Global Market Comments

July 31, 2015

Fiat Lux

Featured Trade:

(SO WHAT IS YOUR ?INFLUENCER? SCORE)

(REPORT FROM THE ORIENT EXPRESS)

Global Market Comments

July 30, 2015

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE AUGUST 3 ZURICH, SWITZERLAND GLOBAL STRATEGY LUNCHEON),

(WELCOME TO THE DEFLATIONARY CENTURY),

(TLT), (TBT),

(MY PERSONAL ECONOMIC INDICATOR),

(HMC), (NSANY), (GM), (F), (TSLA)

iShares 20+ Year Treasury Bond (TLT)

ProShares UltraShort 20+ Year Treasury (TBT)

Honda Motor Co., Ltd. (HMC)

Nissan Motor Co. Ltd. (NSANY)

General Motors Company (GM)

Ford Motor Co. (F)

Tesla Motors, Inc. (TSLA)

Come join me at the?Mad Hedge Fund Trader?s?Global Strategy luncheon, which I will be conducting in the banking capitol of Zurich, Switzerland at 12:00 PM on Monday, August 3, 2015. A three course lunch will be provided.

I?ll be giving you my up to date view on stocks, bonds, foreign currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too.

Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $227.

I?ll be arriving at noon and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The event will be held at a well known central Zurich hotel. The details will be emailed directly to you with your confirmation.

Zurich usually empties out every August, with the Swiss fleeing for Mediterranean beaches, so it is a great time to visit.

Munster Square in the Old Town gives you the flavor of medieval Europe. The vertical needle like Fraumunster is a must see cathedral.

Bahnhoffstrasse offers plenty of shopping, if you don?t mind paying full retail and through the nose. The Swiss National Museum offers a fine display of ancient weapons. Zurich is also a very bicycle friendly city, with several rental locations along the lake.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets to the Seminar, please?click here.

Global Market Comments

July 29, 2015

Fiat Lux

Featured Trade:

(PRESIDENT HILLARY?S COMING TAX HIT),

(THOUGHTS AT SEA ABOARD THE QE2-PART III)

Come join me for afternoon tea for the?Mad Hedge Fund Trader?s?Global Strategy Seminar, which I will be conducting high in the Alps in Zermatt, Switzerland at 2:00 PM on Friday, July 31, 2015.

The guests and I will engage in an open discussion on the crucial issues facing investors today.?Coffee, tea, and schnapps will be made available, along with light snacks.

I?ll be giving you my up to date view on stocks, bonds, foreign currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too.

Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $197.

I?ll be arriving early and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The event will be held at a central Zermatt hotel with a great Matterhorn view, operated by one of the village?s oldest families and long time friends of mine. The hotel is just down the street from the town?s beautiful 17th?century church. The details will be emailed directly to you with your confirmation.

You are welcome to attend in your mountain climbing gear, but you will have to leave your boots at the door. Socks only are welcome, and if it?s cold, we will throw some extra wood on the fire.

Last year, someone came down from the Matterhorn summit straight to the seminar, sunburned and tired, but elated. He even gave me a valued pebble from the summit.

The Swiss National Day is on Saturday, August 1 and Zermatters throw a blowout party to celebrate the event. Citizens converge on the village from all over Switzerland to participate in an hour long parade up the main cobblestoned street, dressed in traditional folk costume and playing mountain instruments.

The Bahnhofstrasse is packed with merchants offering national dishes, fine pastries and plenty of local beer and wine. We usually end up dancing a polka in front of the town church.

If you can still stand up, giant bonfires are lit on the surrounding mountain peaks at sunset, followed by an impressive fireworks display. For the last three years, a torrential downpour followed.

It is all a complete blast, so I attend every year.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets to the Seminar, please?click here.

Life is good.

Since my last letter to you, I hired a Mercedes and a Moroccan driver, driven the three hours from Tangier to Casablanca, and spent a day touring the architecture of the French colonial art deco center of that storied city.

It turns out that my driver only did his job part time. He was in fact a graduate student in economics studying in Tangier and had a lot to say about his fascinating country?s economy.

Jackpot!

I?ll write up his comments in a future letter, subject to the regular fact checking with the IMF and the World Bank. Until then, we have winnings of a difference sort to discuss.

It has been a pretty prosperous time for followers of the Mad Hedge Fund Trader?s trade alert service as well.

After staying out of the market during a tempestuous, white knuckled month, I finally sense an interim market bottom.

In quick order, I phone Trade Alerts into the head office to buy Apple (AAPL), the S&P 500 (SPY), and to sell short the Japanese yen (FXY), (YCS). I caught a $12 move in (AAPL) and a 4% move in the (SPY).

The yen vaporized, producing a very speedy 16.5% profit, which I quickly seized.

I then sought to protect my gains by adding a new short position in the (SPY) close to the recent highs. To get risk neutral, I then added a short position in Treasury bonds (TLT), (TBT).

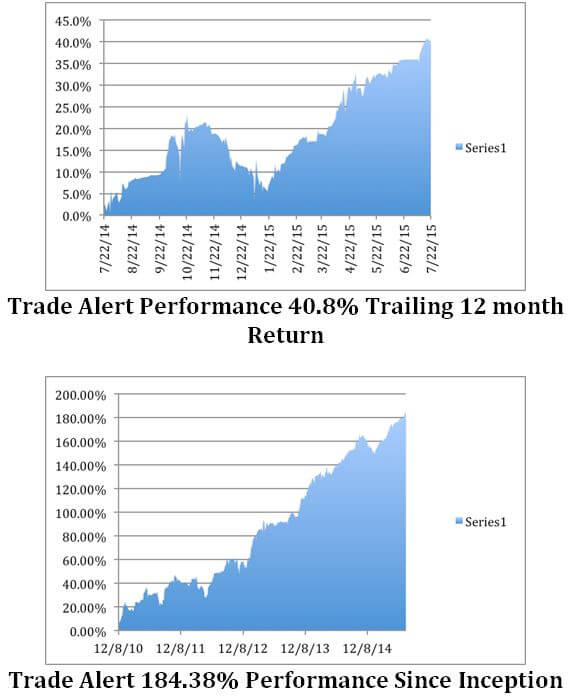

The fruit of these labors was to take the Mad Hedge Fund Trader?s performance for 2015 up to a new all time high at 31.54%. July alone was as hot at the Sahara Desert that I recently escaped, up 4.86%.

This brings my performance since inception four years and eight months ago to 184.38%. That annualizes out to 39.5% per year, not bad in this topsy turvey world. It seems like only a Madman can prosper in these hopeless trading conditions.

Some 15 of the last 16 consecutive Trade Alerts, over the past three months, have been profitable. Followers have found themselves in the green every month of 2015, quite substantially so.

Better than a poke in the eye with a sharp stick. And the best is yet to come!

I started out 2015 with the goal of earning 25% for my readers during the first half, and another 25% in the second half. This latest batch of trades puts me right on track for reaching my yearend goal.

I should take these extended research trips more often! My back office tells me that subscriptions have been falling off in North Korea, Mali has been weak of late, and that a strategy luncheon in Bhutan would be welcome any time.

Under promise and over deliver; it has always been a winning business strategy for me.

This is against a backdrop of major market indexes that are nearly unchanged so far this year, despite sudden bursts of volatility and long, Sahara like stretches of boredom.

The key to winning this year has been to put the pedal to the mettle during those brief, but hair raising selloffs, and then take quick profits. They don?t call me ?Mad? for nothing.

When the market is dead, you sit on your hands.

After all, you are trying to pay for your own yacht, not your broker?s.

When the market pays you to stay away, you stay away.

Those who have made the effort to wake up early every morning and read my witty and incisive prose have an impressive row of notches on their bedpost to show for their effort.

My groundbreaking trade mentoring service was first launched in 2010. Thousands of followers now earn a full time living solely from my Trade Alerts, a development of which I am immensely proud.

Some 50% of my clients are over 50 and managing their own retirement funds fleeing the shoddy but expensive services provided by Wall Street. The balance is institutional investors, hedge funds, and professional financial advisors.

The Mad Hedge Fund Trader seeks to level the playing field for the average Joe. Looking at the testimonials that come in every day, I?d say we?ve accomplished that goal.

It has all been a vindication of the trading and investment strategy that I have been preaching to followers for the past eight years.

Quite a few followers were able to move fast enough to cash in on my trading recommendations. To read the plaudits yourself, please go to my testimonials page by clicking here. Our business is booming, so I am plowing profits back in to enhance our added value for you.

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011, 14.87% in 2012, 67.45% in 2013, and 30.3% in 2014.

Our flagship product,?Mad Hedge Fund Trader PRO, costs $4,500 a year. It includes?Global Trading Dispatch?(my trade alert service and daily newsletter).

You get a real-time trading portfolio, an enormous research database, and live biweekly strategy webinars. You also get Bill Davis?s Mad Day Trader service, which provides great intra day market color.

To subscribe, please go to my website, ?www.madhedgefundtrader.com, click on the ?Memberships? located on the second row of tabs.

And now for the rest of the year.

I can?t wait!

Letter From Casablanca

Letter From Casablanca

The conspiracy theorists will love this one.

Buried deep in the bowels of the 2,000 page health care bill was a new requirement for gold dealers to file Form 1099's for all retail sales by individuals over $600. Specifically, the measure can be found in section 9006 of the Patient Protection and Affordability Act of 2010.

For foreign readers unencumbered by such concerns, Internal Revenue Service Form 1099's are required to report miscellaneous income associated with services rendered by independent contractors and self-employed individuals.

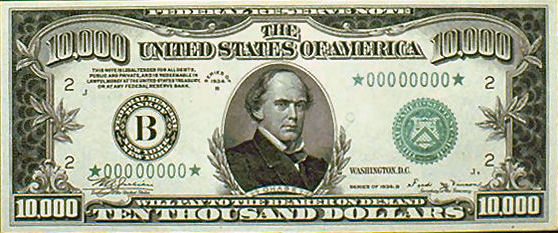

The IRS has long despised the barbaric relic (GLD) as an ideal medium to make invisible large transactions. Don?t you ever wonder what happened to $500, $1,000, $5,000, $10,000, and $100,000 bills?

The $100,000 bill was only used for reserve transfers between banks, and was never seen by the public. The other high denomination bills were last printed in 1945, and withdrawn from circulation in 1969.

Although the Federal Reserve claims on their website that they were withdrawn because of lack of use, the word at the time was that they disappeared to clamp down on money laundering operations by the mafia. In fact, the goal was to flush out income from the rest of us.

Dan Lundgren, a republican from California's 3rd congressional district, a rural gerrymander east of Sacramento that includes the gold bearing Sierras, has introduced legislation to repeal the requirement, claiming that it places an unaffordable burden on small business.

Even the IRS is doubtful that it can initially deal with the tidal wave of paper that the measure would create.

Currency trivia question of the day: whose picture is engraved on the $10,000 bill? You guessed it, Salmon P. Chase, Abraham Lincoln's Secretary of the Treasury.

Ever Wonder Where The $10,000 Bill Went?

Ever Wonder Where The $10,000 Bill Went?

Global Market Comments

July 28, 2015

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE JULY 31 ZERMATT, SWITZERLAND GLOBAL STRATEGY SEMINAR),

(MAD HEDGE FUND TRADER HITS 31.5% GAIN IN 2015),

(WILL GOLD SUFFER THE FATE OF THE $10,000 BILL?)

(GLD), (GDX)

SPDR Gold Shares (GLD)

Market Vectors Gold Miners ETF (GDX)

Global Market Comments

July 27, 2015

Fiat Lux

Featured Trade:

(AUGUST 3 ZURICH, SWITZERLAND GLOBAL STRATEGY LUNCHEON)

(SO WHAT?S NEXT FOR THE MARKETS?),

(SPY), (QQQ), (AMZN), (GOOG), (AAPL), (FB), (GILD), (DIS),

(TESTIMONIAL)

SPDR S&P 500 ETF (SPY)

PowerShares QQQ Trust, Series 1 (QQQ)

Amazon.com Inc. (AMZN)

Google Inc. (GOOG)

Apple Inc. (AAPL)

Facebook, Inc. (FB)

Gilead Sciences Inc. (GILD)

The Walt Disney Company (DIS)

I am writing to you from the bar of the El-Minzah Hotel in Tangiers, Morocco, a one-time favorite of literary greats, F. Scott Fitzgerald, Earnest Hemingway, and Paul Bowls.

A warm, languid breeze coming off the Atlantic Ocean is causing the date palms around the pool to sway in rhythmic fashion.

The city has long been a hotbed of espionage, international intrigue, and illicit trade. It was once home of the Barbary Pirates.

I first came here in 1968 and slept on the roof of a run down medina inn for 50 cents a night and thought it was the deal of the century.

How times change.

If you recognize the place from the pictures below, there?s a good reason. It is the location on which Rick?s Caf? Americain was based in the 1942 Humphrey Bogart film classic, Casablanca, complete with a grand piano.

Damn, and I already sent my white dinner jacket home!

Whenever I check into a hotel with decent broadband or WiFi, I undertake the same ritual drill. It is a practice born of a half century of analyzing markets.

I go to the ever-trustworthy www.stockcharts.com and rapidly run through 100 charts among all asset classes. This immediately gives me an instant snapshot of the global economy, and where to find the action in financial markets.

And what I?m finding today is nothing less than astounding.

On the one hand, a very impressive collapse of all energy, commodity, and precious metal prices suggests that we have already fallen into the morass of a severe recession.

On the other, some 77% of US companies beat forecasts for Q2 earnings and are painting a rosy picture of the future, confirming that the moderate economic recovery still has legs.

Which asset class has it right, and which one is missing the target?

I?ll go with the expansion scenario. I think that the stock market crash in the former Red China is sending us all schools of red herrings on the prediction front.

Middle Kingdom margin calls are triggering capitulation sell offs across the commodities board, leading to fears that the woes of newbie stock speculators will feed into the main economy. This, in turn, will prompt a global recession.

I don?t think this will happen. Rampant stock speculation was engaged in by only 4% of the population, with most of the gains confined to a couple of months.

Most of this was mere paper gains that went as quickly as they came. Thankfully, this was not a decade long build up, like the one we saw in NASDAQ during the 1990?s, which would have been far more damaging.

Furthermore, the government in Beijing is doing everything they can to prevent the collapse from going systemic. I think they will succeed. Only 3% of listed Chinese shares are now freely tradable.

The creation of financial markets from scratch for a major economy, which the Chinese are now attempting to engineer, was never going to be easy. I know, because I went through this with Japan 40 years ago.

Everything else that could have gone wrong this year, Iran, Greece, the Supreme Court decision on Obamacare, the Ukraine crisis, Iraq, has now passed us by, all resolving for the positive, as far as stock markets are concerned.

We have run out of things that could go wrong. A possible ?% Fed interest rate rise in September is so insignificant that it doesn?t even show up on the radar.

So it?s simple. Wait for the Chinese stock bubble to unwind, and then load the boat with global equities.

Except that it?s not that simple.

The US equity markets have been so boring this year that it is creating a situation that is unprecedented in the history of technical analysis. Volatility is now at a staggering 100 year low.

According to the Wall Street Journal, only six stocks, Amazon (AMZN), Google (GOOG), Apple (AAPL), Facebook (FB), Gilead Sciences (GILD), and Walt Disney (DIS) have accounted for more than the entire $199 billion in gains in the S&P 500 this year.

The other 494 stocks in the big cap index have, for the most part, been unchanged, or are losers.

I am proud to say that four of these six, (GOOG), (AAPL), (GILD), and (DIS) have been the subject of successful Trade Alerts or bullish research reports in this newsletter.

That?s not a bad home run record. Just go to www.madhedgefundtrader.com a search for the reports.

The situation is nearly as dire with the NASDAQ (QQQ), where the same stocks account for half of the $664 billion in gains there.

To long in the tooth traders, such as myself, a technical set up like this against falling volume this isn?t just a red warning light. It is an entire Christmas tree?s worth of warning lights.

You can see this in all its eloquence in the chart below of a declining advance/decline ratio, which broke its 200-day moving average on Friday.

This is why I shot out a Trade Alert last week to bail on my ?RISK ON? short position in the Japanese yen (FXY) and to sell short the (SPY).

Now here is the really scary part. All of this is setting up going into the two highest risk months of the year, September and October, from which the legendary stock crashes of old spring.

In other words, the calendar couldn?t be worse for traders.

So here is the bottom line. Positive fundamentals have been checkmated by negative technicals. So we may go nowhere for a while, until corporate earnings catch up with share prices and make them look cheap once again.

S&P 500 earnings traded at 17 times earnings on Friday. Get them back to 16 times earnings in a zero interest rate world, and new money will come pouring in.

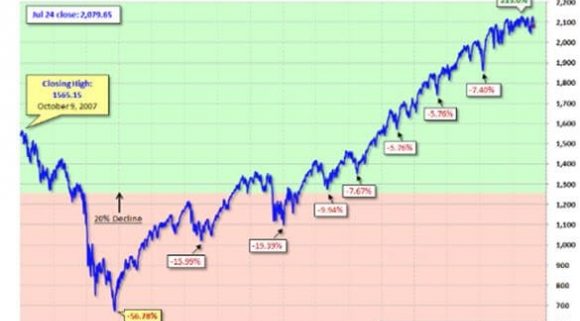

That means we may have to suffer the umpteenth 5% correction of this bull market in the weeks ahead (see chart below), or 10% in a really extreme case.

Just thought you?d like to know.