“Sometimes, when you jump off a bridge, you have to grow your wings on the way down,” said author Danielle Steele.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/01/birds.png235472Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2026-03-27 09:00:232026-03-27 16:07:11March 27, 2026 - Quote of the Day

The Diary of a Mad Hedge Fund Trader is now celebrating its 18th year of publication.

During this time, I have religiously pumped out 3,000 words a day, or 18 newsletters a week, of original, independent-minded, hard-hitting, and often wickedly funny research.

I spent my life as a war correspondent, Marine Corps combat pilot, Wall Street trader, and hedge fund manager, and if you can’t laugh after that, something is wrong with you.

I’ve been covering stocks, bonds, commodities, foreign exchange, energy, precious metals, real estate, and even agricultural products.

You’ve been kept up on my travels around the world and listened in on my conversations with those who drive the financial markets.

I also occasionally opine on politics, but only when it has a direct market impact, such as with the recent administration's economic and trade policies. There is no profit in taking a side.

The site now contains over 20 million words, or 30 times the length of Tolstoy’s epic War and Peace.

Unfortunately, it feels like I have written on every possible topic at least 100 times over.

So, I am reaching out to your, the reader, to suggest new areas of research that I may have missed until now which you believe justify further investigation.

Please send any and all ideas directly to me at support@madhedgefundtrader.com/, and put “RESEARCH IDEA” in the subject line.

The great thing about running an online business is that I can evolve it to meet your needs on a daily basis.

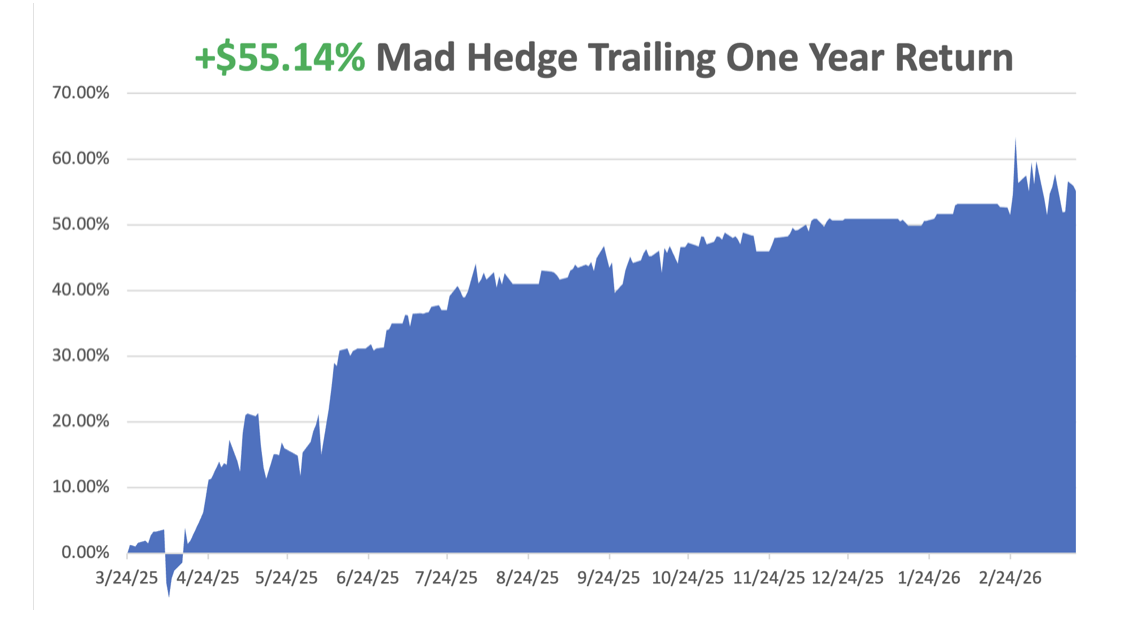

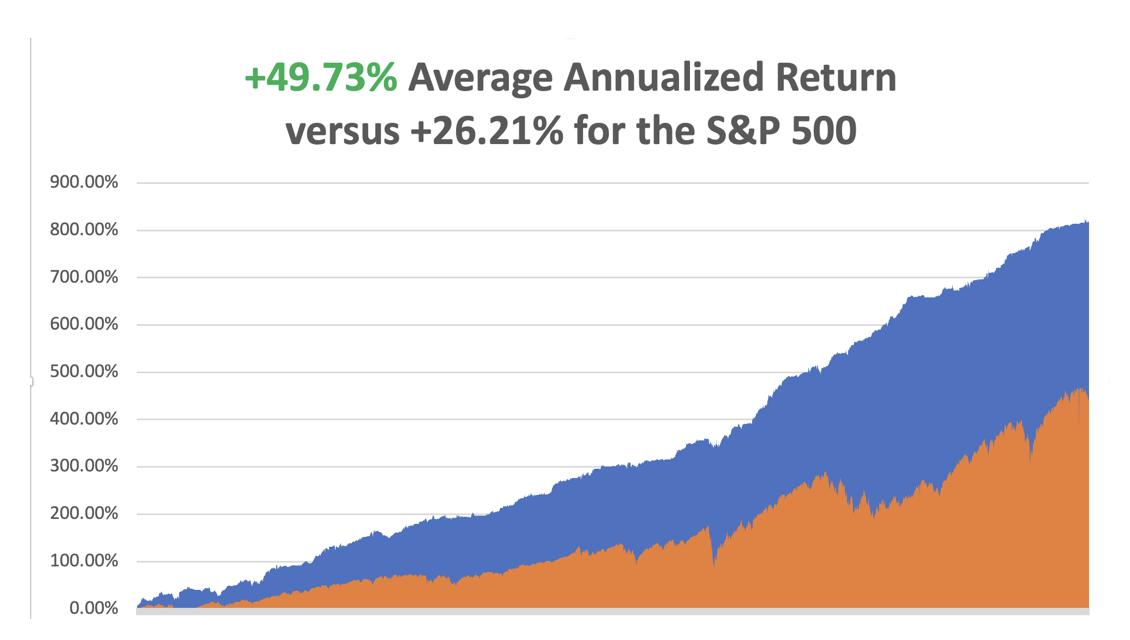

Many of the new products and services that I have introduced since 2008 have come at your suggestion. That has enabled me to improve the product’s quality, to your benefit. Notice how rapidly my trade alert performance is going up, now annualizing at +47%a year.

This originally started out as a daily email to my hedge fund investors, giving them an update on fast-moving market events. That was at a time when the financial markets were in free fall, and the end of the world seemed near.

Here’s a good trading rule of thumb: Usually, the world doesn’t end. History doesn’t repeat itself, but it certainly rhymes.

The daily emails gave me the scalability that I so desperately needed. Today’s global mega enterprise grew from there.

Today, the Diary of a Mad Hedge Fund Trader and its Global Trading Dispatch are read in over 140 countries by 30,000 followers. The Mad Hedge Technology Letter, the Mad Hedge Biotech & Health Care Letter, Mad Hedge AI, and Jacquie’s Post also have their own substantial followings. And the daily Mad Hedge Hot Tips is one of the most widely read publications in the financial industry.

I’m weak in distribution in North Korea and Mali, in both cases due to the lack of electricity. But that may change.

One can only hope.

If you want to read my first pitiful attempt at a post, please click here for my February 1, 2008, post.

It urged readers to buy gold at $950 (it soared to $2,200), and buy the Euro at $1.50 (it went to $1.60).

Now you know why this letter has become so outrageously popular.

Unfortunately, I also recommended that they sell bonds short. I wasn’t wrong on that one, just early, about eight years too early.

I always get asked how long I will keep doing this.

I am already collecting Social Security, so that deadline came and went. My old friend and early Mad Hedge subscriber, Warren Buffett, is still working at 92, so that seems like a realistic goal. And my old friend, Henry Kissinger, is still hard at it at 100 years old.

Hiking ten miles a day with a 50-pound pack, my doctor tells me I should live forever. He says he spends all day trying to convince his other patients to be like me, and the only one who actually does it is me.

The harsh truth is that I don’t know how to NOT work. Never tried it, never will.

The fact is that thousands of subscribers love me for what I do, pay for me to travel around the world first class to the most exotic destinations, eat in the best restaurants, fly the rarest historical aircraft, and then say thank you. I even get presents (keep those pounds of fudge and bottles of bourbon coming!).

Given the absolute blast I have doing this job, I would be Mad to actually retire.

Take a look at the testimonials I get on an almost daily basis, and you’ll see why this business is so hard to walk away from (click here to view them.)

In the end, you are going to have to pry my cold, dead fingers off of this keyboard to get me to give up.

Fiat Lux (let there be light).

https://www.madhedgefundtrader.com/wp-content/uploads/2020/07/John-Thomas-bull2.png514454april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-03-24 09:02:232026-03-24 16:03:51Founding the Mad Hedge Diary of a Mad Hedge Fund Trader

“Believe nothing that you hear, and half of what you see,” said the legendary investor, Ron Baron.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2026-03-24 09:00:192026-03-24 16:03:28March 24, 2026 - Quote of the Day

For the first time in three years, I’m back in the Big Apple!

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting in New York City on Tuesday, June 16, 2026. An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period.

I’ll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I’ll be throwing a few surprises out there too. Tickets are available for $299.

Space is very limited, so get your orders in early.

I’ll be arriving early and leaving late in case anyone wants to have a one-on-one discussion or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive hotel off of Times Square. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the seminar alone, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/statueliberty-e1677767107412.png323480april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-03-19 09:02:572026-03-19 12:16:45Tuesday, June 16, 2026 New York City Global Strategy Luncheon

"I know not with what weapons World War III will be fought, but World War IV will be fought with sticks and stones," said Nobel Prize winner Albert Einstein.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/explosion-quote-of-the-day-e1526421620709.jpg169300MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2026-03-19 09:00:252026-03-19 12:16:25March 19, 2026 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.