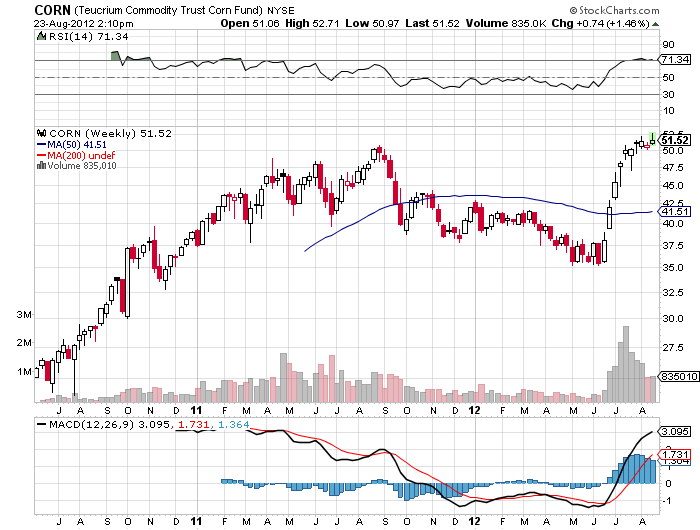

I certainly hope you took my advice to load your portfolio with corn and gold and to dump your equities five years ago. What? You didn?t? Then you have almost certainly suffered on the performance front.

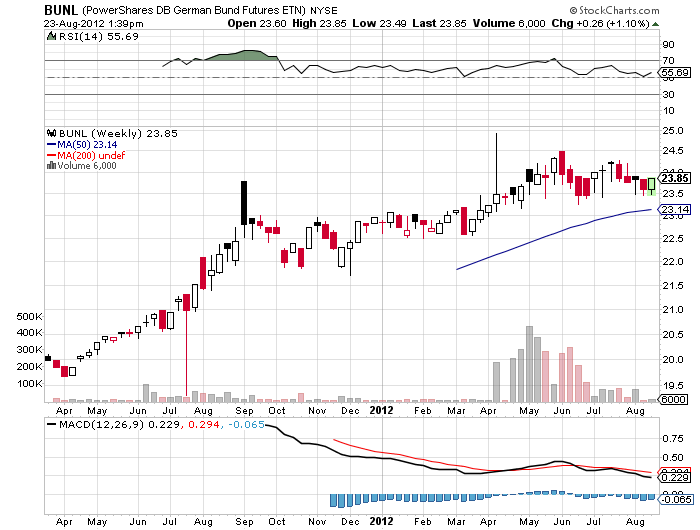

According to data compiled by my former employer, the Financial Times, corn was the top performing asset class since 2007, bringing in a stunning 146% return. Who knew that global warming would be such a winning investment strategy? It was followed by gold (GLD) (144%), US corporate debt (LQD) (44%), US Treasuries (TLT) (38%), and German bunds (BUNL) (26%). This explains why my long gold/short Morgan Stanley (MS) has been going absolutely gangbusters today.

If you ignored my advice and instead loaded the boat with equities, chances are that you are now pursuing a career at McDonalds (MCD), hoping to upgrade to Taco Bell someday. The worst performing asset classes of the past half-decade have been Greek equities (-87%), European banks (-70%), Chinese stocks (-41%), other European equities (-21%), and UK stocks (-11%). If you were in US equities, you are just about breaking even (1%).

Corn is, no doubt, getting an assist from what many are now describing as the worst draught since the dust bowl days of the Great Depression. But there is more to the story than the weather. Empowered with long term forecasts from the CIA and the Defense Department, I have been pounding the table for years that food would become the new distressed asset. These agencies have been predicting that food shortages will become a cause of future wars.

For a start, the world population is expected to increase from 7 billion to 9 billion over the next 40 years. Half of that increase will occur in countries that are net importers of food, largely in the Middle East and Africa. You can also count on the rising emerging nation middle class to increase demand for both the quantity and quality of food. Obesity among children is already starting to become a problem in China.

Managers who have been wrong footed through being overweight equities and underweight bonds will get some respite in coming years. It will be mathematically impossible for government bonds to match their recent performance unless they start charging negative interest rates. My best case scenario has them going sideways to down in the years ahead.

Not so for gold, which will continue to see steady demand from emerging market central banks and their new middle class. Five years ago, gold trading carried a death penalty in China. Today, there are shops on every street corner flogging the latest issue of one ounce Chinese Panda coins.

As for corn, the sky is the limit. If you don?t believe me, try eating a one ounce Chinese Panda.

Is Corn the New Gold?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-23 23:03:582012-08-23 23:03:58The ?Safe? Trade Beats All

The decision by BHP Billiton, one of the world?s largest producers of copper, to postpone its planned $20 billion expansion of its Olympic Dam mine is sounding alarms about the near term state of the global economy. It is telling us that China is slowing faster than we thought, that demand for base metals is shriveling, and that we are anything but close to exiting out current market malaise. This is not good for risk assets anywhere.

The news comes on the heels of a company announcement that earnings would fall from $21.7 billion to $17.1 billion this year. The weakest demand from China in a decade was a major factor. So was the Fukushima nuclear disaster, which dropped prices for uranium, another product of the Olympic Dam mine. Piling on the headaches was a strong Australian dollar, which escalated capital costs. BHP CEO, Marius Kloppers, has said that there will be no new expansion of the company?s capacity approved before mid-2013.

Olympic Dam is the world?s fourth largest copper source and the largest uranium supply. The upgrade was going to involve digging a massive open pit in South Australia that would generate 750,000 tonnes of copper and 19,000 tonnes of uranium a year. Almost the entire output was slated to be shipped to the Middle Kingdom. When Chinese real estate flipped from a ?BUY? to a ?SELL? last year, the days for this expansion were numbered.

I have been following BHP for 40 years, and a number of family members have worked there over the years. So I know it well, and can tell you that their pay and benefits are great. I have used it as a de facto leading indicator and call option on the future of the world economy. When the share price delivers a prolonged multiyear downturn as it has recently done, it is a warning to be cautious and limit your risk.

Hey, I Saw That Parking Place First!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-23 23:02:592012-08-23 23:02:59BHP Cut Bodes Ill for the Global Economy

?Right now, our politics are holding us back. It?s like being the children of permanently divorcing parents. The political environment is a real downer for a lot of people, and their holding back,? said New York Times columnist, Tom Friedman, author of the book, That Used To Be US.

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/children-of-divorced-parents.jpg286400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-23 23:01:102012-08-23 23:01:10August 24, 2012 - Quote of the Day

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2011/10/slider-05-trader-alert.jpg316600Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2012-08-23 10:49:572012-08-23 10:49:57Trade Alert - (GLD) August 23, 2012

During my recent meeting with the senior portfolio managers of the big Swiss banks, I kept hearing the same word over and over: yield, yield, yield! The search for yield by end investors has become so overwhelming that it now trumps all other considerations. So I am starting a series of major pieces on the world?s best yield plays. Those include emerging market debt, REIT?s, master limited partnerships, and junk bonds.

The trick is to enhance your yields without taking insane amounts of risk to get there. In the summer of 2007, investors were accepting vast increases in principal risk in the junk market for a mere 100 basis point increase in interest payments over Treasuries. A year later, that spread exploded to 2,500 basis points. Needless to say, the portfolio managers who made that call are now driving taxis in some of New York?s least attractive neighborhoods.

I have had great luck steering people into the Invesco PowerShares Emerging Market Sovereign Debt ETF (PCY), which is invested primarily in the debt of Asian and Latin American government entities, and sports a generous 4.87%? yield (click here for their site). This beats the daylights out of the one basis point you could earn for cash, the 1.75% yield available on 10 year Treasuries, and still exceeded the 3.98% yield on the iShares Investment Grade Bond ETN (LQD), which buys predominantly single ?BBB?, or better, US corporates.

The big difference here is that PCY has a much rosier future of credit upgrades to look forward to than other alternatives. It turns out that many emerging markets have little or no debt, because until recently, investors thought their credit quality was too poor. No doubt a history of defaults in the region going back to 1820 is in the back of their minds.

You would think that a sovereign debt fund would be the last place to safely park your money in the middle of a debt crisis, but you?d be wrong. (PCY) has minimal holdings in the Land of Sophocles and Plato, and very little in the other European PIIGS. In fact, the crisis has accelerated the differentiation of credit qualities, separating the wheat from the chaff, and sending bonds issues by financially responsible countries to decent premiums, while punishing the bad boys with huge discounts. It seems this fund has a decent set of managers at the helm.

With US government bond issuance going through the roof, the shoe is now on the other foot. Even my cleaning lady, Cecelia, knows that US Treasury issuance is rocketing to unsustainable levels (she reads my letter to practice her English). The ratings agencies have been rattling their sabers about further downgrades of US debt on an almost daily basis, and it is just a matter of time before this, once unimaginable, event transpires again. When it does, there could be a stampede into the debt of other healthier countries, potentially sending the price of (PCY) through the roof.

Since my initial recommendation, my total return on (PCY) has been 50%, not bad for an insurance policy. Money has poured into (PCY, taking assets up nearly tenfold to $2.13 billion over the last four years. Another name to consider in this area is the iShares JP Morgan USD Emerging Markets Bond (EMB)

I lived through the Latin American debt crisis of the seventies. You know, the one that almost took Citibank down? Never in my wildest, Maker?s Mark fueled dreams did I think that I?d see the day when Brazilian debt ratings might surpass American ones. Who knew I?d be trading in Marilyn Monroe for Carmen Miranda?

Time to Trade Her

For Her?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-22 23:03:452012-08-22 23:03:45Reach for Yield With Sovereign Debt

With oil (USO) getting ready to take a run at $100 a barrel once again, the first thing I do when I get up every morning is to curse the oil companies as the blood sucking scourges of modern civilization. I then fall down on my knees and thank goodness that we have the oil companies.

You?ve got to love ExxonMobile (XOM). The world?s largest company announced an unbelievable $127.3 billion in Q2 revenues, generating a gob smacking $15.9 billion in net profits. This year, (XOM) will spend $9.3 billion on exploration and capital spending. Some of their wells easily cost $100 million each. This is why petroleum engineers are getting $100,000 straight out of college, while English and political science majors are going straight on to food stamps.

I recommend (XOM) and other oil majors as part of any long term portfolio. No matter what anyone says, the price of oil goes up, in my lifetime, from $3 a barrel up to $149. The reasons for the ascent keep growing, from the entry of China into the global trading system, to the rapid growth of the middle class in emerging nations. They?re just not making the stuff anymore, and we can?t wait around for more dinosaurs to get squashed.

Oil companies aren?t in the oil speculation business. As soon as a new supply comes on stream, they hedge off their risk through the futures markets or through long term supply contracts. You can find the prices they hedge at in the back of any annual report.

When oil made its big run a few years ago, I discovered to my amazement that (XOM) had already sold most of their supplies in the $20 range. However, oil companies do make huge killings on what is already in the pipeline.

Working in the oil patch a decade ago pioneering the ?fracking? process for natural gas, I got to know many people in the industry. I found them to be insular, God fearing people not afraid of hard work. Perhaps this is because the black gold they are pursuing can blow up and kill them at any time. They are also great with numbers, which is why the oil majors are the best managed companies in the world.

They are also huge gamblers. I swallow hard when I see the way these guys throw around billions in capital, keeping in mind past disasters, like Dome Petroleum, the Alaskan oil spill, Piper Alpha, and more recently, the ill-fated Macondo well in the Gulf of Mexico. But one failure does not slow them down an iota. The ?wildcatting? origins made this a faith based industry from day one, when praying was the principle determinant of where wells were sunk.

Unfortunately, the oil companies are too good at their job of supplying us with a steady and reliable source of energy. They have one of the oldest and most powerful lobbies in Washington, and as a result, the tax code is riddled with favorite treatment of the oil industry. While social security and Medicare are on the chopping block, the industry basks in the glow of $55 billion a year in tax subsidies.

When I first got into the oil business and sat down with a Houston CPA, the tax breaks were so legion that I couldn?t understand why anyone was not in the oil racket. Every wonder why we have had three presidents from Texas over the last 50 years, and looked at a possible fourth last year?

Three words explain it all: the oil depletion allowance, whereby investors can write off the entire cost of a new well in the first year, while the income is spread over the life of the well. This also explains why deep water exploration in the Gulf is far less regulated than California hair dressers.

No surprise then that the industry has emerged in the cross hairs of the debt ceiling negotiations, under the ?loopholes? category. Not only do the country?s most profitable companies pay almost nothing in taxes, they are one of the largest users of private jets.

It is an old Washington nostrum that when things start heading south on the domestic front, you beat up the oil companies. It?s the industry that everyone loves to hate. Cut off the gasoline supply to an environmentalist, and he will be the one who screams the loudest. This has generated recurring cycles of accusatory congressional investigations, windfall profits taxes, and punitive regulations, the most recent flavor we are now seeing.

But imagine what the world would look like if Exxon and its cohorts were German, Saudi, or heaven forbid, Chinese. I bet we wouldn?t have as much oil as we do today, and it wouldn?t be as cheap. Hate them if you will, but at least these are our oil companies. Try jamming a lump of coal into the gas tank of your Prius and tell me what happens.

Love Them, Hate Them or Both?

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/oil.jpg187300DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-22 23:02:202012-08-22 23:02:20Why I Love/Hate the Oil Companies

?Today, 20% of enterprises are using Apple computers on their desktop. For the first time in 30 years, for developers, it is Apple first, not Apple second. This fundamentally changes our investment thesis,? said Ann Winblad of Winblad Hummer Venture Partners.

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/steve-1.jpg286319DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-22 23:01:302012-08-22 23:01:30August 23, 2012 - Quote of the Day

Global Trading Dispatch?s Trade Alert Serviceposted a new all-time high yesterday, clocking a 52.8% return since inception. The 2012 YTD return is now at 12.62%. That takes the average annualized return up to 30.2%, ranking it among the top performing hedge funds in the world. Those happy subscribers who bought my service on May 23 have seen 19 out of 20 trade recommendations turn profitable, reaping a 16.71% gain from my advice.

I really nailed the top of the market on April 2, piling on hefty short positions in the S&P 500 (SPY) and the Russell 2000 (IWM) within a week. Predicting that the conflagration in Europe would get worse, my heavy short in the Euro (FXE), (EUO) was a total home run. I took in opportunistic profits trading the Japanese yen (FXY), (YCS) and the Treasury bond market (TLT) from the short side. I was then able to lock in these profits by covering all of my shorts within 60 seconds of the May 28 market bottom.

In June, I caught almost the entire move up with a portfolio packed with ?RISK ON? trades. I picked up Apple (AAPL) at $530 for a rapid $50 gain. I seized the once in a lifetime opportunity to buy JP Morgan (JPM) at a 40% discount to book value, picking up shares at $31, correctly analyzing that the ?London Whale? problem was confined and solvable.

My long position in Walt Disney (DIS) performed like the park?s ?Trip to the Moon? ride. While Hewlett Packard (HPQ) fell a disappointing 5% on me, I was able to add 140 basis points to my performance through time decay on an options position. The latest performance pop came from the recent surge in gold (GLD) and Apple, my two largest positions.

My satisfaction in all of this comes from the knowledge that thousands of followers are making money in the markets that never would otherwise. I am protecting them from getting ripped off by the sharks on Wall Street with their conflicted and indifferent research.

I am expanding their understanding of not just financial markets, but the world at large. And I am doing this during some of the most difficult trading conditions in history. Only 11% of hedge funds have managed to beat the S&P 500 since January 1.

The roster of winning closed trades is below. This doesn?t include the seven unrealized profitable positions still in my portfolio:

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011. The service includes my Trade Alert Service, daily newsletter, real-time trading portfolio, an enormous trading idea database, and live biweekly strategy webinars. To subscribe, please go to my website at www.madhedgefundtrader.com, find the ?Global Trading Dispatch? box on the right, and click on the lime green ?SUBSCRIBE NOW? button.

Trade Alert Service Since Inception

Thanks Again Steve

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-21 23:04:032012-08-21 23:04:03Gold Surge Pushes Trade Alert Service to New All Time High

Much of the fury in this morning?s nearly 60 point ?melt up? opening in the Dow was generated by hedge funds panicking to cover shorts. Convinced of the imminent collapse of Europe, the impotence of governments, and the death spiral in sovereign bonds, many managers were running a maximum short position at the opening, and for the umpteenth time, were forced to cover at a loss. Meet the new dumb money: hedge funds.

When I first started on Wall Street in the seventies, you heard a lot about the ?dumb money.? This was a referral to the low end retail investors who bought the research, hook-line-and-sinker, loyally subscribed to every IPO, religiously bought every top, and sold every bottom.

Needless to say, such clients didn?t survive very long, and retail stock brokerage evolved into a volume business, endlessly seeking to replace outgoing suckers with new ones. When one asked ?Where are the customers? yachts,? everyone in the industry new the grim answer.

Since the popping of the dot-com boom in 2000, the individual investor has finally started to smarten up. They bailed en masse from equities, seeking to plow their fortunes into real estate, which everyone knew never went down. Since 2007, the exit from equities has accelerated.

Although I don?t have the hard data to back it, I bet the average individual investor is outperforming the average hedge fund in 2012 by a large margin. With such heavy weightings of bonds, including the municipal, corporate, and government flavors, how could it be otherwise? While the current yields are miniscule, the capital gains have to be humongous this year, with Treasury yields plunging from 4% to 1.38% in the last two years alone.

This takes me back to the Golden Age of hedge funds during the 1980?s. For a start, you could count the number of active funds on your fingers and toes, and we all knew each other. The usual suspects included the owl like Soros, the bombastic Robertson, steely cool Tudor-Jones, the nefarious Bacon, the complicated Steinhart, of course, myself, and a handful of others.

The traditional Wall Street establishment viewed us as outlaws, and believed that if the trades we were doing weren?t illegal, they should be, like short selling. Investigations and audits were a daily fact of life. It wasn?t easy being green. I believe that Steinhart was under investigation during his entire 40 year career, but the Feds never brought a case.

It was worth it, because in those days, if you did copious research and engaged in enough out of the box thinking, you could bring in enormous profits with almost no risk. I used to call these ?free money? trades. To be taken seriously as a manager by the small community of hedge fund investors you had to earn 40% a year or you weren?t worth the perceived risk. Annual gains of 100% were not unheard of.

Let me give you an example. In 1989, you could buy a leveraged warrant on a Japanese stock near parity, for $100, that gave you the right to own $500 worth of stock. You bought the warrant and sold short the underlying stock. Overnight yen yields then were at 6%, so 500% X 6% = 30% a year, your risk free return. Most Japanese stock dividends were near zero then, so the cost of borrowing was almost nothing. If the stock then fell, you also made big money on your short stock position. This was not a bad portfolio to have in 1990, when the Nikkei stock index plunged from ?39,000 to ?20,000 in three months, and some individual shares dropped by 80%.

Trades like this were possible because only a smaller number of mathematicians and computer geeks, like me, were on the hunt, and collectively, we amounted to no more than a flea on an elephant?s back. Today, there are over 10,000 hedge funds managing $2.2 trillion, accounting for anywhere from 50% to 70% of the daily volume.

Many of the strategies now can only be executed by multimillion dollar mainframe computers collocated next to the stock exchange floor. Winning or losing trades are often determined by the speed of light. And as the numbers have expanded exponentially from dozens to hundreds of thousands, the quality of the players has gone down dramatically, with copycats and ?wanabees? crowding the field.

The problem is that hedge funds are no longer peripheral to the market. They are the market, and therein lies the headache. How are you supposed to outperform the market when it means beating yourself? As a result, hedge fund managers have replaced the individual as the new ?dumb money, buying tops and selling bottoms, only to cover at a loss, as we witnessed today.

The big, momentum breakout never happens anymore. This is seen in hedge fund returns that have been declining for a decade. The average hedge fund return this year is a scant 2.2%, compared to 13% for the S&P 500. Fewer than 11% of hedge fund managers our outperforming the index, or a simple index fund. Make 10% now and you are a hero, especially if you are a big fund. That hardly justifies the 2%/20% fee structure that is still common in the industry.

When markets disintegrate into a few big hedge funds slugging it out against each other, no one makes any money. I saw this happen in Tokyo in the 1990?s, when hedge funds took over the bulk of trading. Volumes shrank to a shadow of their former selves, and today, Japan has fallen so far off the radar that no one cares what goes on there. Japanese equity warrants ceased trading by 1994.

How does this end? We have already seen the outcome; that investors flee markets run by hedge funds and migrate to those where they have less of an impact. That explains the meteoric rise of trading volumes of other assets classes, like bonds, foreign exchange, gold, silver, and other hard assets.

Hedge funds are left on their own to play in the mud of the equity markets as they may. This will continue until hedge fund investors start departing in large numbers and taking their capital with them. The December redemption notices show this is already underway. Just ask John Paulson, who has one of his funds down 20% year to date, again.

How About 2% and 20%?

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/dumb.jpg240320DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-21 23:02:582012-08-21 23:02:58Hedge Funds: The New Dumb Money

?Rock stars get room keys. I get business cards,? said New York Times columnist, Tom Friedman, and author of the book, That Used To Be US.

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/meishi.jpg213320DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-21 23:01:392012-08-21 23:01:39August 22, 2012 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.