'Fund consultants like to require style boxes such as 'long-short', 'macro', or 'international equities.' At Berkshire, our only style box is 'smart', said 'Oracle of Omaha', Warren Buffet, CEO and the largest shareholder in Berkshire Hathaway.

'Fund consultants like to require style boxes such as 'long-short', 'macro', or 'international equities.' At Berkshire, our only style box is 'smart', said 'Oracle of Omaha', Warren Buffet, CEO and the largest shareholder in Berkshire Hathaway.

Featured Trades: (WELCOME TO WWIII)

1) Welcome to World War III. If there was ever a war that had to happen it is our new military engagement against Libya. Khadafy had made enemies with so many governments as the enfant terrible of the Middle East that putting together a coalition to depose him was a piece of cake. No arm twisting or fake intelligence about weapons of mass destructions needed here. Even Al Qaida hated Khadafi.

Call it 'shock and awe' light. I love it. The leadership is Arab, the French provide close air support, Egyptians the ground troops, and the Italians the pasta and the Tuscan wine (praise the Lord and pass the Antinori?). We just sit back out of harm's way and use up our inventory of outdated tomahawk missiles, while testing out the new models. Think of it as no more than a training exercise for the US. And we do all of this under the mantle of a UN approval. For us it really is a push button war. It is more like a video game that hand to hand combat.

You knew that things were going to play out differently this time when the Arab League voted to support the Libyan rebels and asked for UN assistance. For the past 60 years, this impotent international organization has done nothing but issue periodic rants against Israel and Zionism. This is the first time they have ever done anything useful.

Look at the line up in the coalition, and every national leader found it expedient from a domestic political point of view to take on Libya. The UK, France, Italy, Saudi Arabia, the UAE, Egypt, Jordan, and the US. Everyone needs a weak enemy they can defeat and claim credit for. Keep in mind that Libya's only ally in this fight is Zimbabwe, and it is providing only moral support.

Even President Obama, whose strong words and decisive action will no doubt boost his chances in the 2012 election. All of a sudden, protecting the Libyan people has become a top national priority. Who knew? Did I hear the word 'oil'? The word in Israeli intelligence is that the move was made not to save lives, but oil production facilities. After all, if you want to know what's happening in Libya, you have to call Tel Aviv.

It is also important to note that yet another country has discovered that the weapons and the decades of training they paid the Russians hundreds of billions of dollars for are utterly useless. Targeting coordinates were programmed into cruise missiles while enemy bases were still under construction. The CIA has kept a satellite parked overhead for daily updates. All that was missing was the political will to pull the trigger. Khadafy's supports can do little but fire their AK-47's in the air in utter frustration.

Does Anyone Here Know How to Drive a Manual?

-

If you gave the Joint Chiefs of Staff a map of the Middle East and asked them their favorite target, Libya would be at the top of the list, and Iraq and Afghanistan would be at the bottom. While Libya looks big on a map, it is really a thin strip of coast 20 miles deep and 1,000 miles long. Its military resources are concentrated if confined, easily targeted areas. Its army consists of only 10,000, many mercenaries earning $1,000 a day. Who said there weren't well paid jobs around? The unemployed obviously aren't trying hard enough.

I predict that they will dig Khadafy out of some wretched hole in a few months, put him on trial for war crimes and terrorism, and the world will say good riddance. Sorry, but that's the Marine pilot in me coming out. That will leave the US with a pro-Western government in a major oil producing country whose massive offshore fields it was only just starting to develop.

Looking for a Good Lawyer

-

The market reaction to our third Middle Eastern war in two decades was totally predictable. Traders hate uncertainty and love fact. This brings falling asset prices during the sabre rattling stage and soaring ones when the first shots are fired. If you don't believe me look at the charts for stock market indices at the onset of the 1991 and 2002 Gulf wars.

How Do You Spell 'Foreign Aid'?

-

It's off to the races for oil again, as Libyan crude is now probably off the market for years to come. Macro Millionaire followers are thanking their lucky stars that, having sold oil at $107, they covered at $97. Here we are again at $106 for West Texas intermediate and $116 for Brent. It's been that kind of year.

Semper Fi.

Featured Trades: (MY HOLLYWOOD ROLE)

1) Hollywood Cashes in on Wall Street's Woes. I have done many things in my life: hedge fund manager, pilot, cowboy, journalist, stock broker, mountain climber, translator, guide, etc, etc. etc. Now add technical consultant to Hollywood to the list. According to the New York Times, Simon Baker, star of the TV show 'The Mentalist', is using the Diary of a Mad Hedge Fund Trader as a resource to humanize Wall Street traders in the upcoming film entitled 'Margin Call' (click here for the link).

This is not an easy task, as the public generally considerers denizens of the pit as greedy, soulless, money grubbing monsters, difficult to empathize with in any setting. The star studded thriller includes Kevin Spacey, Demi Moore, and Jeremy Irons, and will focus on a 24 hour period during the height of the financial crisis at a fictional Wall Street bank.

No doubt, the producers are hoping to cash in on the imminent release of Oliver Stone's sequel to the classic film, Wall Street. As with the last film, the great industry guessing game will be identifying who and which institutions in real life are being portrayed. How much do you want to bet that the troubled bank starts with the letter 'L'.

Watch for film crews framing those dark, foreboding shots in the canyons of downtown Manhattan this summer. Release is expected next year. This, I must see. Hey Kevin, baby, have your people call my people and let's do lunch!

A New Role Model?

Featured Trades: (TESLA MOTORS), (TSLA)

2) Tesla: Sell the Sizzle, Then Buy the Steak. So far, the most successful thing Tesla Motors (TSLA) has done is sell stock. The IPO was an absolute blowout success, far and away the best this year, with book building at $14-$16, the size increased by 20%, pricing at $17, and then trading up to $32 on the third day, giving it an impressive market capitalization of $3.3 billion. It fell back to $16 the following week, but then mad a run to $26. Now, here we sit again at $23.

It pulled this off with virtually the entire auto industry and its pet analysts pissing all over the deal from the greatest height possible, as the entire concept of a Silicon Valley based car industry is the greatest affront possible to the Detroit establishment.

I love this company, and I think Elon Musk is incredibly brave. Hell, if I had a billion dollars to throw away, I would probably do the same thing. But much about the new issue reminds me of the Apple IPO some 30 years ago, when it ran up to $21 before its nosedive to $4 (click here for the story). The ill-fated DeLorean Motor Company also comes to mind. All the focus was on the products, which consumers loved, not the business model or the bottom line.

By its own admission, (TSLA) will not make any money for two years or longer, and won't even commit to hard production dates for its crucial S-1 model. I think the way to play this stock is to skip all the hype associated with the stock floatation, as most of the buyers aren't looking for a profitable investment, but bragging rights at the country club.

Just wait for the next meltdown in the stock market to call out the weak holders. The time to buy will be in the PR ramp up to S-1 mass production, which will be just as intensive as the IPO.

There is also a political risk associated with the stock. If the Republicans retake the presidency in 2012 they may trash all alternative energy subsidies as unaffordable luxuries, which Tesla is hugely dependent on for making its S-1's $50,000 price competitive. Always be careful when making investments totally dependent on government subsidies for profitability. Here today, gone tomorrow. If that happens, the Tesla will be joining the Tucker, the DeLorean, and the Pontiac in the dustbin of history.

Oh, and Elon, a little fatherly advice. Don't tell a divorce court that you're broke a week before the market values your holdings in TSLA at $2 billion. You're supposed to impress your new shareholders with the depth of your judgment. Not good, not good.

-

Featured Trades: (RHODIUM), (AAUKY.PK), (PAL), (SWC)

3) Pssst! Have You Heard About'..? When I was at the New York Hard Asset Investment Conference, every hour someone would stop by my table, mention the word 'rhodium', and walk away. My interest piqued, I decided to look into this mysterious metal.

Rhodium (Rh) is in fact the rarest precious metal in the world, and is also the most valuable. The white metal is used primarily as a catalytic convertor by the auto industry as a much more efficient alternative to platinum and palladium (click here for my outrageously profitable calls on platinum and click here for palladium). It is also used in jewelry, the plating of mirrors, and in neutron flux monitors in nuclear power reactors.

South Africa produces 80% of the world's meager 25 metric tonne annual supply, and therein lies the angle. Rolling power shortages in the country has lead to the same intermittent mining stoppages that have affected the other metals.

On the demand side, you can count on a US auto industry that is boosting production from 9.5 million units last year to 15 million units over the next five years to maintain a firm bid. So far, then are running at a 12.5 million annualized rates this year. As a result, rhodium has nearly tripled in the past year to $2,460/ounce, but is still well shy of its $10,000 record high.

Rhodium is not exactly easy to buy. There are no futures contracts, and most of the physical production is tied up in long term contracts. Since the metal is so unbelievably hard, it is difficult to work with, and only one company, the Cohen Mint, is offering .999 fine coins and bars (click here for their website).? But expect to pay a hefty spread over spot, up to 20%, that is standard for a single source supplier.

A more liquid option can be found through buying the shares of the largest rhodium miners, which often appears alongside platinum, like Anglo American (AAUKY.PK), North American Palladium (PAL), or Stillwater Mining (SWC). Granted, prices here are vastly overheated, as they are for so many commodities. But it is something to keep on your list when we get a substantial sell of in 2011.

And don't tell anyone I told you.

-

Featured Trades: (LAS VEGAS CITY CENTER)

4) A Poolside Report from City Center. I write this to you from my poolside cabana at the Aria at City Center, the newest and hottest hotel in Las Vegas, against a background of blaring rock music and helicopters buzzing overhead every five minutes. It's amazing what passes for a swim suit these days, and some of the tattoos I saw were nothing less than shocking.

I'm here because at a throw away rate of $120/night for a room that is worth at least $500, and discount fares offered by the airlines, it is cheaper to spend a weekend in Sin City than it is to stay home. Hotel flacks glibly tell reporters that with an 80% occupancy rate, they are near profitability. But staff tell me those numbers are achieved only because 20% of those rooms have been mothballed and taken off the market.

The glitzy, ultra-modern, Cesar Pelli designed, 16.8 million square foot, 63 acre complex occupies a quarter mile on the city's fabled Strip between the Bellagio and the Monte Carlo Hotels, and will unquestionably become one of the hedonist Wonders of the World. It includes the Mandarin Oriental, Aria, Veer, Vdara, and Harmon Hotels, offering 4,000 rooms and 2,600 condos. They will be adorned by two casinos, a convention center, a new theater for an Elvis themed Cirque du Soleil show, and parking for 6,900.

I wandered in amazement though the gargantuan 'Crystal' shopping mall, where half of the retail space was boarded up in the most tasteful way possible, and marquee luxury names like Fendi, Ermenegildo Zegna, Tiffany, and Louis Vuitton were manned by elegantly dressed and earnest staff, but bereft of a single customer. Despite hiring 12,000 since opening in December, service at the Aria is still glacially slow. My inside guy in Vegas, a blackjack dealer at Caesar's, tells me this is because it is an all-union house. The city is also rife with rumors that the oddly titling Harmon will have to be torn down and rebuilt due to construction flaws.

I spent my free time looking at condos that were initially offered at $600,000, but now could be had for $200,000. To see them, I had to drive through 'ghost suburbs', blighted with dusty, abandoned strip malls and tumbleweed blown office parks that might have been a scene out of a Twilight Zone episode.

Still, how can you hate Vegas? The French toast at hotel Paris, France was to die for, and my masseuse at the Aria, Monique, is clearly God's gift to mankind.

You really have to wonder what MGM-Mirage's Kirk Kerkorian, Dubai World, and their long suffering lenders were thinking when they ponied up $8.5 billion for this venture. Excess is in abundant over supply here, and they clearly thought the good times would go on forever. Instead, they created the worst commercial real estate disasters in human history.

Thanks for the great weekend, Kirk!

-

Featured Trades: (STOPPED OUT ON MY YEN SHORT), (FXY), (YCS)

2) Stopped Out of My Yen Short. My standing stop loss order to cover my short in the Japanese yen got triggered right as it dipped under ?80, a new all-time high. The massive flight to cover huge yen carry trades is the cause, as the world rushes to cover short positions in the yen and sell everything else. These positions have been building up for 20 years, ever since interest rates for the yen fell below those for the rest of the world.

If you are going to lose money, this is the way to do it. Of the 21 positions taken on by the Macro Millionaire program since inception, this has been the smallest one. As it fell, I never doubled up, fully aware of the potential of the Japanese yen to make this kind of spike move against us in the wake of the Great Sendai Earthquake.

The government tried valiantly to stem the appreciation with massive intervention in the currency markets, buying some $186 billion on Monday alone. But it was to no avail. I can imagine that the guy in charge of yen intervention is sitting outside the prime minister's office stewing, while the leadership tries to figure out how to extinguish the nuclear fires. The country is truly not functioning now.

If anything, the yen at ?76, the high so far, will cause more damage to Japan's economy that the earthquake did, making the argument for a weak Japanese currency even stronger. But as the great economist, John Maynard Keynes, said so eloquently, 'the markets will remain irrational longer than you can remain liquid'.? But at this stage, I would rather watch from the sidelines than ride this bucking bronco until those in charge make the right decision.

So it is better to stop out and live to fight another day. Let's just hope the next battle isn't a Waterloo.

-

-

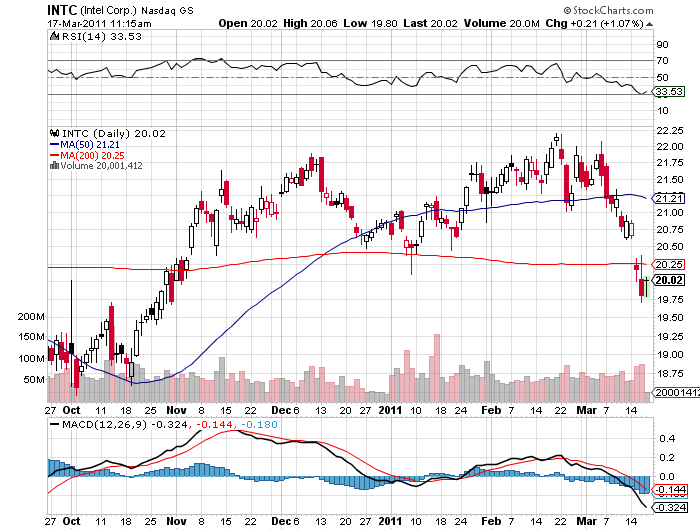

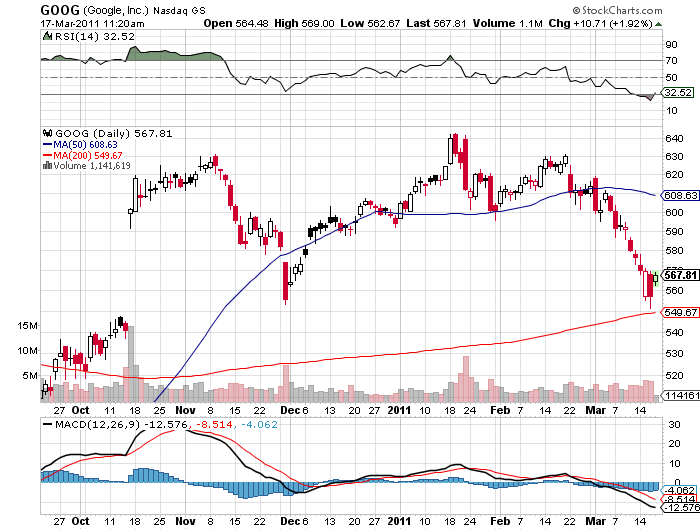

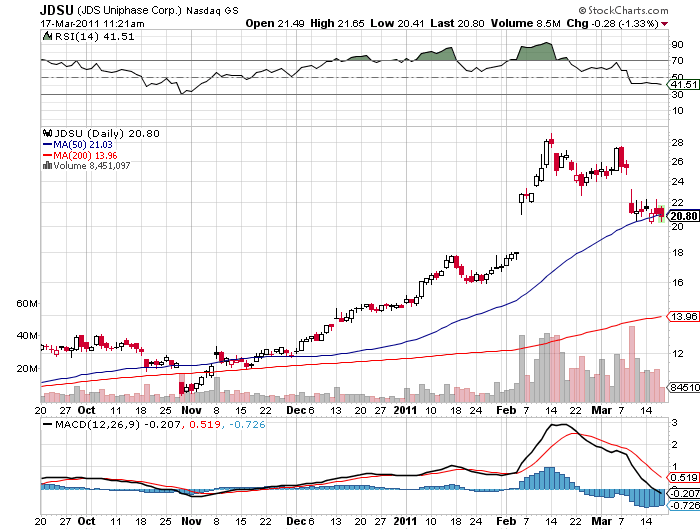

Featured Trades: (MY SHOPPING LIST OF TECHNOLOGY STOCKS), (AAPL), (CSCO), (HPQ), (ORCL), (GOOG), (INTC), (JDSU), (QQQ), (ROM), (XLK)

3) My Shopping List of Technology Stocks. Hedge fund managers are smacking their lips, maneuvering to take advantage of the recent sharp sell off by technology stocks. They are building shopping lists of where to pounce

at the first sign of another upside breakout, much like a famished tiger might behave. Some of the highest quality names have had the biggest falls, some more than 20%, and they are now flaunting dividend yields greater than the 3.2% found on 10 year Treasury bonds.

Here are the names that I am hearing is on the list:

Apple (AAPL)

Cisco (CSCO)

Hewlett Packard (HPQ)

Oracle (ORCL)

Google (GOOG)

Intel (INTC)

JDSU Uniphase (JDSU)

Look at Intel (INTC), which at $20 is selling at a paltry 11 times earnings and a 3.5% dividend yield, and generates the bulk of its sales in the highest growth sectors of the global economy. After the dotcom bust of 2000, these bad boys spent nearly a decade in the penalty box, shunned by the investing world as the poster boys for wild excess. Think Robert Downey, Jr. on steroids. During this time, cash balances doubled, free cash flows soared, outstanding shares shrank, and multiples fell to a tenth of their bubblicious peaks.

I started recommending this group at the absolute bottom of the market in March, 2009 (click here for the call), and it was no surprise to me when they outperformed almost every sector on the upside. With 60%-80% of their earnings coming from abroad, primarily Asia, I saw them really as foreign stocks wearing cowboy hats, pearl snap buttoned shirts, and Ray Ban aviator sunglasses. They did not need banks, as they are almost entirely self-financed, immunizing them from the credit crunch.

They avoided many of the management errors that torpedoed so many other US firms, like derivatives books, leveraged real estate exposure, and LBO debt, and outright stealing. While their American customers were getting poorer, their two billion overseas customers were getting much richer.

The industry represents the last, best hope that America has for competing globally, as it is our only means of staying on top of the international value added chain. It seems that in addition to bulk commodities like corn, wheat, soybeans, coal, timber, aircraft, weapons, movies, and porn, tech companies are among the few that make things foreigners actually want to buy from us.

The lessons of the bubble made them ultra-conservative in their capital spending, which will lead to product shortages and much higher prices in any recovery. There are short squeezes developing for a whole range of tech components. Memory, for example, has seen no capex at all for three years. They are surfing the wave of innovation, and will cash in big time from the mobile computing revolution, cloud computing, and the virtualization of data centers.

During the last tech bubble, the industry did not have the global market that it does today. Now, demand from the rising emerging market middle class is kicking in, as it is for commodities. The two year tech rally we saw from the 2009 lows could just be the down payment of a decade long bull market in these stocks, which will then end with another bubble down the road. When John Chambers, a first class manager, discusses Cisco's (CSCO) long term outlook, he is so effusive, he sounds like he is on ecstasy.

If you don't want to make any bets on single names, you can look at the Technology Select Sector SPDR (XLK), the PowerShares QQQ (QQQQ), or the leveraged ProShares Ultra Technology (ROM). I'll shoot out a trade alert FOR 'Macro Millionaire' readers when I pull the trigger.

'The seller has an upper hand, as a girl might if she were the only female at a party attended by many boys. That lopsided situation would be great for the girl, but terrible fort the boys,' ' said 'Oracle of Omaha', Warren Buffet, CEO and the largest shareholder in Berkshire Hathaway.

Featured Trades: (QE2 JUST ENDED EARLY), (DIG), (JJG), (AAPL)

1) QE2 Just Ended Early. Many observers believe that the massive sell off that we have seen in global equity markets are purely the result of the Great Sendai Earthquake. Fat chance. I think the earthquake is masking the true causes of the liquidation, the end of Ben Bernanke's quantitative easing.

When the market would start discounting the demise of this free lunch for all asset classes and the hedge funds that trade them has been one of the great guessing games this year in the financial markets. Up until last week it was thought that the weakness since February was just another dip to buy into the great liquidity bubble. But no more.

You can see this in the violence and the severity of the sectors that have sold off the most. The ones that flaunted the biggest gains since QE2 started in August are now suffering the worst of the damage. Look no further that my favorite sectors, which were all heavily owned by hedge funds, and now being mercilessly dumped.

In a mere two weeks, my energy play (DIG) plunged 16%, the grain ETF (JJG) is off 17%, while technology bellwether Apple (AAPL) has taken a 7% hickey. The double top in the Apple chart is particularly ominous. And look at Cisco Systems (CSCO) where we snagged a double on a call spread and exited post haste. My friend, Dr. Copper, seems to have taken and extended vacation, with its ETF (CU) off 20%. Ouch!

Regular readers of this letter know that I have been expecting this and have been judiciously scaling out of long since the end of January.

The implication is that this sell off may continue longer and go farther than many traders realize. What will be the next driver to take stock prices skyward? QE3? You must be smoking something. The political balance in Washington will permit no more support for the economy. Tax cuts? We have already gorged ourselves on these for the next two years.

Rising earnings? Coming off a great quarter, forecasts going forward are being ratcheted downward, thanks to the earthquake. I think people will be amazed when they discover how much US manufacturing is dependent on high value added, irreplaceable Japanese parts, from autos to electronics.

I don't think the abundant 'crash' gurus are going to get any satisfaction this year either. The news is bad, but it is not that bad. We are far more likely to die of ice than fire. Sounds like it may be a good time to sell out of the money calls on equities everywhere.

-

More Likely to Die from Ice That Fire

-

-

-

-

Watch Closely. He's About to do a Disappearing Act