“Creativity is just connecting things.” – Said Co-Founder of Apple Steve Jobs

“Creativity is just connecting things.” – Said Co-Founder of Apple Steve Jobs

“Unless you are breaking stuff, you are not moving fast enough.” – Said CEO of Facebook, Mark Zuckerberg

“Patience is a virtue, and I'm learning patience.” – Said CEO of Tesla Elon Musk

Mad Hedge Technology Letter

September 5, 2025

Fiat Lux

Featured Trade:

(HUMANOIDS TO THE RESCUE OR NOT)

(TSLA), (LLM), (AI)

“When something is important enough, you do it even if the odds aren’t in your favor.” – Said Tesla Founder Elon Musk

Mad Hedge Technology Letter

May 12, 2025

Fiat Lux

Featured Trade:

(THE FIGHT FOR AI SUPREMACY)

($COMPQ), (AMZN)

Mad Hedge Technology Letter

May 9, 2025

Fiat Lux

Featured Trade:

(THE FIGHT FOR AI SUPREMACY)

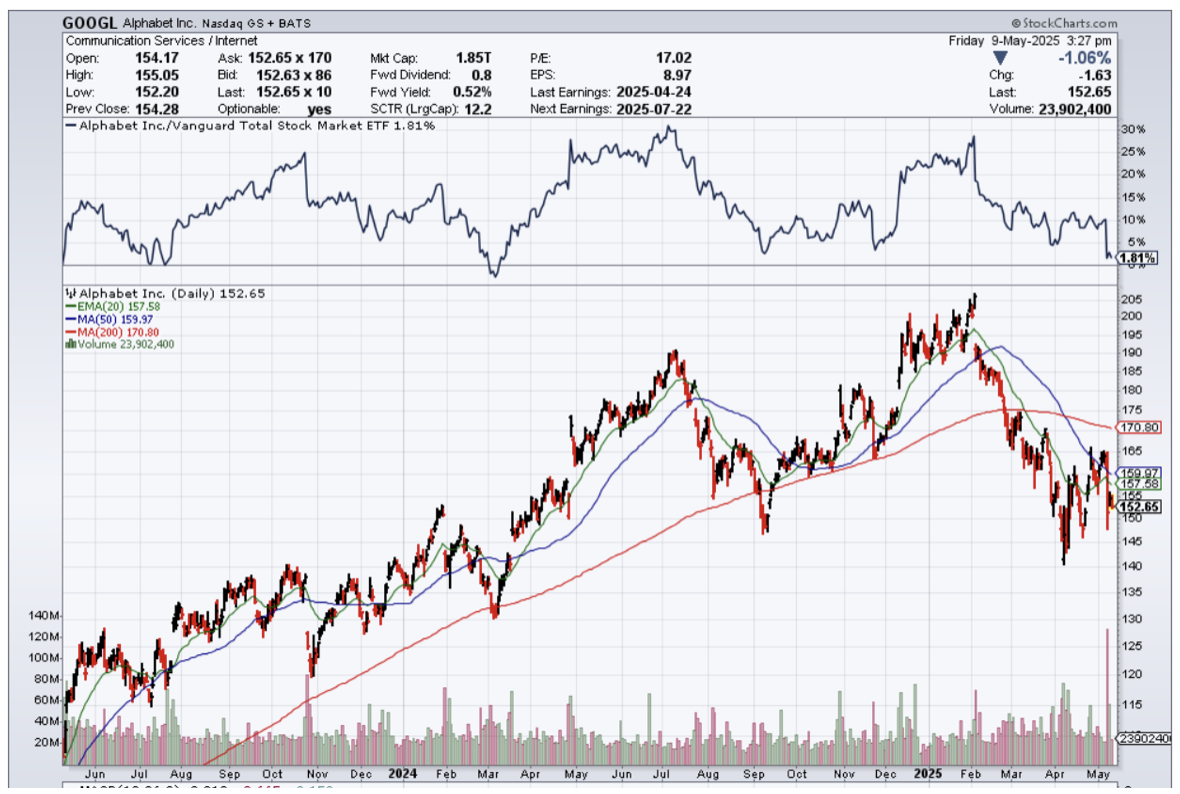

(GOOGL), (AAPL)

We are getting to the part of the cycle where tech could potentially be cannibalizing each other.

The fact is that the overall pie is not growing fast enough, and competition is.

Search is a massive market, and participants are all vying for ad dollars.

Once what was thought of as a duopoly is no longer that and Facebook and Google will need to fight that much harder to command the growth rates they were accustomed to.

The US consumer is gradually becoming weaker and allocating a bigger part of their budget to essentials.

An Apple testimony by one of its executives has now revealed that search operations on Google via Apple's Safari browser decreased for the first time in April 2025, attributing this decline to users increasingly opting for AI-powered tools instead of traditional search engines.

Google’s parent stock Alphabet, was crushed in trading.

This time of development is really damaging for Google, and it puts doubt on their ability to negotiate higher ad rates moving forward.

The executive blamed AI platforms like OpenAI, Perplexity, and Anthropic as alternatives that are becoming more appealing to consumers, signaling a future where AI could play a central role in search functionalities on Apple devices.

The implications of Cue's testimony are profound, especially considering that Apple reportedly receives over $20 billion annually from Google to maintain its status as the default search engine on iPhones and iPads. This lucrative arrangement lies at the heart of the antitrust case brought by the U.S. Department of Justice against Google, raising questions about the competitive landscape of the search engine market.

The market believes that AI will disrupt Google's dominance in search. The decline in stock prices reflects investor anxiety about whether AI could significantly erode Google's market share, which currently stands at approximately 90% of the global search engine market, including a commanding 94% on mobile devices and 79% on desktops.

As the landscape of search technology evolves, the competition between traditional search engines like Google and emerging AI platforms will likely intensify.

As the antitrust case against Google unfolds, the stakes are high not only for the company but also for the broader tech ecosystem. The outcome could have lasting implications for how search engines operate and how consumers access information in the digital age.

Technology is barreling straight into a hairy situation in which the winner will take all in the AI race.

There won’t be enough profits to share around, and the company with the best product will win with consumers.

Search is just one place where AI is being fought.

I do believe we will see the fall of big tech companies, and the ones who are one-trick ponies will run the risk of becoming irrelevant quickly.

Is it fair?

No, but the market will tell us how good each tech companies does AI.

This is bad news for both Apple and Google, and it is not news that these two are lagging far behind in the AI arms race.

However, I do believe this is a good short-term buy-the-dip moment for Google for a trade.

With us moving deeper into 2025, investors are chomping at the bit to hear the commentary about AI developments.

There will be some big disappointments, are those companies unable to recover will be a sell the rallies type of stock.

“Any product that needs a manual to work is broken.” – Said CEO of Twitter Elon Musk

Mad Hedge Technology Letter

May 7, 2025

Fiat Lux

Featured Trade:

(AI AND LOWER EMPLOYEE WAGES)

(TSLA)