"The longer you wait to fire someone, the longer it has been since you should have fired them," said Elon Musk, founder and CEO of SpaceX and Tesla Motors.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/05/Fortune-Cooke-Youre-Fired-e1432762960406.jpg196300DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2026-04-20 09:00:022026-04-20 10:58:15April 20, 2026 - Quote of the Day

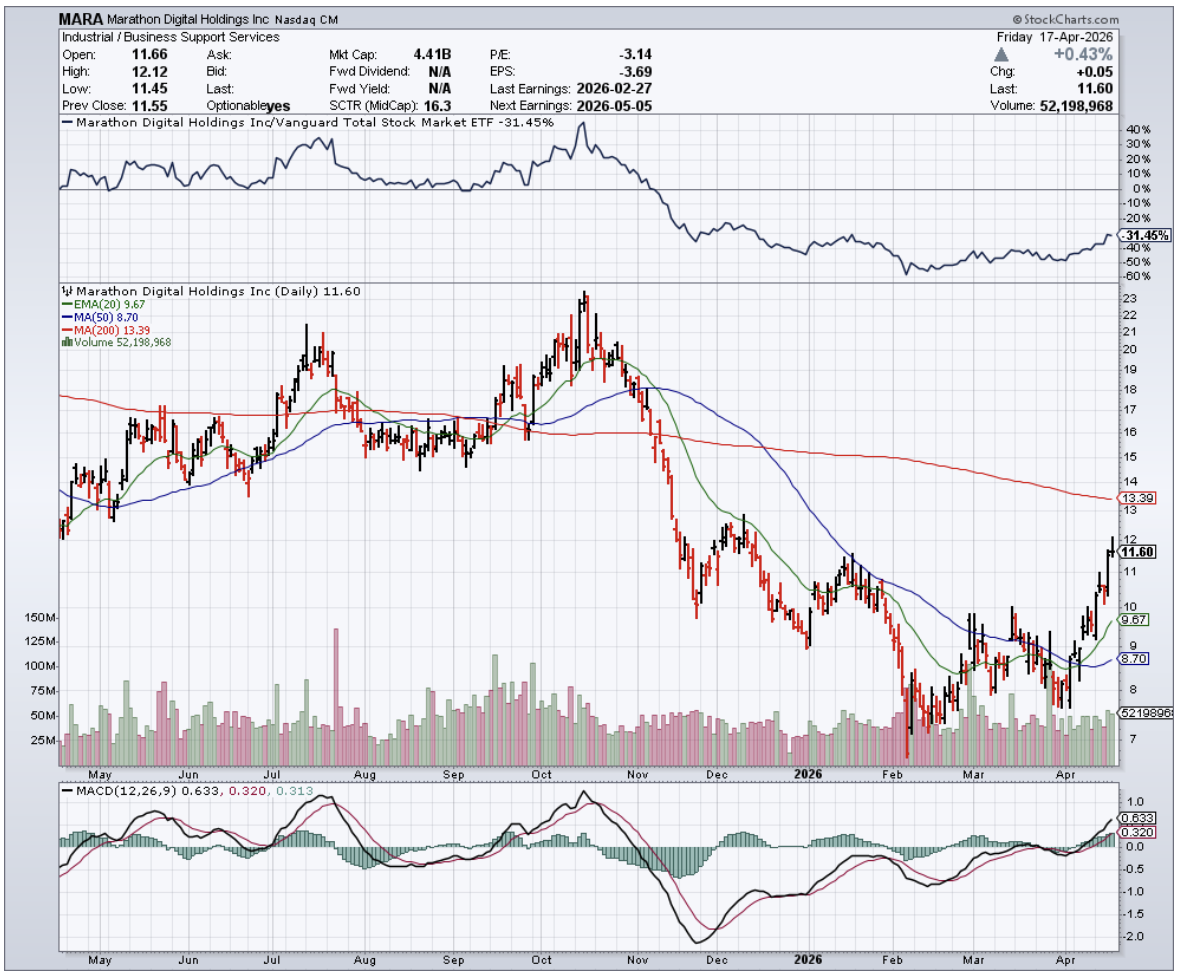

The company now known as MARA Holdings (MARA) started life as Marathon Patent Group, a firm whose primary business was buying up patents and suing technology companies for infringement.

The polite term for this is "non-practicing entity." The impolite term, the one critics used loudly and in public filings, is patent troll.

When that model fizzled around 2018, management pivoted to Bitcoin (BTC) mining. When crypto went mainstream, they rebranded again. Now they're pivoting to AI infrastructure.

Three corporate identities in 15 years. The market has every right to be skeptical, and I understand the instinct completely.

The near-term numbers won't talk you out of that skepticism. Q4 2025 revenue came in at approximately $202 million, down 6%, missing analyst expectations by nearly $50 million.

Daily Bitcoin production fell from 27.1 coins to 21.9, which stings when you consider that the company simultaneously spent money growing its computing power by 25%. More muscle, fewer results.

This is the permanent condition of post-halving Bitcoin mining. Every four years, the block reward gets cut in half, the whole industry keeps piling in anyway, and everyone produces less for more.

G&A expenses ballooned from approximately $19 million to $57 million in a single year, and the company swung from earnings of $1.24 per diluted share to a loss of $4.52.

None of this is a mystery. It's the math of a business model with a structural ceiling.

Which brings us to why the AI pivot is worth taking seriously, even coming from a company with this particular résumé.

Last August, MARA paid approximately $168 million for a 64% stake in Exaion, a computing infrastructure operator that was originally built inside Électricité de France, the French state utility with roughly $122 billion in annual revenues.

EDF didn't sell because it needed the money. It retained a minority stake, stayed on as a paying customer, and sat through a French government regulatory review that scrutinized the deal on national sovereignty grounds. It cleared.

Xavier Niel's NJJ Capital, a name that commands genuine respect in European technology circles, simultaneously took a stake in MARA France as part of the broader arrangement. These are not investors who chase press releases.

The strategic logic is straightforward once you strip away the crypto branding.

MARA already controls the two things AI infrastructure desperately needs and can't conjure overnight: cheap power and physical data center capacity.

Through a separate joint venture with Starwood Capital Group's SDV, it's building toward hyperscale cloud customers using a modular approach that deploys capital in stages rather than in the single massive bets that hyperscalers make.

Faster time to revenue, less capital sitting idle. The company is targeting 1 gigawatt of IT capacity in the near term and says early tenant demand has been strong.

The valuation makes the case on its own.

The forward P/E sits at a multiyear low of 17.77, priced as if the mining business is the whole story. The BTC treasury currently holds approximately 38,689 coins worth roughly $2.9 billion, against a market cap that has been trading in the same neighborhood.

At that math, the Exaion stake, the Starwood joint venture, and 66 exahashes of operating infrastructure are effectively priced at zero.

Obviously, there are risks. BTC sensitivity hasn't gone away, cost discipline is still wanting, and management has a habit of reinventing itself faster than it delivers.

But EDF, Starwood, Niel, and French regulators, who could have simply said no, have all looked at this company and decided to stay in the room.

For a firm that once made its living filing lawsuits, that may be the most valuable intellectual property it has ever produced.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-04-17 13:00:552026-04-24 13:38:36The Troll Under The Data Center

In 1887, two American physicists named Michelson and Morley ran what became the most famous failed experiment in the history of science.

They were trying to detect "luminiferous ether," the invisible medium scientists had believed for centuries carried light waves through the universe.

They found nothing. Ether didn't exist. The null result helped lay the groundwork for Einstein's theory of special relativity, and the concept was buried for good.

Fast forward to 2013: a 19-year-old Russian-Canadian programmer named Vitalik Buterin was scrolling through a Wikipedia list of science fiction terms looking for a name for his new blockchain.

He landed on "Ethereum" because it contained the word "ether," and he liked the idea of his network being the invisible, imperceptible medium that everything else ran on. A dead scientific theory, resurrected as the world's second-largest cryptocurrency.

And now Wall Street is trying to own a piece of it without touching it.

That last part is where ETHA comes in. The iShares Ethereum Trust ETF is BlackRock's answer to investors who want Ether exposure without the crypto wallet, the seed phrase, and the existential dread of accidentally sending $50,000 to the wrong address on an irreversible blockchain.

Launched in June 2024, it now holds $6.86 billion in net assets, custodied entirely through Coinbase Prime, the institutional arm of Coinbase Global (COIN).

One custodian, one exchange, for the entirety of the second-largest cryptocurrency ETF on the market.

ETHA is a Delaware Statutory Trust that holds physical Ether as its sole asset. When you buy shares, you own a fractional claim on that Ether.

You cannot use it to transact on a blockchain or deploy decentralized applications the way direct ETH-USD ownership would allow.

The tradeoff is regulatory compliance, brokerage account accessibility, and no seed phrase to lose.

The expense ratio is 0.25%, shares are created and redeemed in batches of 40,000 by authorized participants, and there's no leverage or derivatives involved.

Now the part that matters for active investors. Since inception, ETHA has returned 49.17% against ETH-USD's 33.52%. That gap looks like alpha. It isn't.

ETHA has been trading at a premium to its NAV, currently 0.33% as of mid-April, driven by institutional demand ahead of the "Glamsterdam Hard Fork," a technical upgrade to the Ethereum network slated for the first half of 2026 aimed at improving throughput and efficiency. That premium ran as high as 0.60% earlier this year before news of potential delays trimmed it back.

When Ether drops and recovers, institutional short-sellers who hedged via ETHA rush to cover, creating a squeeze that further inflates the ETF's price relative to spot.

Historically, ETHA has traded at a discount more often than at a premium; 130 discount days versus 117 premium days in 2025 alone.

Worth knowing alongside ETHA is its newer sibling, ETHB, the iShares Staked Ethereum Trust ETF launched two months ago.

Where ETHA simply tracks Ether's price, ETHB employs a staking strategy to generate yield and is designed to pay distributions, though none have started yet.

Think of it loosely as the difference between holding a stock outright and lending it out for income.

For those who want passive income layered on top of Ether exposure, ETHB is the more interesting instrument.

There's also the trading hours gap. Ether runs 24/7. NASDAQ doesn't.

If Ether surges over a weekend and holds, ETHA gaps up at Monday's open. If it surges and fades before the bell, ETHA's chart looks like nothing happened.

These distortions make short-window performance comparisons between the two almost meaningless.

The annualized volatility is 73%, conservative by crypto standards, given Ether's standing as the second-largest cryptocurrency by market cap.

The Glamsterdam upgrade is the near-term catalyst.

If it executes on schedule, the institutional demand inflating that NAV premium has room to build further. If delays keep accumulating, expect ETHA to revert toward raw ETH-USD performance.

Either way, Ether's investment case ultimately rests on the health of the Ethereum network itself; the same invisible infrastructure Buterin named after a substance that never existed.

The medieval scientists were wrong about ether. Buterin's version, at least, has a market cap.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-04-16 13:00:392026-04-21 10:11:01Ether Way, You're In

Last week, a single Meta (META) employee consumed 328.5 billion tokens in 30 days using Claude Opus 4.6. At published rates, that tab runs $1.9 million. One employee. One month. And Meta didn't flinch.

If you want to understand why CoreWeave (CRWV) just signed two of the largest compute contracts in the short history of AI infrastructure, start there.

The AI bubble crowd has been wrong for three years running, and they're about to be wrong again.

The bear case on CoreWeave always rested on one assumption: that demand for raw compute would plateau as AI companies shifted toward leaner, cheaper inference models. DeepSeek scared everyone in January. The hand-wringing hasn't stopped since.

What the skeptics missed is that Anthropic's new Mythos model, not yet publicly available, is reportedly 5 to 10 times larger than any model ever trained. Pre-training scale, the thing everyone declared dead, is very much alive.

And models of that size don't run on wishful thinking; they run on GPU clusters the size of small cities.

Which is exactly where CoreWeave comes in. Last week, the company expanded its infrastructure agreement with Meta through December 2032, a capacity deal worth $21 billion.

In the same week, CoreWeave inked a separate multi-year arrangement with Anthropic to bring additional compute online starting later this year.

Two of the most aggressive spenders in AI, locking in capacity through the end of the decade, in the same seven-day window.

The financing picture, which spooked investors through most of 2025, is improving faster than the market has priced in.

CoreWeave carries 6x adjusted EBITDA leverage based on FY2025 figures, a number that looks alarming in isolation. Context matters, though.

The company primarily uses asset-backed financing to purchase GPUs rather than the convertible notes that have blown up so many high-growth names before it.

The take-or-pay contract structure means customer prepayments offset a meaningful portion of the upfront capital outlay.

Credit markets are already voting with their feet; spreads on CoreWeave's five-year credit default swaps fell 23% in a single week after the company unveiled an $8.5 billion investment-grade loan facility. When the bond market relaxes, pay attention.

The real insight here sits inside the token economics. Anthropic's revenue has run from $9 billion annualized at the end of 2025 to $30 billion today, even though Claude Opus 4.6 costs roughly 2.6 times more per token than OpenAI's GPT-5 equivalent.

Customers are paying the premium without negotiating. That tells you the bottleneck is capability, not cost.

When AI companies stop haggling over price, the infrastructure providers supplying the underlying capacity operate in a seller's market, and CoreWeave is one of the few scaled sellers that exists.

Still, the risks remain and shouldn’t be glossed over. Execution delays at this leverage ratio are not a nuisance; they are an existential problem.

Vertical integration across the full stack, the only sustainable moat against the hyperscalers long-term, remains unfinished business.

And if the financing market seizes up for any reason, the equity cushion compresses fast. Position size accordingly.

That said, CRWV has recovered most of its early 2026 losses and is pressing against the $115 resistance level that capped every rally since the IPO. The consolidation above $65 has held.

The demand signals coming in from both Meta and Anthropic suggest the market is now baking in a structurally higher CapEx regime through 2027 and beyond.

A decisive break over $115 opens a clean run toward $150, and the January 2027 $120-$130 call spread, currently trading around $4.50, offers a reasonable vehicle for the patient money.

The AI buildout is nowhere near its peak. The customers are not flinching. The only question is whether you want to be the one holding the bill or the one sending it.

One Meta employee spent $1.9 million on tokens last month, and nobody at headquarters lost any sleep. Imagine what the other 70,000 employees are running.

https://www.madhedgefundtrader.com/wp-content/uploads/2026/04/Screenshot-2026-04-15-161411.png6661059Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2026-04-15 16:18:362026-04-15 16:18:36WHAT $1.9 MILLION IN TOKENS TELLS YOU

"Sometimes we stare so long at a door that is closing that we see too late the one that is open," said Alexander Graham Bell, inventor of the telephone.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/06/Father-Son-doors.jpg345227DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2026-04-15 09:00:182026-04-15 14:31:01April 15, 2026 - Quote of the Day

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.