Global Market Comments

April 30, 2025

Fiat Lux

Featured Trade:

(THE LAZY MAN’S GUIDE TO TRADING),

(ROM), (UXI), (BIB), (UYG)

Global Market Comments

April 30, 2025

Fiat Lux

Featured Trade:

(THE LAZY MAN’S GUIDE TO TRADING),

(ROM), (UXI), (BIB), (UYG)

Mad Hedge Biotech and Healthcare Letter

April 29, 2025

Fiat Lux

Featured Trade:

(BIOTECH’S AWKWARD MIDDLE CHILD)

(GILD), (VRTX), (AMGN), (BMY)

Well, folks, I've been trading biotech stocks since before most of today's analysts had their first internships.

After countless dinners with pharma execs and more investor conferences than I care to remember, there's one thing I've learned about this sector – these stocks are a lot like the experimental drugs themselves: sometimes miraculous, sometimes disappointing, and always requiring patience.

That brings us to Gilead Sciences (GILD), which has recently pulled off the financial equivalent of finding a $100 bill in an old jacket: a 90% gain since May 2024.

If you're an income-focused investor eyeing GILD's promising yield like a prospector spotting gold, I'd suggest taking a breath before you stake your claim.

After diving into this company's financial innards with the ruthless precision of a veteran hedge fund manager, I've uncovered some fascinating contradictions.

First off, GILD has undergone a remarkable transformation, shedding its growth-focused biotech skin to become what I call a "mature dividend machine" – offering 9 consecutive years of dividend increases since 2015.

Its current annual dividend of $3.16 per share yields 2.99%, significantly outpacing the biotechnology sector average of 1.92%. Not too bad for a company that cut its teeth on groundbreaking HIV and COVID treatments.

But here's where things get interesting. Despite GILD's revenue looking as seasonal as a summer blockbuster (with predictably lower earnings in the first half of each year), the company's fundamentals show troubling signs beneath the surface.

While Q1 2025 revenue was expected to land around $6.77 billion, the company's economic profitability has fallen off a cliff since 2024. Blame it on negative net income in early 2024 and a Cash Tax Rate that jumped from 25.4% to 30.6% faster than a trader fleeing a market crash.

The historical performance tells an even more sobering tale. From IPO to 2015, GILD delivered average annual returns of 32.25% in 79% of years – performance that would make even the most jaded investor whistle.

But since 2015? The stock managed profits in only 50% of years with an anemic average return of 0.99%, which translates to a 2.17% loss when adjusted for inflation. Ouch.

You might say that the entire sector's going through a rough patch these days, and I would have agreed with you except there are several biotechs still performing well.

Take Vertex Pharmaceuticals (VRTX). Those guys are up 36.7% over the past 52 weeks.

Or consider Amgen (AMGN), whose dividend is growing at a mouth-watering 8.94% annually over five years – nearly triple what GILD is serving up to its shareholders.

Even BioMarin (BMRN), a company most retail investors couldn't pick out of a lineup, has been quietly crushing it with 27.3% revenue growth while GILD's top line moves sideways like a crab with performance anxiety.

And don't get me started on Bristol Myers Squibb (BMY). Despite facing their own patent cliff dramas, they're maintaining a forward P/E of just 7.2 – practically giving away shares – while offering a dividend yield of 4.7%.

So, let me tell you something the glossy investor presentations won't: GILD's forward P/E ratio of 13.35x looks attractively cheap compared to the healthcare sector's 20.13x and the S&P 500's 18.60x.

After having had drinks with several institutional investment managers last week, though, I can assure you that discount exists for a reason.

The smart money has correctly identified that this company is no longer growing profitably, and certain whispers about their pipeline aren't inspiring confidence.

For dividend investors hoping to beat inflation while preserving capital, GILD presents a mixed bag. The dividend growth continues but remains stubbornly below inflation, creating a slow leak in real returns.

And, look, I know the Trump White House isn't exactly making life easy for companies like Gilead. Over whiskey last month with a former FDA bigwig (who shall remain nameless), I heard some concerning murmurs about potential cuts to HIV prevention programs.

Bad news when you're sitting on 40% of the U.S. PrEP market like GILD is.

Bottom line? I'm sticking with "hold" for now. The smart money moves when the smart money knows, and my Rolodex isn't flashing buy signals yet.

I've watched enough biotech darlings flame out to know that patience outperforms panic every time.

When GILD shows signs of recapturing that pre-2014 magic, you'll hear it from me before the CNBC talking heads catch wind of it.

Global Market Comments

April 29, 2025

Fiat Lux

Featured Trade:

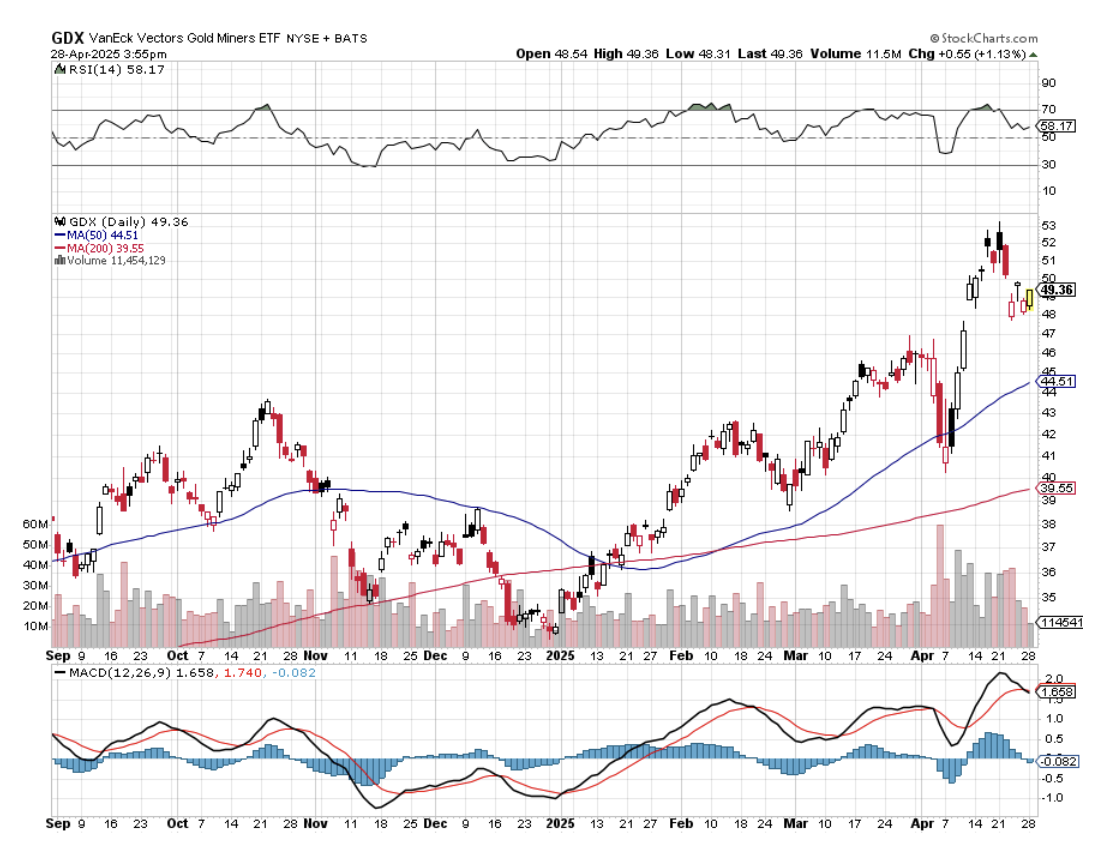

(THE NEXT THING FOR THE FED TO BUY IS GOLD)

(GLD), (GOLD), (GDX), (NEM)

A huge new buyer may eventually enter the gold market.

That could be a year off, maybe two, or three at the most.

I’ll give you a hint who: your taxes will pay for it.

If true, it could send the price of the barbarous relic soaring above $5,000, or even $50,000 an ounce, a target long led by the tin hat Armageddon crowd.

When I spoke to a senior official at the Federal Reserve the other day, I couldn’t believe what I was hearing.

If the American economy moves into the next recession with rising inflation, a near certainty, its hands will be tied. It dare not cut rates for fear of further fanning the flames.

At that point, our central bank’s primary tool for stimulating US businesses will become utterly useless, ineffective, and impotent.

What else is in the tool bag?

How about large-scale purchases of Gold (GLD)?

You are probably as shocked as I am by this possibility. But there is a rock-solid logic to the plan. As solid as the vault at Fort Knox.

The idea is to create asset price inflation that will spread to the rest of the economy. It already did this with great success from 2009-2014 with quantitative easing, whereby almost every class of debt securities was hoovered up by the government.

“QE on steroids” would involve large-scale purchases of not only gold, but stocks, government bonds, and exchange-traded funds as well.

If you think I’ve been smoking California’s largest cash export (it’s not almonds), you would be in error. I should point out that the Japanese government is already pursuing QE to this extent, at least in terms of equity-type investments.

And, as the history buff that I am, I can tell you that it has been done in the US as well, with tremendous results.

If you thought that President Obama had it rough when he came into office in 2009, it was nothing compared to what Franklin Delano Roosevelt inherited.

The country was in its fourth year of the Great Depression. US GDP had cratered by 43%, consumer prices had crashed by 24%, the unemployment rate was 25%, and stock prices had vaporized by 90%.

Mass starvation loomed.

Drastic measures were called for.

FDR issued Executive Order 6102 banning private ownership of gold, ordering citizens to sell their holdings to the US Treasury at a lowly $20.67 an ounce.

He then urged Congress to pass the Gold Reserve Act of 1934, which instantly revalued the government’s holdings at $35.00, an increase of 69.32%. These and other measures caused the value of America’s gold holdings to leap from $4 to $12 billion.

Since the US was still on the gold standard back then, this triggered an instant dollar devaluation of more than 50%. The high gold price sucked in massive amounts of the yellow metal from abroad creating, you guessed it, inflation.

The government then borrowed massively against this artificially created wealth to fund the landscape-altering infrastructure projects of the New Deal.

It worked.

During the following three years, the GDP skyrocketed by 48%, inflation eked out a 2% gain, the unemployment rate dropped to 18%, and stocks jumped by 80%. Happy days were here again.

However, in the 21st-century version of such a gold policy, it is highly unlikely that we would see another gold ownership ban.

Instead, the Fed would most likely move into the physical gold market, sitting on the bid for years, much like it did in the 2010s Treasury bond market for five years. Gold prices would increase by a multiple of current levels.

It would then borrow against its new gold holdings, plus the 4,176 metric tonnes worth $40 billion at today’s market prices already sitting in Fort Knox, to fund a multibillion-dollar tax cut.

Yes, this all sounds like a fantasy. But negative interest rates were considered an impossibility only a few years ago.

The Fed’s move on gold would be only one aspect of a multi-faceted package of desperate last-ditch measures to resuscitate the economy at some point in the future. The time to start buying gold is RIGHT NOW!

Persistent urban legends and Internet rumors claim that the vault is actually empty or filled with fake steel bars painted gold.

That is, until Treasury Secretary Steven Mnuchin visited the vault on his way to view the solar eclipse at government expense in August 2017.

He says the gold is still there. But only if you believe Steve Mnuchin. A lot don’t.

We’ll never know for sure. Visitors are not allowed.

(GLW), (LUMN), (T)

While cruising down Highway 1 last weekend, I received a call from an old friend who runs one of America's largest data centers. He sounded unusually animated, almost giddy.

"John, you wouldn't believe what's happening with our fiber requirements," he said, nearly shouting over the roar of his Tesla. "We're ordering three times more optical cable than last year, and we still can't keep up with demand."

Why the sudden surge? Two letters: AI.

If you thought the AI revolution was just about software, think again. That intelligence needs a nervous system, and Corning Incorporated (GLW) is perfectly positioned to be the backbone supplier of that infrastructure.

The numbers back this up. In Q4 2024, Corning's optical communications segment saw sales jump a stunning 93% year-over-year. Not a typo - ninety-three percent. This wasn't some fluke quarter either.

For the full year, the segment grew 16%, pushing revenue to $4.66 billion and making it Corning's largest business by sales.

I've been following Corning since my days in Japan in the 1970s when they were pioneering fiber optics. Back then, the technology seemed almost magical - glass strands carrying phone calls.

Today, these same glass threads (albeit vastly improved) are what's enabling AI to function at scale.

Let me break it down. Modern AI systems require absurd amounts of GPU computing power. These processors generate tremendous heat and need to communicate with each other at lightning speed. The faster the speed required, the more fiber connections you need.

It's a perfect storm for Corning.

The company's management team clearly recognizes the opportunity. They've launched what they call their "Springboard Plan" targeting over $4 billion in revenue and 20% operating margins by 2026.

The optical communication segment alone is projected to grow at a 30% CAGR through 2027. For context, the long-term average growth rate for the S&P 500 is 3%.

If you’re still not convinced, let's look at who's buying.

Lumen (LUMN) recently inked a deal to have Corning supply 10% of its global fiber optics for the next two years. AT&T (T) signed a deal worth over $1 billion in late 2024.

When telcos are throwing around billions, you know something significant is happening.

And Corning isn't just talking - they're innovating to meet the moment. In March, they launched their GlassWorks AI Solutions, which can dramatically increase data throughput. Their fiber enables 2-4 times more capacity in existing conduits.

That's crucial because nobody wants to tear up streets to lay new pathways if they can avoid it.

What I find particularly attractive about Corning is that it's not a one-trick pony. Yes, optical communications is driving growth, but the company has diversified segments in display glass, life sciences, automotive, and specialty materials. These provide steady cash flow that can fund R&D and growth initiatives.

In other words, Corning can place big bets on the AI revolution without betting the farm.

The latest earnings report confirms this financial strength. Q4 2024 sales jumped 18% year-over-year to $3.9 billion, but even more impressive was the EPS increase of 46% to $0.57.

Profitability is accelerating faster than revenue - the holy grail for any corporation. Free cash flow hit $1.25 billion for 2024, up a hefty 42% from the previous year.

All this would be moot if the stock was outrageously expensive, but it's not.

Corning trades at a forward P/E of 18.30x, slightly below the sector median of 19.04x and in line with the broader S&P 500 at around 18x.

The forward PEG ratio of 1.12x represents a 21.46% discount to the sector median of 1.42x, suggesting the market hasn't fully priced in Corning's growth potential.

There are risks, of course.

As a global supplier, Corning could face headwinds from President Trump's tariffs and ongoing US-China trade tensions. This could impact both demand for their products in China and the cost of raw materials.

But with 170 years of business experience, Corning has weathered far worse storms.

I remember visiting Corning's headquarters in upstate New York back in the 1980s when I was covering technology for a major business magazine. What struck me was their combination of cutting-edge science with old-school manufacturing discipline.

That culture persists today, and it's exactly what's needed to capitalize on the AI infrastructure boom.

So is Corning a worthwhile investment? At its current price, it offers an attractive risk/reward profile for long-term investors. I suggest you buy the dip.

Mad Hedge Technology Letter

April 28, 2025

Fiat Lux

Featured Trade:

(GOOGLE GIVES US SOME GOOD NEWS)

(GOOGL), (NVDA)

I am not saying that Google’s (GOOGL) earnings report will save the market; the market isn’t just GOOGL.

However, the company demonstrated there is still some positive performance out there in the tech sector when many out there are having a hard time.

It is clear that we are about to embark on a journey where big tech actively pulls the levers of shareholder returns to get over the low bar of expectations.

It is true that Google has not innovated for years and is still relying on its cash cow called the Google search engine, to drive ad revenue.

At some point, there will be competition as proprietary technology becomes beatable.

Competition is prompting the company and its rivals to spend heavily on infrastructure, research, and talent. While Google benefits from AI startups spending on its cloud and business tools, it’s also racing to present an answer to popular conversational AI chatbots, which consumers are beginning to think of as an alternative to using Google Search.

Google’s beginning of the answer to that threat — its “AI Overviews” and “AI Mode” in search, in which summarized responses are drafted by generative AI and highlighted ahead of Google’s web links — have seen mixed success. Meanwhile, Google’s AI changes to search have decimated traffic to independent websites across the open web.

Google Cloud brought in an operating profit of $2.18 billion, indicating that Google may be nudging out more profits from Cloud even as sales slow.

The cloud unit is so far the clearest indicator of how the AI boom is contributing to the company’s sales, as startups that require more computing power for their work become customers. Though Google Cloud still lags in third place behind Amazon and Microsoft offerings, it’s one of Alphabet’s most important growth areas.

Alphabet’s board authorized a $70 billion share buyback and boosted its dividend by 5%, to 21 cents a share.

With Google’s search business still holding up at a tough time in global business, I must conclude that Google is doing better than expected.

I believe that we will see a consolidated trend in 2025 of big tech dipping into their huge cash reserves to give back returns to shareholders. Google increasing its dividend by 5% is just the beginning, and we expect bigger returns as we move to the latter part of the year.

There is nowhere to invest in innovation right now in technology, which is why management is quick to buy back stock.

If there is some great project out there, management is keeping it close to its vest.

The long-term problem is that when you fire all the Americans with high wages who secured the company’s success to this point, replacing Americans with cost-cutting employees from India won’t deliver the same amount of innovation as the past in a mature environment.

American tech is supposed to set the bar in innovation, and now they are no,t which is why China is rapidly catching up to Americans on all cutting-edge technology, whether it be EVs or chip manufacturing.

Google is no longer a growth company, and that hurts the stock price.

We could experience a bear market rally that could propel Google along, but that depends on the whims of global politics, which Google has no control over.

If you look at the risk/reward scenario, Google is worth a bullish trade after the wild pullback.

(THE “SELL AMERICA” THREAD HAS TAKEN HOLD)

April 28, 2025

Hello everyone

WEEK AHEAD CALENDAR

MONDAY, APRIL 28

10:30 a.m. Dallas Fed Index (April)

Earnings: Universal Health Services, Domino’s Pizza

TUESDAY, APRIL 29

8:30 a.m. Wholesale Inventories preliminary (March)

9:00 a.m. FHFA Home Price Index (February)

9:00 a.m. S&P/Case Shiller comp. 20 HPI (February)

9:30 a.m. Australia Inflation Rate

Previous: 2.4%

Forecast: 2.2%

10:00 a.m. Consumer Confidence (April)

10:00 a.m. JOLTS Job Openings (March)

Earnings: Visa, Seagate Technology Holdings, Starbucks, Mondelez International, PPG Industries, First Solar, Extra Space Storage, Caesars Entertainment, Booking Holdings, Sysco, Corning, Sherwin-Williams, Altria Group, Kraft Heinz, Coca-Cola, American Tower, Pfizer, Regeneron Pharmaceuticals, Royal Caribbean Group, General Motors, United Parcel Service, Honeywell International, Hilton Worldwide, PayPal

WEDNESDAY, APRIL 30

8:15 a.m. ADP Employment Survey (April)

8:30 a.m. ECI Civilian Workers (Q1)

8:30 a.m. GDP Chain Price (Q1)

8:30 a.m. GDP first preliminary (Q1)

8:30 a.m. Chicago PMI (April)

10:00 a.m. Core PCE Deflator (March)

10:00 a.m. PCE Deflator (March)

10:00 a.m. Personal Consumption Expenditure (March)

10:00 a.m. Personal Income (March)

10:00 a.m. Pending Home Sales (March)

11:00 p.m. Japan Rate Decision

Previous: 0.5%

Forecast: 0.5%

Earnings: Prudential Financial, MGM Resorts International, Allstate, eBay, Qualcomm, Public Storage, Microsoft, Meta Platforms, Invitation Homes, Albemarle, Aflac, Hess, yum! Brands, Norwegian Cruise Line Holdings, Caterpillar, GE Healthcare Technologies, Stanley Black & Decker, Humana, Generac Holdings, Western Digital, Martin Marietta Materials, Automatic Data Processing

THURSDAY, MAY 1

8:30 Continuing Jobless Claims (04/19)

8:30 a.m. Initial Claims (04/26)

9:45 a.m. S&P PMI Manufacturing final (April)

10:00 a.m. Construction Spending (March)

10:00 a.m. ISM Manufacturing (April)

Earnings: Apple, Motorola Solutions, Live Nation Entertainment, GoDaddy, Airbnb, Monolithic Power Systems, Amazon.com, Ingersoll Rand, DexCom, Kellanova, McDonalds, Howmet Aerospace, Hershey, Quanta Services, KKR & Co, Eli Lilly & Co, Estee Lauder Companies, Moderna, IDEXX Laboratories, CVS Health, Mastercard

FRIDAY, MAY 2

8:30 a.m. Hourly Earnings preliminary (April)

8:30 a.m. Average Workweek preliminary (April)

8:30 a.m. Manufacturing Payrolls (April)

8:30 a.m. Nonfarm Payrolls (April)

Previous: 228k

Forecast: 130k

8:30 a.m. Participation Rate (April)

8:30 a.m. Private Nonfarm Payrolls (April)

8:30 a.m. Unemployment Rate (April)

10:00 a.m. Durable Orders (March)

10:00 a.m. Factory Orders (March)

Earnings: T. Rowe Price Group, Chevron, Exxon Mobil, Apollo Global Management

Since April 2, investors have been trying to see through the noise of a tariffed landscape – which has seemingly toppled the U.S. from its perceived position of power.

“Sell America” is now a theme in the macro landscape. U.S. equities have slumped, the U.S dollar has been pummelled, and bonds have sold off. This has forced investors into a rethink on the U.S. exceptionalism trade in the future.

Hiding away from the volatility is possible – diversify into a mix of short-term bonds, gold, utilities, and consumer staples. Think of stocks like Coca-Cola, Procter & Gamble, Walmart & Costco. Or you could also think about an ETF – Vanguard Consumer Staples ETF (VDC). This ETF holds Walmart & Costco. You could also look at the Swiss franc currency ETF – (FXF).

Last Friday, stocks closed out a winning week. The Dow Jones Industrial Average ended 2.5% higher on the week. The S&P 500 was up by 4.6%, while the Nasdaq Composite rose by 6.7%.

This week will be busy with more than 180 companies in the S&P 500 set to release results. Of those, 11 companies in the Dow Industrials are expected to report, as well as four of the Magnificent Seven companies – Amazon, Apple, Meta Platforms, and Microsoft.

The Mag 7 - not what they used to be –have been well and truly knocked off the top rung of the ladder – and investors would be wise to stop putting all their eggs in that one basket. While these companies are still expected to show strong earnings in 2025, mostly, the rest of the market, that is, the other 493 S&P 500 companies, are expected to post double-digit earnings growth next calendar year, catching up to the mega cap leadership.

On Wednesday, the Federal Reserve’s preferred inflation gauge – the personal consumption expenditure price index – is expected to show the annual rate of inflation eased to 2.2% in March from 2.5% in February.

Jobs data will be one to watch this week, as it could start to show signs that the labour market is slowing. Nonfarm payrolls on Friday are projected to show the U.S. added 150,000 jobs in April, down from 209,000 previously, according to FactSet data. The unemployment rate is expected to stay at 4.2%.

MARKET UPDATE

S&P500

The index is near recent highs in the up move from the April 7th low at 4835, breaking above resistance at 5475/85. This is a near-term positive sign and, along with positive technical data, argues for further gains. We can’t be sure yet whether this will be a pattern of limited ranging or a run back to the Feb high at 6147.

Resistance: $5640/50

Support: $5475/85 & $5350/60 & $5185/95

GOLD

Gold has fallen from the April 22 high at $3500. The market was extremely overbought, and this could be the top for at least a few weeks to a month or more. In the short term, there could be more retests towards the high before rolling over.

Resistance: $3367/77 & $3447

Support: $3305/15 & $3257/67 (recent lows) & $3218/28

BITCOIN

There has not really been much change in the big picture view over the last few months. We have seen a large bottoming taking place, with eventual gains above the Jan. peak at 109.40k expected.

The recent rally argues that the final low is likely in place. Bitcoin is now testing resistance at 95.9/96.4k, and this movement could trigger some consolidation for a week or two (not yet confirmed).

On March 17, I suggested several option trades in (IBIT) and (MSTR) that you could enter. A few of these are already in profit, and I expect the rest soon will be.

Further resistance: 98.9/99.4k

Support: 91.3/88.5k

QI CORNER

HISTORY CORNER

On April 28

SOMETHING TO THINK ABOUT

Cheers

Jacquie

Global Market Comments

April 28, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE’S THE BEST-CASE SCENARIO)

(SPY), (TLT), (NFLX), (COST), (NVDA), (TSLA), (MSTR)