“If I had asked what the customers wanted, they would have told me faster horses,” said Henry Ford.

“If I had asked what the customers wanted, they would have told me faster horses,” said Henry Ford.

Global Market Comments

February 9, 2023

Fiat Lux

Featured Trade:

(THE BULL CASE FOR BANKS),

(JPM), (BAC), (C), (WFC), (GS), (MS)

CLICK HERE to download today's position sheet.

Urgent Trader Warning: The Mad Hedge Market Timing Index moved to a one-year high yesterday and is in “STRONG SELL” territory. Any long stock positions you have for the short-term should be hedged. For more details, please visit my Refresher Course at Short Selling School by clicking here.

Caveat Emptor!

“Americans are nothing but self-indulgent weaklings,” said Japanese admiral Isoroku Yamamoto in 1941.

Global Market Comments

February 8, 2023

Fiat Lux

Featured Trade:

(AN EVENING WITH TRAVEL GURU ARTHUR FROMMER)

CLICK HERE to download today's position sheet.

Urgent Trader Warning: The Mad Hedge Market Timing Index moved to a one-year high yesterday and is in “STRONG SELL” territory. Any long stock positions you have for the short-term should be hedged. For more details, please visit my Refresher Course at Short Selling School by clicking here.

Caveat Emptor!

“What is America but beauty queens, millionaires, stupid records, and Hollywood,” said Adolph Hitler in 1941.

Global Market Comments

February 7, 2023

Fiat Lux

Featured Trade:

(THE MAD HEDGE DICTIONARY OF TRADING SLANG)

CLICK HERE to download today's position sheet.

Note: We are moving webinar platforms to Zoom for the February 8, 12:00 EST Mad Hedge Biweekly Strategy

Webinar. To join, please click here.

The Diary of a Mad Hedge Fund Trader is read in 140 counties. About a quarter of our readers run the letter through a Google Translator before reading.

That has created a problem.

Stock trading is probably the most slang and acronym-ridden profession on the planet, second only to the United States Marine Corps. (Semper Fi).

And guess what? The Google Translator has never worked on the floor of a major stock exchange.

That means its translations often come out as gobbledygook or complete nonsense. So, the customers email me asking what the heck I am talking about in my daily newsletters, eating up a portion of my day.

I am therefore enclosing “The Mad Hedge Fund Trader’s Dictionary of Traders’ Slang” below.

To keep this a PG-rated publication, I have left some terms undefined, but you can make a good guess as to their true meaning. It turns out that most traders never got to finishing school, and many are not even gentlemen.

If any of you out there have additional terms you would like to add, please email them to me at support@madhedgefundtrader.com and put “DICTIONARY” in the subject line. I’ll use them in a future update. No doubt there are hundreds, if not thousands more.

Read, enjoy, and laugh.

Accelerated Time Decay – The increasing decline of the value of a stock option as it approaches its expiration date

Black Swan – A term made popular by Nassim Taleb that refers to a sudden, unexpected, low-probability event that has a disproportionately high impact on your portfolio.

Boredom Trading – reaching for marginally profitable trades during quiet markets because there is nothing else to do. Usually a bad idea.

Bottoming Process – When a market makes several failed attempts to make new lows, creating a medium term bottom

Blow off Top – The top of a price spike upward usually associated with a volume spike as well

Bubble – Any assets class rising in price far above and beyond any rational valuation measures

Buy the Dip – BTD/BTFD/BTMFD - Buy the recent decline in prices.

Don’t Catch a Falling Knife – don’t try and buy a stock in free fall

Don’t be a Hero – keep positions small during volatile markets

“Be greedy when others are fearful, and fearful when others are greedy” is a classic Benjamin Graham quote which means “buy bottoms and sell top.”

Pigs Get Slaughtered – Buy a position that is too big for you and it will turn around and bite you

Bull Trap – a strong market move up that sucks in buyers and then dies as soon as the last one is in

Bear Trap – A strong market move down that sucks in lots of short sellers and turns around as soon and the last one sells

Buy When There is Blood in the Streets – Buy stocks at market bottoms

Capitulation Bottom – The last bull throws in the towel, gives up, and dumps all his stock, making the final bottom of a major move

Capitulation Top – The last bear throws in the towel, gives up, and jumps into the market late, making the final top of a major move

Choppy – sudden and erratic price moves within a narrow range

Contrarian – one who trades against the general market consensus

Dead Cat Bounce – A brief rally in s stock that has just seen a sharp drop

Dialing for Dollars – Calling brokerage house customers to sell stocks for commissions

Don’t Fight the Fed – Don’t expect markets to fall when interest rates are falling

Don’t Fight the Tape – Don’t trade against the market trend. Comes for the paper ticker tapes that once transmitted stock prices by telegraph

Dry Powder – Keeping cash in reserve for better trading opportunities

Dumb Money – what inexperienced retail investors are doing. Thanks to the internet, they’re not as dumb as they used to be

Get Filled – Your order is executed

Growing Hair on It – Keeping a position for too long

The Greeks – Greek alphabet letters that refer to option valuation components, such as delta, theta, gamma, and vega

High-Frequency Traders (HFT) – Firms using sophisticated computer programs to take positions for infinitesimally short periods of time taking microscopic profits in enormous volumes. They account for roughly 70% of daily trading volume

Holding the Bag – you are left holding stock in a falling market or short in a rising one

Honor Your Stops - don’t make excuses for ignoring stop losses. This is where the really big hits come from

Killing It – Making a series of successful trades

Locked Market – When the bid and offer are identical

Market Makers – firms that provide market liquidity with two-sided bids and offers, now largely replaced by computers

Melt Up – A straight line move upward in shares with no pullbacks whatsoever, usually triggered by a news or earnings release

Momo – Momentum-based trading, buying rising markets and selling falling ones

Never Short a Dull Market – Quiet markets can often rally sharply because the selling is done

Noise – Random media reporting that has no true impact on the direction of stock prices

Pain Trade – the market is moving against the positions of the trading community

Permabear – A persona who is always bearish, usually driven by some bizarre Armageddon-type ideology, or suffering from paranoia

Permabull – a person who is always bullish, despite deteriorating fundamental conditions

Picking Up Pennies in Front of a Steamroller – Sell short naked put options

Pump and Dump – Unethical brokers run of the prices of small illiquid stocks and then sell them to clients at market tops. The shares usually collapse afterwards. See the movie Wolf of Wall Street

Resistance Level – A price on a stock chart offering technical resistance to further price appreciation

Sell in May and Go Away – The preference for selling shares ahead of a period of seasonal weakness

Sell the Rip – STR/STFR/ STMFR

Short Squeeze – A sharp run-up in share prices that forces short sellers to buy to avoid accelerating losses.

Smart Money – what the best informed, most experienced investors are doing. Not as smart as they used to be.

Snakebit – A surprise news development that comes out of the blue and costs you money

Spoofing – entering orders without any intention of executing them and cancelling them before they can be executed. It is a common tactic of high-frequency traders

Spoos – S&P 500 futures contracts

Squak Box – A small loudspeaker on a desktop in a trading room constantly broadcasting news reports and large trades

Support Level – A price on a stock chart offering significant technical support

Stop Loss - a price at which, when reached, a liquidation of the position is automatically triggered

The Trend is Your Friend – Trade with the market direction, not against it

Theta Burn – Time decay on options

Ticker Tape – A white ¾ inch wide paper tape used to transmit stock prices by telegraph at the rate of 500 characters a minute that was used until the 1950s to transmit stock prices. See ticker tape parade and delayed tape.

Topping Process – occurs when a market makes several failed attempts to make a new high, creating a medium term top

Turnaround Tuesday – the tendency of markets to reverse direction after the markets digest weekend news on a Monday

Yellen Put – an assumption that the Fed will come to the rescue with a monetary easing on any substantial market selloff

“If one of my competitors were drowning, I’d throw them an anchor,” said the legendary Ray Kroc, the founder of McDonald’s.

Global Market Comments

February 6, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE WHIPSAW)

(SPY), (TLT), (TSLA), (QQQ), (DOCU), (META), (AMZN)

CLICK HERE to download today's position sheet.

Note: We are moving webinar platforms to Zoom for the February 8, 12:00 EST Mad Hedge Biweekly Strategy

Webinar. To join, please click here.

Well, that was some week!

The next time there is a Fed interest rate announcement, earnings from all the big tech companies, and a Nonfarm Payroll Report all within five days, I am going to call in sick, volunteer at the Oakland Food Bank, or explore some remote Pacific island!

For good measure, a top-secret Chinese spy balloon passed overhead before it was shot down, which I was able to read all about in USA Today.

Still, when you live life in the front trenches and on the cutting edge and use the kind of leverage that I do, you are going to take hits. It’s all a cost of doing business. If you can’t stand the heat, get out of the kitchen.

The last month in the markets have seen one of the greatest whipsaws of all time. Many leading stocks are up 40%-100%, while the Volatility Index ($VIX) plunged to a two-year low. Stocks have gone from zero bid to zero offered. The bulls are back in charge, for now.

Go figure.

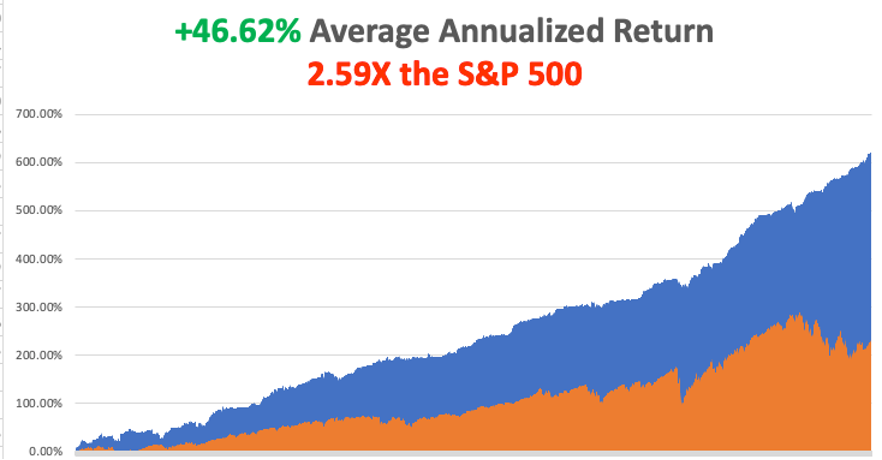

This year has proved full of flocks of black swans so far, with February setting me back -5.70%. My 2023 year-to-date performance is still at the top at +16.65%. The S&P 500 (SPY) is up +9.92% so far in 2023. My trailing one-year return maintains a sky-high +84.10%.

That brings my 15-year total return to +613.84%, some 2.59 times the S&P 500 (SPX) over the same period. My average annualized return has retreated to +46.62%, still the highest in the industry.

Last week, I got stopped out of my short position in the (QQQ), in what will hopefully be my biggest loss of the year, but not the last. Once or twice a year, you get a major gap opening that takes you through one, and sometimes two full strike prices, taking you to the cleaners, and this was one of those times. It takes three more winning trades to make up for these.

I also took small profits on my remaining long in Apple (AAPL). That leaves me 80% in cash, with a double short in Tesla (TSLA). Markets are wildly overextended here with my own Mad Hedge Market Timing Index well into “SELL” territory at 76. Tread at your own peril. Cash is king right here.

Growth stocks are on fire and small caps have been prospering, all classic bull market indicators. This has triggered panic short covering by hedge funds which have seen their worst start to a New Year in decades. The old pros are getting carried out on stretchers.

Maybe this is a good time to hire some kid to do your trading, like one who has never seen markets go down before, one who started his career only on January 1? Or maybe one who retired on December 31 2021, and took a year off?

So, what are markets trying to tell us? That in an hour, the view of the economy has flipped from a mild recession to a soft landing? That interest rates don’t matter anymore? That big chunks of the economy can operate without outside money? That big tech will always make money, it will just rotate from large profits to small ones and back to outrageous ones again?

Those who instead bet on a severe recession are currently filling out their applications as Uber drivers. Warning: it’s harder than it used to be, no more fake IDs or salvage title cars. Next, they’ll want your DNA sample.

If it is any consolation, Fed governor Jay Powell hasn’t a clue about what’s happening either, and that’s with 100 PhD's in economics on his staff. He was just as flummoxed as we over a January Nonfarm Payroll Report that came in 2.5 X expectations on top of 4.5% in interest rate hikes.

Clearly, a new economy has emerged from the wreckage of the pandemic, and no one, not anyone, has quite figured out what it is yet.

Some ten years’ worth of economic evolution has been pulled forward. Everything is digitizing at an astonishing rate. What do I do after slaving away in front of a computer all day? Go back to my computer to have fun. Lots of “zeros” and “ones” there.

It looks like we get a new stock market too.

All of this frenetic market action does fit one theory that I spelled out for you in great detail last week. It is that technology stocks are about to spin off such immense profits that it is about to replace the Fed as a new immense supply of free money.

META up 20% in a day? That’s what it says to me. Notice that Mark Zuckerberg mentioned “AI” 16 times in his earnings call.

Is it possible that I nailed this one….again?

On another related topic, the last three months have just given us a wonderful illustration of how well the Mad Hedge Market Timing Index works (see chart below). We got a strong BUY at an Index reading of 30 on December 22, when the (SPY) began a robust 12% move up. We are now at the top end of an upward trend with my Index at 76. You’d be Mad to add a long position here, at least for the short term.

Someone asked me the other day if the algorithm has gotten smarter in the seven years I have been using it. The answer is absolutely “yes,” and you can see it in my performance. During this time, my average annualized return has jumped from 31% to 46%. That’s because the algorithm gets smarter with the hundreds of new data points that are added every day. Believe it or not, this is how much of the economy is run now.

But there is another factor. I get smarter every year. Believe it or not, when you go from year 54 to 55, you actually learn quite a lot about the markets. Of course, markets are evolving all the time and the rate of change is accelerating. When I saw the market moving towards algorithms, I wrote an algorithm. The challenge is to solve each new problem the market throws at you every year, which I love doing.

Nonfarm Payroll Report at 513,000 Blows Away Estimates, more than double expectations. The Headline Unemployment Rate fell to a new 53-year low at 3.4%. Leisure & Hospitality gained an incredible 128,000, Professional & Business Services 82,000, and Government 74,000. You can kiss that interest rate cut goodbye. Bonds believe it, down 3 points, but stocks are still in Lalaland, reversing a 300-point reversal in the (QQQ)s.

Fed Raises Rates 25 basis points, but Powell talks hawkish, smashing stocks for an hour. He needs more evidence that inflation is finally headed down. He might as well have said he’ll burn the place down. One or two more rate rises to go before the pivot.

Weekly Jobless Claims Hit New 9 Month Low, at 183,000, down 3,000, and is close to a multi-generational low. A recession is rapidly moving off the table as today’s move in tech stocks indicates.

JOLTS Surges Past 11 Million Job Openings in December to a five-month high. The Fed’s assault on labor clearly isn’t working. The million who died from Covid certainly aren’t coming back to work, nor are the 500,000 long Covid cases. That’s 1% of the US workforce.

Ukraine War is Accelerating Move to Green Energy, or so thinks British Petroleum, cutting its ten-year energy demand forecast. Russian energy has proven unreliable at best, and the key pipelines have been blown up anyway. Massive subsidies have been unleashed in Europe and the US for solar, wind, EVs, hydro, and even nuclear. The war gave coal a respite from oblivion, but only a temporary one.

S&P Case Shiller Drops to an 8.6% Annual Gain, the National Home Price Index falling for five consecutive months. No green shoots here. The deeply lagging indicator may not turn positive until yearend. Miami, Tampa, and Atlanta showed the biggest gains, with San Francisco the biggest loser.

Office Occupancy Recovers to 50%, according to a private research firm. New York, San Jose, and San Francisco are still lagging. With the work-from-home trend and high interest rates, commercial properties have entered a perfect storm. Austin, TX was the highest at 68%.

Europe Delivers Surprising Q4 Growth, despite WWIII playing out on its doorstep. GDP increased by 0.1% when a decline was expected. European stocks should outperform American ones in 2023.

IMF Upgrades Global Growth Forecast for 2023 to 2.9% and sees a modest recovery in 2024. The figures are an improvement from the last report, thanks to falling inflation and energy prices. China ending lockdowns is another plus.

General Motors to Invest $650 Million in Lithium Americas, pouring money into a Nevada mine at Thacker Pass, the largest such US investment so far. (GM) says it will raise EV production to 400,000 this year versus 120,000 for all of 2022. Good luck because local environmental opposition to the new mine has been enormous. Goodbye China.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, February 6, no data of note is announced.

On Tuesday, February 7 January 31 at 5:30 AM EST, the Balance of Trade is out.

On Wednesday, February 8 at 7:30 AM, the Crude Oil Stocks are published.

On Thursday, February 9 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, February 10 at 8:30 AM, the University of Michigan Consumer Sentiment is printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, the telephone call went out amongst the family with lightning speed, and this was back in 1962 when long-distance calls cost a fortune. President Dwight D. Eisenhower was going to visit my grandfather’s cactus garden in Indio the next day, said to be the largest in the country, and family members were invited.

I spent much of my childhood in the 1950s and 1960s helping grandpa look for rare cactus in California’s lower Colorado Desert, where General Patton trained before invading Africa. That involved a lot of digging out a GM pickup truck from deep sand in the remorseless heat. SUVs hadn’t been invented yet, and a Willys Jeep (click here) was the only four-wheel drive then available in the US.

I have met nine of the last 13 presidents, but Eisenhower was my favorite. He certainly made an impression on me as a ten-year-old boy, who I remember as a kindly old man.

I walked with Eisenhower and my grandfather plant by plant, me giving him the Latin name for its genus and species, and citing unique characteristics and uses by the Indians. The former president showed great interest and in two hours we covered the entire garden. I still make my kids learn the Latin names of plants.

Eisenhower lived on a remote farm at the famous Gettysburg, PA battlefield given to him by a grateful nation. But the winters there were harsh so he often visited the Palm Springs mansion of TV Guide publisher Walter Annenberg, a major campaign donor.

Eisenhower was one of the kind of brilliant men that America always comes up with when it needs them the most. He learned the ropes serving as Douglas MacArthur’s Chief of Staff during the 1930s. Franklin Roosevelt picked him out of 100 possible generals to head the allied invasion of Europe, even though he had no combat experience.

After the war, both the Democratic and Republican parties recruited him as a candidate for the 1952 election. The latter prevailed, and “Ike” served two terms, defeating the governor of Illinois Adlai Stevenson twice. During his time, he ended the Korean War, started the battle over civil rights at Little Rock, began the Interstate Highway System, and admitted Hawaii as the 50th state.

As my dad was very senior in the Republican Party in Southern California during the 1950s, I got to meet many of the bigwigs of the day. New York prosecutor Thomas Dewy ran for president twice, against Roosevelt and Truman, and was a cold fish and aloof. Barry Goldwater was friends with everyone and a decorated bomber pilot during the war.

Richard Nixon would do anything to get ahead, and it was said that even his friends despised him. He let the Vietnam War drag out five years too long when it was clear we were leaving. Some 21 guys I went to high school with died in Vietnam during this time. I missed Kennedy and Johnson. Wrong party and they died too soon. Ford was a decent man and I even went to church with him once, but the Nixon pardon ended his political future.

Peanut farmer Carter was characterized as an idealistic wimp. But the last time I checked, the Navy didn’t hire wimps as nuclear submarine commanders. He did offer to appoint me Deputy Assistant Secretary of the Treasury for International Affairs, but I turned him down because I thought the $15,000 salary was too low. There were not a lot of Japanese-speaking experts on the Japanese steel industry around in those days. Biggest mistake I ever made.

Ronald Reagan’s economic policies drove me nuts and led to today’s giant deficits, which was a big deal if you worked for The Economist. But he always had a clever dirty joke at hand which he delivered to great effect….always off camera. The tough guy Reagan you saw on TV was all acting. His big accomplishment was to not drop the ball when it was handed to him to end the Cold War.

I saw quite a lot of George Bush, Sr. who I met with my Medal of Honor Uncle Mitch Paige at WWII anniversaries, who was a gentleman and fellow pilot. Clinton was definitely a “good old boy” from Arkansas, a glad-hander, and an incredible campaigner, but was also a Rhodes Scholar. His networking skills were incredible. George Bush, Jr. I missed as he never came to California. And 22 years later we are still fighting in the Middle East.

Obama was a very smart man and his wife Michelle even smarter. Stocks went up 400% on his watch and Mad Hedge Fund Trader prospered mightily. But I thought a black president of the United States was 50 years early. How wrong was I. Trump I already knew too much about from when I was a New York banker.

As for Biden, I have no opinion. I never met the man. He lives on the other side of the country. When I covered the Senate for The Economist, he was a junior member.

Still, it’s pretty amazing that I met 9 out of the last 13 presidents. That’s 20% of all the presidents since George Washington. I bet only a handful of people have done that and the rest all live in Washington DC. And I’m a nobody, just an ordinary guy. It just makes you think about the possibilities.

Really.

It’s Been a Long Road