber without the driver, and they produce their own car.

Talking about the emperor with no clothes on!

As the market begins to stumble a little, I took this chance to execute a short position in Uber shares.

In the short-term, I see several vulnerabilities in its business model, with its latest earnings report being a red flag I cannot ignore.

Uber’s company’s total gross bookings of $40.97 billion fell short of the $41.25 billion forecast. This miss in bookings—a critical metric encompassing ride-hailing, food delivery, and freight revenue—signaled potential demand weakness.

Economic uncertainty and high inflation continue to pressure consumer spending, particularly in the ride-hailing sector.

There’s a growing shift toward more cost-effective transportation options, and people could end up riding a bicycle everywhere, considering how expensive grass-fed steaks are at the store.

With an uncertain economy weighing on commuters, demand for premium ride-hailing services may soften, impacting Uber’s ability to raise fares without losing customers.

Uber’s business model, heavily reliant on human drivers, faces existential risks from emerging technologies, particularly autonomous vehicles.

Tesla’s Full Self-Driving (FSD) technology offers a superior experience, potentially disrupting Uber’s core ride-hailing business.

If Tesla scales autonomous ride-sharing faster than Uber, the company could face significant margin pressure, as it would need to invest heavily to compete or partner with autonomous vehicle providers.

The company’s “upfront pricing” strategy, which uses AI to optimize fares and driver pay, has increased its take rate to around 42% by late 2024, up from 32% in 2022.

While this has driven profitability, it risks alienating drivers by reducing their earnings, potentially leading to higher turnover or reduced driver availability.

This could impair service quality and customer satisfaction, further pressuring bookings. Additionally, Uber’s freight segment, with only 2% revenue growth in Q3 2024, remains a drag on overall performance, and the delivery segment (Uber Eats) faces intense competition from DoorDash and others, limiting margin expansion.

I cannot simply ignore the disappointing bookings growth, macroeconomic pressures, competitive threats from autonomous vehicles, and a stretched valuation. These are all no bueno.

I’m not saying that shares of Uber are headed off a cliff, but I really doubt they are going to report great earnings, and it’s time to position myself for that.

Shares of Uber are up over 53% in 2025, and for a non-AI stock, that’s quite miraculous.

I don’t see it.

Uber doesn’t deserve that type of follow-through in its stock at this late stage of the bull market cycle.

I don’t believe that AI will result in the tide lifting all boats, and Uber is due for a nice pullback.

“I don’t create companies for the sake of creating companies, but to get things done.” – Said Elon Musk

(IT’S A JAY POWELL WEEK – WILL INVESTORS GAIN ANY INSIGHT?)

August 20, 2025

Hello everyone

I’m writing this newsletter after five hours of driving to attend a funeral of someone I have known all my life. I drove two and a half hours to get there, attended the funeral, which went for an hour, and then said hello to the family, and then drove two and a half hours to get home in the pouring rain.

So, it’s been quite a day. It’s 6:00 pm my time, and I’m just starting to write this newsletter.

All eyes are on Jay Powell this week. Investors are looking for hints of what he may do at the September meeting.

Let’s not dwell too much on Powell – and what he might say or do. We can talk about it or write about it until the cows come home – that’s still not going to help you.

Instead, let’s look at some opportunities that may be setting up in the market for the long term.

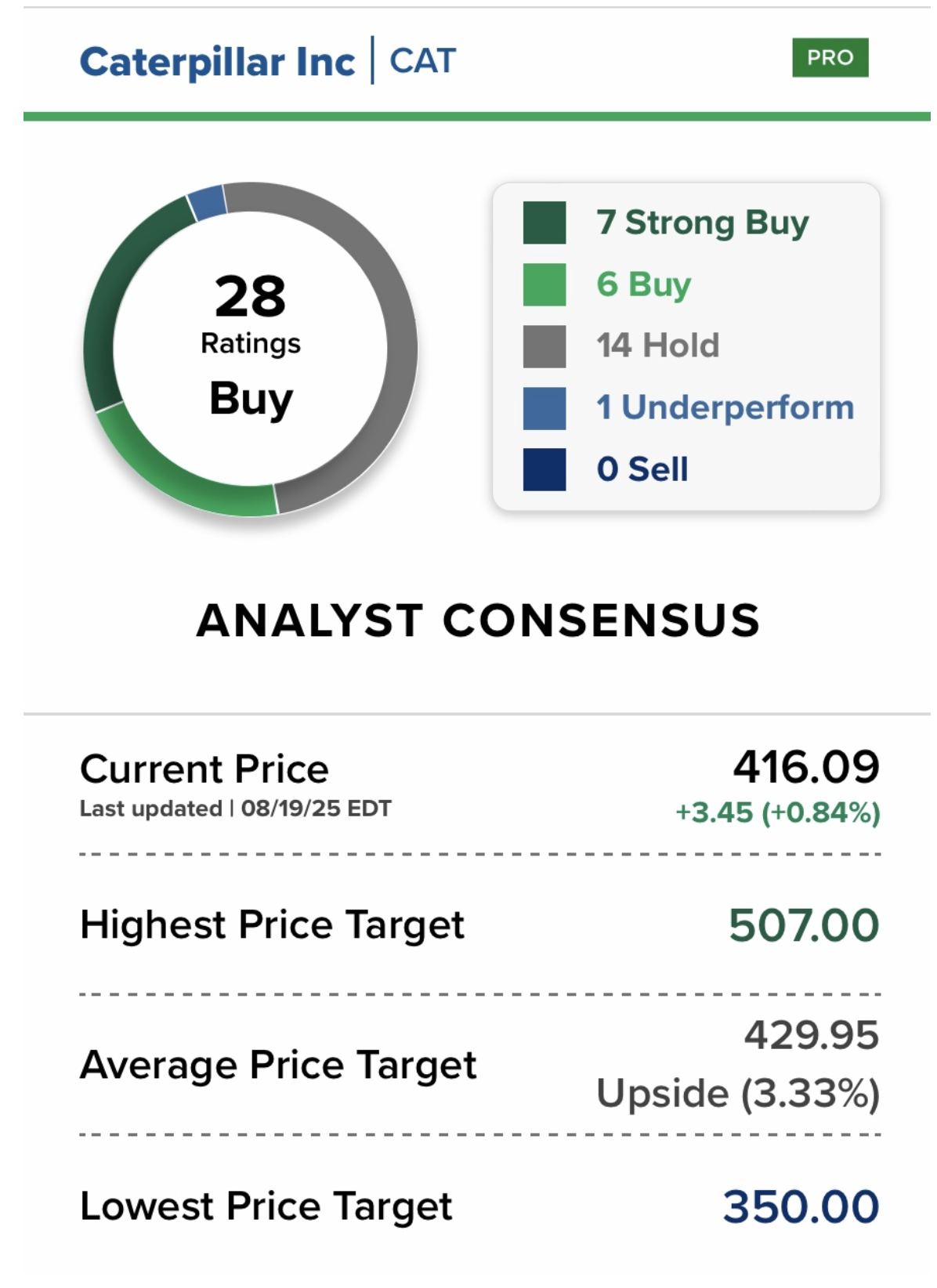

At this stage, I really like Caterpillar (CAT). Look at the chart here. It broke through resistance and has now come down to rest on support, which used to be resistance. The (OBV) On Balance Volume, RSI, and MACD are all converging. The chart is supportive of further movement to the upside.

Importantly, we need to consider (CAT) as like a ‘picks & shovels’ stock for AI. There is already an appetite for the stock via its power gen/data center exposure.

Evercore has upgraded the stock to outperform and raised its price target to $476 per share from $373.

GOLD DEMAND CONTINUES AND PRICE TARGETS KEEP RISING

One of the investment banks, UBS, has just raised its price target for gold next year.

By the end of June 2026, it expects gold to be sitting at around $3,700, up from its original target of $3,500. And by the end of September, it sees the yellow metal at over $3,700.

Driving gold demand are various factors, including the growing deficit and central bank demand, among the most significant. China, India, and Turkey have been major buyers, helping gold overtake the euro as the world’s second-biggest reserve asset next to the U.S. dollar last year.

Keep scaling into those metals’ stocks a little at a time.

Cheers

Jacquie

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Biotech and Healthcare Letter

August 19, 2025

Fiat Lux

Featured Trade:

(THE GRUMPY HUSBAND’S GUIDE TO GETTING RICH)

(NVO), (LLY), (MDGL)

I was having lunch with a buddy in Palo Alto last week when he mentioned that his wife’s doctor just prescribed her Ozempic.

“Cost me eight hundred bucks for a month’s supply,” he grumbled, stabbing his salad.

That’s when it hit me. We’re living through one of those rare moments when an entire industry gets completely reshuffled, and most people are too busy counting calories to notice the real money being made.

The weight loss drug revolution isn’t just changing waistlines, it’s minting fortunes.

Curiously, the Danish company that basically started this whole craze just got absolutely crushed by the market, and nobody seems to care that you can now buy Novo Nordisk (NVO) at fire sale prices.

The story of Novo Nordisk’s recent struggles reads like a perfect storm of competitive pressure and regulatory headaches.

Since the fourth quarter of 2024, the company has been battered by a relentless stream of negative news, while its main competitor, Eli Lilly (LLY), seemingly couldn’t put a foot wrong.

First came the CagriSema phase three results that, while positive, fell short of the street’s lofty expectations.

Then the semaglutide supply issues opened the door for compounders to muscle in on their territory, essentially creating knockoff versions of Ozempic and Wegovy while Novo Nordisk scrambled to meet demand.

Meanwhile, Eli Lilly was busy grabbing market share with their tirzepatide drugs Mounjaro and Zepbound, even publishing head-to-head trial data showing their drug’s superiority over semaglutide.

Add in Eli Lilly’s impressive pipeline advances with orforglipron, their first oral GLP-1 drug, and you had a perfect recipe for investor pessimism around Novo Nordisk.

The company’s stock has dropped 17% since May, and management shocked everyone in late July by cutting their full-year revenue and operating guidance.

But here’s where the narrative gets exciting.

August brought the first real crack in Eli Lilly’s armor when their orforglipron obesity results came in underwhelming, giving Novo Nordisk some much-needed breathing room.

More importantly, the FDA approved semaglutide for MASH treatment just last week, opening up an entirely new revenue stream for Wegovy.

Now, let’s talk about what MASH means in real dollars.

Competitor Madrigal (MDGL) estimates there are 1.5 million diagnosed MASH patients in the United States, but Novo Nordisk believes the actual patient population could be as high as 16 million.

Even if you take the conservative estimate, we’re looking at a multibillion-dollar market opportunity.

Madrigal is already seeing impressive numbers from just 23,000 patients on their MASH drug Rezdiffra, generating over $200 million in quarterly net sales.

Granted, Rezdiffra commands a much higher price than Wegovy, but volume has a way of making up for lower per-unit pricing, especially when you’re talking about treating potentially millions of patients.

The compounder situation, while frustrating, is ultimately a temporary headache.

Novo Nordisk is taking these companies to court, arguing that continued compounding is illegal now that the official shortage has ended. Yes, some compounders are trying to dance around patent protections by claiming “personalized dosing,” but patent law doesn’t typically smile on such creative interpretations.

This legal battle will resolve itself in Novo Nordisk’s favor, it’s just a matter of time.

Looking at the bigger picture, both Novo Nordisk and Eli Lilly are barely scratching the surface in international markets.

The obesity drug expansion has been primarily focused on the United States due to supply constraints, but those days are ending.

International rollout represents massive untapped revenue potential, and Novo Nordisk’s global infrastructure gives it significant advantages in many markets.

The pipeline story remains compelling despite recent setbacks. Beyond CagriSema, which honestly still looks like a solid obesity treatment compared to current semaglutide, the company is advancing high-dose semaglutide that already beat the approved dose in head-to-head trials.

They’re moving oral and subcutaneous amycretin into phase three trials, advancing cagrilintide as monotherapy, and we should see phase one results from their tri-agonist candidate this quarter.

That tri-agonist could potentially rival Eli Lilly’s retatrutide, creating a competitive dynamic that looks very different from today’s narrative.

Perhaps most importantly, Novo Nordisk has a fortress balance sheet with substantial capacity for business development. While their internal pipeline outside obesity and diabetes needs work, their financial resources position them perfectly to acquire promising candidates or entire companies. In biotech, deep pockets often matter more than perfect timing.

The direct-to-consumer angle also deserves attention.

The company just announced a partnership with GoodRx to offer Ozempic and Wegovy at $499 per month for self-paying patients.

While that price point might not drive massive adoption initially, it signals management’s willingness to explore new distribution channels and pricing strategies.

When I look at Novo Nordisk today, I see a company that’s been unfairly punished by a series of unfortunate timing coinciding with a competitor’s hot streak.

The fundamentals remain strong, the addressable markets are enormous, and the recent FDA approval for MASH treatment provides a concrete new growth driver.

This feels like one of those moments where buying the dip makes perfect sense. And who knows? Maybe the next time I’m having lunch in Palo Alto, my buddy will be complaining about how much money he should have made buying Novo Nordisk stock instead of griping about his wife’s prescription costs.

That eight-hundred-dollar monthly bill might just turn into the best investment tip he never took.

Global Market Comments

August 19, 2025

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE FRIDAY, AUGUST 22, INCLINE VILLAGE, NEVADA STRATEGY DINNER)

(THE MAD HEDGE DICTIONARY OF TRADING SLANG)