Mad Hedge Technology Letter

October 8, 2018

Fiat Lux

Featured Trade:

(A LONG-AWAITED BREATHER IN TECHNOLOGY),

(AMZN), (TGT), (NVDA), (SQ), (AMD), (TLT)

Mad Hedge Technology Letter

October 8, 2018

Fiat Lux

Featured Trade:

(A LONG-AWAITED BREATHER IN TECHNOLOGY),

(AMZN), (TGT), (NVDA), (SQ), (AMD), (TLT)

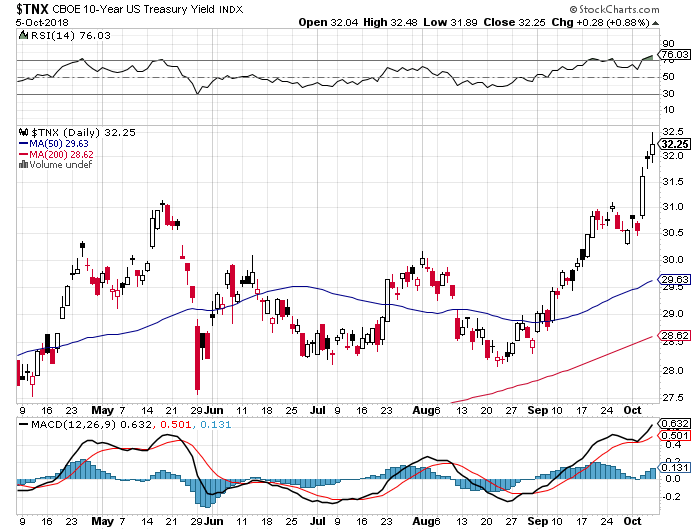

After two years of somnolent complacency, the bond market finally broke out of a two-year range, putting the cat among the pigeons with investors everywhere.

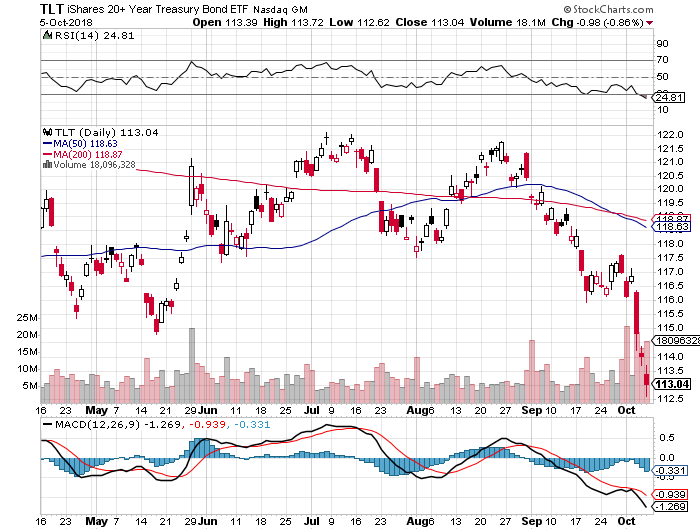

In a mere six weeks, the yield on the ten-year US Treasury bond (TLT) soared by 45 basis points from 2.80% to 3.25%, and 25 basis points during last week alone. It is the kind of move one normally associates with major financial crisis, the bankruptcy of a leading bank, or a major geopolitical event.

Once the 3.11% top was taken out, there was a virtual melt up to 3.25%. Rumors of Chinese dumping of its massive bond holdings were rife. Apparently, trade wars DO have consequences.

The 30-year fixed rate mortgage hit 5%, shutting millions out of the housing market. If you haven’t sold your home by now you’re in for the duration.

Personally, I believe that it was Amazon’s wage hike for 250,000 workers from $12 to $15 an hour that had the bigger impact. The inflation train is obviously leaving the station.

The free ride we have enjoyed in equities since February ended abruptly. The long, long overdue correction is here. This has ignited a rush by managers to lock in gains by selling off their biggest winners, and that would be the large cap tech stocks we have all come to know and love.

It started to be a great week with the settlement of NAFTA 2.0. Suddenly, Canada was no longer deemed a national security threat, and our supply of maple syrup was safe once again. My “trade peace” stocks soared.

The shocker came the next day when Amazon announced that it was raising wages by 25% for its 250,0000 minimum wage US workers. Suddenly, this inflation thing was real. It was the stick that broke the camel’s back.

General Electric (GE) dumped its CEO, after only a year and the stock rocketed 17%. It looks like the hedge fund that makes light bulbs still hasn’t found the “ON” switch.

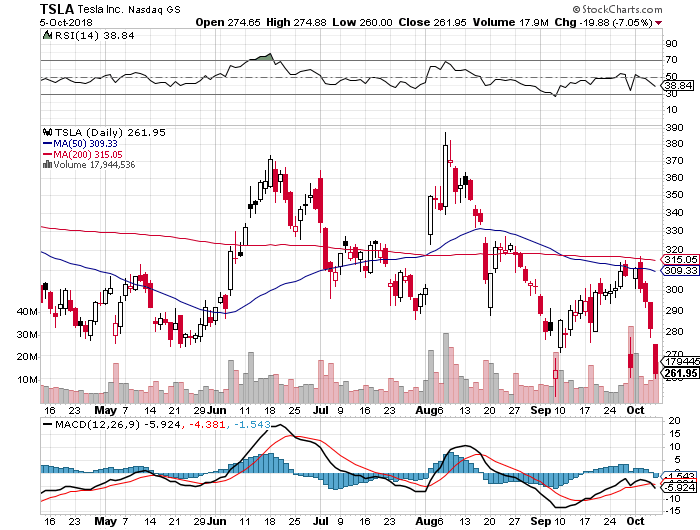

Tesla cut its deal with the SEC for a token amount, and the stock soared 20%. Then Elon tweeted once again, and it fell 20%. With the Defense Department now dependent on Musk to get their spy satellites into orbit there was no way the case against him was ever going anywhere.

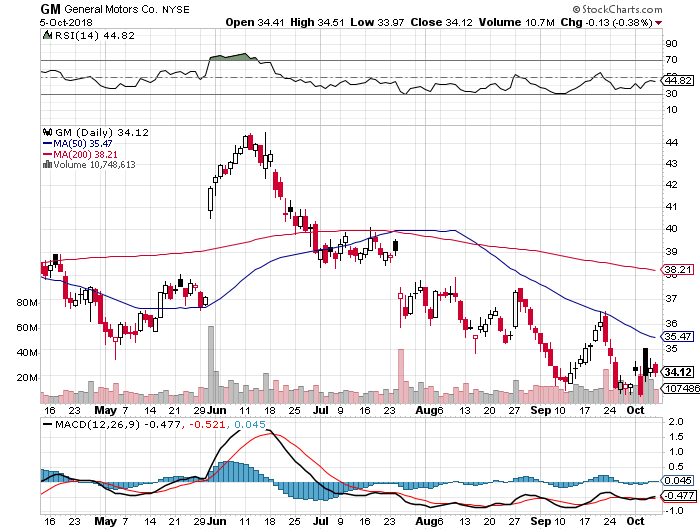

General Motors Q3 sales collapsed by 11.1% YOY as new Tesla 3 sales wiped out the electric Chevy Bolt, down 44%. The two hurricanes didn’t help here either.

Oil prices soared, driven by our new sanctions against Iran, knocking the wind out of transportation stocks like airlines Delta (DAL) and Southwest (LUV). The short squeeze is on, as Europeans scramble to make up lost Iran supplies. The last time this happened we went into a recession.

Tying up the week with a nice bow was the September Nonfarm Payroll Report, which took the headline unemployment rate down to 3.7%, the lowest since 1969.

I remember that year well. I was earning a dollar an hour at the May Company snack bar. Kids who dropped out of my high school were sent off to Vietnam and were killed within weeks. Neither the snack bar nor the May Company nor South Vietnam still exists, but I do. I guess I’m too mean to kill.

Average hourly earnings improved by eight cents to $27.24, and are up 2.8% YOY. Although the print was a weak 134,000, the back month upward revisions for July and August were huge.

Leisure and Hospitality lost 17,000 jobs due to the hurricanes, as did Retail, which shed 20,000 jobs.

Professional and Business Services were up 54,000, Health Care was up 26,000, and Manufacturing gained 18,000.

The performance of the Mad Hedge Fund Trader Alert Service is down -1.42% so far in October. Now, it’s all about keeping positions small. I managed to get a nice bond short off before the big collapse. But the real money was made being long the Volatility Index (VIX) which I missed.

Those who took my advice in the Wednesday Strategy Webinar to buy the iPath S&P 500 VIX Short Term Futures ETN (VXX) March 2019 calls for 50 cents make a quickie 500%.

My 2018 year-to-date performance has retreated to 26.97%, and my trailing one-year return stands at 32.11%.

My nine-year return appreciated to 303.44%. The average annualized return stands at 34.30%. I hope you all feel like you’re getting your money’s worth. The goal here is to minimize losses so we can bounce back quickly to a new all-time high once the dust settles.

Yes, I am looking at BUYING the bond market with a bet that ten-year yields won’t rise above 3.35% in the next month.

This coming holiday shorted week will be pretty non-eventful after last week’s fireworks.

Monday, October 8, is Columbus Day. Stocks will be opened but bonds will be mercifully closed.

On Tuesday, October 9 at 6:00 AM, the September NFIB Small Business Optimism Index is announced.

On Wednesday October 10 at 8:30 AM, the September Producer Price Index is published.

Thursday, October 11 at 8:30 we get Weekly Jobless Claims. At the same time, we get the September Consumer Price Index, the most important inflation indicator.

On Friday, October 12, at 10:00 AM, we learn September Consumer Sentiment. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, it’s fleet week so I’ll be watching the Parade of Ships come in under the Golden Gate Bridge. After that, the Navy’s Blue Angels will be flying overhead using my mountain top home as a key navigation point. I’ll be wishing I was in the air at the stick with them.

Good luck and good trading.

It was the kind of dinner invitation I couldn’t turn down. What I learned was amazing.

I usually prefer to spend my evenings at home catching up on my research, calling customers, and plotting my next great Trade Alert.

So, it takes a lot to get me out of my cozy digs, especially given the recent incredible sunsets we have been getting.

Attending would be senior executives from Tesla (TSLA), General Motors (GM), and engineering professor from the University of California at Berkeley, and the California Air Resources Board.

With US car stocks going ballistic lately, I thought the event would be timely.

The dinner was hosted by a retired billionaire from Microsoft at the top of the Mark Hopkins Hotel in San Francisco.

The topic for discussion would be the very long-term future of the car industry.

I get invited to these things because the guests want to know how their views would fit in within a long-term global geopolitical/economic context, my own particular specialty.

I didn’t want to cramp anyone’s style so I kept my notebook under the table and scribbled away blindly, and illegibly. There’s no particular story line here.

I’ll just give you my random thoughts.

(GM) launched its second-generation Chevy Volt in 2015, and the customer response has been fantastic. The company is building a new $400 million battery plant on the east coast to help meet demand.

Some 60% of the buyers are coming from other automakers. It is fast becoming the new face of Chevy, like the Corvette Stingray and Camaro of years past.

The future is in a 200-mile range $30,000 car, and the Volt is that car, followed by the recently launched all electric Bolt.

Customers want to get away from oil and will only buy the products that accomplish that, be they hybrids or all electric.

He also mentioned that GM is launching an electric bike, which is already widespread in Europe. Not a big needle mover there.

The Tesla guy then proceeded to jump all over him, saying the Volt was “green washing” as usual, since it represents only a tiny fraction of the company’s sales.

GM had a vested interest in promoting the internal combustion engine, in which it had made a century long investment.

Its real focus can be seen in the giant new Suburban factory it was now building in Texas.

Mr. Tesla had driven from the south Bay with his S-1 entirely on autopilot.

The hardware has already been pre-installed in every S-1 produced since 2014, and all that is needed to make them self-driving is to execute a wireless overnight software upgrade.

What is truly amazing is that each car will have a learning program unique to the vehicle. If it misses a hard turn the first time, it will remember that turn and then make it perfectly every time from then on.

The Tesla person said that with the new Gigafactory the company will be on schedule for a tenfold ramp up in car production by 2020.

The $35,000 Tesla 3 that will make this possible will be offered in two wheel and four wheel drive variations. That will take them from 92,000 units a year to 500,000. Q3 2018 Production has already reached 53,000.

I asked him if this means that if your wife suspects you of cheating, will your Tesla rat you out. He answered, “Only if she is a coder.”

Then I wondered what would stop Tesla from selling your driving habits to marketers who would then make special offers from stores you prefer.

A previous Tesla experiment landed me a pair of Seven for All Mankind designer jeans for half off.

Tesla outsells every other luxury car of its class, including the Mercedes S class, the BMW Series 7, and the Audi 8.

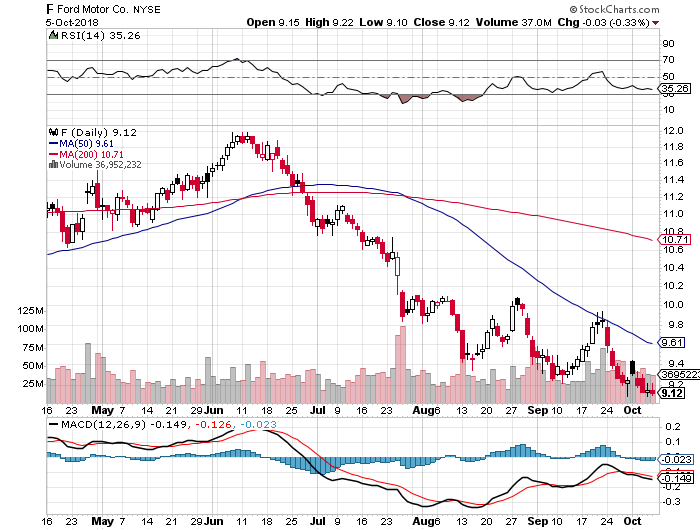

Among the US car industry, only Ford and Tesla have never filed for bankruptcy. Tesla is the first new car manufacturer to succeed since Chrysler made its debut in 1928.

I asked about the S-1 maximum single charge range achieved by a driver.

An enthusiast in Norway managed to take one 800 miles on a flat track with no wind and perfect conditions. Wow! My drive from Lake Tahoe record of 400 miles doesn’t come close, and that involved a 7,000 foot decline from the High Sierra crest.

I also enquired about the Cambridge University battery breakthrough (click here for “Battery Breakthrough Promises Big Dividends.”

He said he was aware of it, but that it takes a long time to get a technology from the bench to the marketplace.

Just with their own in-house tinkering, Tesla is boosting battery ranges by 3-5% a year. The current S-1 gets a 305-mile range, compared to my four-year-old 255-mile range.

The Berkeley professor made some interesting observations about Millennials.

He said that while 75% of baby boomers got drivers licenses at 16, and 70% of Generation Xer’s did so by then, only 55% of Millennials took to the road at that age.

The rule of thumb for anything regarding Millennials is that they do everything late.

The gentleman from the Air Resources Board brought out some interesting facts.

More than 80% of all cancer-causing chemicals entering the atmosphere come from diesel engines, so a major effort will be made to cut back emissions from commercial trucks.

Look for the electric fleet coming to a neighborhood near you. Goodbye Volkswagen!

Workplace charging of employee cars will be the next big growth area for charging stations.

Half of all greenhouse gases derive from the burning of oil. The biggest savings in greenhouse gas emissions will come from a clampdown on the refining industry.

Think Koch Brothers.

I was amazed at his commitment to meet California’s goal of obtaining 50% of its energy from alternative sources by 2030.

The oil industry managed to exempt gasoline from the legislation, SB 350. But Governor Jerry Brown put it back in through an executive order.

The state is paying for the initial build-out of hydrogen refueling stations for the new $57,500 Toyota Mirai. A single tank will take the fuel cell vehicle 312 miles.

The state is making major investments in biofuel, planning to obtain 10% of the 50% target from this source.

During a slow moment, I asked a bleach blond trophy girlfriend sitting next to me of her interest in electric cars, expecting the worst.

To my surprise, she said that last summer, she drove an electric bike from New York to Los Angeles, towing a trailer with a solar panel cut in half to provide power.

The southern route avoided the high mountain ranges. I noticed she seemed unusually tanned, and it wasn’t from a can.

I was humbled. For once, I knew less about electric cars than anyone else in the room.

After the dinner, I went up to the Tesla executive and told him “Job well done.” I used to own one of the oldest S-1’s, number 125 off the assembly line, until it was totaled by a drunk driver on Christmas Eve.

I even tested to their safety claims.

Thank you, Tesla! You saved my life!

Taking profits - it was finally time.

The Nasdaq has been hit in the mouth the last few days and rightly so.

It was the best quarter in equities for five years, and a quarter that saw tech comprise up to a quarter of the S&P demonstrating searing strength.

It would be an understatement to say that tech did its part to drive stocks higher.

Tech shares have pretty much gone up in a straight line this year aside from the February meltdown.

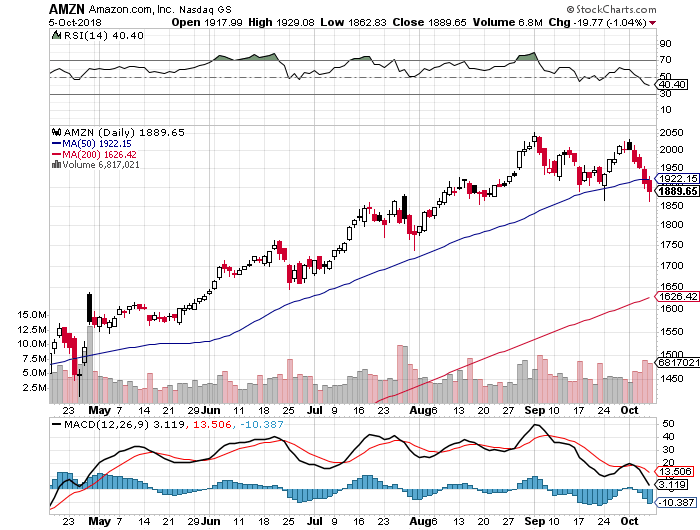

Even that blip only caused Amazon (AMZN) to slide around 10%.

After all the terrible macro news thrown on the market in spades – tech stocks held their own.

Not even a global trade war with the second biggest economy in the world which is critical to exporting products to America was able to knock tech shares off their perch.

At some point, 26% earnings growth cannot sustain itself, and even though the tech narrative is still intact, investors need to breathe.

Let’s get this straight – tech companies are doing great.

They benefit from a secular tailwind with every business pivoting to mobile and software services.

All that new business has infused and invigorated total revenue.

The negative reaction by technology stocks was based on two pieces of news.

Interest rates (TLT) surging to over 3.2% was the first piece of news.

The increase in rates reinforces that the economy is humming along at a breakneck speed.

Yields are going up for the right reasons and this economy is not a sick one indeed.

As rates rise, other asset classes become more attractive such as CD’s and bonds.

The whole world is looking at the pace of rate rises because this will affect the ability for tech behemoths to borrow money to invest in their expensive well-oiled machines.

Three things are certain - the economy is hot, the smart money is buying on the dip now, and Amazon will still take over your home.

Even in a rising rate environment, Amazon is fully positioned to outperform.

The second catalyst to this correction was Amazon’s decision to hike its minimum wage to $15 per hour.

This could lay the path for workers around the country to demand higher pay.

The move was a misnomer as it will eliminate stock awards and monthly bonuses lessening the burden that Amazon actually has to dole out.

Call this a push – the rise in expenses won’t be material and realistically, Amazon can afford to push the wage bill by another order of magnitude, even though they will not.

This was also a way for Amazon founder Jeff Bezos to keep Washington off his back for a few months, and his generous decision was praised by government officials.

The wage hike underscores the strength of the ebullient American economy, and the consumer will benefit by recycling their wages back into Amazon and the wider economy.

Amazon makes up 50% of American e-commerce sales, and when workers are buying goods online, a good chance its coming from Amazon.

In an environment of full employment, the natural direction of wages is up, and this was due to happen.

You can also look at wage inflation as employees gaining at the expense of the corporation.

However, the massive deflationary trends of technology will also make this wage hike quite irrelevant over time as Amazon will automate more of their supply chain to make up for any wage hike that could damage revenue.

Amazon’s economies of scale give the Seattle-based company enough levers and buttons to push and pull to dilute expenses to make this a non-issue.

Each earnings call usually involves CFO of Amazon Brian Olsavsky explaining the acceleration of efficiencies in fulfilment centers bolstering the bottom line.

The stellar innovation in operational expertise moves up a level each quarter if not two levels.

Ultimately, though expensive on the surface, this won’t affect Amazon’s numbers at all, but more critically please the lower tier of workers who fight and scratch for their daily crust of bread.

This win-win scenario casts a positive image of Bezos in the public eye at a crucial time when he plans to recruit another legion of Amazon workers, as Amazon will shortly announce the location of their second American-based headquarter.

In fact, this turns the screws on the smaller retailers who must match the $15 per hour wage or confront a potential disaster of an entire workforce walking out and joining Amazon.

The mysterious Amazon-effect works in many shapes and sizes.

Big retailers like Target (TGT) have griped that it’s near impossible to find seasonal workers for the upcoming holiday season.

Moreover, if inflation remains moderate but contained – technology will power on.

And it will take more than a few prints of rising inflation to impress the Fed enough to expedite the raising of rates.

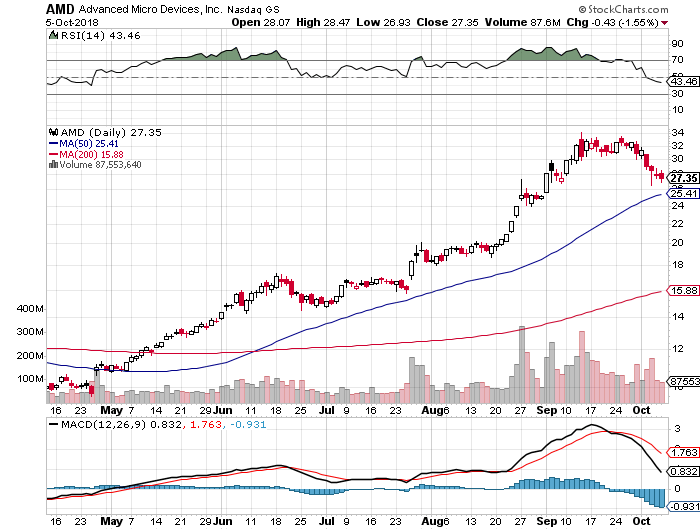

But it is safe to say that investors cannot expect the 100% up moves like in Amazon and Advanced Micro Devices (AMD) in one calendar year moving forward.

Technology has a plate full of challenges facing its share price as we move into the latter part of the fiscal year.

The challenges are two-fold - mid-term elections and navigating a smooth year-end.

Earnings should be good which is already baked into the pie, and the benefits of the tax cut have already worked itself through the system.

The furious pace of share buybacks will eventually subside too.

Management might finally bring out the spin doctors claiming the stronger dollar and worsening trade war is the reason to guide down.

At least tech companies doing business in China might follow this playbook.

Either way, tech shares are demonstrably sensitive right now and while the market needs tech to lead the way, the sector is exhausted from the burden of carrying the bulk of the load.

Freak-outs on rate surges have been a common experience for those old hands presiding over markets for decades.

These are all the staples of a 9th year bull market.

Typical late stage topping action is normal in economic cycles.

After the dust settles, the overreaction will give way to great buying opportunities at great prices, albeit it in the higher quality names.

The chip sector is still one to avoid unless the names are Advanced Micro Devices or Nvidia (NVDA).

Legacy companies have always been a no-go.

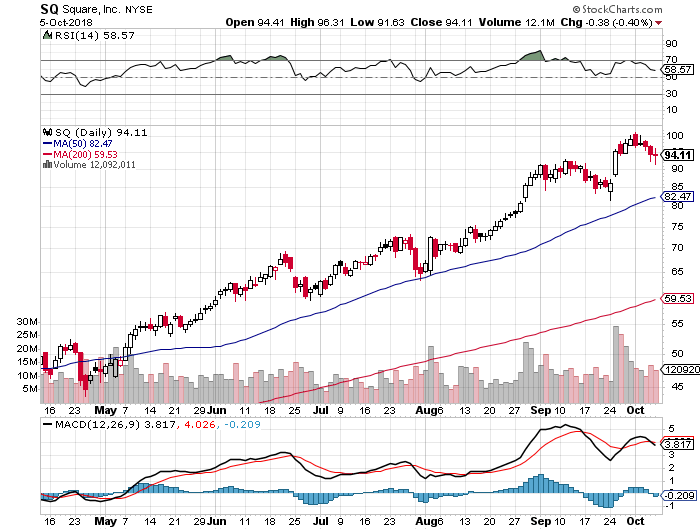

If you want hyper-growth, fin-tech name Square (SQ) would be an ideal candidate.

If buy and hold is your cup of tea, any 10% discount would be a great entry point in any of these quality companies.

“I hope Puerto Rico munis go lower so I can buy more.” – Said Founder of DoubleLine Capital Investment Firm Jeffrey Gundlach three years ago.

When invited to run for president in 1868, Civil War general William Tecumseh Sherman replied, “I would rather spend a year in Sing Sing than Washington DC, and I’d come out a better man.”

Mad Hedge Hot Tips

October 5, 2018

Fiat Lux

The Five Most Important Things That Happened Today

(and what to do about them)

1) The Panic is On. So, stock markets really don’t like rising interest rates? There’s now a rush by managers to lock in gains by selling off biggest winners, and that would be all of technology. Who knew? Worse to come. Click here.

2) Unemployment Rate Hits a 49-Year Low at 3.7%. I remember it well. I was earning a dollar an hour at the May company snack bar. Neither the snack bar nor the May Company still exist, but I do. Bonds take it on the nose. Click here.

3) JP Morgan Lays Off 400 in the Mortgage Department. If you haven’t sold your house by now you’re screwed. Read my piece on how to ride out the next recession. The good news? You’ll be able to refi at 0% during the next recession if you still own your home. Click here.

4) Daimler Benz Will Start Making Batteries in Alabama, in the first serious threat to Tesla (TSLA) since its foundation 15 years ago. Is it time for Elon Musk to stop tweeting and start looking over his shoulder? Click here.

5) Tronc is Changing its Name Back to Tribune Publishing. In the worst rebranding effort in history the owner of the Chicago Tribune and the LA Times is reversing course after only a year. One comedian said “Tronc” was the noise made when newspapers were dumped in the recycling bin. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(WEDNESDAY OCTOBER 17 HOUSTON STRATEGY LUNCHEON INVITATION),

(OCTOBER 3 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (VIX), (VXX), (MU), (LRCX), (NVDA), (AAPL), (GOOG), (XLV), (USO), (TLT), (AMD), (LMT), (ACB), (TLRY), (WEED)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

October 5, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY OCTOBER 17 HOUSTON STRATEGY LUNCHEON INVITATION),

(OCTOBER 3 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (VIX), (VXX), (MU), (LRCX), (NVDA), (AAPL), (GOOG), (XLV), (USO), (TLT), (AMD), (LMT), (ACB), (TLRY), (WEED)

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting in Houston, Texas, on Wednesday, October 17, 2018.

A three-course lunch will be followed by a wide-ranging discussion and an extended question-and-answer period.

I’ll be giving you my up-to-date view on stocks, bonds, foreign currencies, commodities, energy, precious metals, and real estate. And to keep you in suspense, I’ll be tossing a few surprises out there, too.

Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $228.

I’ll be arriving an hour early and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a private downtown Houston club that will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets, please click here.