Featured Trades:?? (AUGUST NONFARM PAYROLL)

3) The Bad News In the August Non Farm Payroll. One of my favorite math professors always used to tell me that statistics were like bikini bathing suits. What they reveal is fascinating, but what they conceal is essential.

If there were ever a chart that showed how the pulse of the economy was flat lining, this is it. The scary thing is not the past, but the prologue. The expectations bar was so low, that anything short of Armageddon had to deliver a stock market rally, which is promptly gave back on Tuesday. Apparently, this is how long it takes for traders to figure out a loss of 54,000 jobs is actually a 'real' loss of 154,000 jobs when population growth is taken into consideration. And we know that these figures omit the millions subject to mandatory furloughs, pay, and benefit cuts. It is back to school season again, and for many municipalities that means it's time to fire more teachers, cops, and firemen.

The 200,000 monthly job gains normally seen at this stage of the economic cycle will not arrive for years, if ever. Over employment in these fields is still legion when compared to the corporate world. While the 67,000 new private sector jobs are laudable, it is not the sort of growth that bull markets are built upon. At this rate, it will take 120 years just to bring the unemployment rate down to 5%. No matter how much money the government throws at the economy, those 25 million mostly blue collar jobs that we shipped to China from 2000-2008 are never coming back. The only question is how many more jobs the Middle Kingdom relieves us of as they relentlessly work their way up the value chain.

The new management in America is all about staying thin and agile, and that involves only hiring a new worker at the point of a gun, lest one become saddled with all of the secondary costs and entitlements that entails. Expect more of the same in coming months, and if you have a job, keep it all costs.

What Statistics Conceal is Essential

4) Thanks for the Testimonials. My request for testimonials about the merits of The Diary of a Mad Hedge Fund Trader overwhelmed me with more than 100 responses. Flattering and humbling at the same time, it is a vindication of all the blood, sweat, and tears that I pour into this letter each day. I will be running some of the best at the bottom of the letter every few days. Thanks, all of you!

'I have been a retail stockbroker for 29 years and I spend a great amount of time reading and "net" surfing for info, ideas, and insights otherwise my clients will receive the same dull, uninspired, and mostly unprofitable opportunities that are primarily designed to generate fees for the large financial institutions that now own virtually everything, including the brokerage firm I worked at for 26 years.'

'I have been checking your site since about January. For several years, before 2008, I have been trying to inspire my clients to look outside the buy and hold stocks/mutual fund strategies of the prior 20 years and to look at other markets, geographically and in an asset class sense. Otherwise I am afraid that their investment returns for the next 10 years will be no better than the last 10 if not worse.'

'I believe I have done a decent job of protecting their assets, but as you know that ain't going to cut it going forward. At some point you need returns, and I truly believe we need a broader scope to achieve that, and that is where you come in.'

'You obviously have a broad view as well as depth, and are not content to write about "another list of high quality dividend paying stocks." Your circle of contacts in business and government, not to mention the industry, is quite impressive and obviously evolved over a number of years. Love your sense of humor.? My view is that only those who really understand their craft can see the humor and irony. And yes it is true that even one idea will more than pay for your subscription cost. '

Thanks again for your unique work.

AJ in Louisiana

Featured Trades: (SOVEREIGN DEBT), (PCY), (LQD)

2) Sovereign Debt Was a Great Place to Hide.? I am constantly asked where to find safe places to park cash by investors understandably unhappy with the risk/reward currently offered by the markets. Any reach for yield now carries substantial principal risk, the kind we saw, oh say, in the summer of 2007.

I have had great luck steering people into the Invesco PowerShares Emerging Market Sovereign Debt ETF (PCY) for the last year, which is invested primarily in the debt of Asian and Latin American government entities, and sported a generous 8.5% % yield (click here for my initial call at XXX). . This beats the daylights out of the one basis point you could earn for cash, the 3.70% yield then available on 10 year Treasuries, and still exceeded the 5.70% yield on the iShares Investment Grade Bond ETN (LQD), which buys predominantly single 'BBB', or better, US corporates.

The big difference here is that PCY has a much rosier future of credit upgrades to look forward to than other alternatives. It turns out that many emerging markets have little or no debt, because until recently, investors thought their credit quality was too poor. No doubt a history of defaults in the region going back to 1820 is in? the backs of their minds.

You would think that a sovereign debt fund would be the last place to safely park your money in the middle of a debt crisis, but you'd be wrong. PCY has minimal holdings in the Land of Sophocles and Plato, and very little in the other European PIIGS. In fact, the crisis has accelerated the differentiation of credit qualities, separating the wheat from the chaff, and sending bonds issues by financially responsible countries to decent premiums, while punishing the bad boys with huge discounts. It seems this fund has a decent set of managers at the helm.

With US government bond issuance going through the roof, the shoe is now on the other foot. Even my cleaning lady, Cecelia, knows that US Treasury issuance is rocketing to unsustainable levels (she reads my letter to practice her English). Moody's has been rattling its saber about a downgrade of US debt on an almost daily basis, and it is just a matter of time before this once unimaginable event transpires. When it does, there could be a stampede into the debt of other healthier countries, potentially sending the price of PCY through the roof.

Since my initial recommendation, my total return on PCY has been 30%, not bad for an insurance policy. Money has poured into PCY, doubling it to a record $707 million in assets. The yield is down to 6.11%. If we get a sudden sell off in Treasury bonds, a scenario that may have already started, I think it will take the rest of the fixed income universe along with it. I therefore want to take the money and run.

I lived through the Latin American debt crisis of the seventies. You know, the one that almost took Citibank down? Never in my wildest, Jack Daniels fueled dreams did I think that I'd see the day when Brazilian debt ratings might surpass American ones. Who knew I'd be trading in Marilyn Monroe for Carmen Miranda? Given the advanced age of this bond bubble, I'm now thinking of swearing off women altogether.

Time to Swear Off Women Altogether?

Featured Trades: (NATURAL GAS), (UNG), (CHK), (DVN), (XTO)

1) Is the UNG Going Under? The poster boy for everything that can go wrong with an ETF is undoubtedly the United States Natural Gas Fund (UNG). If you had studiously done all of your homework a year ago, and concluded that natural gas was severely oversold and about to go up 40%, you would have been dead right. If you then went out and bought the UNG you would have then lost 40%. You would think at first glance that this is a chart for an inverse gas ETF that would only profit from falling gas prices. However, such an instrument doesn't exist.

This dreadful state of affairs was brought about by the intricacies of contango, where far month contracts in the futures markets are trading at premiums to the front month. As each month expired, the managers of UNG bought fantastically rich forward contracts, and then rode them all the way down to spot, as they were mandated to do by their prospectus. They then repeated this exercise every month.

If the contango continues indefinitely, the UNG will eventually approach zero. Moral of the story: don't just punch in a symbol and hit enter. Read the damn prospectus first.

Since we are discussing CH4, I have to tell you that the outlook does not look great. We are just coming out of one of the hottest summers in history, and NG only managed a rally from the $4.30/MCF low to $5.00 . Gas in storage is about to rise again, and gas producers, like Chesapeake Energy (CHK), XTO Energy (XTO),? and Devon Energy (DVN), are racing to out-produce each other in the hope of offsetting falling prices with increased volumes. The price collapse is prompting a Darwinian consolidation of the entire industry. The spot price for NG has already suffered a free fall down to $3.70. It's sad to see such a great molecule fall on such hard times. Pitiful, really.

This is all happening thanks to the new miracle fracting technology, which has suddenly and unexpectedly been used to discover a 100 year supply of natural gas. The Marcellus shale in Pennsylvania, and other fields in Ohio, New York, and West Virginia could power the entire East Coast for decades. The Haynesville shale in Louisiana, Texas, and Arkansas could knock oil out of the box for power generation in the South. Huge fields in North Dakota are yet to be fully developed. All this makes the construction of a gas pipeline from Alaska pointless, once a pet project of former governor Sarah Palin.

It seems that now only need poke a straw in their backyard to obtain a lifetime supply of relatively clean burning energy. Gas majors are now jockeying to exploit untapped shale fields in Europe, with Poland and Germany leading the charge in deploying fracting technology. They must be sweating bullets in Qatar, which just invested $50 billion in facilities intended to export NG to the US and Europe. Looks like they'll have to flare it instead.

The problem is that ETF's have become a great money spinner for Wall Street, replacing earlier income generators, like CDO's, that died in the crash. By the beginning of this year, some 900 ETF's had been created worth $1trillion, generating massive management fees and trading commissions for the industry.

The big question is, when one of these marquee ETF's goes under, will it sour investors on the entire asset class? UNG has already cratered from $8.30 in July to $6.24 today, costing investors millions. Imagine how a leveraged ETF would have fared. Will this be the ETF that kills the goose that laid the golden egg?

Is Natural Gas Going to Burn Investors Once More?

Featured Trades: (TREASURY BONDS), (TBT), (TMV)

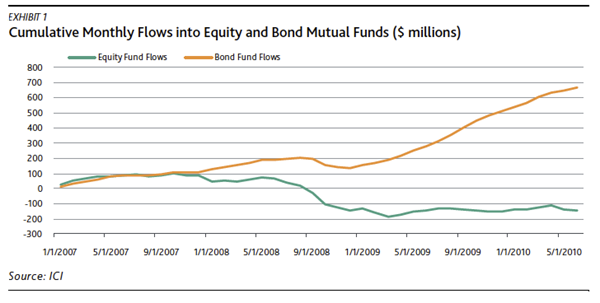

1) Have Treasury Bonds Had It? You are probably tired of my yammering on about how close we are to a multigenerational peak in Treasury bond prices by now.

If you missed my last three pieces on the topic, click here for 'The Great Bond Market Crash of 2010', click here for 'Don't Buy That Treasury Bond", and click here for 'Get Ready for the Sack of Rome'.

After yesterday's dramatic price action, which saw my preferred vehicle, the double leveraged (TBT) up 5% on the day, and the (TMV) tacking on a blistering 10%, you may be forgiven for thinking that the fat lady is getting ready to sing. Take a look at the chart below of the gargantuan cash flows into bonds, and you know that if this is not the top, it is not far off. Listening to the cheerleaders on CNBC applauding the pop in equities and the slide in bonds yesterday, you'd think it was a done deal.

Is the Fat Lady Singing in the Treasury Bond Market?

Featured Trades: (CHINESE SOLAR INDUSTRY), (STP), (YGE), (FSLR)

3) Darwinian Downsizing in the Solar Industry. The solar industry is suffering some 19th century Darwinian style competition, with Chinese manufacturers Suntech (STP) and Yingli Green Energy Holding (YGE) clearly dumping panels in the US and Europe below cost to gain market share.

You may laugh, but I watched the Japanese pursue the same strategy in the seventies and eighties with a vast array of products, from cars to memory chips, to devastating success. They now control half the US automobile market, and the most profitable half at that.

As a solar consumer I shouldn't care, as the 50% price drop has, with Obama's generous tax subsidies, made new installations cheaper than obtaining electricity from my local power company (PGE) at 12 cents a kilowatt. It's just a matter of booking the profit in China instead of Phoenix.

But the predatory pricing has also kicked my beloved First Solar (FSLR) in the shins. Use the weakness to pick up (FSLR) on the cheap. The company is using advanced cadmium telluride based thin film semiconductor technology, which has enabled it to match the Chinese price cuts dollar for dollar, and the engineering will allow them to continue to do so. The Chinese, wedded to an older polysilicon product, can't keep playing this game, unless they want to hemorrhage cash, or face US anti-dumping enforcement. To see more on the current fundamentals of solar, please click here.

Featured Trades: (DBA), (CORN), (PHO), (GLD), (SLV), (FXC), (FXA), (IDX), (TUR), (ECH), (EPOL), (TBT), (YCS)

1) Lee O'Dwyer of 5T Wealth Management.? My guest on Hedge Fund Radio this week is Lee O'Dwyer, a portfolio manager at 5T Wealth Management in the sunny climes of Napa, California. Lee is at the vanguard of a new wave of financial advisors sweeping the nation that is leading the way for individual investors during these difficult times, when everyone is seeking the 'new normal'. O'Dwyer is cherry picking for his clients the best money management techniques that have evolved over the last 30 years, and discarding the dross.

5T Wealth Management is offering sophisticated hedge fund management trading and risk control techniques, that until now, have only been available to the big boys, and making them available to the retail investor. Their goal is to achieve absolute returns at all times and strive for every trade to be profitable. Relative performance benchmarked to an arbitrary index, such as the S&P 500, has been consigned to the dustbin of history. We are all traders now, whether we realize it or not. Buy and hold is dead. Unlike your past broker, Lee does not expect you to pay him a big bonus and take him out to lunch because he lost only 10% when an index dropped 20%.

To avail yourself of O'Dwyer's considerable talents you need only open a custody account at a major house like Fidelity, Goldman Sachs, or Morgan Stanley. You then sign a third person limited power of attorney that enables 5T to execute trades on your behalf, but not withdraw any funds. As you can log into your account online at anytime, transparency is total and complete. The positions are there in all their glory for you to view and analyze at any time, for better or for worse. There are no black boxes, homemade account statements, or a 'need to know' basis. The arrangement gives many individual investors all the security they deserve in the wake of the ugliness thrown up by the unfortunate Madoff affair.

For all of this, Lee charges the 1% management fee and the 20% performance bonus that is standard in the hedge fund community. A 'high watermark' means that bonuses are only paid out on new net increases in asset values. This makes double dipping in a volatile market impossible. SEC rules limit 5T to accepting only accounts with a minimum size of $750,000 from investors with $1.5 million in liquid assets. The new financial reform act will stair step annual income requirements from $200,000 a year now, to $300,000 and $400,000 down the road.

Lee employs a global long/short macro strategy that scours the world for only the cream of investment opportunities. Long term, he likes commodities (CU), food (DBA), (CORN), water (PHO), other resource plays, and precious metals (GLD), (SLV). He is enamored with the currencies of the commodity producing countries like Canada (FXC) and Australia (FXA). He is very bullish on emerging markets, like the BRIC's, as well as other new entrants such as Indonesia (IDX), Turkey (TUR), Chile (ECH), and Poland (EPOL).

On the short side, he is adamant that the 30 year Treasury bond (TBT) is reaching the end of an epochal bubble. Lee also thinks that rapidly deteriorating fundamentals and a coming demographic nightmare demand that the Japanese yen (YCS) is headed for a generational fall. In the US O'Dwyer likes technology, energy, and commodity plays, but doesn't expect much from the main indexes for the coming decade.

Lee hales from England where he obtained a degrees from the University of Wales, focusing on international relations, economics, and accounting. He immigrated to the US in 1993 where he joined a major US hedge fund, learning every corner of the alternative investment business from the ground up. In 2007, he moved on to 5T Wealth Management, an SEC registered investment advisor based just outside San Francisco. During the 2008 financial crisis, Lee limited his maximum draw down to 15% when the S&P 500 crashed 58%. He quickly earned back losses during the rebound that followed, much to the delight of his investors.

As a result, 5T Wealth Management is rapidly attracting new investors, and today boasts $110 million in assets under management. You can learn more about Lee O'Dwyer and 5T Wealth Management by visiting his website at http://www.5twealth.com/ . To listen to my interview with Lee O'Dwyer in full on Hedge Fund Radio, and to gain a glimpse into the future of retail asset management, please click on the play arrow above.

Featured Trades: (AFRICA), (EZW), (AFK), (GAF)

2) Some Feedback on South Africa. The great thing about the Internet is that sometimes it gives you back more than you put into it. In response to my piece on South Africa (EZW) a few days ago and my other work on Africa generally (AFK), (GAF) (click here for 'Feel Like Investing in a State Sponsor of Terrorism' ), a flood of data poured in bolstering my arguments in favor of the dark continent.

Africa has a population that approaches India and China's, possibly making it the next cheap labor market. Some 60% of the planet's remaining uncultivated land is there, which is why China, Libya, and Saudi Arabia have been pouring billions into agriculture there. Africa has 40% of the world's gold reserves and 10% of its oil reserves, with massive deposits of coal and other key resources.

If you have any doubts about Africa, take a look at the direct investment that has been pouring into the banking sector in South Africa in recent years, the most stable and best capitalized industry on the continent. HSBC has gobbled up Ned Bank, Barclays has gobbled up ABSA Bank, and China has taken a 20% stake in Standard Bank, probably the best run institution is the sector. Having been a four decade observer of the global financial system, I can tell you from experience that the changing of the guard in the banking system often presages major long term bull markets. You want to follow the smart money here.

Despite all this, only 3% of global direct investment finds there way there. Prices? are so low and earnings leverage so great that any dire political risks you can come up with, and there are definitely some out there, have got to already be priced in. It's just a matter of time before the markets address this imbalance.

Is Africa a Sleeping Giant?

Featured Trades: (COPPER), (ECH), (DBB), (FCX), (JJC)

iPath Dow Jones-UBS Copper Sub Index Total Return ETN

PowerShares DB Multi Sector Commodity Trust Metals

iShares MSCI Chile Index ETF

3) Is Copper the New Red Gold? Federal detention centers in the San Francisco Bay area are slowly filling up with a new type of criminals. Illegal immigrants and petty drug dealers are being joined by a rising tide of copper thieves raiding abandoned government facilities for their heavy gauge copper electrical wire. At current prices a decent night's haul can net crooks up to $20,000 at recycling centers.

Long known as 'Dr. Copper', because it is? the only commodity with a PhD in economics, the red metal has long been an excellent forecaster of economic activity around the world. Hedge fund managers have been impressed by copper's ability to hold up, and even advance in the face of 'double dip' threats from the US economy. While demand for American home construction remains in the basement, this weakness is more than offset by surging demand from China, whose own construction industry remains on a tear.

It also helps that they're not making copper anymore. Some of the world's largest mines are reaching the end of their useful lives, with increasing amounts of capital being poured into ripping a declining grade of ore from the earth. Global production has fallen 12% during the first half of this year. This is a problem because the opening of a new mine can take as long as 15 years, once the time required for government approvals, infrastructure, water supplies, transportation, and yes, bribes, is added in. What's in the pipeline is all there is for the next five years.

Copper is also benefiting from its accelerating 'monetization.' International investors, disgusted with the choices available in global stock and bond markets, are increasingly diversifying into the red metal, as well as other 'hard' assets like gold, silver, coal, oil, nickel, iron ore, and others. This is one reason why the big metals exchanges are finding their inventories at a low ebb. It's anyone's guess, but perhaps half of the current $4.40/pound in the copper price is accounted for by investor, as opposed to end user demand.

The obvious plays here are in the dedicated copper ETN (JJC), and the base metal ETF (DBB). Another candidate is Chile's ETF (ECH), which has tacked on a blistering 13% since I recommended it a month ago (click here for 'Chile is Hot'). And you can look at Freeport McMoran (FCX), the world's largest publicly listed copper producer. And yes, you can even buy .999 fine copper bullion bards at Amazon by clicking here.

I have some hedge fund friends who have discretely stashed thousands of copper bars in warehouses around the country, expecting the red metal to hit $6/pound within the next three years. If the doesn't work out, I guess they can always ea their inventory by pursuing a new career as an electrician. Hey, a good union and a steady $70/hour paycheck, what's so bad about that?

Copper Mines Are Running on Empty

Featured Trades: (ZHOU XIAOCHUAN), (FXI), ($SSEC),

(TUR), (EPOL), (EWY)

iShares FTSE/Xhinhua China 25 ETF

iShares MSCI Turkey Investable Market Index ETF

iShares MSCI Poland Investable Market Index ETF

South Korea iShares ETF

1) China's Central Bank Governor Defects to the US. The fiber optic cable that makes up the Chinese Internet is absolutely burning up today with rumors that the governor of the People's Bank of China, Zhou Xiaochuan, the Middle Kingdom's equivalent to Federal Reserve governor Ben Bernanke, has defected to the US. The Chinese authorities' efforts to censor the story has only succeeded in pouring fuel on the flames. Even if the rumors turn out to be untrue, this could mark the end of three decades of political stability in China.

The report was relayed to the US by Asia Pacific analyst Matt Gertken at STRATFOR, a Texas based boutique private intelligence and geopolitical forecasting firm. It is believed that Chuan was forced to leave the country because of an anti corruption scandal, or worse, a dramatic shakeup of China's macroeconomic and monetary policies. Chuan has not been seen in public since August 26.

China is facing a generational change in leadership in 2012, and the maneuvering has already begun over whether the country's breakneck economic reform policies will continue to move ahead, stagnate, or reverse. Many in the 2.25 million People's Liberation Army, where an underpaid rural underclass is well represented, have not been happy with the overemphasis on development of the coastal population centers. Even prime minister Web Jiabao has felt the heat. The brouhaha may explain why the main Shanghai index has sold off 5% in the past week, and the ETF (FXI) has clocked even bigger losses.

The story was just one of a daily outpouring of intelligence nuggets which I have been able to glean from STRATFOR's premium subscription service. The combined output of an impressive 70 man research team steeped in credentials and fluent in local languages has a global reach stretching from Vietnam to the Sudan and Latin America. They include coverage of several emerging markets now moving into prime time, which I have written on extensively, like Turkey (TUR), Poland (EPOL), and South Korea (EWY).

STRATFOR is one of a handful of private intelligence firms that hedge funds increasingly rely on, especially when considering a position in frontier markets where hard data is scarce. Readers of the Diary of the Mad Hedge Fund Trader can claim a $50 discount off STRATFOR's $349 annual fee by clicking here.

China's Central Bank Governor Zhou Xiaochuen:

Soon to Open a Liquor Store in Los Angeles?