Mad Hedge Biotech and Healthcare Letter

December 26, 2024

Fiat Lux

Featured Trade:

(PHASE 2 OR NOT PHASE 2: THAT'S NOT EVEN A QUESTION IN 2025)

(LLY), (NVO)

Mad Hedge Biotech and Healthcare Letter

December 26, 2024

Fiat Lux

Featured Trade:

(PHASE 2 OR NOT PHASE 2: THAT'S NOT EVEN A QUESTION IN 2025)

(LLY), (NVO)

I had dinner with a veteran biotech investor at San Francisco's Waterbar earlier this month, watching the Bay Bridge lights while discussing what's coming for biotech in 2025.

"The game is changing," he said, picking at his salmon. "It's not about platform promises anymore. Show me the Phase 2 data, or don't show up at all."

He's nailed what I've been seeing in my recent travels through the biotech corridors of Boston, San Diego, and Basel. The days of throwing money at shiny new platforms are ending.

That means that by 2025, we'll see venture capital concentrate in fewer but larger deals, especially in companies with solid Phase 2 data.

Let me break down what this means for our portfolio next year. First, North America will dominate in advanced biologics and AI-driven drug discovery. I've toured enough labs recently to see that our capabilities in these areas are leaving others in the dust.

Europe's doubling down on sustainable manufacturing and rare diseases - smart move given their regulatory environment. Asia? They're positioning to own generics and biologics manufacturing, with India making particularly interesting moves in antibody-drug conjugates.

The money's following these regional specialties. If you're investing in biotech companies that don't align with their region's strengths, you might find yourself waiting longer for returns than a Red Sox fan waiting for another World Series.

My contacts in several major VC firms confirm they're already adjusting their 2025 strategies around these regional strengths.

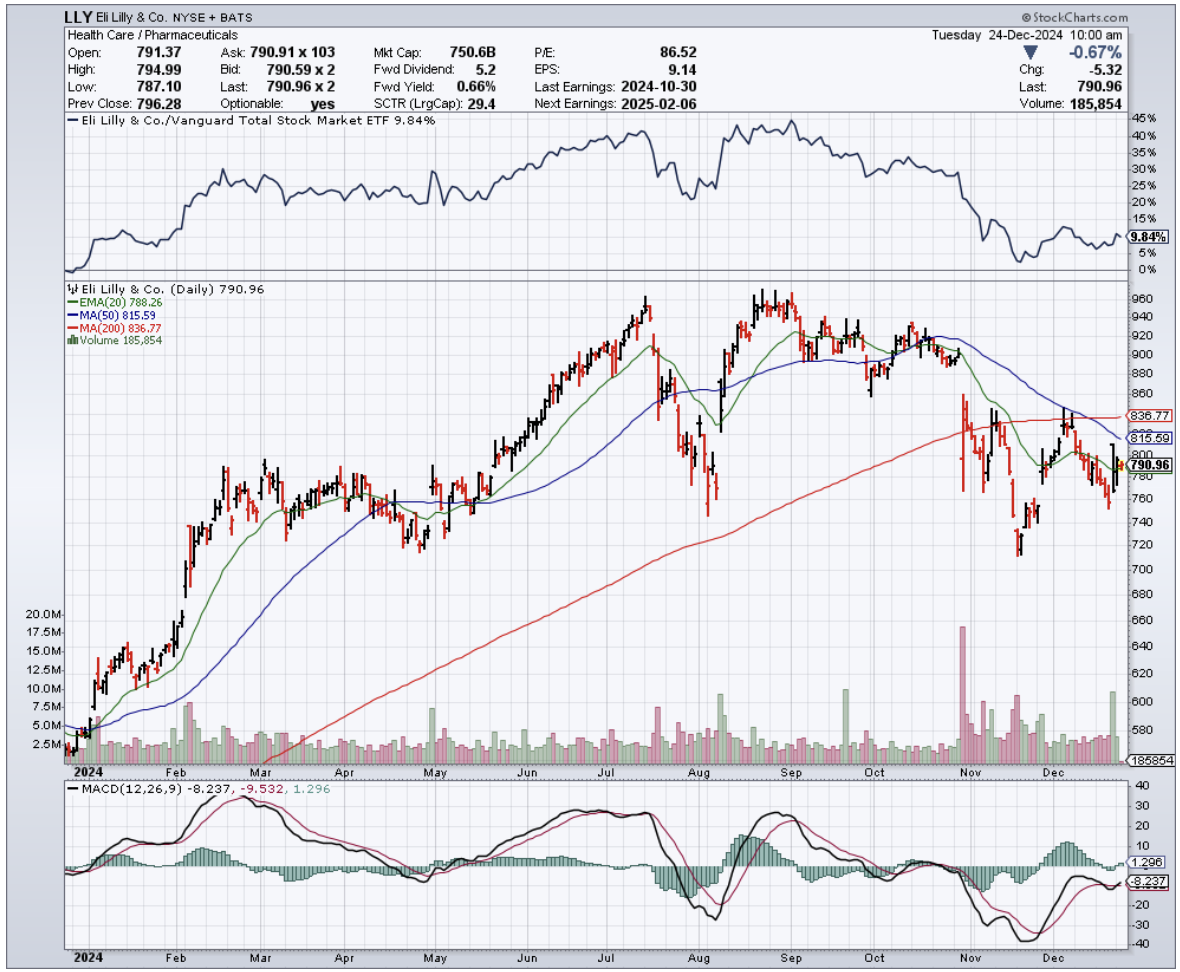

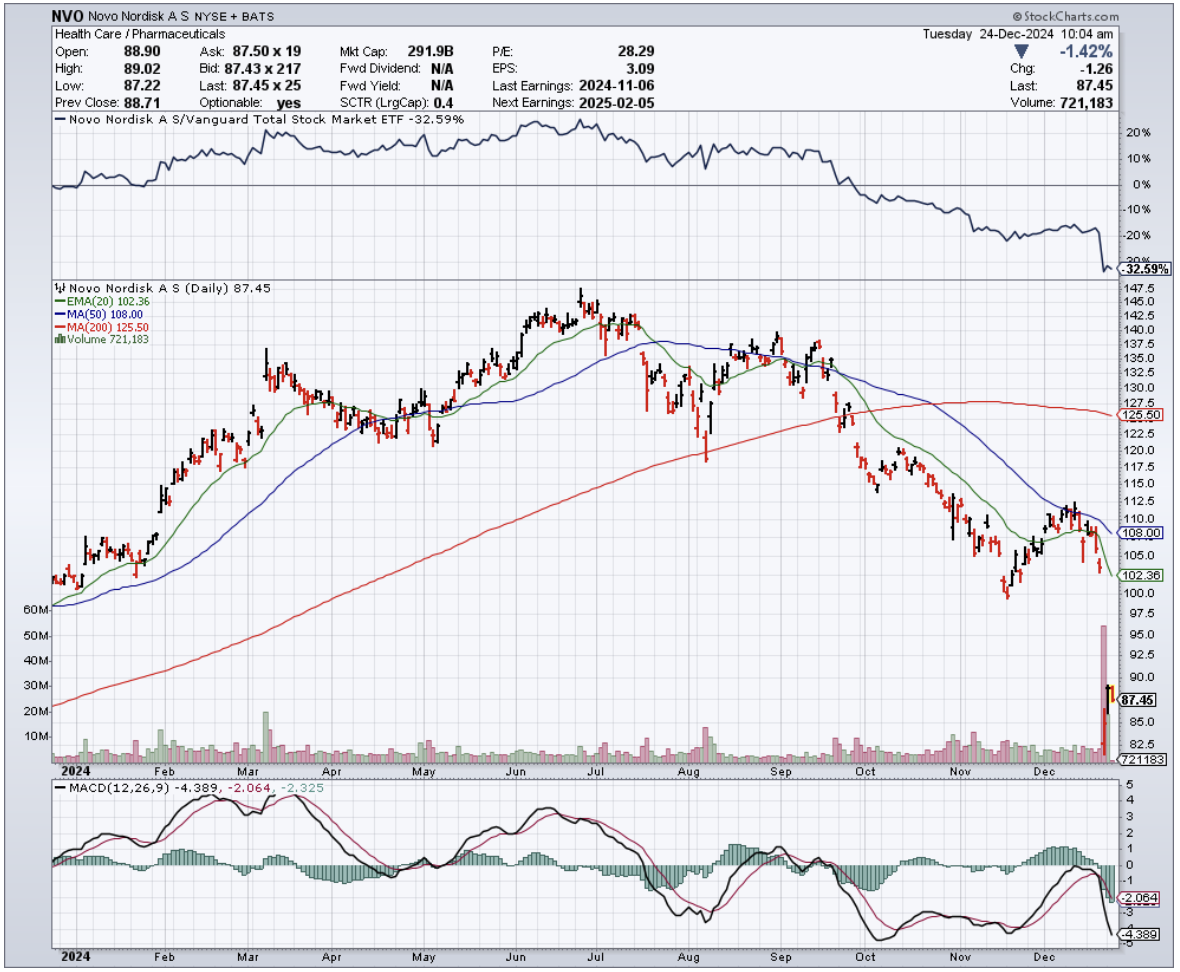

Here's what's really interesting: obesity and GLP-1 drugs are the exception to every rule. After watching Eli Lilly (LLY) and Novo Nordisk's (NVO) recent success, everyone wants a piece of this action.

Even early-stage obesity plays are attracting serious capital, bucking the trend toward late-stage investments.

But remember this about 2025 - being picky about Phase 2 data isn't just smart, it's survival. We're heading into a market where strong clinical validation will matter more than ever.

I've seen enough biotech cycles to know that when the market gets selective, you want to be where the data is solid.

The numbers back this up. Looking at the trends, Phase 2 companies have consistently captured the highest deal sizes, except for that brief period in 2023 when obesity deals sent Phase 1 valuations through the roof.

By 2025, expect this preference for Phase 2 assets to become even more pronounced. Phase 3 investments have been declining - dropping from $4.2 billion in 2021 to $1.7 billion in 2024 - partly because companies with strong Phase 2 data are getting snatched up through partnerships or acquisitions before they even get to Phase 3.

Speaking of partnerships, watch Big Pharma's moves carefully in 2025. They're increasingly hungry for de-risked assets, and strong Phase 2 data is their favorite meal.

I had lunch with a Big Pharma exec last week who told me they've completely restructured their BD team to focus on Phase 2 assets in their regional sweet spots.

As for AI platforms? They'll still get funded - companies like Xaira and Generate:Biomedicines are proving that. But by 2025, they'll need to show more than just fancy algorithms. The market's going to demand real clinical validation.

I recently visited an AI-driven drug discovery company where the CEO proudly showed me their latest neural network. "That's great," I told him, "but show me your clinical data." The silence was deafening.

So, what’s the play here? Well, I'm keeping my own biotech portfolio focused on companies with strong Phase 2 assets heading into 2025, especially in regional sweet spots.

And yes, I've got a position in the obesity space - sometimes a trend is too strong to ignore, even for an old contrarian like me.

One final thought: keep an eye on those time gaps between funding rounds. They're getting longer, and by 2025, companies that don't fit neatly into regional specialties or lack solid clinical data might find themselves in the financial equivalent of a Phase 2 trial that never ends.

Now, if you'll excuse me, I've got a call with a German biotech CEO about their sustainable manufacturing process. These regional specialties aren't going to research themselves.

Mad Hedge Biotech and Healthcare Letter

December 24, 2024

Fiat Lux

Featured Trade:

(THE LAB RESULTS ARE IN)

(GILD), (TSLA), (WVE), (EDIT), (CRSP), (LLY), (NVO), (WMT), (CVS), (CCCC), (RHHBY)

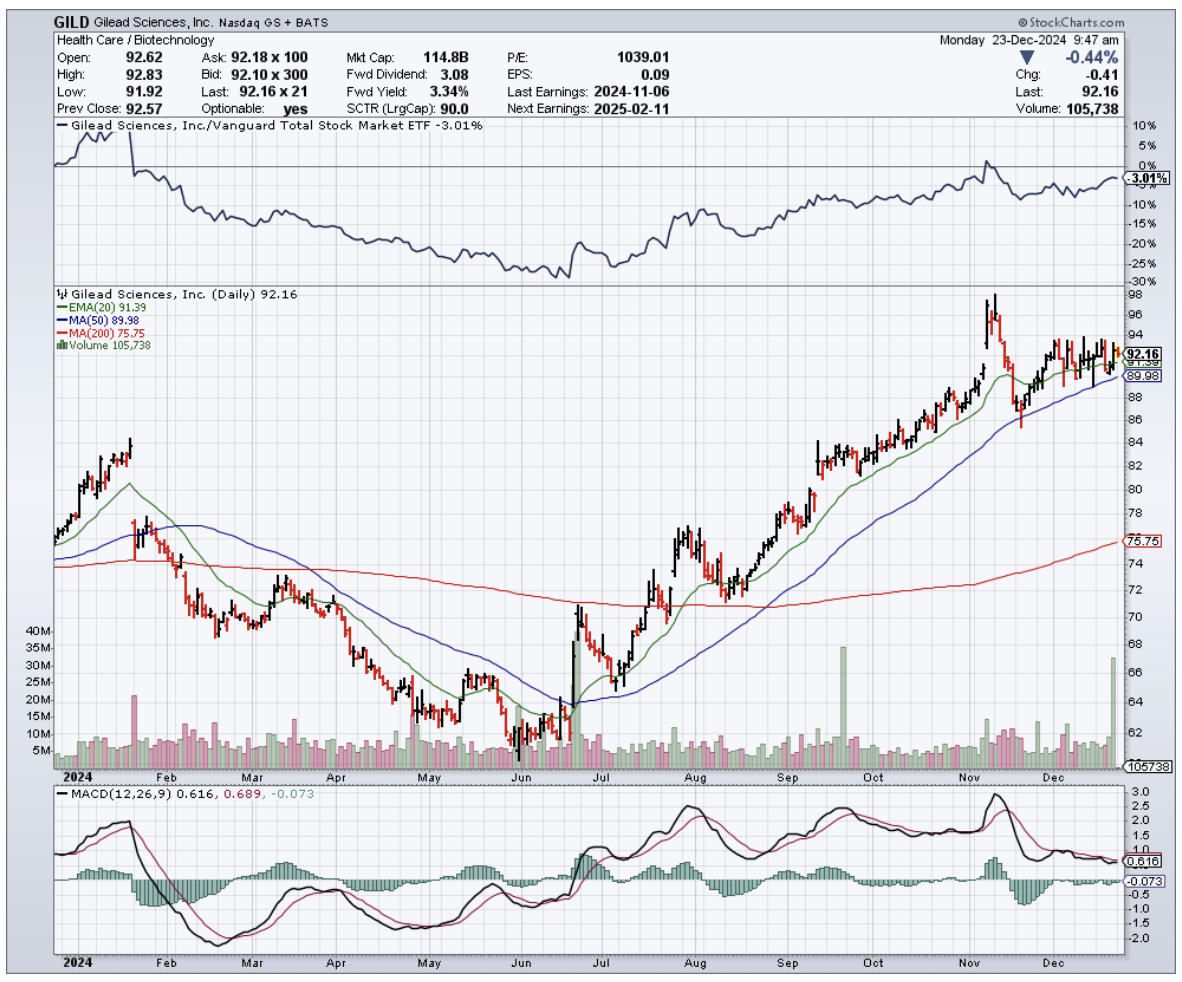

I found myself gridlocked in Bay Area traffic a few days ago, inching past Gilead's (GILD) sprawling Foster City headquarters, when my phone lit up with a call from an old friend at Goldman.

“Alright, tell me—what’s the real story with biotech this year?” she asked, her tone hovering somewhere between curiosity and exasperation. “Half my portfolio feels like a masterstroke, the other half... well, let’s just say it’s testing my patience.”

As I watched a Tesla (TSLA) weave through traffic like it was auditioning for a Fast & Furious reboot, I smiled.

Biotech has always been a bit of a high-stakes chess game—brilliance in one corner, chaos in another, and always a few surprises lurking behind the next move.

“Let me break it down for you,” I said, steering the conversation as carefully as I did my car through the bumper-to-bumper maze.

First, the winners are crushing it, and I mean crushing it. Gilead (GILD) finally cracked the code on HIV treatment, developing what's essentially a vaccine that doesn't require popping pills like they're Tic Tacs.

My contacts in clinical development tell me the Phase 3 data in cisgender women is nothing short of spectacular. With a $6 billion annual market potential by 2028, this isn't just another incremental advance - it's the kind of breakthrough that makes everyone in biotech salivate.

Then there's Wave Life Sciences (WVE) and their RNA editing technology. Remember when we thought CRISPR was the only game in town? Well, Wave just showed us there's more than one way to edit a gene.

Their liver-targeting therapy is the first successful RNA editing in humans - think of it as spell-check for your DNA, but reversible. The market's currently at $1.1 billion, but with 35% CAGR through 2030, this train is just leaving the station.

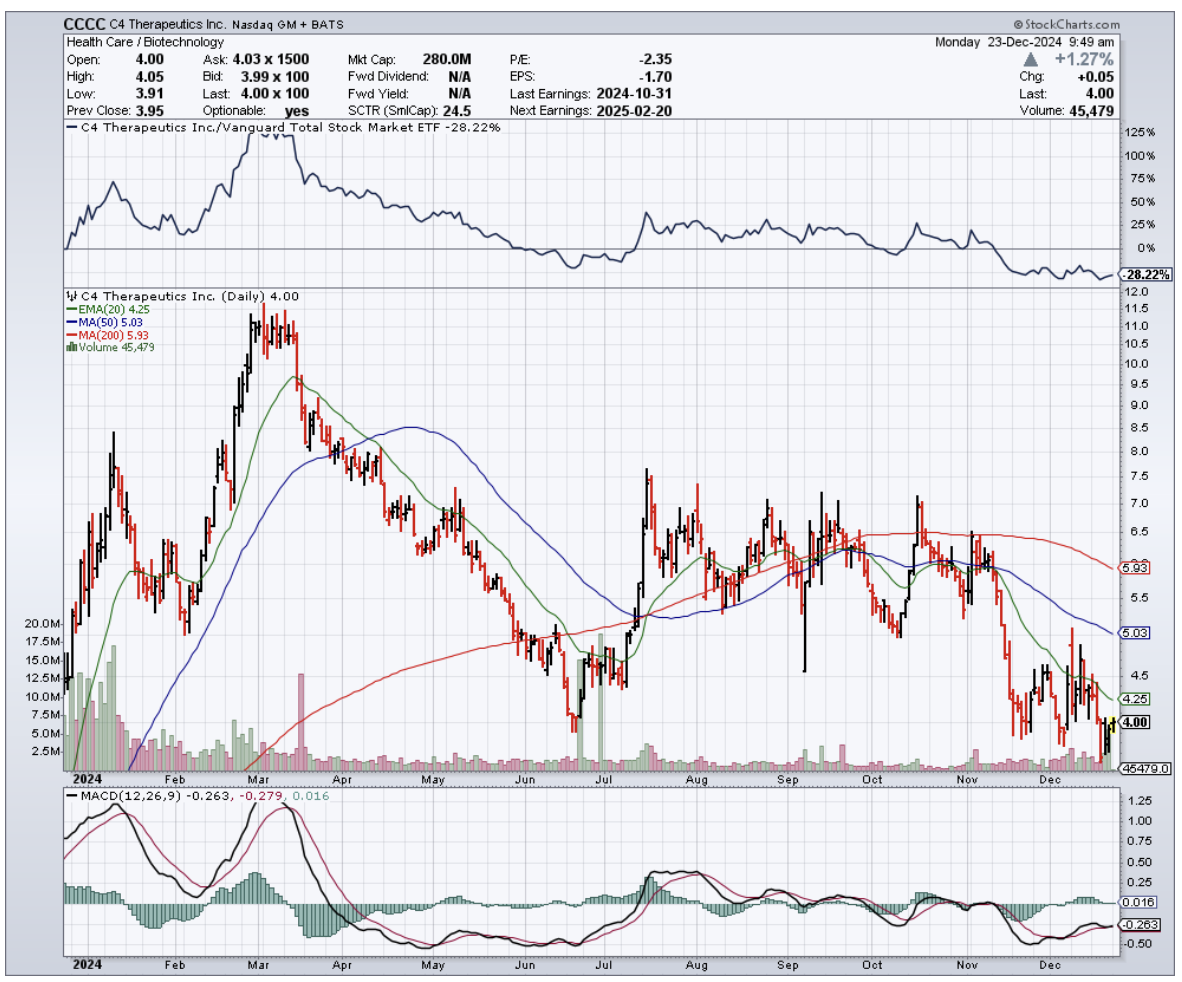

Speaking of trains leaving stations, molecular glue developers like C4 Therapeutics (CCCC) are watching Big Pharma back up the Brink's truck.

We're talking $8 billion in licensing deals this year alone. After all, when Roche (RHHBY) drops $300 million upfront - not milestone payments, mind you, but cold hard cash - you know they've seen something special in the data room.

But here's where it gets interesting, and I had to pull over at this point in the conversation because my friend wasn't going to like what came next.

CRISPR stocks? Down 20%. Editas (EDIT) and CRISPR Therapeutics (CRSP) are learning that revolutionary science doesn't always translate to revolutionary returns.

My friend Janet at the Fed might be talking about higher rates, but these companies are bleeding cash faster than a Silicon Valley startup's WeWork budget.

The obesity market? Unless your name is Eli Lilly (LLY) or Novo Nordisk (NVO), you're probably not having a great time.

Only three startups cleared $100 million in funding this year. In biotech terms, that's like trying to build a house with pocket change.

The global market's sitting at $4.1 billion, but it's more crowded than a San Francisco coffee shop during a tech conference.

And don't get me started on Walmart (WMT) and CVS (CVS) trying to play doctor. They thought they could disrupt traditional healthcare with their “get your physical next to the garden tools” model.

The result? A combined loss of $250 million and a wave of clinic closures.

The lesson here is clear: just because you can sell lightbulbs and Band-Aids in the same aisle doesn’t mean you should try to diagnose strep throat next to the automotive department.

A kid in a modded Subaru WRX cut me off as I wrapped up the call, but I left my friend with this: In biotech, timing is everything.

Gilead and Wave are showing us that patience pays off when the science is solid. Meanwhile, CRISPR stocks remind us that even the most promising technology needs good timing and deep pockets.

So, watch those clinical trial results like a hawk, and keep an eye on where the venture money's flowing.

But most importantly, remember what my old mentor used to say: "In biotech, you're not just betting on the science - you're betting on the scientist, the CFO, and sometimes, just sometimes, on whether people are ready to get their flu shot next to the garden center."

Now, where's that highway patrol when you need them?

Mad Hedge Biotech and Healthcare Letter

December 19, 2024

Fiat Lux

Featured Trade:

(SURVIVAL OF THE SOLVENT)

(KOD), (GOSS), (BLUE), (SIOX), (CDAK), (GLPG)

The biotech industry likes to measure success in breakthroughs, but 2024 taught us to count it in survivors.

Sure, we saw remarkable wins in schizophrenia and obesity treatments - enough to keep Big Pharma writing checks that would make anyone pause.

But those layoff numbers? They keep climbing, and I've seen enough market cycles to know what that means.

Yes, the Nasdaq Biotechnology Index eked out a 5.4% gain in 2023, but don’t let that calm surface fool you.

Beneath it, some companies were taking on water faster than a paper boat in a tsunami. It’s not exactly the environment to make your local biotech cheerleader grin ear to ear.

Still, there is value in understanding what went wrong.

Take Kodiak Sciences (KOD) - and I mean that literally because the market sure did. They watched their high hopes for an age-related macular degeneration treatment encounter the brick wall of trial results that proved no better than existing standards of care.

The market’s reaction was swift and merciless, erasing more than 70% of Kodiak’s valuation. Back in my hedge fund days, we called this kind of drop a "character-building event."

Then there's Gossamer Bio (GOSS), which missed its endpoints in pulmonary arterial hypertension so badly you'd think they were aiming for a different disease altogether.

They learned the hard way that lofty ambitions can deflate at high altitudes when critical endpoints fail to materialize, leaving the company staring at a gaping hole where investor confidence used to be.

Bluebird Bio (BLUE)? They've been playing regulatory red light green light with their gene therapy platform.

Despite having the science that could make this possible, they struggled to justify the hefty R&D spending necessary to bring complex and costly treatments to a market that can turn stingy when results arrive late and uncertain.

Speaking of tough breaks, Sio Gene Therapies (SIOX) discovered the cruel reality that neurodegenerative pipelines rarely behave the way spreadsheets say they should.

And poor Codiak BioSciences (CDAK) - their exosome therapy platform imploded so spectacularly that they were forced to declare bankruptcy.

Even Galapagos NV (GLPG) found itself stuck reassessing once-promising late-stage candidates. Those strategic alliances they bragged about last year aren't looking quite so strategic anymore, either.

It would be easy to pin the blame on management missteps or scientific overreach, but the numbers are showing something else.

FDA’s Center for Drug Evaluation and Research did not exactly smile on the biotech crowd’s ambitions. In 2022, it approved 37 novel drugs. By December 2023, fewer than 30 had made the cut.

Want more sobering statistics? The probability of a drug making it from Phase I to FDA approval sits at 7.9%. In immuno-oncology alone, we've got over 1,500 active trials fighting for attention. Overcrowding would be an understatement.

Meanwhile, global biopharmaceutical R&D spending topped $200 billion in 2022 - that's a lot of investor cash burning through labs with no guarantee of return.

Remember the IPO party from a few years back? Well, 2023 saw fewer than 20 biotech IPOs brave the public markets. That's not caution - that's fear.

For those still interested in this sector - and I know you're out there - some of these disasters might offer lessons, or even opportunities.

The iShares Biotechnology ETF exists for those who prefer to spread their risk. Smart move, considering what we've seen this year.

Let's talk specific names. Bluebird Bio might still have a chance if they can get their regulatory act together and convince insurers to cover their therapies.

Sio Gene Therapies could find new partners - though I wouldn't hold my breath. Galapagos has Gilead (GILD) in their corner, which counts for something in this market.

So here's my take: hold Kodiak if you can stomach more volatility - they've already taken their biggest hits.

Same goes for Bluebird Bio, but only if you've got patience. Galapagos? Keep it, but watch those pipeline updates like a hawk.

Gossamer Bio? Time to consider an exit. Sio Gene Therapies lacks catalysts, and Codiak - well, bankruptcy speaks for itself.

The lesson from Kodiak, Gossamer, Bluebird, Sio, Codiak, and Galapagos is simple: brilliant science means nothing without solid analysis, realistic timelines, and serious cash. 2024 proved that point six times over.

Sure, everyone in biotech wants to change the world. The hard part? Staying solvent long enough to make it happen.

Mad Hedge Biotech and Healthcare Letter

December 17, 2024

Fiat Lux

Featured Trade:

(THE BIG BATCH THEORY)

(CTLT), (DHR), (RGEN), (AVTR), (NVO), (PFE), (LLY), (MRK)

If I had a nickel for every time someone said pharmaceutical manufacturing was boring, I could’ve started bidding against Novo Holdings for Catalent (CTLT) myself.

Sure, I’d still be $16.5 billion short, but you get the point—this deal is huge, and it’s about to make some smart money look even smarter.

Here’s the deal: Novo Holdings is shelling out $16.5 billion to snap up Catalent, a contract development and manufacturing organization (CDMO).

If that acronym sounds like alphabet soup, let me translate: CDMOs are where the real action happens.

These are the guys behind the curtain making sure your miracle drugs and life-saving treatments aren’t just ideas—they’re products hitting the market at scale.

The numbers don’t lie. The CDMO market sits at $146 billion right now.

Fast-forward to next year, and that balloons to $243.3 billion. By 2029, it’s cruising toward a cool $332 billion.

And if you think that’s impressive, just wait: the broader pharmaceutical outsourcing trend is nowhere near slowing down.

In 2014, Big Pharma still clung to in-house production for 66.3% of its output.

Today? That figure’s down to 51%, and dropping fast. Why? Because outsourcing lets the specialists handle the hard stuff—faster, cheaper, and more efficiently.

For investors, Catalent’s immediate upside is a no-brainer. The acquisition premium is pure gravy, but that’s not the whole story.

Rivals like Lonza Group (SWX: LONN) and Samsung Biologics are already feeling the heat.

The biologics CDMO market alone is expected to expand by $10.63 billion between 2024 and 2028, and you better believe those two are scrambling to stay ahead.

If you own shares, keep your seatbelt fastened. If you don’t, well… you might want to rethink that.

And here’s where it gets really interesting: Novo Holdings may be private, but its publicly traded golden child, Novo Nordisk (NVO), is set to ride this wave like a pro surfer.

They’re already a global powerhouse in biologics, and Catalent’s souped-up manufacturing capabilities are going to help them scale production with military-grade efficiency.

Lower costs, tighter operations, bigger margins—it’s like handing a Formula 1 car to an already championship-winning team.

So if you’re not watching Novo Nordisk stock, you’re doing it wrong.

Of course, it’s not just the big CDMO players who stand to win here. Companies like Danaher (DHR), Repligen (RGEN), and Avantor (AVTR) are quietly cashing in on this gold rush.

These firms supply the picks, shovels, and critical bioprocessing tools that CDMOs need to keep production humming.

As Catalent scales under Novo Holdings, demand for these essentials will go through the roof.

Zooming out, the pharma manufacturing landscape is evolving at a breakneck pace.

The CDMO market is expected to hit $530.3 billion by 2033, growing at a steady 7.7% CAGR.

That’s not speculative growth—it’s a structural shift, backed by demand for biologics, gene therapies, and personalized medicine.

In short, we’re entering an era where outsourcing is king, and companies with the infrastructure to capitalize on it are poised to dominate.

Don’t forget about the big dogs in Big Pharma, either.

Pfizer (PFE), Eli Lilly (LLY), and Merck (MRK) aren’t just spectators in this game. They’re snapping up CDMO capacity, investing in biologics, and doubling down on therapies with blockbuster potential.

The Catalent deal is just the latest chess move in a game where the stakes keep getting higher.

So what does this mean for you? If you’re holding Catalent, congratulations—your portfolio is about to get a nice bump.

But the real play here isn’t Catalent alone. It’s understanding that CDMOs, suppliers, and adjacent players are the unsung heroes of this industry transformation.

You want exposure to the companies enabling the next wave of medical innovation? This is where you look.

Novo Holdings just threw down the gauntlet, and the smart money is already moving. The pharmaceutical manufacturing sector isn’t boring—it’s booming.

So, while everyone’s chasing flashy biotech startups and blockbuster drugs, the real smart money is quietly following the companies that make those breakthroughs possible.

Catalent isn’t just a $16.5 billion deal—it’s proof that outsourcing is the new backbone of pharma’s future. Call it “The Big Batch Theory:” scale up, outsource smart, and watch the returns multiply.

Ignore this shift, and you’re leaving money on the table.

Now, if you’ll excuse me, I need to check my CDMO positions. Just like a perfectly run batch, they’re growing fast—and that’s exactly how I like it."

Mad Hedge Biotech and Healthcare Letter

December 12, 2024

Fiat Lux

Featured Trade:

(BREAKING THE MOLD)

(MRK), (PFE), (GILD), (AZN), (DSNKY), (JNJ)

Did you know that in the 1890s, scientists tried to cure cancer by injecting patients with... bread mold? (Spoiler alert: it didn't work.)

Fast forward to 2024, and Merck just announced something that makes moldy bread look like, well, moldy bread: their new cancer drug achieved a 100% complete response rate in its Phase 3 trial.

That's doctor-speak for "the cancer completely disappeared in every single patient." Not 99%. Not 99.9%. One hundred percent.

The drug in question is zilovertamab vedotin, and it belongs to a fascinating family of medications called antibody-drug conjugates, or ADCs.

These drugs are essentially molecular delivery trucks - the antibody part knows exactly where to go, while the drug part carries the cancer-fighting payload.

It's a bit like having a microscopic postal service that only delivers to cancer cells, except instead of Amazon packages, it's delivering something more lethal.

The story of how Merck got their hands on this drug is equally interesting.

In 2020, they wrote a check for $2.75 billion to acquire a company called VelosBio. To put that number in perspective, that's enough money to fund a small space program, or if you're feeling particularly eccentric, to buy 5.5 million laboratory mice (a purchase that would probably raise some eyebrows at the bank).

The global market for ADCs hit $7.72 billion in 2023, and some analysts predict it could reach $44 billion by 2029. I asked three different economists to explain these projections and got four different answers, but they all agreed on one thing: it's a lot of zeros.

And, as expected, the competition in this field is intense. Pfizer (PFE) bought Seagen for $43 billion. AstraZeneca (AZN) and Daiichi Sankyo (DSNKY) partnered up for Enhertu, while Gilead Sciences (GILD) nabbed Immunomedics and their wonderfully named drug Trodelvy.

Even Johnson & Johnson (JNJ), which most people associate with baby shampoo and that bottle of Band-Aids in their medicine cabinet, jumped into the fray by buying Ambrx Biopharma.

Then there's Mersana Therapeutics, partnered with Merck. They're smaller than the pharmaceutical giants, but in biotech, size isn't everything. (I once visited a lab where groundbreaking cancer research was happening in a space roughly the size of my kitchen.)

What makes Merck's achievement particularly remarkable is its rarity. In the world of cancer research, getting a 100% response rate is about as common as finding a unanimous decision on social media. It represents a fundamental shift in how we treat cancer, moving from traditional chemotherapy to these precisely targeted treatments.

For investors wanting a piece of this molecular magic, here's the thing: success in biotech isn't like picking a winning racehorse (though both can make your palms equally sweaty).

It's about finding companies that have mastered the three-ring circus of innovation, partnerships, and research pipelines. And yes, I've spent enough time in research facilities to know that "pipeline" is just a fancy word for "stuff we hope works but haven't broken yet."

Merck's perfect score suggests they've cracked one particular code, but companies like Seagen (now part of Pfizer), AstraZeneca, and Daiichi Sankyo are all pushing boundaries in their own ways.

Despite the competition, Merck's recent achievements still look the most promising. The company's breakthrough with zilovertamab vedotin suggests they're not just throwing darts at a laboratory wall - they're onto something big. So when their stock dips, smart money takes notice.

Similarly, Seagen, now under Pfizer's umbrella, looks particularly promising, especially given their established track record in the ADC space and Pfizer's deep pockets. Add them to your watchlist, too.

AstraZeneca and Pfizer, meanwhile, merit a steady "hold" position in your portfolio - like that reliable sourdough starter that keeps producing even if it's not particularly exciting at the moment.

Both companies have proven ADC programs and the resources to weather market volatility, even if they're not currently serving up the kind of headline-grabbing results that Merck just delivered.

Remember those 19th-century scientists with their bread mold? Turns out, they were onto something, even if their execution was a bit... moldy.

And while I wouldn't recommend their treatment methods today (please don't raid your fridge for experimental purposes), their spirit of innovation lives on in every precisely-targeted ADC molecule. After all these years, I guess you could say cancer treatment has finally risen above its moldy beginnings.