Mad Hedge Biotech and Healthcare Letter

November 19, 2024

Fiat Lux

Featured Trade:

(HONEY, I SHRUNK THE MARKET CAP)

(ABBV), (BMY), (AVNX)

Mad Hedge Biotech and Healthcare Letter

November 19, 2024

Fiat Lux

Featured Trade:

(HONEY, I SHRUNK THE MARKET CAP)

(ABBV), (BMY), (AVNX)

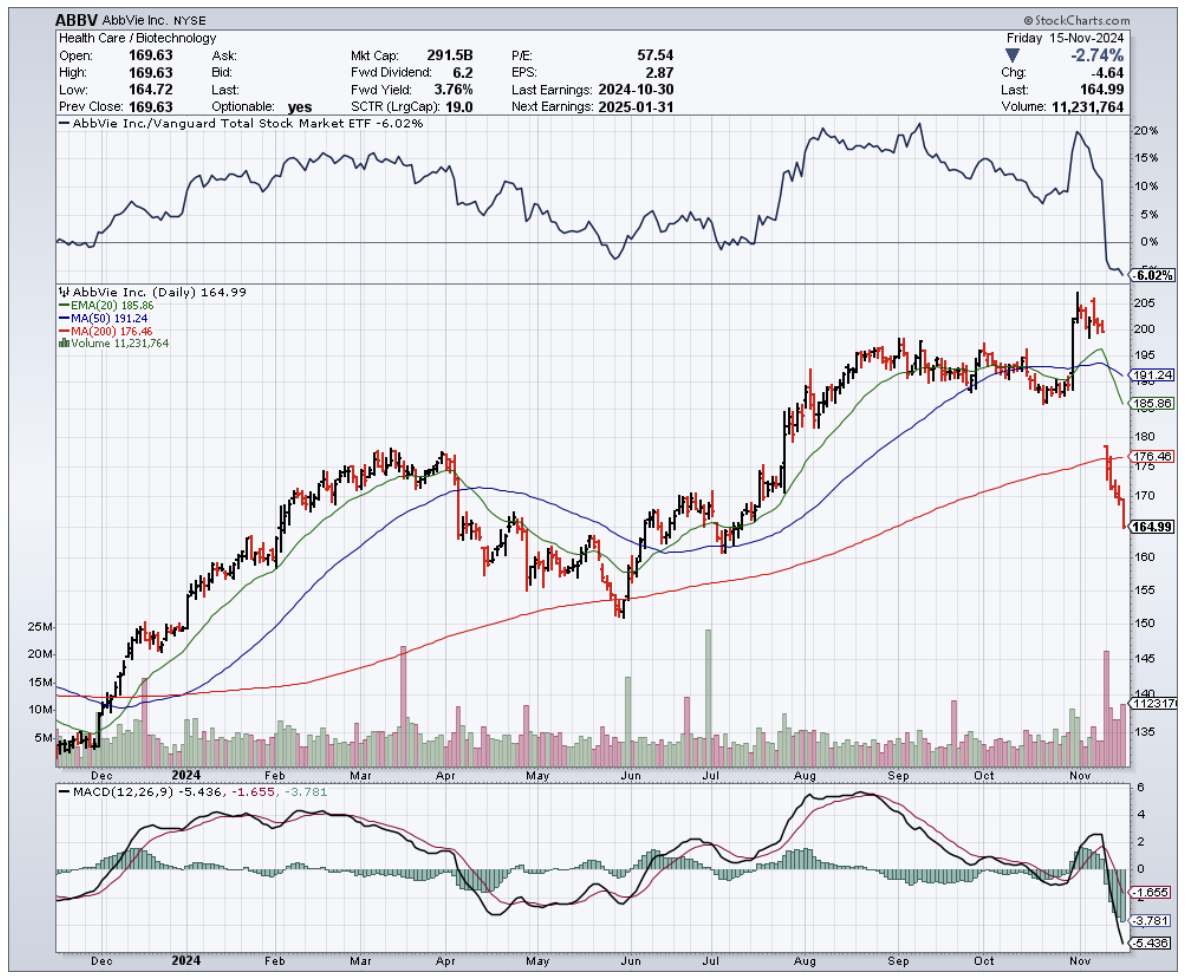

If you've ever wondered what $9 billion in disappointment looks like, ask the folks at AbbVie (ABBV). They've just learned the hard way that even the most promising psychiatric drugs can pull a vanishing act worthy of Houdini when it comes to clinical trials.

Their great hope, emraclidine – a name that sounds like it could either cure schizophrenia or clean your bathtub – recently face-planted in not one, but two Phase 2 trials.

Dr. Roopal Thakkar, AbbVie's Chief Scientific Officer, probably wishes this particular day came with a reset button, as the company's experimental once-daily pill performed with all the therapeutic punch of a sugar tablet in treating schizophrenia.

Somewhere, in a parallel universe, there's probably a version of Dr. Thakkar who didn't just watch $40 billion in market value evaporate faster than a teenager's allowance at a gaming convention.

Unfortunately, in our universe, AbbVie's stock took a 12.6% nosedive to $174.43.

But here's where it gets interesting, in that peculiar way that only Wall Street can manage. While AbbVie was having its very bad, no-good day, Bristol Myers Squibb (BMY) was practically dancing in the streets.

Their shares shot up 11% faster than you can say "competitive advantage." Why? Because their own schizophrenia drug, Cobenfy (another name that sounds like it came from the same random pharmaceutical name generator), just got the FDA's blessing.

Talk about impeccable timing.

Let's put this in perspective: We're talking about a global market worth $7.90 billion in 2023, projected to balloon to $11.35 billion by 2030. And it's not just about money.

The World Health Organization tells us there are 24 million people worldwide living with schizophrenia.

In the U.S. alone, it affects between 0.25% and 0.64% of adults, according to the National Institute of Mental Health. That's roughly the population of a small city, all waiting for better treatment options.

Meanwhile, other players in this high-stakes game are making moves that would impress a chess grandmaster.

Take Teva Pharmaceutical Industries (TEVA), busy cooking up a long-acting injectable version of olanzapine.

Or Alkermes plc (ALKS), sitting pretty with their $1.17 billion in revenue for 2022, thanks partly to their own injectable antipsychotic, Aristada.

Then there's H. Lundbeck A/S (HLBBF), the Danish company that spends 18% of its $2.7 billion revenue on R&D, like a scientist with an unlimited coffee budget.

And let's not forget the plucky underdog, Anavex Life Sciences Corp. (AVXL), burning through cash like a marathon runner through calories ($31.6 million in losses for 2022) while chasing their own psychiatric breakthrough.

Their compound, ANAVEX 3-71, sounds like a droid from Star Wars but might just be the next big thing in schizophrenia treatment. Or not.

That's the beauty and terror of biotech investing – you never quite know if you're backing the next breakthrough or the next spectacular failure.

AbbVie, thankfully, isn't exactly heading for the poorhouse. Their blockbuster drug Humira raked in $21 billion in 2022 alone – enough to buy everyone in New Zealand a really nice dinner.

The truth is, navigating the biotech market is less like following a recipe and more like trying to predict where lightning will strike while riding a unicycle.

So here's your biotech shopping list, served with a side of market reality.

AbbVie's spectacular face-plant has created a buying opportunity for the patient investor (that $21 billion Humira cushion makes for a soft landing).

Bristol Myers Squibb is strutting around with their fresh FDA approval like they own the place (and right now, they kind of do).

And if you're feeling particularly adventurous, Anavex Life Sciences offers a lottery ticket that might just pay off.

Whatever you choose, just remember to keep your antacids handy.

Mad Hedge Biotech and Healthcare Letter

November 12, 2024

Fiat Lux

Featured Trade:

(BONE OF CONTENTION)

(AMGN), (NVO), (LLY), (PFE), (VKTX), (GPCR), (AZN)

Who knew the devil could lurk in an Excel spreadsheet? More specifically, in a hidden tab that, until recently, was minding its own business like a shy teenager at a school dance.

That is, until some eagle-eyed analyst at Cantor Fitzgerald decided to right-click their way into a $12 billion nightmare for Amgen.

(If you're wondering how to find these hidden tabs yourself, just right-click on any visible tab in Excel. Though after this debacle, pharmaceutical companies might start password-protecting their spreadsheets like they're nuclear launch codes.)

The data in question concerns MariTide, Amgen's hopeful contestant in the "help-America-lose-weight" sweepstakes.

The hidden tabs revealed what the published paper in Nature Metabolism conspicuously didn't mention: bone density scans that would make an osteoporologist reach for their stress ball.

Patients receiving the 420-milligram dose saw their bone density drop by about 4% over 12 weeks - the kind of number that sends stock traders reaching for their sell buttons faster than you can say "osteoporosis."

Speaking of selling, this discovery sent Amgen's stock tumbling 7%, which in the biotech world is like watching $12 billion vanish faster than free cookies at a Weight Watchers meeting.

Amgen, doing what pharmaceutical companies do best when faced with uncomfortable data, assured everyone that their Phase 1 study doesn't suggest any bone safety concerns. (One imagines their PR team working overtime, possibly sustained by the same stress-eating habits their drug aims to curb.)

Now, let's talk about the increasingly crowded room of companies trying to help elephants become gazelles.

Novo Nordisk (NVO), the current crown prince of weight-loss drugs, is sitting pretty with Wegovy raking in 17.3 billion Danish kroner (about $2.5 billion) in just one quarter.

They're so confident they're throwing $11 billion at Catalent faster than you can say "production scale-up." That's enough kroner to buy every Danish pastry in Copenhagen, though that might defeat the purpose.

Not to be outdone, Eli Lilly's (LLY) Zepbound is showing off with weight loss results that would make Jenny Craig jealous - we're talking 21% body weight reduction.

Together with Novo Nordisk, they're expected to dominate 80% of the market, leaving other companies to fight over the crumbs like desperate dieters at a birthday party.

Still, the supporting cast is equally fascinating.

Pfizer's (PFE) danuglipron and Structure Therapeutics' (GPCR) GSBR-1290 are trying to turn these injectable drugs into pills, because apparently not everyone enjoys playing pin cushion.

Viking Therapeutics (VKTX) is getting creative with VK2735, a dual GLP-1 and glucagon receptor agonist, which is pharmaceutical speak for "two mechanisms of action are better than one."

Meanwhile, AstraZeneca's (AZN) AZD5004 is trying to join the party, though their early Phase I results are about as impressive as a rice cake at a dessert buffet.

Now, let’s take a look at the numbers. The global anti-obesity drugs market is expected to balloon from $6.15 billion in 2024 to an eye-watering $37.94 billion by 2032.

But, that seems to be just the conservative estimate. Some analysts are betting this market could hit $150 billion by the early 2030s.

So, what’s the smart move here?

For those watching this space (while probably patting their own midsections thoughtfully), the message is clear: This market is hotter than a freshman chemistry experiment gone wrong.

But as Amgen's Excel adventure shows, sometimes the devil really is in the details - or in this case, in Tab 9, hidden away like a chocolate bar in a dieter's sock drawer.

And like my old friend Deng Xiaoping used to say, sometimes you have to cross the river by feeling the stones.

Today, those stones are telling me this: hold off on buying Amgen - that bone density data isn't just a minor setback, it's a potential deal-breaker.

If you really want to take part in the action, opt for Novo Nordisk and Eli Lilly for their proven ability to execute and dominate.

And for those of you who, like me, enjoy a bit of calculated risk-taking, consider a speculative position in Structure Therapeutics and Viking Therapeutics.

Before you get too excited, though, I'd suggest limiting these speculative plays to no more than 5% of your portfolio each - promising early-stage biotechs can deliver spectacular returns, but they can also crash faster than a poorly maintained MIG-25.

Mad Hedge Biotech and Healthcare Letter

November 12, 2024

Fiat Lux

Featured Trade:

(MEDTECH’S TRUMP CARD)

(RMD), (STE), (TNDM), (JNJ), (BDX), (MDT), (BSX), (SYK), (ZBH)

After seeing Trump sweep back into office, my phone's been ringing off the hook with one question: "What happens to my portfolio now?"

Look, I've been around this circus since covering Reagan in the White House press corps, and I can tell you that market hysteria rarely matches reality.

But this time, we need to pay attention - especially in the $567 billion medtech industry that's about to face some serious disruption.

What's different now? Trump's not just talking about those 10% to 20% blanket tariffs anymore - he's dead serious about slapping a potential 60% tariff on Chinese imports.

And after spending years watching supply chains twist themselves into pretzels during COVID, this is going to hit different.

To understand just how big this could be, let's look at what's really at stake here.

In vitro diagnostics makes up 18% of the medtech industry, and cardiology devices are sitting at $75 billion in 2024, expected to hit $95 billion by 2028.

Those aren't just numbers on a page - they represent real money that could take a serious hit. If these tariffs go through, we're looking at a 3.2% hit to S&P 500 earnings per share in 2025.

And it gets worse - add another 1.5% drop if our trading partners decide to play hardball with retaliatory tariffs.

Given all this, where should you put your money? The answer lies in looking at who's already ahead of the curve.

Well, established players like Johnson & Johnson (JNJ) and Becton Dickinson and Co. (BDX) are looking increasingly shrewd with their local-for-local manufacturing strategy.

They might not give you the same adrenaline rush as scaling Mount Everest, but they're solid holds in this environment.

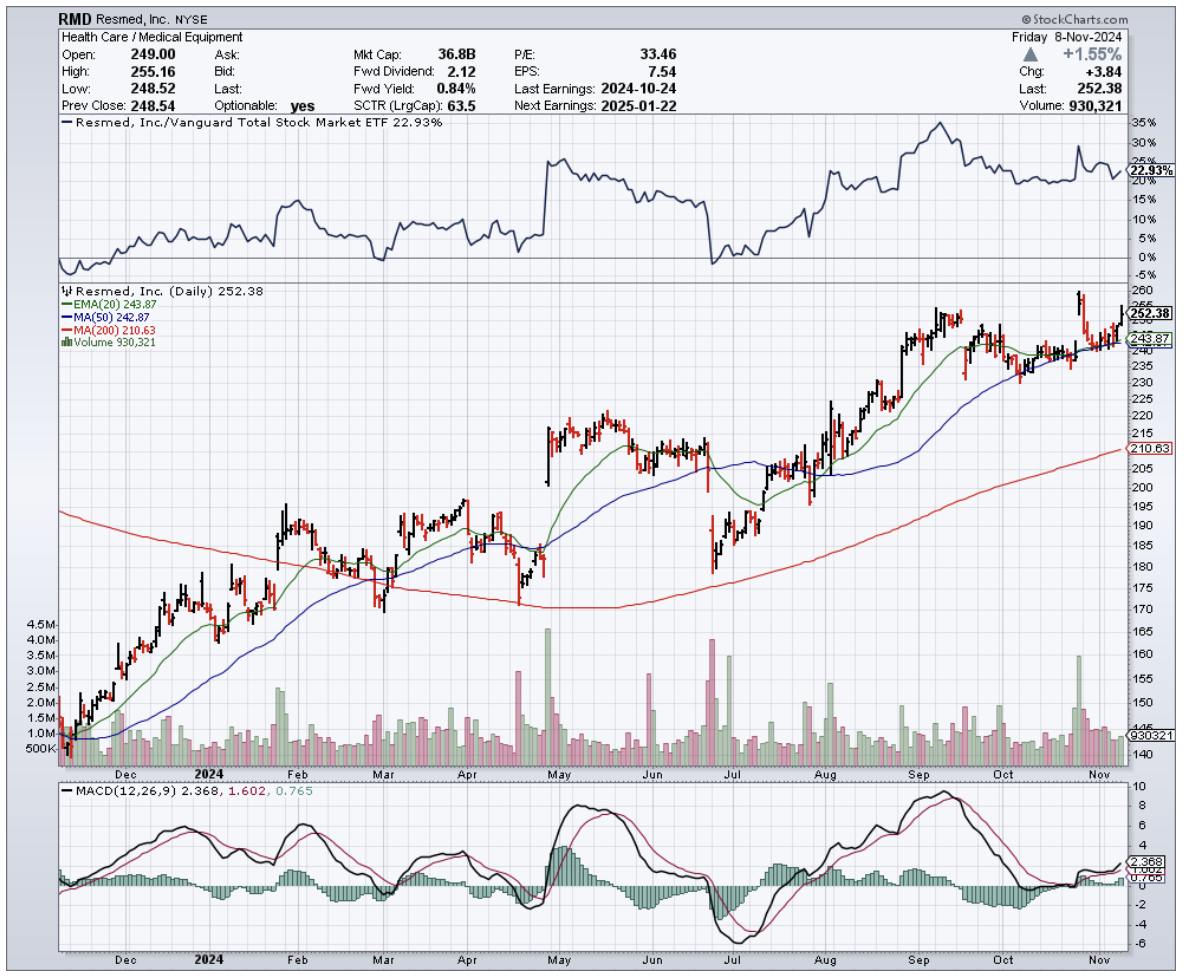

But they’re not the only companies securing their positions. ResMed (RMD), for instance, just posted third-quarter sales up 11% to $1.22 billion, with adjusted earnings jumping 34% to $2.20 per share.

That's not just good numbers - that's a company that knows how to execute regardless of who's in the White House.

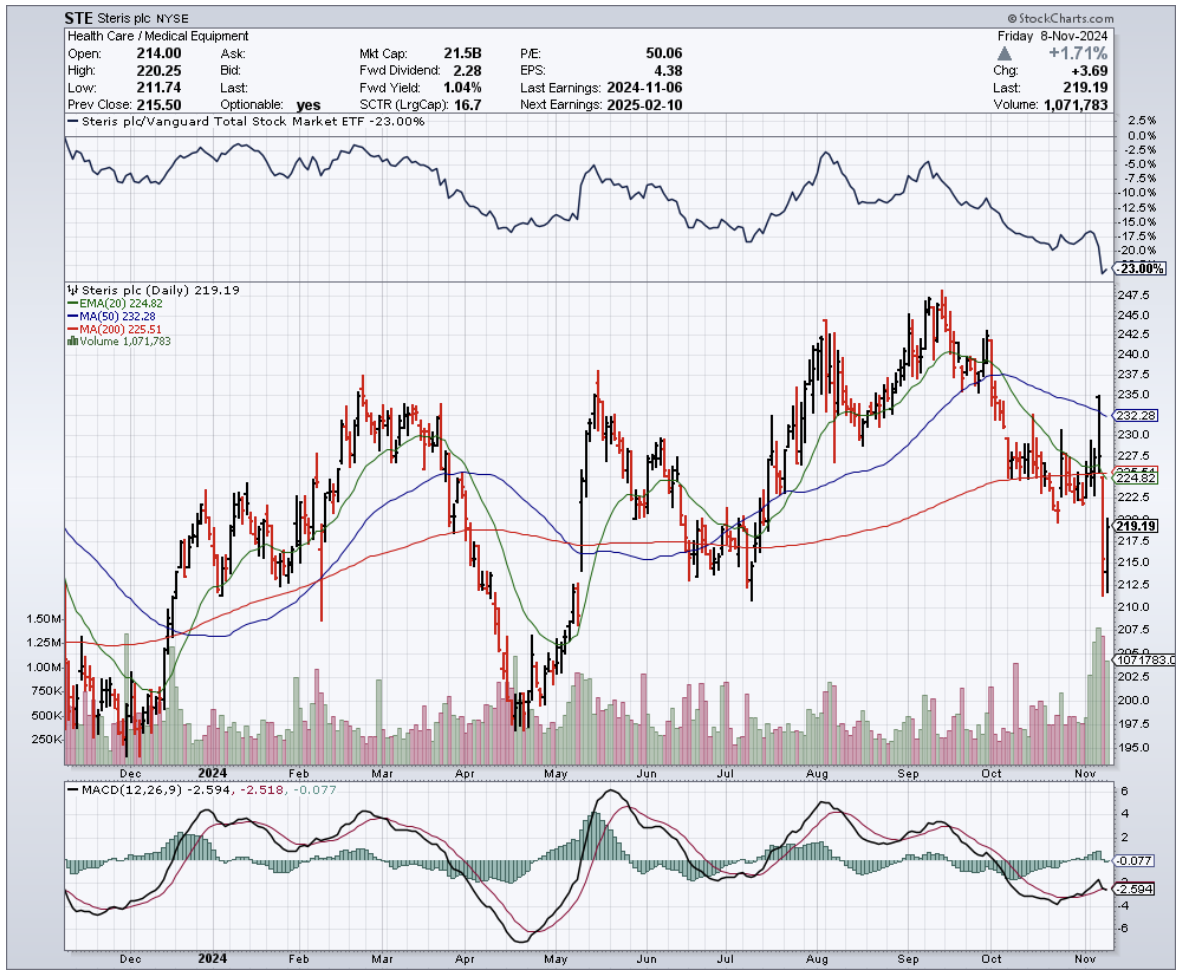

In the same vein, Steris deserves attention. Their "front-shoring" strategy in Malaysia isn't just smart - it's prescient. After years of covering Asia for The Economist, I can spot smart positioning when I see it.

Now, let's talk about some of the bigger players in the room. Medtronic (MDT), our industry giant, is giving me pause.

Sure, they're a global leader, but their heavy reliance on Chinese manufacturing and components is about to become a serious headache under these new tariffs.

Same story with Boston Scientific (BSX) - they've got manufacturing facilities in China that could turn from assets to liabilities pretty quickly.

Stryker (SYK) and Zimmer Biomet (ZBH) are in the same boat, but with a twist. Both companies have been smart enough to spread their supply chains globally, but they're still catching enough Chinese exposure to make me nervous.

When those tariffs hit their component costs, watch their margins. This isn't just about bottom lines - it's about how much wiggle room these companies have to absorb higher costs without passing them on to hospitals and patients.

On the flip side, I'm watching companies like Tandem Diabetes Care (TNDM) with growing concern.

Their heavy Asian supply chain exposure under Trump's trade policies is going to be about as comfortable as my MIG-25 flight at 90,000 feet - and trust me, that wasn't comfortable at all.

But, what’s really telling is where the smart money is flowing.

Keep your eyes on three key trends that are reshaping the industry: supply chain resilience, M&A activity (now up 18% to $57.7 billion), and digital transformation.

About 30% of medtech companies are getting serious about digitizing their operations - and they're the ones to watch.

So, here's my bottom line: Trump's return is going to shake up medtech, but not every tremor is an earthquake.

The winners in this new landscape will be companies that have already diversified their manufacturing outside China, built up strong balance sheets to absorb these tariff impacts, and proven they can adapt - like ResMed and Steris have shown us.

The real champions will be those making serious investments in digital transformation. These are the companies that won't just survive Trump's trade policies - they'll thrive under them.

And if you're still holding onto companies with heavy Chinese exposure?

Well, let's just say it might be time to look for higher ground - and I'm speaking as someone who's made that call at both 20,000 feet on Everest and during the 2008 crash.

The medtech industry isn't going anywhere - people will always need medical devices. But which companies thrive under Trump's second term? That's going to depend on who's prepared for the storm and who's still standing in the open.

Now, if you'll excuse me, I've got some vintage wine to open. Making sense of these markets is thirsty work.

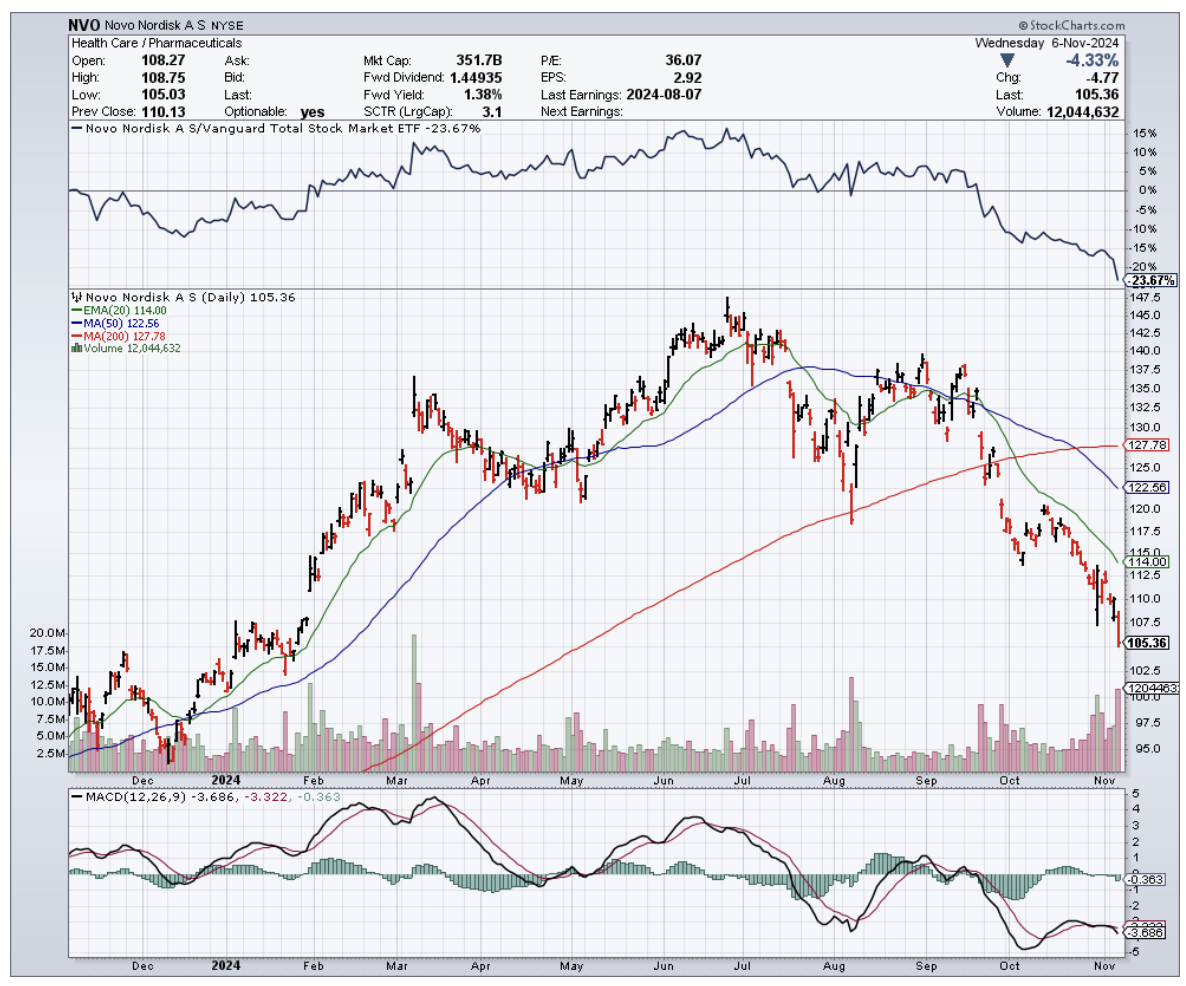

Mad Hedge Biotech and Healthcare Letter

November 7, 2024

Fiat Lux

Featured Trade:

(COPENHAGEN’S CASH COW)

(NVO), (LLY), (AMGN), (RHHBY), (PFE)

The first time I visited Denmark, my taxi driver had an unusual conversation starter.

"You know what's our biggest company?" he asked, navigating Copenhagen's rain-slicked streets. "Not LEGO, not Maersk. It's the diabetes people." He was right.

Novo Nordisk (NVO), which began in the 1920s with a borrowed insulin recipe and a dream of treating diabetes, has morphed into Denmark's crown jewel of pharmaceuticals.

The company that once extracted insulin from cow pancreases (collected by the truckload from local slaughterhouses) is now making the kind of money that would make a Viking raid look like pocket change.

In the third quarter of 2024 alone, Novo Nordisk reported a 21% profit surge to 27.3 billion Danish kroner (that's $2.45 billion for those of us who don't speak currency converter).

The star of this financial show? A drug called Wegovy, whose sales have skyrocketed to 17.3 billion kroner in Q3, leaving analysts' predictions in the dust like a marathoner who's found an extra gear.

But before we pop the champagne (or the sugar-free sparkling water, given the company's focus), let's peek behind the Danish curtain.

The story of Novo Nordisk is like watching a high-wire act at the circus - thrilling, precisely executed, but with plenty of observers holding their breath about what could go wrong.

But, it's now a far cry from the days when company founders Harald and Thorvald Pedersen would personally deliver insulin to local pharmacies by bicycle.

The company has carved out its empire in the rather unglamorous-sounding GLP-1 receptor agonist market.

Don't let the clunky name fool you - this market was worth a hefty $36.79 billion in 2023 and is growing faster than bacteria in a petri dish, with projections showing a 21.65% annual growth rate from 2024 to 2030.

By 2031, we're looking at a potential $150 billion market, with obesity treatments accounting for $90 billion of that pie.

Novo Nordisk's triple threat - Wegovy, Ozempic, and Rybelsus - have been dominating this space like a scientific dream team.

Not bad for a company that once had to import porcine intestines from China to keep up with insulin production in the 1960s.

But success attracts competition like moths to a flame, and the flames are getting crowded.

Enter Eli Lilly (LLY), strutting into the party with Mounjaro, which raked in $1.5 billion in Q2 2024 sales alone - a 71% quarterly growth that probably caused some sleepless nights in Denmark.

Meanwhile, Amgen (AMGN) and Viking Therapeutics (VKTX) are cooking up their own weight-loss concoctions in their respective labs.

Viking's oral GLP-1 drug is particularly interesting - imagine taking a pill instead of giving yourself a shot. For needle-phobic patients, that's like choosing between a day at the spa and a day at the dentist.

Speaking of setbacks, Novo Nordisk recently had to wave the white flag on ocedurenone, their hoped-for kidney disease drug.

After spending $1.3 billion to acquire it from KBP Biosciences (ouch), the phase 3 trial results came back with all the excitement of a flat sofa.

The company had to write off $816.5 million - the kind of number that makes accountants reach for the antacids.

Now they're left with just one CKD program based on semaglutide, the same ingredient that makes Wegovy, Ozempic, and Rybelsus tick. It's a reminder that even in the age of sophisticated molecular modeling and AI-driven drug discovery, pharmaceutical development can still be as unpredictable as Danish weather.

As if that weren't enough to keep executives up at night, Hims & Hers Health (HIMS) is preparing to crash the party with a generic version of liraglutide (the secret sauce in Novo's older drugs Victoza and Saxenda) as soon as 2025.

While these older medications contribute less than 10% to Novo's revenue, it's like watching the first raindrops of what could become a storm.

The ghosts of those early insulin-producing pancreases might be chuckling at how history repeats itself - from fighting for insulin patents in the 1920s to defending weight loss drug territory today.

The company's stock currently trades at a forward P/E ratio of 33.2x, with analysts expecting a 22.4% annual earnings growth through 2025.

That's the kind of valuation that makes value investors break out in hives - 37 times trailing earnings and 12.95 times trailing sales means this stock is priced like a luxury handbag, where any scuff could send the price tumbling.

For those eyeing Novo Nordisk like a dessert cart at a weight-loss clinic, the decision isn't simple.

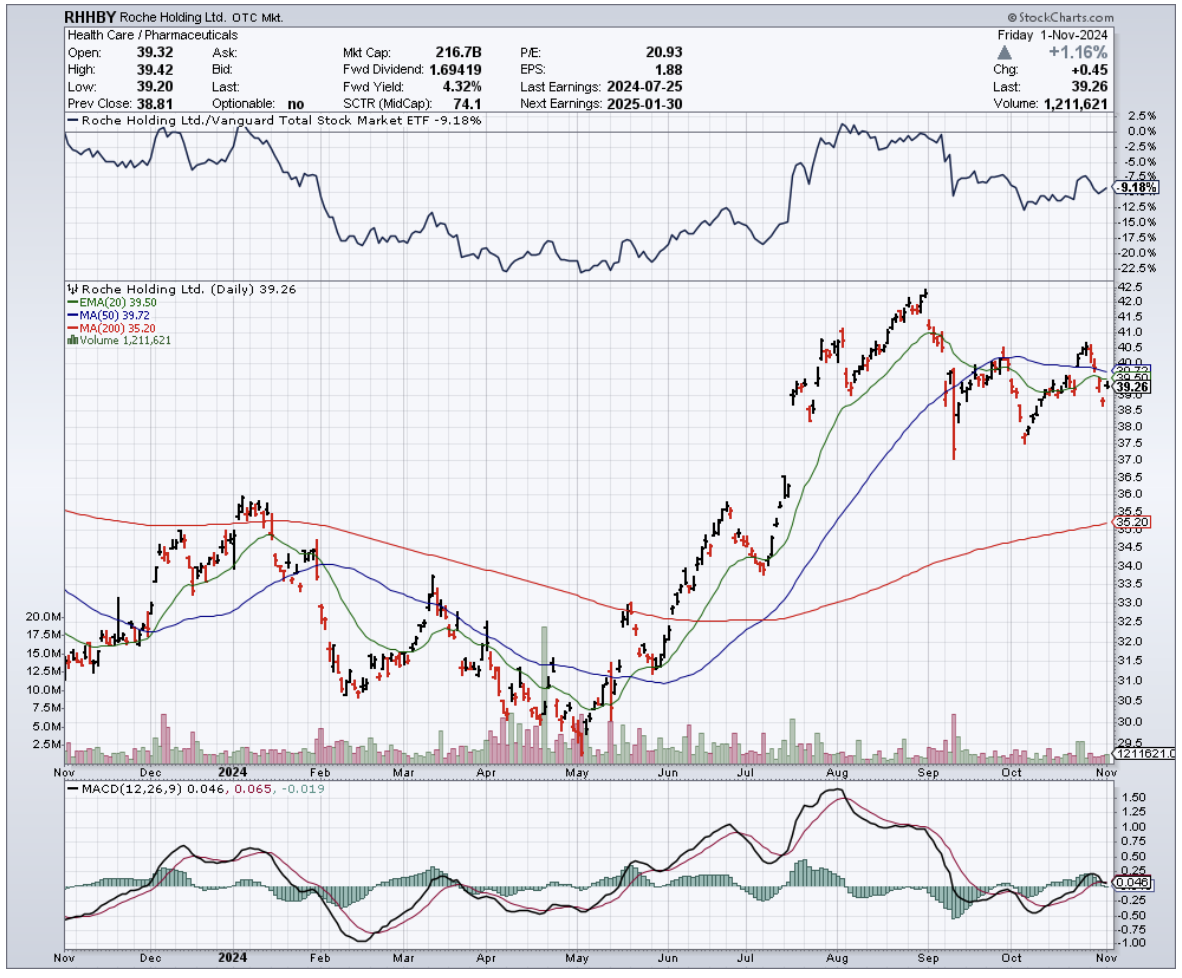

The company's dominance in the GLP-1 market is impressive, but with competitors like Eli Lilly, Amgen, and Pfizer (PFE) circling like hungry sharks, and Roche's (RHHBY) recent acquisition of Carmot Therapeutics adding another player to the mix, the waters are getting choppy.

The prudent move? Current shareholders might want to hold onto their tickets for this roller coaster ride while keeping a white-knuckled grip on the safety bar.

New investors might want to wait in line until the price becomes more reasonable - like waiting for the post-holiday sale at a luxury boutique.

And for those looking to spread their bets, Eli Lilly, Amgen, and Roche offer alternative ways to play in this space, each with their own mix of risk and potential reward.

Anyway, going back to that taxi driver in Copenhagen? He had one more thing to say: "Those Novo people, they started with dead cows and now they're making drugs from bacteria in giant steel tanks. Who knows what they'll do next?"

Indeed, from slaughterhouse pancreases to billion-dollar weight loss drugs, Novo Nordisk's story reads like a scientific fairy tale. But in the world of biotech investing, even fairy tales need solid earnings reports.

For now, this Danish giant continues to prove that sometimes the best investment stories start with someone asking, "What if we could do this better?" - even if "this" means figuring out how to get insulin from a cow pancreas.

Mad Hedge Biotech and Healthcare Letter

November 5, 2024

Fiat Lux

Featured Trade:

(DANCING WITH SHADOWS)

(RHHBY), (SGMO), (LLY), (BIIB), (ABBV)

In 1906, Dr. Alois Alzheimer first encountered what he called a “mysterious” mental illness, examining the brain of a 55-year-old woman who had died under strange neurological circumstances.

Over a century later, that mystery hasn’t let up. We’re still scratching our heads—and burning through money.

By 2050, Alzheimer’s is projected to cost the U.S. healthcare system $1.3 trillion, more than the entire GDP of Australia.

But something’s happening at Roche (RHHBY) that’s got my scientific spidey senses tingling.

Roche has been chasing Alzheimer’s solutions for over two decades, pouring resources into this elusive brain burglar that defies every rule in the book.

And yet, here they are—undaunted, driven by a noble (and, yes, profitable) goal to relieve the massive toll AD takes on patients, families, and entire healthcare systems.

It hasn’t been smooth sailing; setbacks and “whoops, not this time” moments have kept things bumpy. Recently, though, I’ve been seeing hints of a breakthrough that just might bring this long, shadowy dance with Alzheimer’s closer to the light.

For those who've been reading my letter since 2008, you know I rarely get excited about big pharma unless there's real meat on the bone. Well, this time there is, and it's called Brainshuttle technology.

If you’ve never heard of it, think of it as a kind of souped-up delivery service for the brain—no, not that kind. This tech helps Roche’s meds cross the blood-brain barrier, that stubborn security guard that only lets a select few molecules into the brain.

It’s great at keeping out random junk but also frustratingly good at blocking drugs we actually want to get in there.

Brainshuttle could change that, allowing antibodies to cross over more easily and making lower doses (and hopefully fewer nasty side effects) possible.

Enter trontinemab, a drug that’s caught a lot of eyes recently. Armed with Brainshuttle, this amyloid-beta antibody is like the brain’s personal pest control.

Early trials are promising: Roche reported that trontinemab is sweeping out amyloid plaque faster than a Roomba on espresso, and all at lower doses.

Less dose, more punch, and fewer side effects? Sounds like the AD holy grail. They’re even eyeing an accelerated approval path with the FDA.

Now, the FDA isn’t exactly known for sprinting to approval—especially with Alzheimer’s drugs—but trontinemab’s early results make it a strong contender.

But Roche isn’t putting all its eggs in one beta basket. AD research has been dominated by amyloid-beta, but there’s another protein that scientists are pretty excited about: tau.

If amyloid-beta is the ringleader, tau is the muscle, the heavy that clogs up brain cells and wreaks havoc.

To tackle tau, Roche has teamed up with Sangamo Therapeutics (SGMO), a company with tech that sounds like it’s straight out of a sci-fi novel—zinc finger molecules.

These little DNA-grabbers are designed to silence the tau gene, essentially telling it to cool it and stop producing the stuff that clogs up the brain.

The partnership also gives Roche access to something else in Sangamo’s arsenal: an adeno-associated virus capsid. (Translation: a delivery mechanism that gets things across the blood-brain barrier.)

If these tools work as planned, Roche may have a real chance to give AD a one-two punch with both amyloid-beta and tau treatments.

But let's be real here. This is still the Wild West of biotech, and Roche has had its share of setbacks.

They recently walked away from a partnership with UCB, returning the rights to an anti-tau antibody called bepranemab.

Even though UCB called the Phase 2a data "encouraging," it apparently didn't meet Roche's internal bar. That's the thing about Alzheimer's drug development - it's about as predictable as my teenager's mood swings.

The competition isn't sleeping either. Eli Lilly (LLY), Biogen (BIIB), and AbbVie (ABBV) are all throwing everything but the kitchen sink at this disease. But Roche's Brainshuttle technology might just be their secret weapon in this fight.

Here's what keeps me optimistic: Roche’s multi-pronged strategy, combining amyloid-beta and tau, might just give them an edge. It’s not guaranteed—far from it—but having multiple avenues does give them a better shot at success.

This is what I call a "chess not checkers" opportunity. The potential payoff is massive - we're talking about a market that could make crypto's best days look like pocket change. But timing is everything.

So, I'll be watching trontinemab's development like a hawk. The Sangamo collaboration is also on my radar - any breakthrough in tau-targeted therapies could be a game-changer.

As always, don’t bet the farm, folks—not even on a biotech darling like this. But if you’re itching to add a little intellectual flair to your portfolio, Roche’s Alzheimer’s gambit is worth a look. Buy the dip, but set those stop losses. After all, even the best-laid plans of mice and biochemists often go awry.