It is the greatest conundrum facing traders, investors, and financial advisors today.

The recent "soft" economic data says the economy is booming, animal spirits are roaring, and the Trump trade is alive and well.

The "hard" data indicates that the economy is fading, fear and uncertainty are rampant, and you should sell everything immediately.

It is the greatest hard/soft divergence in the modern history of the US economy.

What's a poor investor to do?

Get this one right, and you'll make a killing. Get it wrong, and your portfolio will turn to ashes.

The numbers are undeniable.

"Soft" data comprises various poll-driven reports, such as consumer confidence and business surveys. These have been running.

The University of Michigan Consumer Sentiment Index hit a decade high in January and is up enormously YOY. Business surveys of every description are breaking records.

That "hard" data comprises economic reports that measure actual activity, such as retail sales.

These have not rebounded nearly as much as the soft data. Retail sales, housing sales, and the negative wealth effect of a falling stock market have all been turning in in-line or disappointing prints.

Here's a further complicating factor. Soft data is forward looking, while hard data is decidedly backward focused, often turning in numbers that are months old.

As a result, many private economic forecasters, and even different agencies of the US government are coming up with spectacularly diverging economic predictions based on the hard/soft weighting of their models.

The Federal Reserve Bank of New York's model, which gives more weight to the soft data, is currently projecting a 3% gross domestic product "print" this year.

On the other hand, the Federal Reserve Bank of Atlanta's model, which incorporates less soft data, is expecting only a 1% print.

You might as well throw a dart at the wall in a dive bar and pick a number.

Dig deeper into the numbers, and your conclusions can only become more disturbing.

It turns out that the overwhelming bulk of positive sentiment is coming from largely small businesses in red Trump-supporting states. They're clearly drinking the Kool-Aid.

You get almost the opposite result on the East and West Coasts, or in surveys that only look at Fortune 500 companies.

Eventually, only one group will be right. Either the hard data will catch up with the soft data, or it won't.

With November midterm elections getting closer by the day, with no new legislation passed this year, I believe the Trump trade will take MUCH longer to play out than expected.

In fact, a major economy-shifting bill may not pass at all this year.

So don't dump your stocks on pain of death. The bull market in stocks probably has at least another year to run.

Just don't expect too much excitement for the next several months.

Sell every rally AND buy every dip. This is what the pros are doing, with great success, as well as the followers of the Diary of a Mad Hedge Fund Trader.

Is This One Hard, Soft, or Both?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/STORY-3-image-2-1-e1522353630440.jpg200300MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-04-02 01:06:512018-04-02 01:06:51The Hard/Soft Data Conundrum

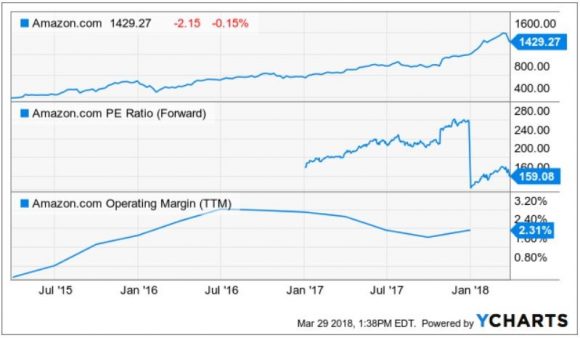

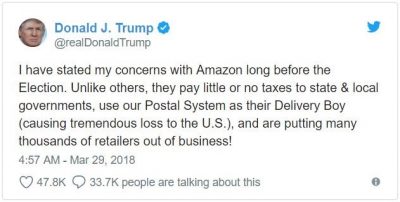

POTUS's Amazon tweet of March 29 has given investors the best entry point into Amazon (AMZN) since the January 2016 sell-off. Since then, the stock has essentially gone up every day.

Entry points have been few and far between as every small pullback has been followed by aggressive buying by big institutional money.

The 200-point nosedive was a function of the White House's dissatisfaction of leaked stories that would find their way into the Washington Post owned by Amazon CEO Jeff Bezos, my former colleague and good friend.

Although there are concerns about Amazon's business model, notably its lack of actual profits, there is no impending regulatory action. And, if there is one company that's in hotter water now, it's Facebook (FB), which inadvertently sells every little detail about your personal life to third-party Eastern European hackers.

Amazon's e-commerce business does not violate the Federal Trade Commission Act of 1914 of "deceptive" or "unfair practices."

The American economy has rapidly evolved thanks to hyper-accelerating technology, and the jobs required to support the modern economy have changed beyond all recognition.

The Clayton Antitrust Act of 1914 addressing harmful mergers that destroy competition hasn't been breached either since Amazon has grown organically.

Analyzing the most comprehensive law, the Sherman Antitrust Act of 1890, which was originally passed to control unions, espouses economic freedom aimed at "preserving free and unfettered competition as the rule of trade."

And, in a way, Amazon could be susceptible, but it would be awfully difficult to persuade the U.S. Department of Justice (DOJ) Antitrust Division and would take a decade.

Amazon's business model will change many times over by the time any antitrust decision can be delivered, or even entertained.

Helping Amazon's case even more is the DOJ interpretation of the three antitrust rules. It is the company's duty to first and foremost protect the consumer and ensure business is operating efficiently, which keeps prices low and quality high. Antitrust laws are, in effect, consumer protection laws.

Amazon's e-commerce segment epitomizes the DOJ's perception of these 100-year-old laws.

The controversial part of Amazon's business model is funneling profits from its Amazon Web Services (AWS) division as a way to offer the lowest prices in America for its e-commerce products.

This strategy has the same effect as dumping since it is selling products for a loss, but it is not officially dumping.

POTUS has usually delivered more bark than bite. The steel and aluminum tariffs went from no exceptions to exceptions galore in less than a week. Policies and employees change in a blink of an eye in the White House.

The backlash is a case of the White House not being a huge admirer of Amazon, but individual government workers probably have Amazon boxes stacked to the heavens on their doorsteps.

It is true that Amazon has negatively affected retail business. It is doing even more damage to traditional shopping malls, which it turns out are owned by close friends of the president. The mom-and-pop stores have disappeared long ago. But Amazon could argue this trend is occurring with or without Amazon.

In addition, Walmart (WMT) was the original retail killer, and it currently is morphing into another Amazon by investing aggressively into its e-commerce division. Does the White House go after (WMT) next?

Unlikely.

Amazon didn't create e-commerce.

Amazon also didn't create the Internet.

Amazon also does pay state and local taxes, some $970 million worth last year.

Technology has been a growth play for years.

Investors and venture capitalists are willing to fork over their hard-earned cash for the chance to own the next Google (GOOGL) or Apple (AAPL).

Many investors do lose money searching for the next unicorn. A good portion of these unicorns lose boatloads of money, too.

Spotify, slated to go public soon, is a huge loss-maker and investors will pay up anyway.

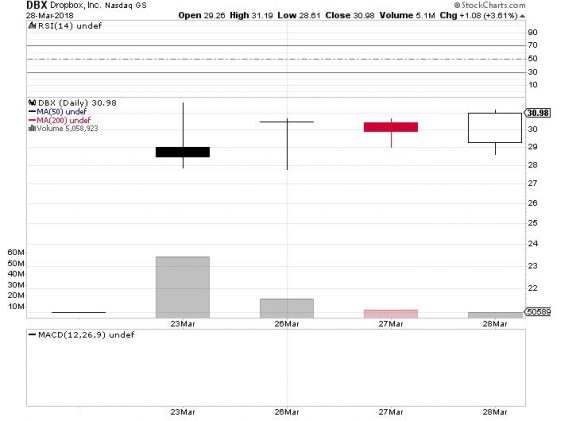

Investors went gaga for Dropbox (DBX), already up 40% from its IPO, and it lost $112 million in 2017.

The risk-appetite is hearty for these burgeoning tech companies if they can scale appropriately.

Should investors be prosecuted for gambling on these cash-losing businesses?

Definitely not. Caveat emptor. Buyer beware.

It is true that Amazon pumps an extraordinary percentage of revenues back into product development and enhancement.

But that is exactly what makes Amazon great. It not only is focused on making money but also on making a terrific product.

The bulk of its enhancement is allocated in warehouse and data center expansion. Splurging on more original entertainment content is another segment warranting heavy investment, too, a la Netflix (NFLX). Did you spot Jeff Bezos at the last Oscar ceremony?

Contrary to popular belief, Amazon is in the black.

It has posted gains for 11 straight quarters and expects a 12th straight profitable quarter for Q1 2018.

The one highly negative aspect is profit margins. It is absolutely slaughtered under the current existing model.

However, investors continually ignore the damage-to-profit margins and have a laser-like focus on the AWS cloud revenue.

Amazon's AWS segment could be a company in itself. Cloud revenue last quarter was $5.11 billion, which handily beat estimates at $4.97 billion.

Amazon's cloud revenue is five times bigger than Dropbox's.

The biggest threat to Amazon is not the administration, but Microsoft (MSFT), which announced amazing cloud revenue numbers up 98% QOQ, and has grown into the second-largest cloud player.

(MSFT) is equipped with its array of mainstay software programs and other hybrid cloud solutions that lure in new enterprise business.

(MSFT) has the chance to break Amazon's stranglehold if it can outmuscle its cloud segment. However, any degradation to Amazon's business model will not kill off AWS, considering Amazon also is heavily investing in its cloud segment, too.

Lost in the tweet frenzy is this behemoth cloud war fighting for storage of data that is somewhat lost in all the political noise.

This is truly the year of the cloud, and dismantling Amazon is only possible by blowing up its AWS segment. The more likely scenario is that AWS and MSFT Azure continue their nonstop growth trajectory for the benefit of shareholders.

Antitrust won't affect Amazon, and after every dip investors should pile into the best two cloud plays - Amazon and Microsoft.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-04-02 01:05:512018-04-02 01:05:51Why There Will Never Be an Antitrust Case Against Amazon

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Take a look at the worst performing stocks of the past two weeks and they all have one theme in common: artificial intelligence.

You can trace the beginning of the move back to the Arizona crash by an Uber AI autonomous driven car that killed a pedestrian.

As all those who have studied chaos theory in mathematics, it's like the proverbial butterfly that flapped its wings in a Brazilian rain forest, which then triggered a typhoon in Japan.

Never mind that the pedestrian was jaywalking at night wearing dark clothes. AI is supposed to see this. My guess is that only a sensor failure could have caused the accident, a dud $5 part, which means it has nothing to do with AI.

This is the second autonomous driving death in three years. The last one, involving a Tesla Model S-1 in Florida, didn't see the back of a white truck while driving into the sun, and crashed into it, killing the driver.

And here is the problem if you are a trader or investor.

Autonomous driving has been a major theme in the entire tech sector for the past two years.

You can start with the car companies, Tesla (TSLA), Uber, and Google's (GOOGL) Waymo, and extend all the way out through the entire ecosystem.

That would include the chip makers, NVIDIA (NVDA), which is suspending its autonomous program, Intel (INTC), Advanced Micro Devices (AMD), and the chip equipment maker Lam Research (LRCX).

So, is it game over for these companies? Is it time to pick up our marbles and play elsewhere (there is nowhere else)?

I don't think so.

Let's look at the hard numbers involving automobile accidents. During the same three-year period that AI cars killed two people, human drivers killed a staggering 100,000, and left millions with injuries.

So there is absolutely no doubt that AI is the superior technology. AI-driven cars don't text while driving, drink, take drugs, drive while tired, overdo it with an afternoon of wine tasting in Napa Valley, or look down at their cell phones, as did the safety driver in the ill-fated Uber car in Phoenix.

AI is not just a self-driving car theme. It is permeating every aspect of the modern economy and will continue to do so at an accelerating pace. It is no one-hit wonder.

All that is happening now is that AI and tech stocks in general are backing off from grievously overbought conditions.

As we approach the next round of earnings reports in a month, the market focus rapidly will shift back from tedious and distressful technicals. That's when they will rocket again.

There is an old market term for the current state of technology stocks. It is known as a "Buying Opportunity."

I haven't been able to touch stocks I love for months because they were completing upward moves of 50% to 300% over the past two years.

They have just become touchable once again.

To watch the video of the Phoenix crash and the expression of the clueless safety driver, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/uber-image-6-e1522274442669.jpg288480MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-03-29 01:07:562018-03-29 01:07:56Is It All Over for Artificial Intelligence?

Thanks to China's "one child only" policy adopted 30 years ago, and a cultural preference for children who grow up to become family safety nets, there are now 32 million more boys under the age of 20 than there are girls.

Large-scale interference with the natural male:female ratio has been tracked with some fascination by demographers for years and is constantly generating unintended consequences.

Until early in the last century, starving rural mothers abandoned unwanted female newborns in the hills to be taken away by "spirits."

Today, pregnant women resort to the modern day equivalent by getting ultrasounds and undergoing abortions when they learn they are carrying girls.

Millions of children are "little emperors," spoiled male-only children who have been raised to expect the world to revolve around them.

The resulting shortage of women has led to an epidemic of "bride kidnapping" in surrounding countries. Stealing of male children is widespread in Vietnam, Cambodia, Laos, and Mongolia.

The end result has been a barbell-shaped demographic curve unlike that seen in any other country.

The Beijing government says the program has succeeded in bringing the fertility rate from 3.0 down to 1.8, well below the 2.1 replacement rate.

As a result, the Middle Kingdom's population today is only 1.2 billion instead of the 1.6 billion it would have been.

Political scientists have long speculated that an excess of young men would lead to more bellicose foreign policies by the Middle Kingdom.

But so far the choice has been for commerce, to the detriment of America's trade balance and Internet security.

In practice, the one-child policy was only applied to those who live in cities or had government jobs. That is about two thirds of the population.

On my last trip to China I spent a weekend walking around Shenzhen city parks. The locals doted over their single children, while visitors from the countryside played games with their three, four, or five children. The contrast couldn't have been more bizarre.

Economists now wonder if the practice also will understate China's long-term growth rate. Parents with boys tend to be bigger savers, so they can help sons with the initial big-ticket items in life, such as an education, homes, and even cars.

The endgame for this policy has to be the Japan disease; a huge population of senior citizens with insufficient numbers of young workers to support them. The markets won't ignore this.

In the latest round of reforms announced by the Chinese government was the demise of the one-child policy.

But no matter how hard you try, you can't change the number of people born 30 years ago.

The boomerang effects of this policy could last for centuries.

After watching the performance of technology stocks over the past two weeks, you may be on the verge of slitting your wrist, overdosing on drugs, and then jumping off the Golden Gate Bridge.

However, the results reported by tech companies this week say you should be doing otherwise.

As tech companies confront upcoming regulation and an overseas trade war, it has felt like a death by a thousand cuts.

It almost is starting to feel as if being a technology company is akin to drinking from a poisoned chalice.

I beg to differ.

I will tell you why the destiny of tech is quite positive.

The long-term secular growth drivers will prevail of accelerated earnings amid a backdrop of global economic synchronized expansion.

Assiduous capital reallocation programs will attract investors instead of detract from them.

The ironic angle to the precarious diplomatic tumult is that regulation will ultimately benefit the current pacesetters and culprits of technology because the barriers of entry become insurmountable.

The trade war has the same effect as the data regulation because it is ultimately for the betterment and protection of domestic, made-in-USA technology.

Washington knows the FANGs all too well, and the bull market will cease to exist if Beijing buys out our technological expertise.

Short-term pain for long-term gain. That's it in a nutshell.

The White House further understands that it's better to start a trade war now when it holds a stronger hand. No doubt after 20 more years of an ascending China, the Middle Kingdom will leverage its economic clout for diplomatic power dictating the outcome more ruthlessly.

Effectively, Trump's trade fracas is a one step back and two steps forward policy. During the one step back phase simply seems as if the economy is taking a nosedive into the ocean floor.

Love it or hate it, technology is becoming more (and not less) ubiquitous. However, it's gone too far too fast, and society and public officials require time to absorb the new environment or you risk the current backlash.

Simultaneously, America is in the one step back phase of data regulation, trade laws, and society's backlash of encroaching tech.

Bad timing.

The teething problems will gradually subside, the stock market will re-ignite, and tech will advance further into regular life.

The market even has seen some green shoots with the blockbuster Dropbox (DBX) IPO up over 40% intraday on the first day of trading.

In the S-1 filing required for IPOs, (DBX) stated that it may "not be able to achieve or maintain profitability" because of increasing expenses. The disclosure also prefaced its "history of net losses" to justify the business direction.

(DBX) lost $111.7 million in 2017, on revenues of just over $1 billion.

Technology must be doing something right if loss-making firms are treated with a 40% gain on IPO day; and, Spotify, an even bigger money loser, will go public next week.

If investors are smitten with loss-making tech companies, I imagine they feel quite comfortable with the ones earning billions in quarterly profits and growing at a pace where analysts cannot hike their price targets quick enough, making them look foolish.

The outstanding gains by (DBX) was for one reason and one reason only.

It's a pure cloud play, and pure cloud plays have been rewarded in spades.

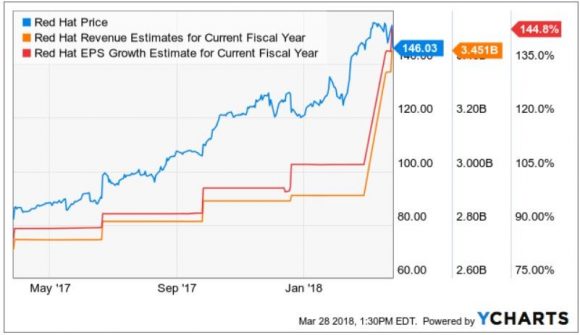

Red Hat's (RHT) stellar earnings were on the heels of the (DBX) IPO success.

Red Hat is a medium-size unadulterated cloud play that lacks the financial resources of the FANGs but is still turning a profit.

It is the poster boy for enterprise cloud companies flourishing in an unrelenting fierce environment.

If the world is going to hell in a handbasket, then how did Red Hat achieve aggregate billings growth of 25%?

Everyone and their uncle expect tech companies to start floundering, but the opposite is true. They overpromise then over deliver to the upside every quarter.

Red Hat booked the most deals over $1 million in Q4 2017 in its history.

Cross-selling cloud applications was especially strong with 81% of deals over $1 million spending on multiple software services.

The critical subscription revenue comprised 88% of Q4 revenue and is up 15% YOY. Application development-related subscriptions were up 42% YOY, higher than the infrastructure-related subscription revenue growing 17% YOY.

Companies are churning out innovation on top of their existing platforms using various software solutions. And every company in the world is migrating toward cloud software and infrastructure. There has never been a better time to be a pure cloud company.

The most poignant telltale sign was that Red Hat renewed 99 out of 100 of its top deals and disclosed that multiyear deals were healthy.

Ansible, its software for automating data center operations, OpenShift, its software for container-based deployment and management, and OpenStack, an infrastructure-as-a-service (IaaS) for cloud computing are the underpinnings to Red Hat's supreme business.

The reoccurring revenue salted away is legion.

The FY 2018 guidance was even more impressive than the quarterly earnings report. Red Hat expects a revenue range between $800 million and $810 million, up from the $748 million last quarter and expects quarterly EPS at $0.81, up from $0.70 last quarter.

Toward the end of the earnings call, Red Hat CEO Jim Whitehurst described the cloud growth environment as "very, very, very fast growth."

Market conditions and heightened volatility could stay irrational for longer than expected but leadership stocks are always the last to fall.

If (DBX) can catch a bid, and headway is made on political issues, then jump back into the cloud names that perform like Red Hat and about which I have been beating the drum.

And don't forget that these regulatory and political hindrances all point toward giving big cap tech cozier conditions and an elevated runway from which to operate.

"We know where you are. We know where you've been. We can more or less know what you're thinking about." - said Eric Schmidt in 2010, the former executive chairman of Google from 2001-2017

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-03-29 01:05:192018-03-29 01:05:19Technology's Upside in the Trade War

Come join me for lunch at the Mad Hedge Fund Trader's Global Strategy Update, which I will be conducting in New York, NY, on Thursday, June 14, 2018. An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period.

I'll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I'll be throwing a few surprises out there, too. Tickets are available for $278.

I'll be arriving at noon and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive downtown private club. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/Statue-of-Liberty-e1522265320563.jpg293480Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-03-28 15:23:012023-06-28 16:48:58SOLD OUT - Thursday, June 14, 2018 - New York, NY, Global Strategy Luncheon

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.