In the biotechnology and healthcare industry, reaching a $1 trillion market cap is akin to scaling Mount Everest without oxygen. Yet, Eli Lilly (LLY) has emerged as an unexpected contender, catching the investing world’s attention by not just climbing the mountain but being on the verge of planting its flag at the summit.

A year ago, if you'd whispered in my ear that Eli Lilly's stock was about to skyrocket nearly 140%, I might have choked on my coffee. But here we are, and the buzz isn't just about the rocket ride — it's whether Eli Lilly can be the first biopharma behemoth to hit the $1 trillion market cap. Wild, right?

So, what's cooking at Eli Lilly that's got everyone so revved up? Well, they've got a couple of aces up their sleeve.

Sure, they've been making waves with Verzenio for breast cancer and Jardiance for diabetes, but the real game-changer? Tirzepatide, sold under their brand name Mounjaro for type 2 diabetes and is now strutting the stage as Zepbound for weight loss. This isn't just any old drug; it's the blockbuster that's got everyone from Wall Street to Main Street talking.

But what makes tirzepatide so darn special? It's the first of its kind, a dual GLP-1/GIP agonist, making it a heavyweight champion in the fight against obesity. With sales already blasting past the $5 billion mark in record time, it's like watching a rocket take off without any signs of slowing down.

Now, I know what you're thinking. "But hey, aren't there other big fish in the sea?" Sure, Johnson & Johnson (JNJ), Pfizer (PFE), and Merck (MRK) are doing their thing, but next to Eli Lilly's recent performance, they're looking a bit like they're running in slow motion.

And while Novo Nordisk (NVO) has been gaining traction in the diabetes market with its own version of the treatment, Eli Lilly’s tirzepatide is in a league of its own. In fact, this drug is projected to become the top-selling treatment in history, with the potential to rake in sales north of $25 billion.

For context, AbbVie (ABBV) Humira had an annual record of $21.2 billion, and that’s already the recorded highest-selling therapy in history. But, the road to hitting these goals demands many more new indications.

That’s why it comes as no surprise that tirzepatide is eyeing a new target: metabolic dysfunction-associated steatohepatitis, or MASH for short. It's a fancy way of saying "a really bad liver problem," and it's a growing issue globally.

Beyond tirzepatide, Eli Lilly's expanding in a few other markets. Alzheimer's, for one, where their potential therapy, donanemab, is making waves and presents a potential competitor to Biogen’s (BIIB) Leqembi.

And let's not overlook their recent wins with cancer medicine Jaypirca and ulcerative colitis therapy Omvoh. It's like Eli Lilly's hitting bingo on every card.

With all these in mind, can Eli Lilly truly reach that $1 trillion valuation? With their current market cap already north of $715 billion, it looks like the company is ready to take home the title. Assuming a modest compound annual growth rate of about 7%, that trillion-dollar dream could become reality quicker than you can say "biopharma giant."

As investors, industry watchers, and, frankly, anyone with a pulse on the future of medicine keep their eyes glued to this unfolding story, the message is clear: Eli Lilly is not just about the numbers. It's about setting new benchmarks, pushing boundaries, and cashing in on cures in the most spectacular way possible.

So, if you're wondering where the smart money is heading in the biotechnology arena, following Eli Lilly's trail might just lead you to a treasure trove of opportunities. I suggest you buy the dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-27 12:00:152024-02-27 11:13:48Cashing In On Cures

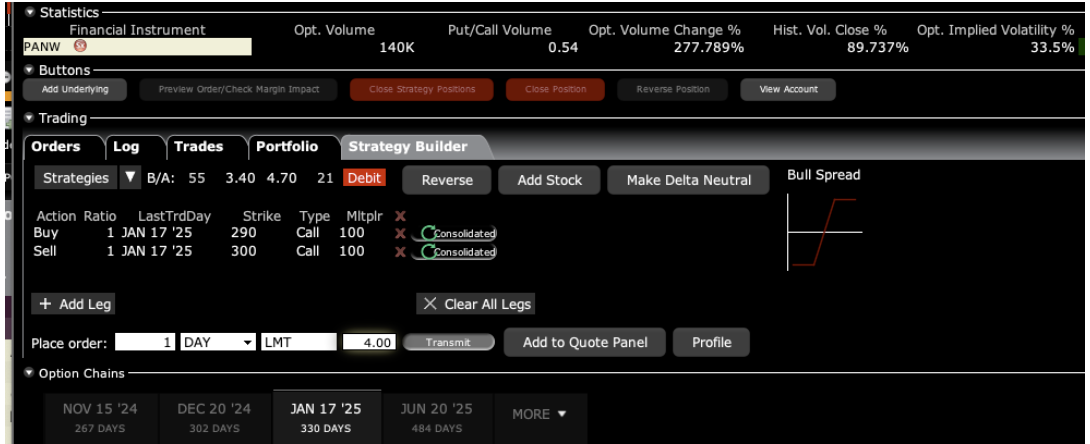

BUY the Palo Alto Networks (PANW) January 17, 2025 $290-$300 out-of-the-money vertical Bull Call spread LEAPS at $4.00 or best

Opening Trade

2-27-2024

expiration date: January 17, 2025

Number of Contracts = 1 contract

A 32% selloff in the (PANW) on disappointing guidance is the best entry point we are going to get for this LEAPS this year. Is hacking going out of style? I think not. If anything, it is going to get much worse, thanks to AI.

While the chance of winning a real lottery is something like a million to one, this one is more like 10:1 in your favor. And the payoff is 150% in a year. That is the probability that (PANW) shares will rise by only 9.90% over the next 11 months.

The logic behind this LEAPS is fairly simple.

After keeping interest rates too low for too long, and then raising them too far too fast, what does the Fed do next? It then lowers interest rates too far too fast. In other words, a mistake-prone Jay Powell will keep on making mistakes. That’s what you get with a Fed chair who only has a degree in political science.

I am using the very conservative $290-$300 strike price. (PANW) shares only need to return to where they were two days ago to hit the maximum profit point in this position, and they have 11 months to do it.

If that is not enough profit for you, perhaps you should consider another line of business.

I am therefore buyingthe Palo Alto Networks (PANW) January 17, 2025 $290-$300 out-of-the-money vertical Bull Call spread LEAPS at $4.00 or best.

Don’t pay more than $5.00 or you’ll be chasing on a risk/reward basis.

I am going out to only a January 17, 2025 expiration because I think this trade will work fairly quickly. Please note that these options are illiquid, and it may take some work to get in or out. Executing these trades is more an art than a science.

Let’s say the Palo Alto Networks (PANW) January 17, 2025 $290-$300 out-of-the-money vertical Bull Call spread LEAPS are showing a bid/offer spread of $3.80-$4.20, which is typical. Enter an order for one contract at $3.80, another for $3.90, another for $4.00, and so on. Eventually you will enter a price that gets filled immediately. That is the real price. Then enter an order for your full position at that real price.

A lot of people ask me about the appropriate size. Remember, if the (PANW) does NOT rise by 9.90% in 11 months, the value of your investment goes to zero. The way to play is to use a venture capital approach and buy LEAPS in ten different companies. If one out of ten increases ten times, you break even. If two of ten work you double your money, and if only three of ten work you triple your money.

You never should have a position that is so big that you can’t sleep at night, or worse, need to call John Thomas asking if you should sell at a market bottom. Please also note that I don’t follow LEAPS prices on a daily basis. I tend to buy them and forget about them. So if the stock suddenly doubles, which is possible, I WILL NOT send out a trade alert to take profits. That is up to you.

There is another way to cash in. Let’s say we get half of your double in the next three months, which from these low levels is entirely possible. Then you could earn half of the maximum potential profit in months. You can decide whether to keep the threefold return or go for the full 1 ½ bagger. It’s a nice problem to have.

Notice that the day-to-day volatility of LEAPS prices is miniscule since the time value is so great, usually sporting implieds of less than 10%. This means that the day-to-day moves in your P&L will be small. It also means you can buy your position over the course of a month just entering new orders every day. I know this can be tedious but getting screwed by overpaying for a position is even more tedious.

Look at the math below and you will see that a 9.90% rise in (PANW) shares will generate a 150% profit with this position, such is the wonder of LEAPS. That gives you an implied leverage of 15.5:1 across the $290-$300 space.

Only use a limit order. DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES. Just enter a limit order and work it.

This is a bet that (PANW) will not fall below $300 by the January 17, 2025 option expiration in 11 months.

Here are the specific trades you need to execute this position:

Buy 1 January 2025 (PANW) $290 calls at………….…….$40.00

Sell short 1 January 2025 (PANW) $300 calls at…..……$36.00

Net Cost:………………………….………..…….........……...….....$4.00 Potential Profit: $10.00 - $4.00 = $6.00

(1 X 100 X $6.00) = $600 or 150% in 11 months.

To see how to enter this trade in your online platform, please look at the order ticket below, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Debit Spread”by clicking here.

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep-in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

“Those who expect double digit returns going forwards are going to be severely disappointed,” said Bill Gross, CEO of bond giant, PIMCO.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Baby.jpg175216Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-02-27 09:00:162024-02-27 09:50:59February 27, 2024 - Quote of the Day

The Amazon of Latin America is a stock that has done well this year, but that doesn’t mean the party is over.

Like many other tech stocks this year, they have performed exceptionally strong in the past year and MercadoLibre (MELI) is no different.

The stock has returned 42% in the past year and the 13% dip from the most recent earnings report has presented an appetizing entry point.

The Amazon of Latin America fell the most in nearly two years after posting fourth-quarter earnings that fell short of analyst estimates, hoisting a major hurdle to the major stock rally over the past year.

Shares slumped 13% Friday, the worst intraday drop since May 2022, after the company reported earnings per share of $3.25 — about half of the $7.17 analysts had forecast. It was the first miss since at least mid-2022.

The lower number, which was boiled down to one-off costs and higher logistics left a sour taste in the mouth of MELI investors.

MercadoLibre's revenue growth over the last three years has been in overdrive, averaging 56.8% annually.

This quarter, MELI registered an impressive 41.9% year-on-year revenue growth.

Usage Growth As an online marketplace, MercadoLibre generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, MercadoLibre's daily active users, a key performance metric for the company, grew 24.6% annually to 145 million. This is fast growth for a consumer internet company.

In Q4, MercadoLibre added 48 million daily active users, translating into 49.5% year-on-year growth.

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like MercadoLibre because it measures how much the company earns in transaction fees from each user.

Furthermore, ARPU gives us unique insights as it's a function of a user's average order size and MercadoLibre's take rate, or "cut", on each order.

MercadoLibre's ARPU growth has been excellent over the last two years, averaging 16.8%. The company's ability to increase prices while growing its daily active users at such a fast rate reflects the strength of its platform, as its users are spending significantly more than last year. This quarter, ARPU declined 5% year on year to $29.39 per user.

It posted full-year net revenue of around $14.5 billion and net income of $1.2 billion for the year. Revenue and payment volumes beat expectations for the last three months of 2023.

Naturally, buyers and sellers gravitate towards a singular marketplace, consolidating the dominion of Amazon and Mercado Libre while marginalizing smaller retailers.

This monopolistic stranglehold, compounded by the excessive capital investments requisite for technological infrastructure, inventory management, and advertising, perpetuates a vicious cycle of exclusion and inequality, relegating smaller players to the fringes of the digital marketplace.

MELI is part of this duopoly in South America and I see any big dips as good buying opportunities.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-26 17:58:092024-02-26 18:08:08Check Out the Amazon of Latin America

Investing in AI feels a bit like trying to sip from a firehose – overwhelming, to say the least. The landscape is teeming with contenders, from savvy businesses harnessing AI to sharpen their edge, to the wizards creating the software that's the lifeblood of AI.

But let’s not forget the unsung heroes: the hardware components. These are the bread and butter of AI, and companies like NVIDIA (NVDA), Advanced Micro Devices (AMD), Super Micro Computer (SMCI), and Taiwan Semiconductor (TSM) are the rock stars on this stage.

Yet, there's a titan in the shadows, poised for a spotlight moment: ASML Holding (ASML).

Imagine every AI model as a gourmet dish, and at the heart of each, there’s a microchip – the secret sauce. Crafting these chips requires machinery so advanced it might as well be from the future, and ASML is the master behind it.

Known as EUV (extreme ultraviolet), ASML holds the technology behind powerful lithography machines that sketch the delicate, conductive traces on chips.

We're talking about a finesse so fine that these traces are now as narrow as 3 nanometers. To put that into perspective, a strand of human hair is a hulking 80,000 nanometers in comparison.

Here's why it's a big deal.

First off, let's get to grips with what EUV is all about. Imagine trying to paint the Mona Lisa on a grain of rice. Sounds impossible, right? That's what microchip manufacturers were up against, trying to fit more and more transistors onto a chip to power the brain of AI systems.

Enter EUV technology. It's like swapping out a bulky paintbrush for a laser-precise pen, allowing for incredibly detailed patterns on microchips.

This means more power, speed, and efficiency for AI technologies, from autonomous cars to smart appliances.

In essence, EUV is making the impossible possible, allowing chips to get smaller, faster, and smarter.

Now, why should you care? Because EUV technology is the golden ticket in the semiconductor industry. It's what's going to fuel the next wave of AI advancements.

As AI technologies become more integrated into our lives, the demand for these super-powered chips is going to skyrocket.

So, where does ASML fit into this picture?

Well, ASML is the only show in town when it comes to EUV lithography systems. They've got a monopoly on this game-changing tech.

As AI continues to grow, so does the need for what ASML provides. It's like owning the only factory that makes the secret sauce everyone needs. And with the semiconductor industry being as competitive as it is, having that kind of edge is invaluable.

Their status as a lone wolf in this arena justifies their revenue guidance of $32.4 billion to $43.2 billion by 2025, coupled with a gross margin that's as impressive as their tech.

Thanks to the advent of AI, the semiconductor industry is on the brink of a gold rush, with analysts forecasting a boom of 42 new fabrication plants in 2024 alone.

This is a significant leap from the past, signaling a rebound in spending on the very semiconductor manufacturing equipment that ASML specializes in.

After a slight dip in 2023, spending is expected to skyrocket to $124 billion by 2025.

ASML, riding this wave, has already seen its order books bulge with bookings worth $9.936 billion in just the last quarter of 2023.

This puts ASML in an enviable position, with a backlog that's more robust than its revenue forecast for the year.

The company, which reported revenues of $29.81 billion in 2023, is eyeing a repeat performance in 2024, with sights set on even greater growth fueled by this semiconductor spree.

What's the bottom line for ASML? This company is projected to report a significant earnings leap from 2025, driven by improved market conditions and a backlog that's the envy of the industry.

With predictions pointing towards earnings of $36 per share in 2026 and a potential stock price surge to $1,260, ASML represents a golden opportunity for investors looking to tap into the semiconductor industry's growth without paying the premium prices commanded by others like Nvidia. I suggest you buy the dip.

Midjourney prompt:"The Fine Line of the Future"

https://www.madhedgefundtrader.com/wp-content/uploads/2024/02/Screenshot-2024-02-26-153138.jpg8771329Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2024-02-26 15:27:522024-02-26 15:41:44THE FINE LINE OF THE FUTURE

(VOLATILITY LIKELY IN THE NEXT TWO WEEKS AFTER CHINESE NEW YEAR ENDS)

February 26, 2024

Hello everyone,

We are in the final week of February.Corporate earnings are winding down.But there will be plenty of economic data being released this week to keep us on our toes.One to watch will be the January personal consumption expenditure report after the consumer price and producer price reports earlier this month came in hotter than expected.

Week ahead calendar

Monday, February 26, 2024

8 a.m. Building Permits final (January)

10 a.m. New Home Sales (January)

10:30 a.m. Dallas Fed Index (February)

Japan Inflation Rate

Previous:2.6%

Time:6:30 pm ET

Earnings:Fidelity National Information Services, Domino’s Pizza

Tuesday, February 27, 2024

8:30 a.m. Durable Orders (January)

9 a.m. FHFA Home Price Index (December)

9 a.m. S&P/Case -Shiller comp.20 HPI (December)

10 a.m. Consumer Confidence (February)

10 a.m. Ri9chmond Fed Index (February)

Earnings:eBay, First Solar, ExtraSpace Storage, Axon Enterprise, Norwegian Cruise, Line Holdings, J.M. Smucker, AutoZone, Lowe’s

Wednesday, February 28, 2024

8:30 a.m. GDP Chain Price second preliminary (Q4)

8:30 a.m. Wholesale Inventories SA preliminary (January)

1:45 p.m. New York Federal Reserve Bank President and CEO John Williams keynote remarks in an event LIA Regional Economic Briefing, New York.

8:30 a.m. Personal Consumption Expenditure (January)

8:30 a.m. Personal Income (January)

9:45 a.m. Chicago PMI (February)

10 a.m. Pending Home Sales Index (January)

11 a.m. Kansas City Fed Manufacturing Index (February)

8:10 p.m. New York Federal Reserve Bank President and CEO John Williams moderated a discussion in an event at Citizens Budget Commission 92nd Annual Gala, New York.

Earnings:Hewlett Packard Enterprise, Autodesk, Best Buy, Bath & Body Works,

Hormel Foods.

Friday, March 1, 2024

9:45 a.m. Markit PMI Manufacturing final (February)

10 a.m. Construction Spending (January)

10 a.m. ISM Manufacturing (February)

10 a.m. Michigan Sentiment final (February)

Euro Area Inflation Rate

Previous: 2.8%

Time: 5:00 am ET

Prediction:

Over the next two weeks volatility returns to the market.

VIX- should break out to the upside.

Markets should correct to the downside.

Crude oil may rise as markets correct.

Bitcoin continues to rise.

Nasdaq- We reached 18,000 and capitulation hit.A reasonable possibility is for tech to fall toward the 200-day MA at around 16,000.First targets are 17,501, and then 16,678.

The U.S.$ will continue to rise for a while – the yen will weaken, and the Euro will fall.

As the U.S.$ goes up Gold will have one more downside push.This is the time to accumulate your one- and two-year out of the money LEAPS in Gold and Silver stocks and even Platinum. Keep averaging in.Gold could fall towards the 1960 -1952 target area.

The peak is coming in the U.S.$.Then we will go to long currencies.

Home Depot and Walmart are stocks to watch as they will show how much disposable income people have in the U.S.If we see data showing less disposable income it will be an early sign of things to come a year from now.Visa and Mastercard are also worth watching.

Warren Buffett’s annual letter has been released.The first without his long-time partner, Charlie Munger, who passed away last November at the age of 99.

Here are three takeaways from that letter to his shareholders.

1/ Quality

“We want to own either all or a portion of businesses that enjoy good economics that are fundamental and enduring.

Always buy low.

Some of Buffett’s portfolio stocks include Apple, Bank of America, Coca-Cola, and Chevron.

2/ Invest long

“When you find a truly wonderful business, stick with it.Patience pays, and one wonderful business can offset the many mediocre decisions that are inevitable.”

3/ The bigger picture

Buffett’s flagship business, the freight rail giant BNSF is facing earnings headwind, a crunch in margins, and rising costs.

“Rail is essential to America’s economic future.It is clearly the most efficient way – measured by cost, fuel usage, and carbon intensity – of moving heavy materials to distant destinations.Trucking wins for short hauls, but many goods that Americans need must travel to customers many hundreds or even several thousand miles away.

Buffett notes that “a century from now BNSF will continue to be a major asset of the country and Berkshire.”

People will be sitting around campfires trading stories about last week’s NVIDIA move for decades.

Analysts have been struggling to outdo each other in describing their earnings report that came out on Thursday. Here’s my favorite: The gain in the company’s market capitalization on that day, at $278 billion the largest in history, exceeded its TOTAL market capitalization at the pandemic bottom.

And here I deserve some bragging rights. Mad Hedge followers went into last week’s melt-up, UP TO THEIR EYEBALLS in (NVDA). They owned the stock, call options, and call spreads. The LEAPS alone delivered a 12X return, and some readers who customize their own strike prices (the $295-$300s) received a 50X return. It was almost everyone’s largest position.

It was easy for me to do the NVIDIA trade. When the company launched its first high-end graphics card in 1993, every computer geek out there flocked to them. I used to tear apart my company’s PCs, throw out the graphics cards they came with, and install NVIDIA cards. The performance improvement was remarkable, especially for advanced mathematical calculations.

The company is blessed. It went public at $12 a share just before the Dotcom Bust and the IPO window closed for years. Adjusted for 12:1 splits over the years and that drops the original IPO price to $1. A dollar invested in 1999 would be worth $750 at last week’s high. NVIDIA’s CEO, Jensen Huang, is now one of the richest men in the world solely through the ownership of his NVIDIA shares.

God Bless America!

Also last week, my inbox was jammed with inquiries on what company will become the next NVIDIA. And here is the bad news. There aren’t any 750:1 returns anywhere on the horizon. There are not even any 175:1 opportunities that we earned from Tesla (TSLA) over the years either where we also had heavy exposure.

And the reason is very simple. You are not going to get the entry points today with the Dow Average at 39,000 that you got in 2009 when it was at only 6,000, or when it was at a mere 600 when I joined Morgan Stanley in 1982. The last decent entry point for (NVDA) was the $100 pandemic low in April 2020.

Want to own the next (NVDA)? Try buying (NVDA), where an analyst raised his target to $1,420, up 80% from the Friday close. It’s just a matter of time before its market cap jumps from $2 trillion to $3 trillion, making it the largest company in the world. That’s what an airtight monopoly in the world’s most valuable product gets you.

Technology earnings are now exploding at such a rapid pace that it is time to consider the unthinkable: What if stocks don’t need interest rate cuts for the bull market to continue? After all, the companies seem to be doing just fine without any such assistance.

Why try to fix what isn’t broken?

In fact, these large cash flow companies would take a hit on their income statements as they are already net creditors to the financial system. Apple (AAPL) alone would lose $8 billion in annual income if interest rates went back to zero.

While that may be true for the Magnificent Seven or the AI Five, it is not true for the Unimagnificent 493. They actually need cheaper money for their stock prices to get going or even just to survive. That is especially true for all the falling interest rate plays, like bonds, utilities, real estate, precious metals, energy, and foreign currencies.

And don’t even talk to me about small caps, which depend on low interest rates for the breath of life.

It says a lot that Warren Buffet believes there is nothing left to buy in his annual letter to shareholders, an early Mad Hedge subscriber. His spectacular annual compounded returns of 19.8% a year, more than double that of the S&P 500 (SPY), are now a thing of the past.

The few targets left out there are few and far between and heavily picked over. (BRK/B) has also lost the advice of its principal mentor, Charlie Munger at the ripe old age of 99. Last year Berkshire acquired Dairy Queen and Berkshire Energy. But at $905 billion in assets under management, those will hardly move the needle. The 93-year-old Buffet has outperformed the S&P 500 by 141:1 since 1964.

Who says age is an impediment?

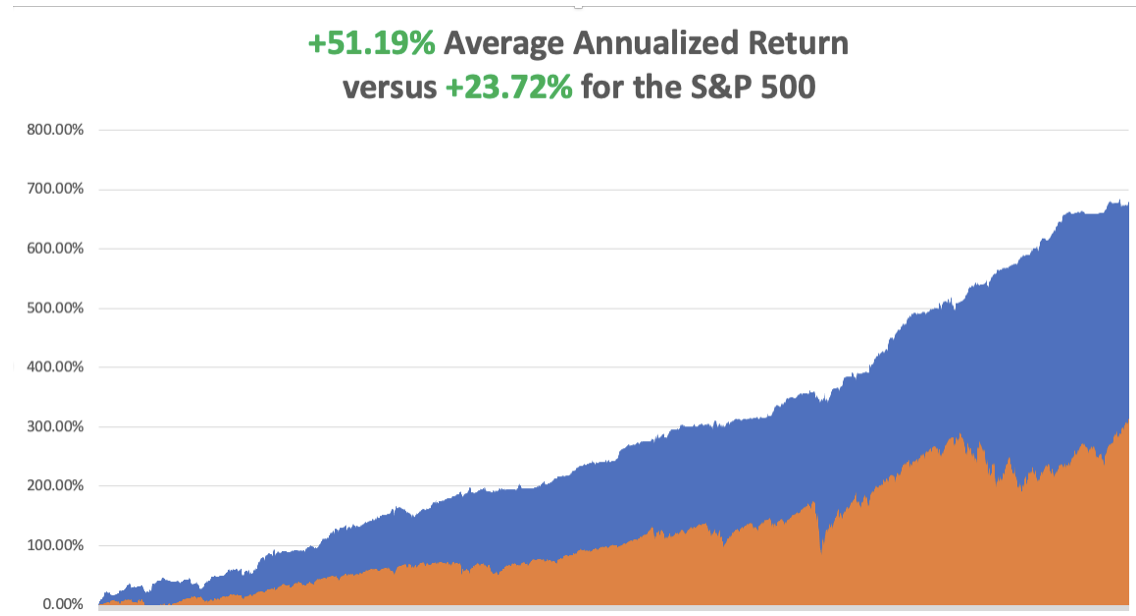

So far in February, we are up +5.92%. My 2024 year-to-date performance is also at +1.64%.The S&P 500 (SPY) is up +6.50%so far in 2024. My trailing one-year return reached +57.73% versus +38.67%for the S&P 500.

That brings my 15-year total return to +678.27%. My average annualized return has recovered to +51.19%,another new high.

Some 63 of my 70 trades last year were profitable in 2023.

I used the ballistic move-in (NVDA) to take profits in my double long there. I am maintaining a single long (AMZN) and am 90% in cash given the elevated level of the markets.

NVIDIA Announces Blowout Earnings, with AI reaching the “tipping point” according to the CEO Jensen Huang. Revenues came in at a spectacular $22.1 billion versus an expected $20.6 billion off the backing of exploding data center demand, up 33%. Earnings were up 22% QOQ and 225% YOY. The shares exploded $100 in the aftermarket at one point, up 15.6%. Forward guidance was ramped up too. Buy NVDA on dips. At a PE multiple of 18X, it is the cheapest AI stock out there.

Mad Hedge Clocks Biggest One Day Gain in 16 Years, with a double weighting in NVIDIA (NVDA), up +6.072%. If you like that the Mad Hedge Technology Letter is doing even better, up +13% YTD. And we are still early days into the tech melt-up, which could go on for another decade. Our YOY gain is up +59.62%. The harder I work, the luckier I get.

Existing Home Sales Jumped 3% YOY, boosted by lower mortgage interest rates in November and December. Inventories of homes for sale in January increased to 1.01 million units, up 3.1% from January 2023, but still at a low 3-month supply. The median existing home price for all housing types in January was $379,100, up 5.1% from a year earlier and an all-time high for the month of January.

Weekly Jobless Claims Dropped to a one-month low, down 12,000 to 201,000. No recession here. California and Kentucky saw the largest declines.

China Bans Stock Selling, by institutional investors at market openings and closes when liquidity is the greatest. It’s part of the government’s most forceful attempt yet to prop up the nation’s $8.6 trillion stock market. It’s another sign of a weakening China. When restrictions are placed on markets, capital flees. Whoever thought of this one must have a hole in their head. Avoid (FXI).

California demolishes Solar Providers, cutting the price the utility PG&E has to pay for home power providers by 75%. Solar companies like SunPower (SPWR), are down 89% since last year. Avoid solar providers for now, which was always a low value-added business.

Amazon (AMZN) is getting added to the Dow Average, opening it up to massive index buying. Retailer Walgreens Boots Alliance (WBA) is getting bumped. Since 1896, the blue-chip index has made few changes to its 30-stock lineup, having altered its constituents about 60 times in its 128-year history. Buy (AMZN) on dips.

US Stocks now account for 70% of Global Stock Market Capitalization, thanks to the ballistic moves in big tech. This level represents the largest country weighting since I helped create this index way back in 1986. It also now has the lowest exposure to non-US stocks. Money is pouring into the US from all corners of the world, the planet's most successful economy.

Natural Gas Hits (UNG) Three Year Low, at $1.63MM BTU, and down an eye-popping 50% in a month. Warm weather, high inventories, and overproduction due to cheap capital are the price killers. An LNG train broke down, cutting export demand. If you didn’t get out on the double in December you’re toast. Avoid (UNG).

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, February 26, the New Home Sales are announced.

On Tuesday, February 27 at 8:30 AM EST,the Durable Goods are released. The S&P Case Shiller for December is announced.

On Wednesday, February 28 at 2:00 PM, the Q2 GDP second readis published.

On Thursday, February 29 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Core Consumer Price Expectations.

On Friday, March 1 at 2:30 PM, the December ISM Manufacturing PMI is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, the telephone call went out amongst the family with lightning speed, and this was back in 1962 when long-distance cost a fortune. President Dwight D. Eisenhower was going to visit my grandfather’s cactus garden in Indio the next day, said to be the largest in the country, and family members were invited.

I spent much of my childhood in the 1950s and 1960s helping grandpa look for rare cactus in California’s lower Colorado Desert, where General Patton trained before invading Africa. That involved a lot of digging out a GM pickup truck from deep sand in the remorseless heat. SUVs hadn’t been invented yet, and a Willys Jeep (click here) was the only four-wheel drive then available in the US.

I have met nine of the last 13 presidents, but Eisenhower was my favorite. He certainly made an impression on me as a ten-year-old boy, who I remember as a kindly old man.

I walked with Eisenhower and my grandfather plant by plant, me giving him the Latin name for its genus and species and citing unique characteristics and uses by the Indians. The former president showed great interest and in two hours we covered the entire garden. I still make my kids learn the Latin names of plants.

Eisenhower lived on a remote farm at the famous Gettysburg, PA battlefield given to him by a grateful nation. But the winters there were harsh, so he often visited the Palm Springs mansion of TV Guide publisher Walter Annenberg, a major campaign donor.

Eisenhower was a one-of-a-kind brilliant man that America always came up with when it needed them the most. He learned the ropes serving as Douglas MacArthur’s Chief of Staff during the 1930’s. Franklin Roosevelt picked him out of 100 possible generals to head the Allied invasion of Europe, even though he had no combat experience.

After the war, both the Democratic and Republican parties recruited him as a candidate for the 1952 election. The latter prevailed, and “Ike” served two terms, defeating the governor of Illinois Adlai Stevenson twice. During his time, he ended the Korean War, started the battle over civil rights at Little Rock, began the Interstate Highway System, and admitted Hawaii as the 50th state.

As my dad was very senior in the Republican Party in Southern California during the 1950s, I got to meet many of the bigwigs of the day. New York prosecutor Thomas Dewy ran for president twice, against Roosevelt and Truman, and was a cold fish and aloof. Barry Goldwater was friends with everyone and a decorated bomber pilot during the war.

Richard Nixon would do anything to get ahead, and it was said that even his friends despised him. He let the Vietnam War drag out five years too long when it was clear we were leaving. Some 21 guys I went to high school with died in Vietnam during this time. I missed Kennedy and Johnson. Wrong party and they died too soon. Ford was a decent man and I even went to church with him once, but the Nixon pardon ended his political future.

Peanut farmer Carter was characterized as an idealistic wimp. But the last time I checked, the Navy didn’t hire wimps as nuclear submarine commanders. He did offer to appoint me Deputy Assistant Secretary of the Treasury for International Affairs, but I turned him down because I thought the $15,000 salary was too low. There were not a lot of Japanese-speaking experts on the Japanese steel industry around in those days. Biggest mistake I ever made.

Ronald Reagan’s economic policies drove me nuts and led to today’s giant deficits, which was a big deal if you worked for The Economist. But he always had a clever dirty joke at hand which he delivered to great effect….always off camera. The tough guy Reagan you saw on TV was all acting. His big accomplishment was not to drop the ball when it was handed to him to end the Cold War.

I saw quite a lot of George Bush, Sr. whom I met with my Medal of Honor Uncle Mitch Paige at WWII anniversaries, who was a gentleman and fellow pilot. Clinton was definitely a “good old boy” from Arkansas, a glad-hander, and an incredible campaigner, but he was also a Rhodes Scholar. His networking skills were incredible. George Bush, Jr. I missed as he never came to California. And 22 years later we are still fighting in the Middle East.

Obama was a very smart man and his wife Michelle even smarter. Stocks went up 400% on his watch and Mad Hedge Fund Trader prospered mightily. But I thought a black president of the United States was 50 years early. How wrong was I. Trump I already knew too much about from when I was a New York banker.

As for Biden, I have no opinion. I never met the man. He lives on the other side of the country. When I covered the Senate for The Economist, he was a junior member.

Still, it’s pretty amazing that I met 10 out of the last 14 presidents. That’s 20% of all the presidents since George Washington. I bet only a handful of people have done that, and the rest all live in Washington DC. And I’m a nobody, just an ordinary guy.

It just makes you think about the possibilities.

Really.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Long Road

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/john-thomas-white-house.jpg500665april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-26 09:02:552024-02-26 10:54:29The Market Outlook for the Week Ahead, or Who Needs Rate Cuts?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.