Mad Hedge Biotech and Healthcare Letter

October 31, 2024

Fiat Lux

Featured Trade:

(BORN WITH A SILVER SEQUENCE)

(ILMN), (PACB), (TMO)

Mad Hedge Biotech and Healthcare Letter

October 31, 2024

Fiat Lux

Featured Trade:

(BORN WITH A SILVER SEQUENCE)

(ILMN), (PACB), (TMO)

When my kids were born years ago, the most advanced technology in the delivery room was the fetal heart monitor, which had all the predictive power of a Magic 8 Ball with a medical degree.

Those primitive days feel like ancient history now.

Today, as I watch my friends' grandchildren entering the world, they're getting something I would have traded my first hedge fund for: a complete genetic blueprint that makes a heart monitor look like two cups and a string.

Enough nostalgia. Let me cut straight to the chase, because nothing makes me twitchier than analysts who dance around the point like nervous fathers in a delivery room.

What I want to say is that I'm betting big on something called whole genome sequencing (WGS) for every newborn. And don't worry - this isn't just another biotech pipe dream cooked up by optimistic PhDs with too much venture capital.

Having spent years in Japan during the 1970s watching semiconductor technology transform from an expensive curiosity into an industrial necessity (rather like sushi in Manhattan), I recognize the same patterns emerging here.

The cost trajectory alone is enough to make a value investor weep with joy - from $100 million per genome in 2001 (roughly the price of a small island) to less than $600 today, with Illumina (ILMN) pushing to bring it to $100.

And what do we get for this bargain-basement pricing?

The numbers from the GUARDIAN project are juicier than an insider trading tip - and completely legal, I might add.

They're screening newborns for over 200 genetic conditions, while most hospitals are still stuck at 30, like they're using a genetic View-Master instead of an IMAX theatre.

In their first 4,000 participants, they found actionable diagnoses in 3.7% of newborns - conditions that traditional screening would have missed like a banker misses market crashes.

Let's look at the hard economics.

In NICU settings, ultra-rapid genome sequencing is already saving $14,265 per child and changing patient management in 37% of cases.

Early intervention in spinal muscular atrophy alone saves over $4 million in lifetime costs per patient - the kind of numbers that make healthcare administrators actually smile, a rare sight indeed.

These clinical benefits translate directly to the bottom line.

Just consider the market size. We're looking at $62.9 billion by 2030, growing at 18.2% annually.

The newborn screening market alone will hit $2.27 billion by 2025, and if that doesn't get your investment synapses firing, you might want to check your own genetic predisposition to opportunity recognition.

But impressive market numbers are just the beginning.

The technology landscape is shifting faster than trading algorithms during a Flash Crash. Stanford Medicine is now diagnosing genetic diseases in under eight hours - a process that used to take longer than getting approval for a mortgage.

Companies like Illumina, Pacific Biosciences (PACB), and Thermo Fisher Scientific (TMO) are playing a game of genetic leapfrog, each advance more impressive than the last.

Meanwhile, Sophia Genetics and their AI cohort are turning genetic data into actionable insights faster than you can say "double helix."

Having watched technology transformations unfold before, I know what I'm seeing.

My years in Japan taught me one crucial lesson (aside from never mix wasabi with everything just because you can): the difference between routine technological advancement and true paradigm shifts is as clear as the gap between a good investment and a great one.

What we're witnessing now - plummeting costs, advancing technology, and clear market demand - is rarer than a hedge fund manager admitting they were wrong.

And the implications are staggering. Think about this: we're approaching an era where every child starts life with a complete genetic roadmap.

It's like getting the ultimate user manual at birth, except this one actually tells you something useful, unlike those assembly instructions from Swedish furniture companies.

Smart money should be building positions now, while the broader market is still scratching its head like a freshman in advanced calculus.

The companies that establish themselves as leaders in this field won't just be successful - they'll be as fundamental to healthcare as smartphones are to teenagers.

As both a parent and an investor who's seen more market cycles than a laundromat, I haven't been this excited since I discovered you could actually make money going short. This is one of those rare moments when doing well and doing good align so perfectly, it's like finding a unicorn that also files your taxes.

Don't miss this one. Some opportunities in life are as rare as a bearish call at a bull market convention - this is one of them.

Mad Hedge Biotech and Healthcare Letter

October 28, 2024

Fiat Lux

Featured Trade:

(WHEN WALL STREET MET PHARMA)

(PFE), (TSLA), (AAPL)

If corporate America were a dinner party (and let's face it, sometimes it absolutely is), Pfizer (PFE) would be that guest who showed up fashionably late with an award-winning bourbon pecan pie during the pandemic, and is now being quietly judged for bringing Trader Joe's crackers to the latest soirée. The pharmaceutical giant, which briefly enjoyed the kind of celebrity usually reserved for Tesla (TSLA) and Apple (AAPL), finds itself in the midst of what we might delicately call a boardroom intervention. With its stock price taking a dive, Pfizer attracted the attention of Starboard Value, a hedge fund with a billion dollars' worth of opinions about how to run things better.

Unfortunately for Starboard, these problems are not that simple to fix. Here's the thing about making breakthrough drugs: 9 out of 10 fail, each costs about $2 billion to develop, and even the most brilliant scientists can't tell you which one will work until the very end. This uncertainty sits at the heart of Pfizer's current predicament. After delivering a ratings blockbuster with its COVID-19 vaccine and Paxlovid treatment, the company now faces the pharmaceutical industry's dreaded sophomore album syndrome.

On top of that, every successful drug faces the same issue: it comes with its own expiration date. Patents run out, generic competitors swoop in, and suddenly everyone's asking, "What's next?"

And here's where it gets more interesting, in the way that all corporate power plays are interesting if you enjoy watching incredibly wealthy people disagree about how to become even wealthier. Take Starboard's critique of Pfizer's performance. It has all the subtlety of a CNN town hall debate, spiced up with the potential involvement of former Pfizer CEO Ian Read and CFO Frank D'Amelio — a plot twist as unsurprising as finding a filibuster in the Senate.

Having previously applied its corporate reconstruction techniques to the restaurant industry (think less Thomas Keller, more Olive Garden optimization), the hedge fund now fancies itself as something of a pharmaceutical expert. This is like suggesting that because someone successfully managed a food truck, that same person is qualified to run a three-Michelin-star restaurant.

Granted, Starboard has an impressive track record in corporate makeovers, much like the HGTV stars of Wall Street. Still, renovating a pharmaceutical company isn't the same as flipping a restaurant chain. There's something uniquely challenging about applying fast-casual dining turnaround principles to the development of life-saving medications. Some processes simply can't be rushed unless you enjoy explaining to the FDA why you thought clinical trials were more of a suggestion than a requirement.

As we try to figure out what's happening with the pharma giant right now, it helps to keep in mind that the key question isn't just whether Pfizer needs a makeover (though that's certainly part of it), but whether Wall Street's "time is money" philosophy can successfully coexist with the "science takes time" reality of drug development. It's the corporate equivalent of trying to teach quantum physics to a day trader - theoretically possible, but likely to result in some interesting misunderstandings along the way.

So, what's the play here? Looking at Pfizer's current stock price of around $28.45 (down 2.47%), the chart looks about as exciting as a waiting room magazine collection.

While the stock hovers below its 50-day moving average and sits near the lower end of its $25.20 - $31.54 yearly range, there are a few bright spots: a healthy 5.91% dividend yield and several promising projects in the pipeline - an RSV vaccine and an obesity treatment that could have customers lining up around the block again.

But here's my recommendation: Keep this one on your watchlist, but hold off on placing your order just yet.

Think of Pfizer as that once-trendy restaurant that's neither closing its doors nor winning any new Michelin stars - it's simply simmering on medium heat while the new chef (courtesy of Starboard) debates menu changes with the original kitchen staff.

Will Starboard's intervention prove to be the corporate equivalent of a breakthrough drug, or more like one of those miracle cures you see advertised at 3 AM?

The answer, like most things in the pharma world, will take time to develop. And in this battle of wits within corporate America, sometimes the hardest pill to swallow is patience - though I suspect Starboard would prefer it in fast-dissolving form.

After all, when Wall Street meets Pharma, it's less about whether the patient needs the medicine and more about timing the market's appetite.

For now, let's keep this one in the "worth watching" category until we see some signs of the stock's vital signs improving.

Mad Hedge Biotech and Healthcare Letter

October 24, 2024

Fiat Lux

Featured Trade:

(A HEALTHCARE STOCK THAT OWNS TOMORROW)

(UNH), (HUM), (ELV), (CVS)

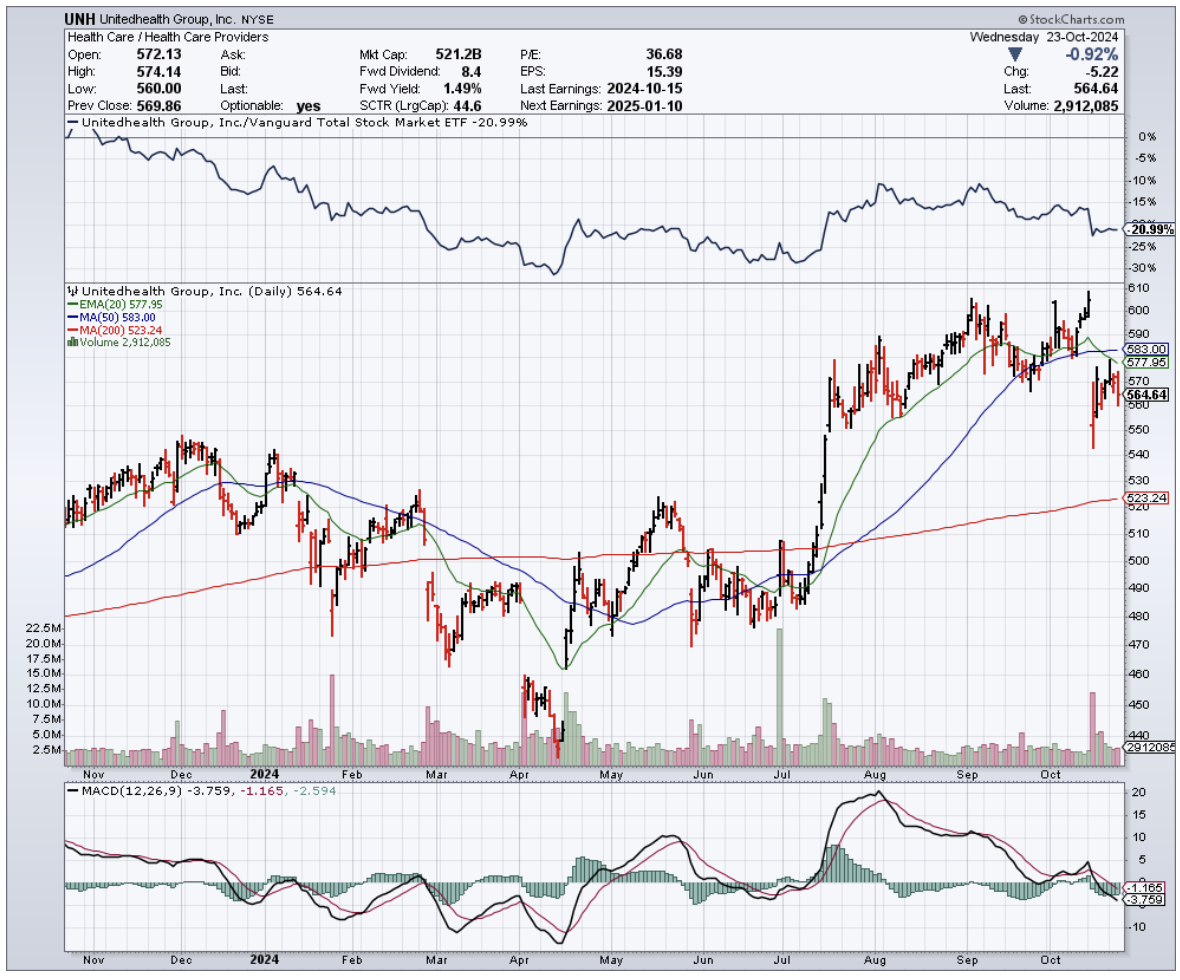

After decades of watching healthcare stocks, I've learned one immutable truth - demographics always win. And right now, demographics are handing UnitedHealth Group (UNH) the keys to the kingdom.

The numbers tell an impressive story. UnitedHealth just reported Q3 2024 revenue of $100.82 billion, up 9.2% year-over-year. That's a billion dollars above what Wall Street expected, even after weathering a nasty cyberattack on their Change Healthcare unit in February.

Let's put this in perspective. By 2031, America's national health expenditure will hit $7.17 trillion - more than the GDP of Japan and Germany combined. This isn't just another growth story.

Besides, having managed hedge fund money through multiple market cycles, I’d like to think that I know the difference between lucky timing and structural advantage. From the looks of how things are going, UnitedHealth has engineered themselves the latter.

The company's UnitedHealthcare segment tells only part of the story, bringing in $74.85 billion in Q3, up 7.2% from last year.

Their Medicare Advantage enrollment grew from 7.65 million to 7.81 million people, while their U.S. commercial health plans expanded from 27.25 million to 29.73 million members.

Yes, they took a hit on their global numbers after selling their Brazilian business - dropping from 5.48 million to 1.34 million customers. But sometimes the best deals are the ones you don't do.

The real story here is Optum and its aggressive push into value-based care.

While competitors are still figuring out how to merge technology with healthcare delivery, UnitedHealth has already built a fortress. Their $13 billion acquisition of Change Healthcare wasn't just about processing claims - it was about owning the healthcare data highway.

Optum's revenue jumped 12.5% to $63.79 billion, with their pharmacy division surging 18.5% to $34.21 billion. They processed 410 million prescriptions in Q3 alone - that's 30 million more than last year.

What Wall Street is missing is UnitedHealth's positioning for the post-COVID healthcare landscape. They're not just riding the telehealth wave - they're reshaping it.

Their OptumRx digital platform now handles 80% of all prescription transactions, while their virtual care visits have grown tenfold since 2019.

In fact, the regulatory environment plays into their hands.

While smaller players struggle with Medicare Advantage rate adjustments and value-based care requirements, UnitedHealth's scale and technology infrastructure turn these challenges into opportunities.

Their compliance systems and data analytics capabilities give them a moat that gets wider every quarter.

Wall Street expects Q4 revenue between $100.48 billion and $104.14 billion. Their P/S ratio of 1.41x looks rich compared to Humana (HUM) at 0.29x and Elevance Health (ELV) at 0.57x. But in this market, scale and execution command a premium.

Looking ahead, I see UnitedHealth hitting $552 billion in revenue by 2028. The catalysts are clear: aging demographics, rising chronic disease management post-COVID, and the unstoppable march toward value-based care.

Their Q3 non-GAAP EPS of $7.15 beat estimates by 12 cents. By 2028, I expect EPS to reach $44, with their P/E ratio dropping from 22.75x to 12.99x.

Their balance sheet remains rock solid - net debt/EBITDA ratio below 1.5x, with investment-grade ratings from S&P Global (SPGI), Fitch, and Moody's (MCO).

UnitedHealth also keeps growing its dividend by double digits, maintains a predictable business model, and outperforms competitors like CVS Health (CVS) and Humana on ROE.

Admittedly, they slightly lowered their 2024 adjusted EPS guidance, spooking some traders. But in my experience, Wall Street's short-term panic creates long-term opportunities.

So, what’s the play here? I suggest you build a position in UnitedHealth now while the stock has pulled back. Scale in gradually if you're concerned about timing, but don't miss this opportunity.

Remember, in the end, this isn't just about healthcare - it's about owning a piece of America's unstoppable demographic destiny. And that's a trend even a skeptic like me can believe in.

Mad Hedge Biotech and Healthcare Letter

October 22, 2024

Fiat Lux

Featured Trade:

(TICK TALK)

(AAPL), (ABT), (BSX), (MDT), (RMD), (INSP), (DXCM), (PODD)

While waiting two hours to vote at the Incline Village Library this weekend, I counted the number of smartwatches in the line.

Seemed like everyone was checking their heart rates in the cold. One woman's Apple Watch even suggested she sit down after standing too long in the 40-degree weather.

That got me thinking about the billions flowing into medical wearables - and where that money should really be going instead.

Let's start with some sobering numbers about atrial fibrillation (AFib), the crown jewel of smartwatch detection capabilities.

Yes, Apple's (AAPL) 2020 study showed their watches can detect 84% of AFib cases during monitoring sessions. Sounds impressive, until you dig deeper.

Of the 50 million Americans wearing smartwatches, these devices identify only about 5,000 new AFib cases annually - a mere 0.083% of the 6 million Americans affected by the condition.

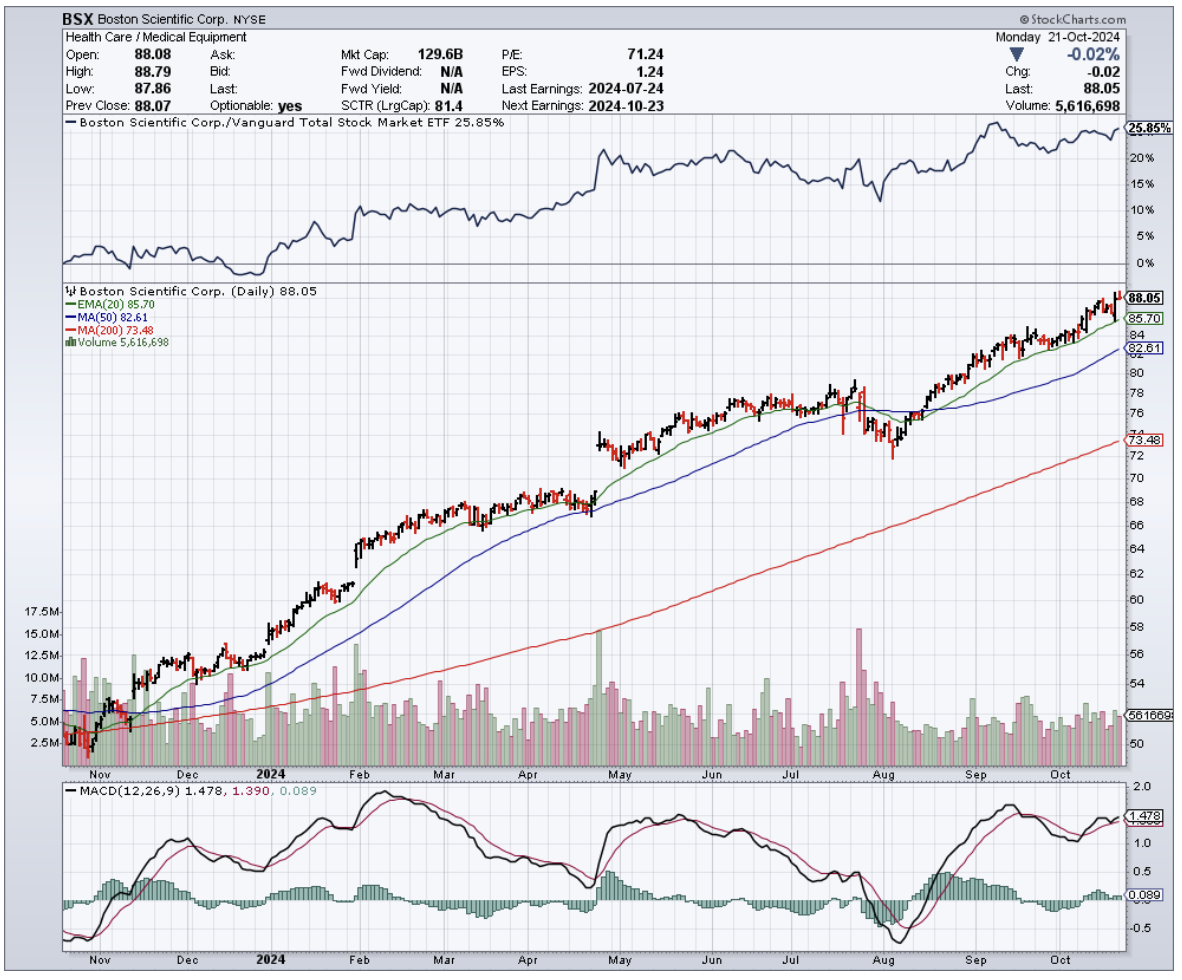

Plus, the real money tells a different story. The U.S. performs 250,000 ablation procedures yearly, creating a $3.2 billion market growing at 10% annually.

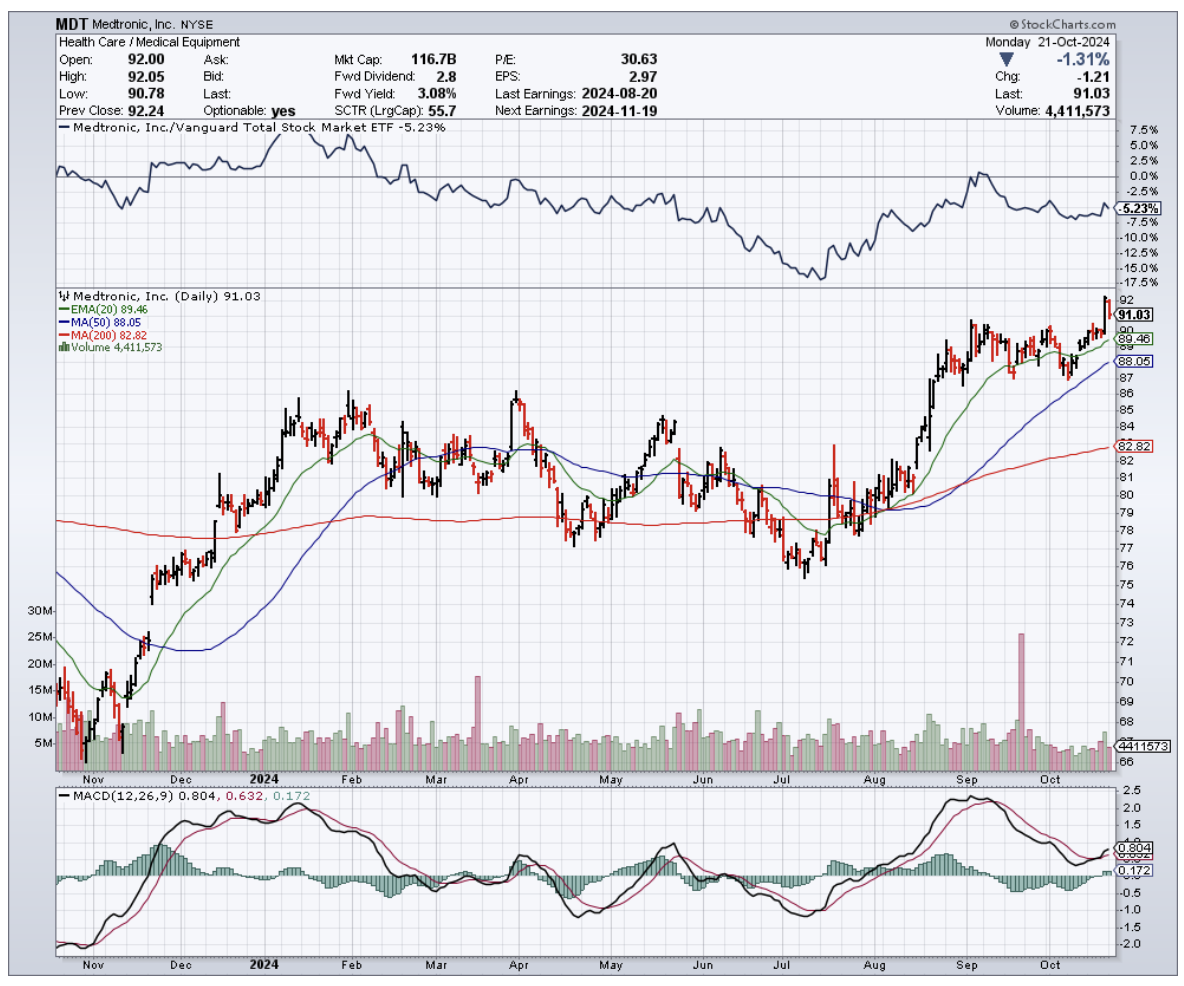

Abbott Laboratories (ABT), Boston Scientific (BSX), and Medtronic (MDT) dominate this space, with combined annual revenues of $12.4 billion from their cardiac rhythm management divisions alone.

Those 5,000 smartwatch-detected cases? They represent just 2% of annual ablation procedures. Not exactly the revolution we've been promised.

The story doesn't improve when we look at sleep apnea detection.

While Apple and Samsung tout their sleep-monitoring capabilities, their watches identify only about 60,000 of the 2 million new sleep apnea cases diagnosed yearly - that's 3% of new diagnoses.

Meanwhile, ResMed (RMD) and Inspire Medical Systems (INSP) generated combined revenues of $4.8 billion last year from sleep apnea treatments.

The smartwatch contribution to their patient pipeline is barely a rounding error.

Still, it’s not like this sector is a complete waste. The global smartwatch market stands at $58 billion and is projected to reach $98 billion by 2027, growing at 10.5% annually. Impressive, until you compare it to the traditional medical device market: $495 billion, reaching $718 billion by 2029.

The cardiac monitoring device segment alone represents $24.5 billion, expanding at 6.9% annually.

More importantly, traditional medical device companies are growing their revenues faster than smartwatch detection is adding to their patient base.

But, like I said, don't write off the sector entirely. The next generation of smartwatches promises some intriguing possibilities.

Continuous blood pressure monitoring could tap into a $23 billion market.

Non-invasive glucose tracking might crack the $28 billion diabetes monitoring space by 2027.

Enhanced sleep diagnostics could open up another $12.8 billion in opportunities.

So what's the smart play here?

Near term, keep your focus on established leaders like Abbott and Medtronic. Their upcoming Q4 earnings reports will tell us more about traditional patient acquisition trends than any smartwatch sales figures.

Watch for FDA clearances too - Abbott's new cardiac mapping system, expected in Q1 2025, could be a game-changer.

Looking out 12-24 months, keep your eye on companies like Dexcom (DXCM) and Insulet (PODD) as glucose monitoring moves mainstream.

ResMed's new sleep diagnostic platforms, launching mid-2025, could redefine how we think about sleep medicine.

Meanwhile, Boston Scientific's push into AI-enhanced cardiac monitoring might just bridge the gap between consumer tech and serious medical devices.

For long-term thinkers, watch for companies developing hybrid solutions that combine traditional devices with consumer tech.

The real breakthrough will come when medical device makers start acquiring wearable technology companies. That's when you'll know the revolution is real.

Remember, following the patient flow matters more than following the hype flow. Just like timing your visit to avoid a two-hour voting line, timing in the market is everything.

And right now, the time is right for medical device stocks, not their flashier smartwatch cousins.

Mad Hedge Biotech and Healthcare Letter

October 17, 2024

Fiat Lux

Featured Trade:

(NO TEARS HERE)

(JNJ)

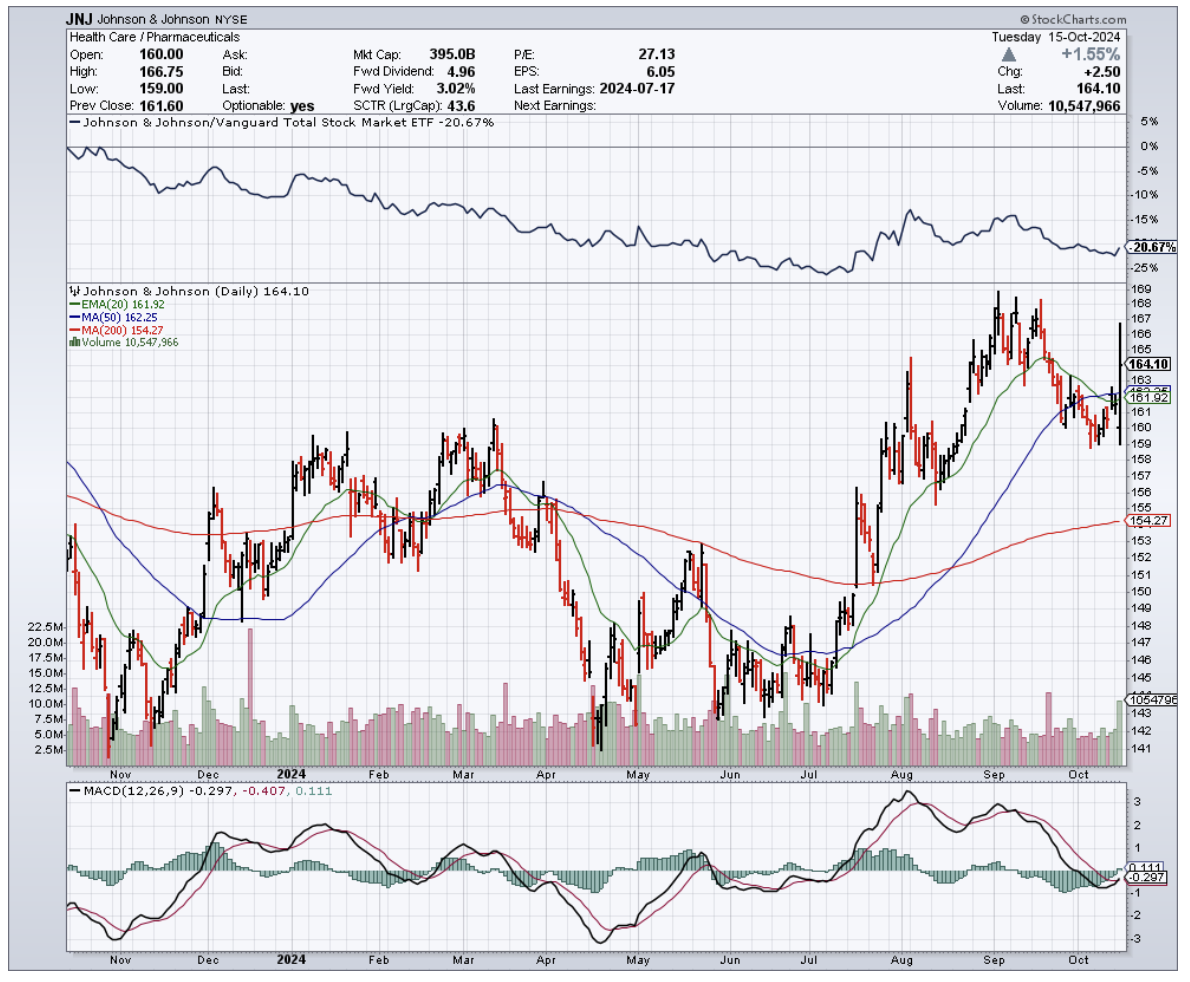

If you've been following my adventures in the market jungle for any length of time, you know I've got a nose for opportunity that'd make a bloodhound jealous. Well, folks, that nose is twitching something fierce, and it's pointed straight at Johnson & Johnson (JNJ).

Now, I know what you're thinking: "John, J&J? Aren't they as exciting as watching paint dry?" Before you dismiss this company, let me tell you—this isn't your grandma's Band-Aid shop anymore.

First off, let's talk about their pharmaceutical arm. It's not just flexing; it's practically bench-pressing the competition with one hand tied behind its back. I'm talking about a lineup that includes immunology juggernauts like Stelara and Tremfya, and cancer-fighting dynamos such as Darzalex and Erleada.

But here's the kicker—they've got over 40 late-stage clinical trials cooking. That's no mere pipeline; it's a veritable gusher of potential blockbusters.

The surprises from J&J don't end there. They recently spun off their consumer health unit faster than you can say "No more tears." Why? To zero in on their real money-makers: pharmaceuticals and medical devices. It's like watching a prizefighter shed weight before a title bout—leaner, meaner, and ready to deliver a knockout punch to the market.

Speaking of punches, J&J has been on an acquisition spree that'd make a Silicon Valley startup blush. On October 9th, they snatched up V-Wave for a cool $1.7 billion, adding to their previous grabs of Abiomed ($16.6 billion in 2022) and Shockwave Medical ($13.1 billion in 2024). And if you think they're splurging just for the heck of it, think again. This triple play gives J&J a solid foothold in the $60 billion cardiovascular device market, which is growing at a heart-racing 8% annually.

So, what does V-Wave bring to a giant like J&J? It's not just another cog in the medical machine. V-Wave is developing innovative treatment options for heart failure patients. Their device has already snagged the FDA's breakthrough device designation in 2019 and Europe's CE mark in 2020. For J&J, this means they can hit the ground running, spreading V-Wave's Ventura Interatrial Shunt across the globe faster than you can say "cardiovascular revolution."

As for their Q3 results? Let's just say J&J didn't settle for merely meeting expectations—they exceeded them. We're looking at a 5.4% adjusted operational revenue growth, with their cardiovascular business shooting up 26.5% year-over-year.

Now, I'm no fortune teller—if I were, I'd be writing this from my private island—but I'd bet my favorite Bloomberg terminal that their cardiovascular business is going to keep pumping life into J&J's MedTech segment. With more folks lining up for cardiovascular procedures than a Black Friday sale, J&J is poised to ride this wave like a pro surfer at Pipeline.

Of course, it's not all sunshine and rainbows. Their China business is facing more headwinds than a kite in a hurricane, thanks to an anti-corruption campaign that's thrown a monkey wrench into their marketing machine.

But hey, this is J&J we're talking about—a company that's been around since Grover Cleveland was in the White House. They've seen tougher times than this and come out swinging.

So, what's the bottom line? I'm slapping a "Buy" rating on this stock, with a fair value of $195 per share. For those of you looking for a stock that combines the stability of a mountain with the growth potential of a tech startup, J&J might just be your golden ticket.

Now, if you'll excuse me, I've got a sudden urge to go check my own blood pressure after all this excitement.

P.S. If J&J ever decides to venture into stem cell therapy for aging knees, you can bet I'll be first in line. These well-worn joints have a few more mountains to climb!