“2024 will be the fourth year of living dangerously,” said Ed Yardeni of Yardeni Research.

“2024 will be the fourth year of living dangerously,” said Ed Yardeni of Yardeni Research.

Mad Hedge Biotech and Healthcare Letter

April 9, 2024

Fiat Lux

Featured Trade:

(A PHARMA TORTOISE IN A MARKET FULL OF HARES)

(JNJ)

For the thrill-seekers who get a kick out of watching industries move faster than a cat on a hot tin roof, riding the wave of trending growth stocks might be for you.

But for those who prefer a good night's sleep over night sweats about market swings, pinning down stocks that promise a smooth sail towards retirement is the name of the game.

Now, if I were to put my money on one sector that's as steady as they come, I'd bet the farm on healthcare.

Why, you ask? Well, let’s take a look at the numbers.

U.S. healthcare spending ballooned to a jaw-dropping $4.5 trillion in 2022. That’s $13,493 for every man, woman, and child. With an army of about 10,000 baby boomers daily marching into Medicare eligibility, it's a safe bet this number's on a one-way trip up.

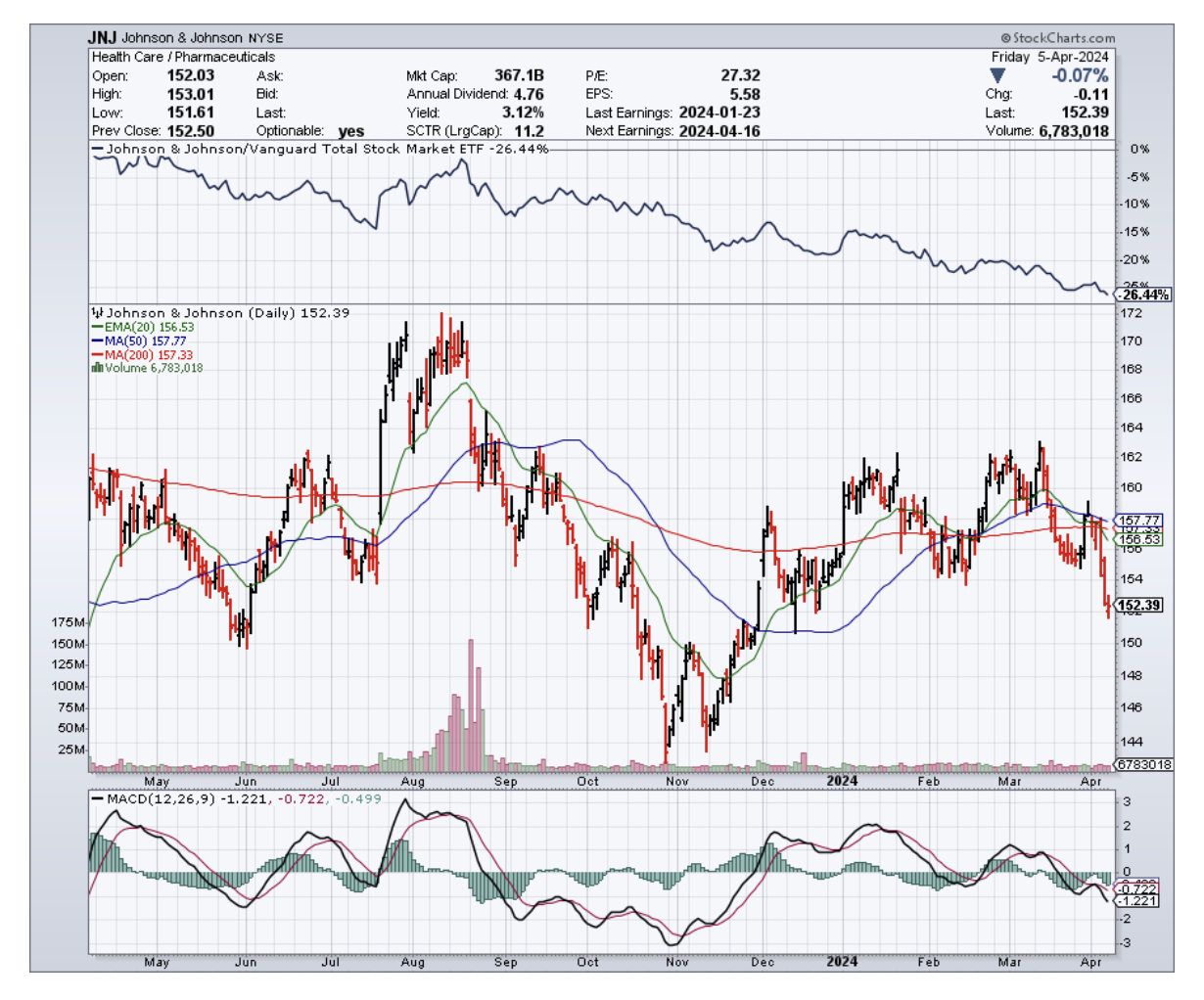

Let’s talk about a healthcare giant arena that might not make you rich overnight, but it's a dividend machine you can count on: Johnson & Johnson (JNJ).

Think of J&J as the responsible older sibling of your portfolio. They recently raised their dividend for the 61st year in a row. That's a 3.1% yield right now – a pretty good return for such a dependable company.

Over the past five years, J&J’s payout has beefed up by over 25%. Quite the feat, especially considering it just slimmed down by spinning off its consumer health division.

This strategic move has made J&J a lean, mean, dividend-paying machine. They're now laser-focused on their core businesses: med tech and pharmaceuticals.

This focus is paying off – they raked in a sweet 11.1% jump in adjusted earnings in 2023. With dividends sitting pretty at $4.76 a share and a clear path for growth, this blue chip just keeps getting better.

But J&J's not just a big fish in the healthcare pond – it's practically the whole ocean. They hauled in a jaw-dropping $85.2 billion in revenue last year. This company has a decades-long track record of turning its massive size into consistent growth for shareholders.

Case in point: J&J just made a big power play, grabbing Shockwave Medical (SWAV) for a cool $13.1 billion.

Not bad for a company that clearly loves shopping for heart-focused companies – remember when they scooped up heart device maker Abiomed for $16.6 billion in 2022? This latest acquisition isn't just about beefing up their medical device game. It's their ticket to dominating the cardiovascular space.

But, J&J's not content with just hearts; they're setting their sights on robot-assisted surgery with their new Ottava device.

Sure, they might be playing catch-up to Intuitive Surgical (ISRG), but think about it: barely any surgeries use robots right now. This market has potential written all over it

Of course, it's not all sunshine and roses in the land of Big Pharma. J&J's had its share of courtroom battles and regulatory headaches, just like any mega-corporation.

But they've weathered the storm, and their credit rating is better than Uncle Sam's. That shows a kind of resilience you just can't fake.

In today's volatile market, it's easy to get swept up in the hype of flashy, high-risk stocks – the hares of the investing world. But what if true wealth lies in the slow and steady pace of the tortoise?

In the pharma world, J&J is proof that slow and steady progress, unwavering reliability, and a continuous effort to innovate are the secrets to long-term success. They might not be the flashiest stock, but their steady march of growth and consistent dividends make them a quiet force in the pharma world.

So the next time you're tempted to chase the latest market fad, remember the pharma tortoise – and consider adding a reliable blue-chip like J&J to your portfolio. If you see a dip, don't hesitate, buy it.

Global Market Comments

April 9, 2024

Fiat Lux

Featured Trade:

(APRIL 23 HAVANA CUBA STRATEGY LUNCHEON)

(My Favorite Passive/Aggressive Portfolio)

(ROM), (UYG), (UCC), (DIG), (BIB)

Come join me for lunch for my Global Strategy Luncheon, which I will be conducting in Havana Cuba at 12:00 PM on Tuesday, April 23, 2024. A three-course lunch is included.

I’ll be giving you my up-to-date view on stocks, bonds, currencies commodities, precious metals, and real estate.

And to keep you in suspense, I’ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $219.

I’ll be arriving early and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at one of Earnest Hemingway’s favorite bars in Old Havana. US Relations with Cuba have run hot and cold over the years and now it is possible for me to make this trip so I thought I’d jump at the chance.

Only bring cash in $1 denominations as credit cards are not accepted in Fidel Castro’s worker paradise and there is no change. Nor is there any cell phone coverage. And drink anything but bottled water on pain of death. And bring your own toilet paper and toilet seat as none are available in public restrooms.

Hopefully, the Cuban Air Force won’t shoot me down on the way to Havana as they have done with others in the past as I will be flying my own plane. But if I am, don’t worry. I got an “A” in Ditching at Sea in flight school and am bringing a friend with two very ample flotation devices.

I look forward to meeting you and thank you for supporting my research.

To purchase tickets for this luncheon, please click here.

Mad Hedge Technology Letter

April 8, 2024

Fiat Lux

Featured Trade:

(BRANCHING OUT)

(INTC), (MSFT)

Intel (INTC) is an intriguing chip company that has been around for a long time but has seldom been at the vanguard of the tech movement.

Until now…

Remember the US government is pouring dollars at the tune of billions upon billions into the domestic semiconductor industry to maintain a competitive advantage that is quickly being challenged by China.

Intel could solidify itself as a real tech player if it can figure out the foundry business which has been largely ineffective as of late.

Even if the foundry business is a big-time loss maker right now, Intel is laying the groundwork to become a strategically important company to the US government and US tech industry in 5 years.

Government dollars are usually viewed as a more stable stream of revenue.

It’s true that Intel is better known for designing its own chips, but that type of barrier to entry isn’t as high as foundry production.

Many chip companies aren’t interested in the production of what they design, because of the capital-intensive nature of the process.

It’s easier to outsource designs and just collect the product after.

Intel shares fell 4% last Tuesday after the company revealed long-awaited financials for its semiconductor manufacturing business or foundry business.

Intel said its foundry business recorded an operating loss of $7 billion in 2023 on sales of $18.9 billion. That’s a wider loss than the $5.2 billion Intel reported in its foundry business in 2022 on $27.5 billion in sales.

It has been pitching investors to double down on an external foundry business to make chips for other companies.

In theory, it sounds promising.

Intel’s role as one of the only U.S. companies doing cutting-edge semiconductor manufacturing on American soil was a big reason it secured nearly $20 billion in CHIPS and Science Act funding last month.

Its management said that it expected its foundry’s losses to peak in 2024 and eventually break even “midway” between this quarter and the end of 2030.

The company previously said that Microsoft (MSFT) would use its foundry services and that it has $15 billion of revenue for the foundry already booked.

The foundry business at Intel will ostensibly drive larger revenue momentum each approaching year to 2030.

Granted, it doesn’t take one day for chip production to come online, but the contract signed with Microsoft is a positive signal that will likely lead to other behemoths inking deals.

Intel even admitted that the lack of profitability in the foundry business from the past was correctable through better focus and execution.

I do believe Intel morphing into a multi-dimensional chip company is highly supportive of a higher share price only if they can get a handle on expense control.

Many times companies go too big with the government subsidies and need even more subsidies to dig themselves out of a hole.

I don’t believe that will be the case with Intel’s foundry business and installing a concrete plan has gone a long way to soothe investor fear.

The stock was crushed in 2020 and hit a nadir of $25 per share in 2023.

Intel shares then reversed and doubled to around $50 per share.

They have now settled in the high $30 range and I do believe any dips should be bought and held long-term.

(MARKETS HAVE A LOT OF DATA TO DIGEST THIS WEEK)

April 8, 2024

Hello everyone,

Week ahead calendar

Monday, April 8

Switzerland Unemployment Rate

Previous: 2.4%

Time: 1:45 am

Tuesday, April 9

6 a.m. NFIB Small Business Index (March)

Japan Consumer Confidence

Previous: 39.1

Time: 1:00 am

Wednesday, April 10

8:30 a.m. Consumer Price Index (CPI) (March)

8:30 a.m. Hourly Earnings final (March)

8:30 a.m. Average Workweek final (March)

10 a.m. Wholesale Inventories final (February)

2:00 p.m. Treasury Budget NSA (March)

2:00 p.m. FOMC Minutes

Earnings: Delta Air Lines

Thursday, April 11

8:30 a.m. Continuing Jobless Claims (3/30)

8:30 a.m. Initial Claims (04/06)

8:30 a.m. Producer Price Index PPI

Euro Area Interest Rate Decision

Previous: 4.5%

Time: 8:15 am

Earnings: CarMax

Friday, April 12

8:30 a.m. Export Price Index (March)

8:30 a.m. Import Price Index (March)

10 a.m. Michigan Sentiment preliminary (April)

UK GDP Growth Rate

Previous: -0.3%

Time: 2:00 am

Earnings: State Street, Wells Fargo, JPMorgan Chase, Progressive, Citigroup

Top of mind for investors this week will be inflation numbers that are out on Wednesday. Markets are already digesting rising Treasury yields, so the data could provide an added dose of medicine that the market may love or just really hate.

The numbers will confirm whether we are headed towards the Fed’s 2% target or whether a reassessment or shift is needed on interest rate policy and outlook. Even if March numbers are good, investors should still remain cautious about where inflation will sit in the months ahead.

The number of jobs added to the U.S. economy in March was beyond expectations, really highlighting the labour market’s strength. Of significance, however, was the fact that average hourly earnings were in line with forecasts, suggesting that the labour market and the economy as a whole are not overheating. Currently, the CME Fed Watch Tool shows markets are pricing in three rate cuts this year, starting in June. Wait for the data; it will tell a story.

The markets are feeling brittle about yields, and any further negative data could tip us into a little more volatility, and more of a correction here.

Rising Treasury yields and higher oil prices saw the DJIA close lower by 2.3% last week. West Texas Intermediate crude oil futures topped $87 a barrel last week, reaching a five-month high. The 10-year Treasury yield hit 4.4% last Friday.

Despite these readings, many investors remain optimistic that stocks can continue to rally, citing a broadening out in the rally – meaning that it is not just the tech sector leading the rally, but a participation of all sectors – and a strong economy, which are constructive signals for markets.

The market’s “Bigger Picture” outlook remains Bullish. We would need to see a strong break below 5,140 to signal a deeper retracement back towards the 4990 area.

The uptrend in Gold and Silver remains in progress, and we are awaiting a breakout from a symmetrical triangle in Bitcoin, with a target of around $82,000.

Cheers,

Jacquie

Global Market Comments

April 8, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WINDFALL YEAR),

(FCX), (TLT), (TSLA), (NVDA), (FCX),

(XOM), (WPM), (GLD), (CCJ), (META), (AMZN),

(AN EVENING WITH TRAVEL GURU ARTHUR FROMMER)

This year seems to be the year of the windfall.

In January, we loaded up on Big Tech (AMZN), (MSFT), which then went ballistic.

In February, we doubled up on NVIDIA (NVDA), which then nearly doubled.

In March, spotting the shift into commodities, energy, and precious metals we loaded the boat with gold Freeport McMoRan (FCX), gold (GLD), silver (WPH), and oil (XOM), (OXY), which launched into torrid two-week straight up moves which continue. And for good measure, we dove into NVIDIA one more time.

Even the trades I thought about and talked about but never executed took off like a scalded chimp, such as uranium producer Cameco (CCJ), up 30% in weeks.

And while you’d think that trades like this would generate the performance of a lifetime, in fact, I begrudgingly admit I'm lagging behind the index this year. It’s incredibly annoying when after working 12 hours a day seven days a week, the indexers, the investors who sit on their hands all day and do nothing, are making more money than I am.

That’s because I put out a handful of ill-timed short positions in the S&P 500 (SPY) and Freeport McMoRan (FCX) which cut my numbers by half.

You may ask why I suffered the madness of putting out shorts when we are in a bull market and that everything is going straight up every day! That’s because I am the Mad Hedge Fund Trader, not the Mad Long-Term Investor. And hedge funds are always supposed to have balanced longs and shorts. I can tilt this by keeping only one short position against a basket of longs. But even those single longs have proved painfully expensive.

The issue here is that the market is not breathing as it normally does. There is no ebb and flow to let you in and out of positions. Sectors flatline, then launch into bull moves that take them up almost every day for months. That is an impossible market to trade.

I have only seen this twice during my lifetime: during the Great Japanese Stock Bubble of the 1980s and the Dotcom Bubble of the 1990s, which means we are in another one of these great bubbles, which will probably be the last of my lifetime.

The previous two great bubbles went on for five years. Greed can last a long time. If you count the October 26, 2023 low as the start of the new bull market, we have 4 ½ years to run in this one. What is more likely is that the pandemic low in April of 2020 was the start of this new bull market and we have averaged a 25% a year return in stocks since then. That means we have at least another year to run…. or more.

Valuations are at the high end of their recent range at 21 times S&P 500 earnings. But during the 1990’s bubble, the market average reached an earnings multiple in the 30s, and technology stocks reached a stratospheric 100 times earnings.

And today, earnings are still rising, sometimes quite sharply, such as the case with (NVDA) and (META). It’s when earnings are falling but stocks are still rising that you have to worry, as happened in 1999 and the first four months of 2000. In the 1980s in Tokyo, nobody ever looked at earnings.

Another frustration with trading today is the collapse of market volatility from $22 to $12 over the past year. That means we are getting paid half of what we were a year ago for the same options trade. You can make up for this loss of volatility by getting more aggressive with strike prices or maturities, but then that increases the number of stop losses.

And that’s the way it is.

You trade the market you have, not the one you want. But what do I know? I’ve only been doing this for 55 years.

I just thought you’d like to know.

NVIDIA Quarterly Earnings

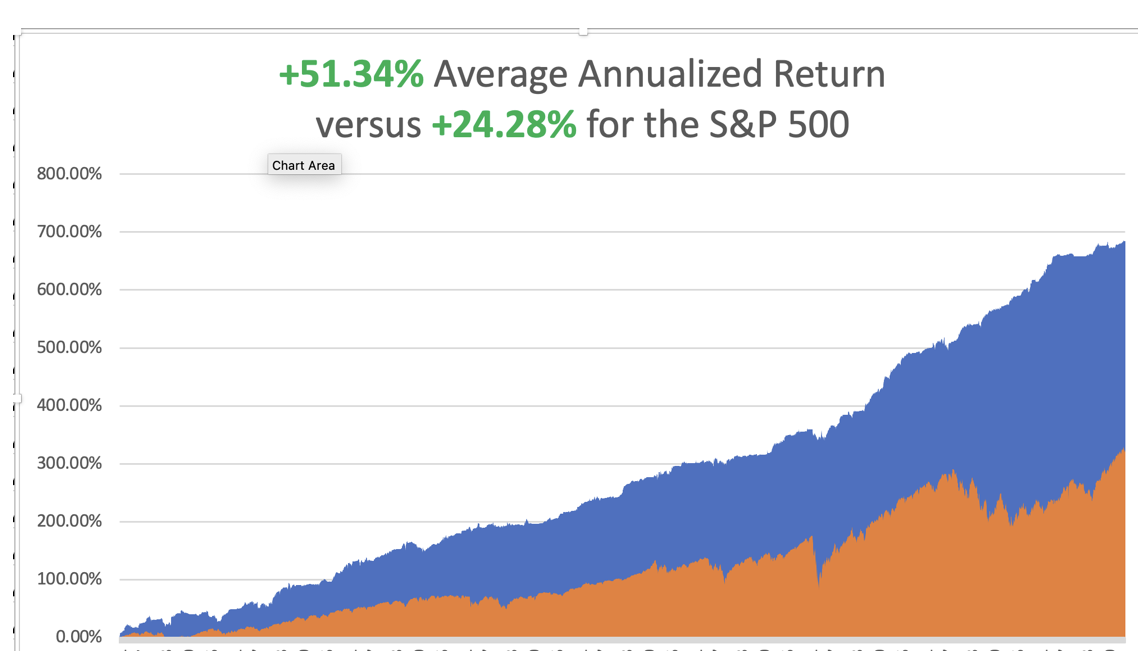

So far in March, we are down -1.44%. My 2024 year-to-date performance is at +6.67%. The S&P 500 (SPY) is up +7.93% so far in 2024. My trailing one-year return reached +41.09% versus +38.92% for the S&P 500.

That brings my 16-year total return to +684.56%. My average annualized return has recovered to +51.57%.

Some 63 of my 70 round trips were profitable in 2023. Some 13 of 19 trades have been profitable so far in 2024.

I stopped out of my short position in Freeport McMoRan (FCX) last week. Markets that go straight up are hard to trade. I also came off my long in (TLT) close to cost. I initiated new longs in Tesla (TSLA) and NVIDIA (NVDA). I let my existing longs run in Freeport McMoRan (FCX), Occidental Petroleum, ExxonMobile (XOM), Wheaton Precious Metals (WPM), and Gold (GLD).

I am 70% invested and 30% in cash given the massive upside breakout in commodity, precious metals, and energy we have witnessed.

Nonfarm Payroll Jumps by 303,000 in March, almost double what was expected. The headline unemployment rate drops 0.1% to 3.8%. Wages rose 0.3% for the month and 4.1% from a year ago, both in line with Wall Street estimates. Health care led with 72,000 new jobs, followed by government (71,000), leisure and hospitality (49,000), and construction (39,000). Interest rate cuts fade into the future.

Weekly Jobless Claims Jump to 221,000, up 9,000, a two-month high. The weekly claims report from the Labor Department on Thursday also showed fewer people remaining on jobless rolls towards the end of March, suggesting that laid-off workers continued to find work, though not as easily as two years ago. There were 1.36 job openings for every unemployed person in February compared to 1.43 in January. Worker shortages persist in industries like construction.

Investors are Piling into Cash, with Money-Market funds getting $82 billion in the week through Wednesday. Investors are still flocking to cash funds, and history suggests redemptions won’t begin until a year after the Federal Reserve starts cutting interest. 5.35% for 90-day US Treasury Bond yields are still a huge draw for the cautious.

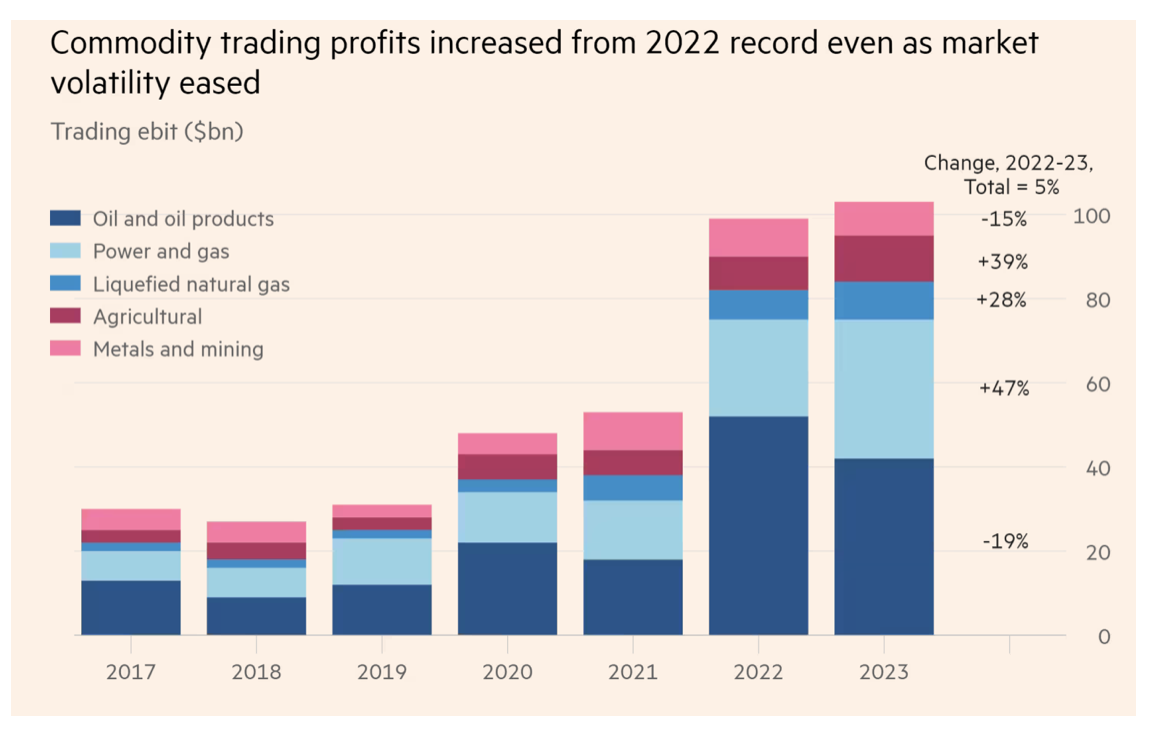

Commodities Trading Firms Harvest Record Profits, some $104 billion in 2023. The surprise increase from 2022, when the fallout from the war in Ukraine pushed up prices and supercharged profits, was driven by a wave of new entrants into the sector — including tech-focused traders and hedge funds — and rising returns from power trading activities. The figures reflect profits from the entire sector, including independent traders, banks, hedge funds, and national oil companies. This year will be even better.

Oil Continues to Bubble of Tight Supplies, supported by geopolitical tensions in the Middle East, concerns over tightening supply, and expectations about demand growth as economies improve. I’m keeping my longs in (XOM) and (OXY) and looking to pick up (COP) and (FANG).

US Dollar to Stay Higher for Longer, as a result of the higher for longer Fed tilt on interest rates. High-yielding currencies are always the strongest. The buck is up 3.3% this year against a currency basket.

Toyota Sales Soar by 20% in Q1, closely followed by Honda at 17.3%. General Motors delivered a pitiful 1.5% decline. Hybrids are the name of the day, outselling EVs and ICE cars. Toyota played it safe and won, at least for now.

Disney Wins Proxy Fight with Nelson Peltz, retaining complete control of the board. It’s a defeat for Peltz and a stamp of approval for the company’s board and CEO Bob Iger’s efforts to turn around the company. Nelson can now sell his shares for a big profit, up 30%.

PCE Comes in Hot at 0.3% for February, and 2.8% YOY, taking bonds. Personal Consumption Expenditures give an early read on inflation trends that the Fed loves. The economy is clearly much hotter than traders understand. Consumer spending shot up 0.8% on the month, well ahead of the 0.5% estimate. Personal income increased 0.3%, slightly softer than the 0.4% estimate.

Tesla Sales are Disastrous as expected, coming in at only 386,810, down 8.5% YOY. Shares drop as much as 6.7%, extending the biggest rout in the S&P 500. Analysts slashed projections in recent days, but not by enough. The Berlin factory was shut down and competition in China is ramping up. Still, Tesla produced 46,561 more cars than it sold in the quarter. For what it’s worth, BYD sales in China were even worse. The bottom for (TSLA) is fast approaching.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 8, at 7:00 AM EST, the US Consumer Inflations Expectations are announced.

On Tuesday, April 9 at 8:30 AM, the NFIB Business Optimism Index will be released.

On Wednesday, April 10 at 11:00 AM, the Core Inflation Rate for March is published

On Thursday, April 11 at 8:30 AM, the Weekly Jobless Claims are announced. The final read of the Q2 US GDP is also out.

On Friday, April 12 at 8:30 AM, the Producer Price Index is out. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, since many of you are now planning long overdue summer vacations, I thought I would pass on what I learned from the ultimate travel guru of all time.

After all, who knows how long it will be until the next pandemic? The next decade, next year, or next week?

When I backpacked around Europe in 1968, I relied heavily on Arthur Frommer’s legendary paperback guide, Europe on $5 a Day, which then boasted a cult-like following among impoverished, but adventurous Americans. The charter airline business was then booming, plunging airfares, and suddenly Europe came within reach of ordinary Americans like me.

Over the following years, he directed me down cobblestoned alleyways, dubious foreign neighborhoods, and sometimes converted WWII air raid shelters, to find those incredible travel deals. When he passed through town some 50 years later, I jumped at the chance to chat with the ever-cheerful worshipped travel guru.

Frommer believes there are three sea change trends going on in the travel industry today. Business is moving away from the big three travel websites, Travelocity, Orbitz, and Priceline, who have more preferential lucrative but self-enriching side deals with airlines than can be counted, towards pure aggregator sites that almost always offer cheaper fares, like Kayak.com, Sidestep.com, and Fairchase.com.

There is a move away from traditional 48-person escorted bus tours towards small group adventures, like those offered by Gap Adventures, Intrepid Tours, and Adventure Center, that take parties of 12 or less on culturally eye-opening public transportation.

There has also been a huge surge in programs offered by universities that turn travelers into students for a week to study the liberal arts at Oxford, Cambridge, and UC Berkeley. His favorite was the Great Books program offered by St. John’s University in Santa Fe, New Mexico.

Frommer says that the Internet has given a huge boost to international travel, but warns against user-generated content, 70% of which is bogus, posted by the hotels and restaurants touting themselves.

The 94-year-old Frommer turned an army posting in Berlin in 1952 into a travel empire that publishes 340 books a year, or one out of every four travel books on the market. I met him on a swing through the San Francisco Bay Area (his ticket from New York was only $150), and he graciously signed my tattered, dog-eared original 1968 copy of his opus, which I still have.

Which country has changed the most in his 60 years of travel writing? France, where the citizenry has become noticeably more civil since losing WWII. Bali is the only place where you can still actually travel for $5/day, although you can see Honduras for $10/day. Always looking for a deal, Arthur’s next trip is to Chile, the only country in the world he has never visited.

With the advent of AI, Arthur has been met with an onslaught of new competition. Recently, Amazon (AMZN) has been flooded with hundreds of new travel books written entirely by algorithms. They have no human author who’s ever visited the country in question and are written entirely from existing information found on the Internet. But they’re cheap.

You can easily spot them from their wishy-washy non-committal language and factual errors and omissions. For example, I recently found a travel book about Ukraine that neglected to mention that there was a war going on there and that its cities were being bombed by Russians daily.

Not for me.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Arthur’s Next Big Play is Bali

1968 on the French Riviera